SONAR System Market Size, Share & Industry Analysis, By Product Type (Hull-Mounted, Stern-Mounted, Sonobuoy, and DDS), By Application (Commercial and Defense), By Platform (Ship Type and Airborne), By Solution (Hardware (Transmitter, Receiver, Control Units, Displays, Sensors (Ultrasonic Diffuse Proximity Sensors, Ultrasonic Retro-Reflective Sensors, Ultrasonic Through-Beam Sensors, VME-ADC, and Others), and Others) and Software), By End-User (Line Fit and Retrofit), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

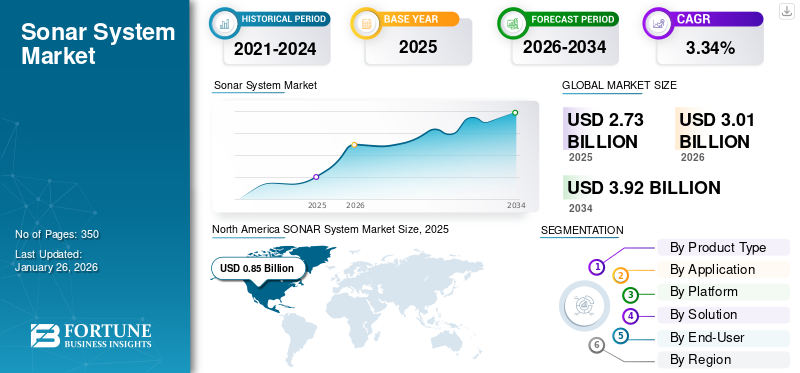

The global SONAR system market size was valued at USD 2.73 billion in 2025. The market is projected to grow from USD 3.01 billion in 2026 to USD 3.92 billion by 2034, exhibiting a CAGR of 4.25% during the forecast period. North America dominated the flexible lid stock packaging market with a market share of 31.35% in 2025.

Sound Navigation and Ranging (SONAR) is an advanced technique that uses sound propagation to navigate and communicate with objects inside the water. Increasing naval ship procurement, up-gradation activities, and rising commercial ship deliveries globally is estimated to drive the market growth. Diver detection systems, surveillance network SONAR, synthetic aperture SONAR, and twin inverted pulse SONAR are latest technological trends emerging in the market.

The fast convergence and consolidation of advanced digital signal processing and artificial intelligence (AI) by SONAR systems have greatly improved the capability of systems to distinguish real underwater threats from noise. This has also improved detection levels and minimal false alarms. Further, AI software allows for real-time processing of complex acoustic signatures, conducts automatic target identification, and allows predictive maintenance essential to both military operations and commercial ventures.

In addition, multi-frequency arrays and synthetic aperture SONAR capabilities enhance detection ranges and resolution imagery and improve operational performance in anti-submarine warfare, seabed mapping, and mine hunting. Evolution to lighter, smaller, module-based hardware with ability to plug into AUVs and USVs streamlines the product adoption by enabling flexible, scalable system installation in a broad range of maritime environments. Lockheed Martin Corporation, L3Harris Technologies Inc., Raytheon Technologies Corporation, Teledyne Technologies Inc., and Thales Group are some of the most prominent players in the market, accounting for a dominating market share. These companies are a major growth driver for the market by developing highly sophisticated systems, and integrating them with latest technologies such as UUVs and focusing on enhanced signal processing and resolution.

Download Free sample to learn more about this report.

SONAR SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.73 billion

- 2026 Market Size: USD 3.01 billion

- 2034 Forecast Market Size: USD 3.92 billion

- CAGR: 4.25% from 2026–2034

- North America dominated the SONAR system market with a 31.35% share in 2025.

- The hull mounted segment is projected to hold a 51.24% market share in 2026.

- The defense segment is expected to account for 65.95% of the global market in 2026

North America

North America maintained market leadership due to increasing naval modernization and rising shipbuilding activities across the region.

