Hydrographic Survey Equipment Market Size, Share & Industry Analysis, By Type (Sensing System, Positioning System, Subsea Sensor, Unmanned Vehicle, Software), By Application (Port & Harbor, Oil & Gas, Cable, Charting), By Depth (Shallow Water, Deep Water), By Platform (Surface Vessels, USVS & UUVS, Aircraft), By End User (Commercial, Research, Defense)And Regional Forecast, 2026-2034

Hydrographic Survey Equipment Market Size and Future Outlook

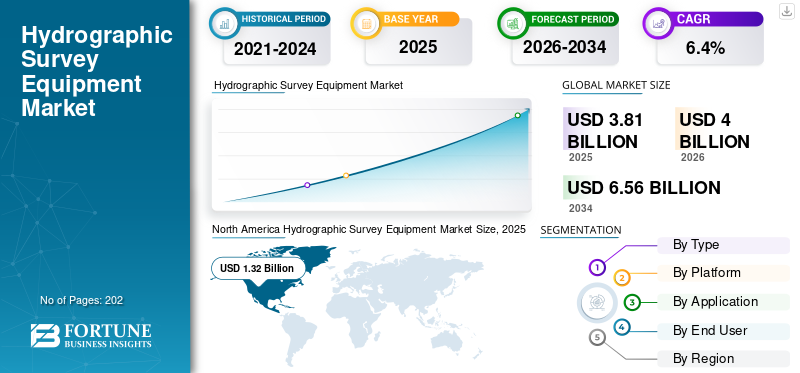

The global hydrographic survey equipment market size was valued at USD 3.81 billion in 2025. The market is projected to grow from USD 4.00 billion in 2026 to USD 6.56 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the global hydrographic survey equipment market with a market share of 34.64% in 2025.

Hydrographic survey equipment refers to the specialized tools and technologies used to measure and map underwater features such as seabeds, shorelines, and water depths. The equipment includes sonar systems such as multibeam and side-scan sonars. These sonars use sound pulses to create detailed images and depth profiles of underwater terrain. With the help of these equipment, underwater physical features and hazards are identified which is used for application such as marine navigation, construction, dredging, and environmental monitoring.

The major players in the market include Kongsberg Maritime (Norway), Teledyne Technologies (U.S.), iXblue (France), Innomar Technologie GmbH (Germany), Kongsberg Maritime, and others. These key companies offers integrated hydrographic survey systems including multibeam echosounders, positioning, and motion reference units. They provide hardware and software solutions catering to offshore energy, naval, and charting sectors. For instance, Konsberg Maritime offers EM 2040P multi-beam echosounder, and Seapath 130 Series GNSS-aided inertial system for hydrographic surveying. Moreover, Teledyne Technologies provides a wide range of sonar systems, acoustic doppler current profiler (ADCP), and navigation solutions designed for deep to shallow water surveys in offshore construction and coastal mapping.

Download Free sample to learn more about this report.

Hydrographic Survey Equipment MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.81 billion

- 2026 Market Size: USD 4.00 billion

- 2034 Forecast Market Size: USD 6.56 billion

- CAGR: 6.40% from 2026–2034

- North America dominated the global hydrographic survey equipment market with a market share of 34.64% in 2025.

- The acoustic systems segment held the largest market share by type in 2025.

- The offshore oil and gas survey segment accounted for the largest application share in 2025.

North American

The North America region holds the largest share in the market, valued at USD 1.32 billion in 2025, and is expected to grow at a significant CAGR during the forecast period.

Europe

Europe is experiencing steady growth, supported by offshore renewable energy projects and marine technology advancements.

Asia Pacific

Asia Pacific is expected to witness the fastest growth due to expanding offshore activities and port infrastructure development.

U.S.

Government investments in coastal resilience and modernization of maritime navigation infrastructure continue to drive market growth.

Japan

Increasing focus on marine research, offshore infrastructure, and advanced hydrographic technologies supports market expansion.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Adoption of Autonomous Underwater Vehicles (AUVs) & Unmanned Surface Vessels (USVs) Expected to Drive Market Growth

The autonomous underwater vehicles (AUVs) and unmanned surface vessels (USVs) are used for hydrographic survey for improving survey efficiency and data quality. These vehicles and vessels allow automating data collection which reduces the time and manpower required for surveys. Therefore, they enable large-area, high-resolution ocean floor mapping at lower operational costs compared to traditional crewed vessels. Thus, there is an increase in utilization of autonomous AUVs & USVs for hydrographic surveying and environmental data acquisition.

