Hydraulic Workover Unit Market Size, Share & Industry Analysis, By Service (Workover and Snubbing), By Capacity (Below 150 Tons, 151-200 Tons, and Above 200 Tons), By Installation (Skid-Mounted and Trailer-Mounted), By Application (Onshore and Offshore), and Regional Forecast, 2026-2034

Hydraulic Workover Unit Market Size

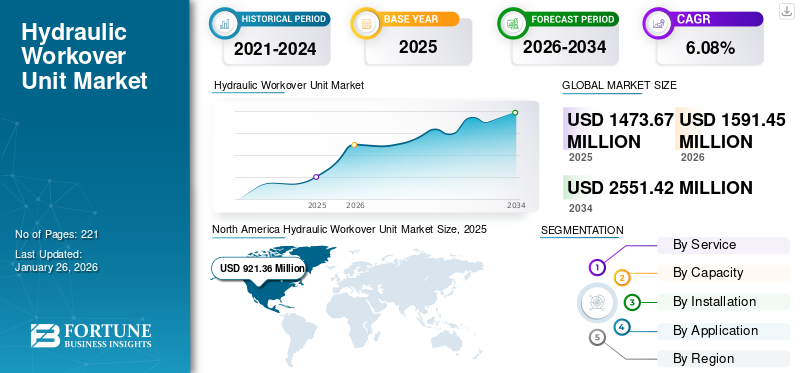

The global hydraulic workover unit market size was valued at USD 1,473.67 million in 2025 and is projected to grow from USD 1,591.45 million in 2026 to USD 2,551.42 million by 2034, exhibiting a CAGR of 6.08% during the forecast period. North America dominated the hydraulic workover unit market with a market share of 62.52% in 2025.

Hydraulic Workover Unit (HWU) is a specialized technique used in the oil and gas industry for the maintenance, repair, and intervention of oil and gas wells. It involves the use of these units and equipment manufactured to access the wellbore, perform various downhole operations, and optimize the well's performance without the need to drill a new well. Hydraulic workover operations can include tasks, such as pulling and running tubing, equipment replacement, well cleanouts, stimulation, and addressing well integrity issues. It is a cost-effective and flexible method for extending the productive life of wells and maximizing hydrocarbon recovery.

The impact of COVID-19 on the market has been notable due to disruptions in the oil and gas industry. However, the situation may have evolved since then. The pandemic led to a decrease in oil and gas demand, resulting in reduced drilling and well-maintenance activities. For instance, According to the U.S. Energy Information Administration, North Dakota crude oil production declined from an average of 1.5 million barrels per day (b/d) to 0.9 million b/d between December 2019 and May 2020, a decrease of more than 615,000 b/d (41.6%). This decline in production is greater than it would have been if producers had merely halted new wells and allowed production from current wells to decline naturally.

Download Free sample to learn more about this report.

Hydraulic Workover Unit Market Trends

Increasing Focus toward Brownfields to Propel Market Growth

A mature oil and gas field has exceeded peak production. These oil fields hold a large part of the global crude oil production. With advanced and improved technological approaches, such as Enhanced Oil Recovery (EOR), the production of mature oil fields has seen a significant increase. Increasing recovery from mature fields has required expansion of the well and enhancement in production through well intervention and work-up. As oil reserves declined, companies increasingly focused on developing equipment required to access the remaining reserves of mature wells. The main focus is on improving recovery and prolonging life. However, increased water incision with restricted topside facilities, increasing flow control issues, rising operating costs, and integrity issues due to mature facilities have resulted in brownfields being operationally and economically impractical. The rising demand for workover services is expected to fuel market growth over the forecast period.

Download Free sample to learn more about this report.

Hydraulic Workover Unit Market Growth Factors

Huge Investment in Offshore Oil and Gas Developments to Propel HWU Market

Huge Investment in offshore oil and gas developments to propel hydraulic workover unit market growth. Recently, there has been an amplified focus on reducing energy consumption in several industries, including building and construction. Heating consumes significant energy in the residential and commercial sectors. For instance, in its extraordinary session of 25th August 2022, the Spanish Parliament sanctioned a law that comprised actions to encourage energy efficiency and saving. In addition, the Russia-Ukraine crisis has shifted France's government's focus toward reducing energy consumption.

The aim is to reduce energy consumption by 10% by 2024. To accomplish this, an enterprise and work organization energy sobriety plan and a guide to decent practices for businesses are being drawn up. As well as the prime minister of France also called on all companies to make their energy efficiency plan in September 2022. These measures or laws might help fuel the demand for energy-efficient heating solutions workover units. These units are commonly used as heating systems in large-scale commercial and residential infrastructure. These units have the potential to maintain a preferred temperature by utilizing lower water temperatures, which saves energy.