Europe

Europe accounted for 25.89% of global market revenue in 2025, supported by growing maritime surveillance investments.

Asia Pacific

Asia Pacific is witnessing strong growth driven by increasing defense spending and expanding naval capabilities in emerging economies

U.S

The U.S. market continues to expand with increased procurement of advanced naval defense and underwater surveillance systems.

Japan

Japan’s SONAR system market is forecast to reach USD 0.17 billion by 2026, supported by maritime security enhancement programs.

Read More

Market Dynamics

Market Drivers

Rising Defense Expenditures and Maritime Security Concerns Accelerate Adoption of Advanced SONAR Systems

Growing defense spending and increased maritime security needs drive the demand for advanced systems in naval combat. With growing geopolitical tension and border conflicts worldwide, especially in Asia Pacific, countries are seeking to upgrade naval systems to secure sea lanes, seabed assets, and national interests.

India, China, and Japan are arming their warships with next-generation SONAR to improve detection, underwater surveillance, and maritime domain awareness. Anti-submarine warfare (ASW), mine laying, and detection of underwater threats are enabled by SONAR technology, therefore these form the backbone of contemporary naval defense.

Technological developments in artificial intelligence-driven signal processing, synthetic aperture SONAR, and network SONAR for reconnaissance currently impart additional functionality to these systems. Adding unmanned underwater vehicles (UUVs) and autonomous underwater vehicles (AUVs) to SONAR delivers the tactical edge to navies in the form of more stable and adaptive underwater surveillance.

- In January 2025, U.K.-based technology group ELAC Sonar secured a contract worth USD 16.75 million to develop SONAR systems for the Italian Navy. This investment by the Italian navy is part of a broader agreement involving the delivery of systems for Italy's new submarine initiative.

Expansion of Offshore Energy Exploration and Subsea Infrastructure Propels Market Growth

Offshore crude oil production of competitive subsea exploration and construction is gradually shifting toward the requirement of accurate SONAR solutions and aggressively driving the SONAR systems market growth. While global energy demand continues to grow, oil & gas and alternative energy project endeavors increasingly rely upon sophisticated SONAR technology for accurate and effective underwater surveying, resource exploration, and infrastructure examination. Systems are critical in finding subsea oil and gas reservoirs, seabed geology, and the safety and integrity of offshore platforms and pipelines. It is demanded by highly hostile and deeper offshore plays where traditional survey methods fall short and real-time high-resolution SONAR imagery becomes imperative.

- In February 2025, U.S.-based SONAR systems conglomerate Ultra Maritime signed a production-planning contract with Indian engineering pioneer Bharat Dynamics Limited (BDL) to initiate the co-production of the U.S. sonobuoys in India.

Additionally, high-technology SONAR assistance with autonomous underwater vehicle deployment is revolutionizing offshore exploration based on the success of high-technology survey operations in conditions unsuitable for manned operations, focusing on enhancing data quality and operation efficiency. Synthetic upgrading of SONAR services designed for application within the offshore oil & gas industry has risen, led by organizations such as Kraken Robotics, to implement high-definition imagery in complicated subsea operations. They enhance the accuracy of exploration and lower the risk and expense of operations.

Market Restraints

High R&D Costs and System Complexity Due to Limited Accessibility Hinders Market Growth

High R&D expense and system complexity are significant issues that act as restraints for the SONAR system market growth i.e., by restricting access to small-scale commercial customers. Sophisticated systems involve massive investments in R&D, advanced sensor technologies, and digital signal processing, and therefore, their production, deployment, and maintenance are costly. These are immensely expensive for small defense entities and commercial operations of higher size and are an obstacle to small businesses, fisheries, and research entities with constrained budgets.

Further, the complexity of contemporary SONAR—often requiring interfacing with artificial intelligence, machine learning, and high-level data analysis—requires technical expertise to operate and interpret results. Small adopters lack trained personnel or capacity to harness these systems to their maximum capacity, thus limiting its adoption.