- For instance, in April 2025, Unique Group’s Uni-Mini Unmanned Surface Vessel (USV) successfully completed a shallow-water hydrographic multibeam survey in Kwinana, Western Australia. The autonomous USV was equipped with the Norbit iWBMS multibeam sonar and it delivered high-resolution bathymetric data in a restricted near-shore area.

MARKET RESTRAINTS:

Lack of Skilled Labor & High Initial Investment for Advanced Equipment to Limit Market Expansion

Modern hydrographic equipment such as advanced multibeam echosounders and autonomous underwater vehicles require specialized training and expertise, which are currently in short supply. This shortage hampers efficient deployment and limits the adoption of new technologies in the hydrographic survey equipment industry, which is expected to affect the market negatively. Moreover, the high initial investment costs for advanced hydrographic equipment pose a barrier, particularly for smaller organizations and developing regions, restricting market growth.

MARKET OPPORTUNITIES:

Expansion of Offshore Renewable Projects Presents Growth Opportunities for Market Growth

One significant market opportunity in the hydrographic survey equipment sector is the growing demand driven by offshore renewable energy projects, particularly wind farms. As these projects expand globally, there is an increasing need for detailed seabed mapping and underwater infrastructure inspection to support site selection, construction, and maintenance activities. Moreover, there is rise in huge investment in offshore wind farm projects due to effort to reduce carbon emissions and meet the modern energy demands.

- For instance, in November 2025, Cadeler, an offshore wind company signed two firm contracts valued at approximately USD 676.12 million for the full-scope transportation and installation of offshore wind turbines and their foundations. The foundation work for construction of wind farm is set to begin in early 2029 and turbine installation in early 2030.

Such projects encourages the adoption of advanced hydrographic survey technologies such as high-resolution multibeam sonar systems and other survey equipment, which provide precise data required for these complex projects. All such developments and expansion of offshore renewable energy projects presents lucrative opportunities for the growth of the market.

HYDROGRAPHIC SURVEY EQUIPMENT MARKET TRENDS:

Integration of AI and Machine Learning in Hydrographic Survey Equipment Is a Significant Trend in Market

A key trend in the market is the use of AI in hydrographic survey equipment to enhance the processing and interpretation of sonar and multibeam data. The AI integration in the surveys allows automating tasks such as seabed classification, feature detection, and anomaly identification. For instance, AI algorithms analyze high-resolution bathymetric data in real-time to distinguish between different seabed types such as rock, sand, or vegetation, which is critical for accurate mapping and habitat assessment. In addition, there is increasing adoption of AI technology in hydrographic survey equipment to enable autonomous navigation, collision avoidance, and route planning.

- For instance, in July 2025, Robosys Automation integrated its Voyager AI Survey autonomy suite onto Uncrewed Survey Solutions' newly commissioned 6.5-meter USS Accession unmanned surface vessel (USV), enabling advanced autonomous navigation, collision avoidance, and anti-grounding features for marine surveying.

MARKET CHALLENGES:

Environmental and Regulatory Constraints Acts a Challenge for Market

A key market challenge in the market is environmental and regulatory constraints that restrict operations in sensitive marine ecosystems.

- For example, the strict regulations, such as those outlined in NOAA's Hydrographic Surveys Specifications and Deliverables (HSSD 2025), mandate environmental compliance including metadata documentation, quality control for seabed impacts, and limitations on survey timing.

These regulations are enforced to protect habitats such as coral reefs or coastal zones. These rules often prohibit equipment deployment in protected areas, require permits with lengthy approval processes, and enforce noise/vibration limits on sonar systems to minimize marine life disturbance. All such factors are expected to present challenges for the hydrographic survey equipment market growth during the forecast period.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Rising Demand for Deep-Water Surveys in Turbid Conditions and AUV/USV Integration Drives Acoustic Systems Segment Growth

By type, the market is segmented into acoustic systems, positioning systems (GPS/GNSS), optical systems (LiDAR), sensors, software, and others.