RESTRAINING FACTORS

Increasing Focus Toward Promoting Clean Energy Solutions to Hamper Market Growth

There is a growing focus of many countries to reduce their carbon footprint and dependence on fossil fuels. The oil and gas sector has the potential to grow significantly after the global renewable investment. China, Europe and the U.S. are the top three markets for renewable investment. According to the MENA solar energy report, up to 37,000 MW of new solar, wind, and hydroelectric projects are planned to be commissioned worldwide. Solar Energy projects would specifically source about 12000-15000 MW. The IEA expects global energy investment to increase by over 8% in 2022 to a total of USD 2.4 trillion, well above pre-Corona levels. Investment is increasing in all parts of the energy sector. Still, the biggest impetus in recent years has come from the energy sector, particularly in renewables and grids and increased spending on end-use efficiency. The increasing share of electricity generation from renewable sources may hamper substantial investment in oil and gas. Also, the need to reduce carbon emissions has fueled the uptake of renewable energy, with government incentives being given across the globe. In addition, the growing demand of renewable energy in generating electricity with great benefits may lead to high acceptance of traditional fuels.

Hydraulic Workover Unit Market Segmentation Analysis

By Service Analysis

Workover Segment Holds a Dominant Share Owing to Its Application in Providing Optimization Activities and Better Performance

Based on service, the market is bifurcated into workover and snubbing.

The workover segment is projected to dominate the hydraulic workover unit market, reaching USD 1,115.39 million in 2026, accounting for 70.09% of the global market share. The workover segment dominated the market as the market focuses on interventions performed on oil and gas wells using hydraulic workover units. This market segment involves pulling the tubing and sometimes the casing out of the wellbore to access downhole equipment or perform maintenance, repairs, and optimization activities.

On the other hand, the snubbing segment of the market focuses on well interventions using snubbing units. Snubbing is a technique used to work on wells under pressure without the need to kill the well or remove the tubing from the wellbore. It's particularly valuable for addressing live wells or wells with high-pressure conditions.

By Capacity Analysis

Above 200 Tons Segment Leads the Market as It Can Handle the Weight of Various Components

Based on the capacity, the market is divided into below 150 tons, 151-200 tons, and above 200 tons.

The above 200-tonne segment is projected to reach a capacity of USD 907.26 million in 2026, accounting for a 57.01% share of the global market. This capacity includes lifting heavy components and equipment in and out of the well. A capacity of above 200 tons is particularly preferred as this ensures that these units can handle the weight of various components used in interventions, packer pumps, and other tools. Whether a shallow or deep well, a 200-ton offshore or onshore operation can meet this requirement.

The 150-200 ton segments holds the significant market share and it refers to the specific category or range of units designed to handle loads within that weight range.

Below 150 ton segment these units are dedicated to perform tasks such as wellbore cleaning, fishing, sidetracking etc. This segment also have a significant share in the market

To know how our report can help streamline your business, Speak to Analyst

By Installation Analysis

Skid-Mounted Segment Holds a Major Share Due to Various Benefits as They Can Be Assembled as a Modular Unit

The installation segment is of two types: skid-mounted and trailer-mounted.

The skid-mounted segment accounted for the majority of share in the global hydraulic workover units market owing to the tremendous benefits as skids are assembled as modular units, so skid-mounted process equipment can be more easily disassembled and reassembled when needed. Easier to install than a stick-build approach. Skid-mounted equipment is moved to the desired location and connected to existing machinery, often with single-point process connections. Skid-mounted systems provide additional safety, support, and protection for industrial equipment, often including complex piping, sensitive valves, and other valuable components. The skid-mounted type of installation is advantageous for onshore and offshore vessels as the demand for skid-mounted installation is greater. The skid-mounted segment accounting for 55.93% of the global market share.

The trailer mounted segment also holds a good market value in the industry and it refers to a specific category of units that are mounted on trailers for mobility and ease of transportation.

By Application Analysis

Onshore Segment Holds Major Share as It Can be Easily Installed and Cheaper Than Offshore Installations

Based on the application, the market is segmented into onshore and offshore.

The onshore segment is dominating the market as oil and gas industry is facing increasing demands to clarify the impact of the energy transition on its operations and business models and the contribution it can make to reducing greenhouse gas (GHG) emissions. The offshore segment also holds a significant share and it refers to a specific category of unit that are designed and optimized for use in oil and gas operations.

REGIONAL INSIGHTS

By region, the market has been studied and analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Hydraulic Workover Unit Market Size, 2025 (USD million)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed 62.52% to the global market in 2025, with a valuation of USD 921.36 million, and is projected to reach USD 1008.59 million in 2026. Due to increasing oil and gas production in North America, demand for raw materials is expected to increase during the forecast period. The number of new oil and gas fields being developed in North America for the use of hydraulic work units. The increased focus on brownfield projects and drilling activity in the Permian is resulting in steady growth that is slower than before. The U.S. market is projected to reach USD 696.20 million by 2026.