Various established players in the market have superior technology and capacity, making it difficult for new entrants and small companies to compete or innovate at large scale. This limited access inhibits market penetration in the commercial market and innovation by lower, potentially disruptive entrants.

Market Opportunities

Growing Demand for AUVs Due to Emergence of AI-Integrated SONAR Technologies Offer Lucrative Opportunities

The rapid development and miniaturization of SONAR technology, particularly artificial intelligence-based, stimulates the demand for autonomous underwater vehicles (AUVs) in defense applications, scientific research, and commercial applications.

Miniature AI-driven SONAR allows AUVs to sonar-map complex and dynamic underwater scenes more autonomously and precisely. Future breakthroughs predict combining different types of sensors—i.e., SONAR, Doppler velocity logs, and inertial measurement units—through sophisticated AI algorithms to enhance simultaneous localization and mapping (SLAM) to enable greater navigation and environment perception even in GPS-denied settings.

New technologies including the sparse-aperture SONAR arrays that are designed at MIT and Lincoln Laboratory to act autonomously highlight the swarms of small autonomous vehicles equipped with SONAR and can scan the seafloor at rapid rates and higher resolutions than existing single-vehicle systems. It also accelerates deep-sea and infrastructure exploration, costs less to run and increases mission lifespan.

In naval defense, navies are trying to create systems combining AUVs and unmanned underwater vehicles with future SONAR for sustained observation, mine hunting, and anti-submarine warfare, using AI for rapid processing of acoustic information and improved threat detection.

- In January 2025, researchers from Belgium unveiled the development of a 3D SONAR system, which while combined with high-speed, high-range cameras, makes it easier to experience bat echolocation in action. The camera and 3D system make it easier for underwater detection.

SONAR System Market Trends

Integration of AI and Machine Learning to Provide Enhanced Real-time Data Processing in Modern SONAR Systems

The integration of machine learning (ML) and artificial intelligence (AI) in modern SONAR transforms real-time data processing and operational effectiveness in defense, commercial, and research sectors. AI-powered SONAR platforms employ sophisticated algorithms to scan vast amounts of acoustic information, rapidly separating valid targets from ambient noise—a function previously constrained by human analysis and slower signal processing. Recent advancements, such as attention-based deep neural networks (ABNNs), have reached promising target recognition precision even under noisy and occlusive underwater conditions.

For instance, ABNNs can control attention to the prominent features in SONAR data, removing redundancy, noise, and significantly enhancing detection under adverse conditions such as shallow or congested water. In military applications, AI-based SONAR are being onboarded on submarines and unmanned underwater vehicles to achieve edge processing that helps limit decision latency and enhance real-time situational awareness.

- For instance, in May 2025, Thales group unveiled a contract from the Singapore Navy to equip their navy with an AI-powered mine power system. The SONAR system is said to accurately detect, classify, and neutralize mines in real-time at one of the busiest maritime straits in the region.

Download Free sample to learn more about this report.

Russia-Ukraine War Impact Analysis

Ongoing War Conditions and Geo-Political Tensions Significantly Influence Market

Current war crises have profoundly impacted the demand and development of SONAR, primarily by prompting technological advancements and raising their stature as naval defense strategies. High-intensity geopolitical tensions, including those fueled by East European conflict and Indo-Pacific maritime tensions, escalated, allowing countries to increase underwater reconnaissance. This has also witnessed a surge in investment in the next-generation SONAR technologies offering higher detection precision, greater range, and faster real-time data processing.

For instance, Russian and Ukrainian ports are the largest crude oil, wheat, and corn export hubs. The current war situation has shut down the cargo import and export through the sea, resulting in inactive growth in the marine sector. The Russia-Ukraine conflict has made a higher impact on the showcase of the SONAR, both inside military and commercial circles, in different ways. On the military front, the war has impacted different European countries, including Poland, and is set to increase their defense budget due to raised security dangers and a recommendation from NATO to spend a minimum of 2% of GDP on defense.