The acoustic systems is further divided into sonars, profilers, and echo sounders. Moreover, optical systems comprises LiDAR & laser systems, cameras, and positioning systems include GNSS (Global Navigation Satellite Systems) such as RTK GPS for high-accuracy horizontal positioning.

The acoustic systems segment holds the largest hydrographic survey equipment market share as these systems are increasingly used during deep water survey with turbid conditions, where light penetration is difficult. There is rise in integration of acoustic systems with AUVs/USVs for mapping underwater frontiers and water body features. Moreover, the equipment manufacturers are constantly upgrading their product portfolio by developing and launching advanced acoustic systems for enhancing hydrographic survey capabilities.

- For instance, in October 2024, CHC Navigation launched the RiverStar ADCP 1200/600 series, advanced Acoustic Doppler Current Profilers featuring innovative 5-beam technology and a 300kHz frequency for high-accuracy water flow measurement in depths ranging from 0.3m to 180m.

Optical systems (LiDAR) segment is fastest growing segment and is projected to grow at a highest CAGR of 9.7%. The factors responsible for segment growth is increasing demand for optical systems to conduct surveys in shallow clear waters under 50 meters. The optical equipment increases the speed of survey with the help of its waveform analysis and fast coverage. Offshore wind farm site selection and nautical charting increasingly need detailed vertical water data. In such surveys optical systems are preferred which is expected to increase the hydrographic survey equipment market demand.

By Platform

Large-Scale Surveys for Oil & Gas & Naval Sector Boosts Demand for Surface Vessels Segment

Based on platform, the market is segmented into surface vessels, unmanned surface & underwater vehicles (USVs & UUVs), and aircraft.

Surface vessels segment lead market growth due to their versatility in handling large-scale surveys across shallow and deep waters. The surface vessels are preferred platforms in surveys equipped with advanced sonar for comprehensive bathymetric mapping, port and harbor management, and offshore infrastructure monitoring. Increasing demand for accurate data collection in oil & gas exploration, naval operations and marine navigation is expected to drive the segment growth.

- For instance, in October 2025, the Port of Rotterdam Authority successfully completed the Netherlands' first open-water trial of an unmanned surface vessel (USV), the 3-meter V3000 from Demcon Unmanned Systems, in Prinses Margriethaven on Maasvlakte 2. The V3000 performed hydrographic survey tasks such as depth measurements in hard-to-reach areas for safe marine navigation.

Unmanned Surface & Underwater Vehicles (USVs & UUVs) segment is experiencing fastest growth with a CAGR of around 7.8% owing to its advantages such as low operating costs, and reduced fuel consumption. These vehicles are able to access hazardous or restricted areas such as nearshore zones and under-ice regions, and operate 24/7, which increases its popularity for frequent offshore wind farm surveys and environmental monitoring. Numerous OEMs are increasingly designing advanced USVs to simplify survey operations for small teams with the integration of navigation and sonar technology.

- For instance, in November 2025, SatLab unveiled the HydroBoat 1200MB, a compact uncrewed surface vehicle (USV) integrating the HydroBeam M2 multibeam echosounder for efficient 3D hydrographic surveys in inland and nearshore waters.

To know how our report can help streamline your business, Speak to Analyst

By Application

Rising Offshore Energy Investments Support Offshore Oil and Gas Survey Segment Growth

Based on application, the market is segmented into coastal & port development, underwater, infrastructure inspection, maritime navigation & construction, flood & disaster management, offshore oil and gas survey, cable and pipeline route surveys, environment monitoring, and others.

Offshore oil and gas survey segment acquires the largest share in the market driven by the need for precise seabed mapping to support exploration, drilling, pipeline routing, and platform installation in challenging deepwater environments. Advanced hydrographic survey equipment provides high-resolution bathymetry and sub-bottom profiling to identify geohazards and ensure infrastructure integrity, reducing project risks and costs. Therefore, increasing offshore energy investments and stricter environmental regulations is expected to drive the segment growth.

Maritime navigation & construction segment grows with fastest growth rate of 8.4%. The segment grows due to increasing port expansions, harbor deepening, and coastal infrastructure projects required to accommodate larger vessels and growing maritime trade volumes. Hydrographic surveys guide dredging, berth design, and underwater construction by delivering highly accurate seabed data essential for safe navigation and structural planning. Thus, the rising demand for hydrographic survey to ensure safe vessel movement and day‑to‑day operations in marine environment is expected to drive segment growth.