Middle East & Africa

The Middle East & Africa is the second largest region expanding the market. The market in Middle East & Africa reached USD 291.37 million in 2025, representing 19.77% of total market revenue, and is projected to reach USD 305.45 million in 2026. Saudi Arabia, UAE and Oman will continue to increase their drilling and production with a focus on developing gas assets for Saudi Arabia and UAE. The energy transition and CO2 capture are also receiving increasing interest in all three countries. World Oil expects regional drilling to increase by 16.8%. Regional oil production rose 10.8% to 27,465 MMbpd in 2022. The developing oil industries and drilling activities are driving the market.

Asia Pacific

In Asia Pacific, there is an emerging exploration activities that contribute to the significant growth. The Asia Pacific market was valued at USD 127.96 million in 2025, capturing 8.68% of global revenue, and is estimated to reach USD 137.64 million in 2026. The presence of established oil and gas companies impacts the whole market through their services. The Japan market is projected to reach USD 19.85 million by 2026. The China market is expected to reach USD 77.63 million by 2026, while the India market is anticipated to reach USD 22.26 million during the same year.

Europe

Europe accounted for USD 73.25 million in 2025, representing 4.97% of the global market share, and is projected to reach USD 77.37 million in 2026.

Latin America

In Latin America, due to offshore exploration activities and the development of projects, there is a high demand in the market. In 2025, the Latin America market stood at USD 59.74 million, representing 4.05% of global demand, and is projected to grow to USD 62.4 million in 2026.

Key Industry Players

Haliburton Dominates the Market Due to High Industry Demand and a Vast Product Portfolio

The global market is highly consolidated, with only a few players providing hydraulic workover units to various countries. Moreover, Halliburton dominated the hydraulic workover unit market as the company accounted for half of its market share. However, there are various other players actively operating across the globe to cater to the demand for hydraulic workover units across the industry.

LIST OF TOP HYDRAULIC WORKOVER UNIT COMPANIES:

- Halliburton (U.K.)

- Superior Energy Services (Netherlands)

- Joeny Holdings (Nigeria)

- EEST Energy Services Limited (Thailand)

- VELESTO ENERGY BERHAD (Malaysia)

- Noble GA Engineering & Services (Malaysia)

- Canadian Energy Equipment Manufacturing FZE (United Arab Emirates)

- ENEXD Group (Dubai)

- WellGear (Netherland)

- HANDAL ENERGY BERHAD (Malaysia)

- High Arctic Energy Services (Canada)

- Cudd Energy Services (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- July 2023 - EEST Energy Services (Thailand), a leading global offshore contractor and services provider, is proud to announce that it has been awarded a USD 9 million contract from Hibiscus Petroleum Berhad, Malaysia, under T7's IWS contract Global Berhad, Malaysia. The contract includes the provision of well work-out/replacement and well plugging and abandonment services utilizing the innovative EEST-502 hybrid hydraulic conversion unit.

- September 2022 - Helix Energy Solutions Group said that it has entered into an extension agreement of two years of its well intervention charter and services. The negotiated extension is scheduled to conclude in December 2024 and directly follows Helix’s current contracts with Petrobras.

- February 2022 – Valesto Energy signed a contract with ExxonMobil and got the provision of a hydraulic workover unit and other services in Malaysia.

- July 2021 - Norwegian energy company ASA announced that the Noble Sam Turner drilling program commenced a spring 2021 well work-out and maintenance campaign and completed three well work-outs, contributing to nearly 2000 bpd positive operating performance results during the Drill program’s second quarter. The use of HWUs contributed significantly to the success of the campaign.

- April 2021 – Oilfield services firm Archer recently signed an offer letter to purchase 100% of the share of Deepwell, which is a Norwegian well intervention company focused on mechanical wireline and cased hole logging services.

REPORT COVERAGE

The research and business intelligence report offers an in-depth analysis of the market. It further provides details on the adoption of hydraulic workover units across several regions. Information on trends, drivers, opportunities, threats, and restraints of the market can further help stakeholders gain valuable insights into the market. The report offers a detailed competitive landscape by presenting information on key players, along with their strategies, in the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.08% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Service

By Capacity

By Installation

By Application

By Region

|

Frequently Asked Questions

A study by Fortune Business Insights states that the global hydraulic workover unit market was valued at USD 1,473.67 million in 2025.

The global market is projected to grow at a CAGR of 6.08% over the forecast period.

The North American market size stood at USD 921.36 million in 2025.

Based on application, the onshore segment holds a dominating share of the global market.

The global market size is expected to reach USD 2,551.42 million by 2034.

Increasing offshore exploration drives market growth.

Halliburton, Well Gear Group and Joney Holdings are some of the top players actively operating across the market.

- 2021-2034

- 2025

- 2021-2024

- 221

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us