The increment in Poland's defense budget to 4% of GDP in 2024 has accelerated maritime modernization activities, including procuring progressed SONAR frameworks for modern and overhauled ships including mine countermeasure ships and frigates. Ukraine and Russia invest heavily in SONAR to keep up with the latest defenses.

- For instance, in April 2023, Ukrainian naval forces unveiled the development of unmanned underwater vehicles. The prototypes were presented in the Brave1 exhibition, and the operational range for these UUVs is about 2,000 km.

SEGMENTATION ANALYSIS

By Product Type

Hull Mounted Segment Dominates as Defense Forces Focus on Improving their ASW Capabilities

The market is segmented into hull-mounted, stern-mounted, sonobuoy, and DDS based on product type.

The hull-mounted segment accounted for the highest share in 2024. Naval and military civil operations are credited an inherent advantage through hull-mounted SONAR. The finest subsea sensor used by naval ships, the hull-mounted SONAR, has long-range hard-detection and track capability essential to anti-submarine warfare (ASW), navigation underwater, seabed and obstacle survey, as well as survey of resources. The hull mounted segment is projected to dominate the market with a share of 51.24% in 2026.

New and existing ship installations are motivated by naval upgradation, maritime trade growth, and independent shipping deployment, all necessitating the latest subsea detection. Advancements in technology have led to sensor sensitivity, signaling capacity to process, and miniaturization being upgraded to levels that support the installation of hull-mounted SONAR and maintenance in many vessels. The growing need for naval security, especially due to future submarine attacks and border conflicts, also stimulates investment in the same by defense and commercial naval industries.

The sonobuoy segment is expected to grow at the highest CAGR in the forthcoming years. Demand for sonobuoys is growing rapidly due to its growing use in anti-submarine warfare (ASW), naval reconnaissance, offshore exploration, and oceanic research. Deployable and expendable sonobuoys offer near-real-time underwater acoustic data to support submarine and underwater threat detection and tracking from sea or air-launched platforms. It is driven by growing naval modernization, encompassing maritime security tensions, and the necessity for low-cost, flexible ASW capability, particularly in heightened submarine activity and border disputes. Advanced technology in terms of effective acoustic sensors, battery longevity, wirelessly sent data, and machine-learning processing has made the sonobuoys efficient, accurate, and ubiquitous. Defensibility, merchantability, and strategic purchases by high-power navies drive long-term growth for the product category.

To know how our report can help streamline your business, Speak to Analyst

By Application

Defense Application Leads Owing to Growing Use of SONAR Systems for MCM Operations

By application, the market is divided into commercial and defense.

The defense segment held the largest share of the market in 2024 and is anticipated to grow at the highest CAGR over the forecast period. Defense segment is the market’s stronghold for SONAR, with increasing demands for high-technology underwater monitoring, mine location, ASW, and seaport defense propelling the demand. Rising geopolitical tensions and naval modernization are prompting governments to invest heavily in sophisticated SONAR technology with improved detection, tracking, and threat recognition capabilities. The defense segment is projected to dominate the market with a share of 65.95% in 2026.

The use of SONAR in mine countermeasures, diver detection, and defense of strategic maritime infrastructure has become highly critical in the context of emerging underwater attack threat. Incorporating sensor fusion, 3D imaging, and AI has also improved SONAR's efficiency in defense to augment maritime security and operational excellence for naval weapons globally.

- In March 2025, the Thales group, a pioneer in the SONAR market, unveiled winning a contract to supply integrated SONAR suites for the Netherlands Navy. This contract aims to integrate the sonar suites with the Netherlands Royal Navy’s new Orka-class submarines.

The commercial segment is anticipated to showcase significant growth during 2025-2032. The market for the SONAR is growing at a very impressive rate due to the rising demand for hydrographic surveys, offshore oil and gas exploration, and fisheries. The SONAR technique is crucial in seabed mapping, underwater pipeline searching, and safe navigation of merchant vessels. Other global ship deliveries and retrofitting activities highly impact the adoption rate due to ongoing businesses' desire to optimize efficiency and safety in operations.