- For instance, in October 2026, INS Sutlej, the Indian Navy's hydrographic survey ship, successfully concluded its 18th joint mission with the Mauritius Hydrographic Service, mapping 35,000 square nautical miles to bolster marine charting, and coastal regulation.

By End User

Demand for Underwater Mapping in Ports, Dams and Renewables Drive Energy & Infrastructure Developers Segment Growth

Based on end user, the market is segmented into national hydrographic & government agencies, commercial survey & geospatial companies, energy & infrastructure developers, and defense & naval forces.

Energy & infrastructure developers segment dominates the market due to increasing demand for precise underwater mapping to support large-scale infrastructure projects such as bridges, dams, ports, and renewable energy installations. Offshore project developers contract survey providers to assess environmental impacts and obtain data on water depths, seabed composition, which is expected to drive the segment growth in the market.

- For instance, in May 2025, Terradepth, Ocean Data as a Service (ODaaS) provider received a five-year master services agreement with a major offshore energy company to deliver cost-effective autonomous hydrographic survey and data services.

Defense & Naval Forces segment is expected to grow at a steady rate with 5.2% CAGR. The naval forces require hydrographic information for safe naval navigation, mine detection, and undersea surveillance. Moreover, increasing naval modernization and maritime security initiatives across the globe boost demand for advanced survey equipment.

- For instance, in February 2024, Indian Navy commissioned INS Sandhayak, a survey vessel and equipped it with Kongsberg's HUGIN autonomous underwater vehicle (depth-rated to 1,000m), multi-beam echo-sounders, ROVs, side-scan sonars, and HiPAP systems. The vessel was used for hydrographic surveys of ports, harbors, channels, and deep seas to ensure safe navigation.

Hydrographic Survey Equipment Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

NORTH AMERICA

North America Hydrographic Survey Equipment Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region holds the largest share in the market, valued at USD 1.32 billion in 2025, and is expected to grow at a significant CAGR during the forecast period. The market in the region is growing due to coastal infrastructure development, and increasing focus on maritime safety and environmental monitoring. Moreover, the regulatory mandates to update nautical charts and enhance disaster preparedness bolster market growth.

- For instance, in January 2025, Fugro was awarded a new five-year indefinite delivery/indefinite quantity (IDIQ) contract by the National Oceanic and Atmospheric Administration (NOAA) to provide hydrographic survey services supporting the creation and maintenance of accurate nautical charts for safe maritime navigation within U.S. waters.

In addition, the presence of leading survey equipment manufacturers such as Teledyne Technologies Inc., EdgeTech, R2Sonic Inc., and research institutions also fuels innovation and adoption in this region. U.S., government funding for coastal resilience projects and modernization of maritime navigation infrastructure is significantly driving the global hydrographic survey equipment market. The strategic emphasis on maintaining navigational safety and supporting offshore energy operations in the country supports the market expansion.

EUROPE

In Europe, the market is expected to witness steady growth due to the surge in offshore renewable energy projects, especially wind farms. Moreover, major European ports are upgrading to manage larger vessels which increases the demand for regular dredging surveys. This is expected to push the adoption of advanced hydrographic technology and equipment. In addition, the rise in hydrographic surveys to generate electronic navigational charts for safe marine navigation also boost the equipment demand.

- For instance, in January 2025, Guernsey Ports conducted a week-long hydrographic survey of Guernsey's east coast using the 6.5m Cheetah catamaran Shoreline (callsign 2EUL9) equipped with multi-beam sonar to map seabed depths and contours for updated electronic charts.

ASIA PACIFIC

The Asia Pacific market is experiencing rapid growth driven due to expansion of port development projects and coastal construction initiatives. . Expanding offshore oil and gas fields, coupled with offshore wind projects, demand detailed seabed mapping with the help of advanced hydrographic equipment. Moreover, the government initiatives to enhance maritime logistics and ensure safe navigation is also expected to rise the need for hydrographic surveys.

- For instance, in February 2025, Australia handed over a state-of-the-art Shallow Water Multi-Beam Echo Sounder to Sri Lanka Navy Hydrographic Service at for conducting coastal and harbor surveys for updated nautical charts, enhancing safe navigation and Sri Lanka's Safety of Life at Sea compliance.

LATIN AMERICA

The Latin America market is driven by offshore oil exploration in countries such as Brazil in pre-salt fields which requires deepwater survey data for exploration and infrastructure integrity. In addition, the rising port modernization throughout the region ensures safe navigation for rising exports, which drives region growth during the forecast period.

MIDDLE EAST & AFRICA

In the Middle East and Africa, the market growth is fueled by strategic investments in port expansions and transshipment hubs. Oil-rich countries in the region require subsea pipeline route surveys and environmental assessments critical for resource exploitation which propels the need for hydrographic survey services, which in turn drives market growth.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Innovation, Integration of AI, and Product Upgrade Drive Competitive Dynamics in Market

The hydrographic survey equipment market is characterized by companies, including Kongsberg Gruppen ASA (Norway), Teledyne Technologies Inc. (US), EdgeTech (US), and others. These firms offer surveying equipment such as multi-beam echo sounders, autonomous underwater vehicles (AUVs), remotely operated vehicles (ROVs), side scan sonars, and data processing systems. Market leaders aim to make continuous innovation and development of high-accuracy, efficient, and scalable equipment to meet the growing demand from maritime, oil and gas, environmental monitoring, and defense sectors.

In addition, to strengthen their market position, market players are making strategic investments in R&D, collaboration with research institutions, and the adoption of protective technologies to ensure robust, reliable, and precise data acquisition in challenging marine environments

LIST OF KEY HYDROGRAPHIC SURVEY EQUIPMENT COMPANIES PROFILED:

- Kongsberg Gruppen ASA (Norway)

- Teledyne Technologies Inc. (U.S.)

- EdgeTech (U.S.)

- iXblue SAS (France)

- Sonardyne International Ltd. (U.K.)

- Fugro N.V. (Netherlands)

- R2Sonic Inc. (U.S.)

- Chesapeake Technology Inc. (U.S.)

- CEE HydroSystems (U.S.)

- Hydro-Tech Marine Technology Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Hydro-Tech launched the MS8240, a new-generation Multibeam Echo Sounder offering adjustable multi-frequency operation from 150 kHz to 700 kHz for enhanced resolution and range.

- June 2025: Picotech’s Podlet multibeam sonar package, paired with Blue Robotics’ BlueBoat USV, was introduced as a new one-person-portable hydrographic survey solution capable of IHO Special Order surveys in shallow waters

- February 2025: CHC Navigation (CHCNAV) introduced the HQ-400 compact multibeam echosounder for high-resolution bathymetric and hydrographic surveys, integrating sonar, IMU and sensors in a 2.7 kg head for use on survey boats and USVs.

- January 2025: Fugro secured a new five-year IDIQ contract from NOAA’s Office of Coast Survey to provide hydrographic survey services for U.S. nautical charting, leveraging advanced technologies such as remote and autonomous survey systems

- April 2023: Sonardyne launched its new Origin Acoustic Doppler Current Profilers (ADCPs) at Ocean Business 2023, including the Origin 600 and Origin 65 models designed for marine research, offshore renewables, and defense applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, By Platform, By Application, By End User, and Region |

| ByType |

Acoustic Systems

Positioning Systems (GPS/GNSS)

|

| ByPlatform |

|

| By Application |

|

| By End User |

|

| By Region |

North America (By Type, By Platform, By Application, By End User, and Country)

Europe (By Type, By Platform, By Application, By End User, and Country)

Asia Pacific (By Type, By Platform, By Application, By End User, and Country)

Latin America (By Type, By Platform, By Application, By End User, and Country)

Middle East & Africa (By Type, By Platform, By Application, By End User, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.81 billion in 2025 and is projected to reach USD 6.56 billion by 2034.

In 2025, the market value stood at USD 1.32 billion.

The market is growing at a CAGR of 6.4% during the forecast period of 2026-2034.

The surface vessels segment led the market by platform in 2025.

The key factors driving the market are growth of market are rising adoption of autonomous underwater vehicles (AUVs) & unmanned surface vessels (USVs) for hydrographic survey.

Kongsberg Gruppen ASA (Norway), Teledyne Technologies Inc. (U.S.), EdgeTech (U.S.) and among others are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us