Advancements in technology for digital signal processing and integration with UUVs have enhanced system reliability and performance, making them necessary in resource exploration and environmental monitoring. As offshore business and sea trade continue to travel farther from home, the dependence of commercial businesses on advanced SONAR technology will also be in a dynamic growth position.

By Platform

Ship Type Platform will Grow Rapidly as Market Witnesses Growing Seaborne Trade Globally

Based on platform, the market is classified into ship type and airborne.

The ship type segment accounted for the largest market share in 2024 and is anticipated to grow with the highest CAGR in the forthcoming years. Installing SONAR on naval ships by authorities is necessary due to the growing need for high-performance underwater surveillance, navigation security, and mission success in naval warfare and merchant shipping. Naval commanders all over the globe are spending billions of dollars on SONAR-equipped ships to support anti-submarine warfare, mine detection, and maritime security operations against rising geopolitical tensions and sophisticated underwater threats. In commerce, expanding offshore and ocean business creates demand for SONAR in tankers, cargo ships, research vessels, and cruise ships for secure transportation, seabed exploration, and ocean condition surveillance. The ship type segment is expected to lead the market, contributing 72.17% globally in 2026.

Improved detection and measurement of possibility with multi-beam and synthetic aperture SONAR technology has created the need and usage of these systems for contemporary shipping. With renewal of fleet and compliance being crucial, ship owners and shipping authorities accord high priority to the adoption of new-generation SONAR technology in builds and retrofits.

The airborne segment will witness significant growth during the forecast period. Airborne systems are used due to their critical role in emergency underwater reconnaissance and area-wide intelligence gathering. Patrol aircraft, helicopters, and unmanned aerial vehicles equipped with SONAR facilitate instant deployment, rapid data collection, effective anti-submarine warfare, search and rescue, and coastal border patrol operations. Other instances of encroachment on maritime security and border disputes and rising defense spending, are driving investment in airborne SONAR, especially by dominant navies.

- In June 2021, the Boeing company partnered with the U.S. Navy to provide an upgraded version of the airborne anti-submarine warfare (ASW) sonar for the Navy's P-8A Poseidon. The contract worth USD 24 million is expected to boost the aerial anti-submarine capabilities of the U.S. Navy.

Technological developments such as miniaturization, artificial intelligence integration, and signal processing engineering have improved airborne SONAR performance and accuracy making it possible to employ it for military as well as civilian purposes, such as oceanography and fishery management. Mobility and quick response of air platforms make them an absolute necessity in contemporary maritime operations.

By Solution

Hardware Solution Holds Leadership Position Due to Increasing Use of Ultrasonic Sensors

Based on solution, the market is segmented into hardware and software.

The hardware segment accounted for the largest market share and will grow at the highest CAGR over the forecast period. Hardware solution design is compelled mainly by mounting requirements for ultrasonic sensors and accompanying equipment such as control units, display units, data storage units, and alarms. These hardware components make it possible to do high-resolution imaging, loop control, liquid-level sensing, and through-beam detection, which are highly crucial for defense and civilian naval applications. Advances in technology enabled the creation of more capable, longer-lasting, and multifunctional hardware, which is needed to be installed on new warships or retrofitted into them. Increased naval modernization, shipbuilding, and demand for stable underwater observation drive demand for improved hardware solutions, thus making this segment dominant. The hardware segment will account for 62.75% market share in 2026.

The software segment will hold a significant market share during 2025-2032. The need for high-level information processing, real-time monitoring, and many functions in SONAR evokes software solution programming. Contemporary SONAR software uses artificial intelligence and machine-learning capabilities to improve detection rates, enable automatic threat detection, and minimize false alarms. These software platforms allow effortless integration into shipboard command systems, remote control, and adaptive decision-making capability critical to anti-submarine warfare and commercial seabed mapping. With growing complexity and data dependency in marine operations, investment in next-generation software is crucial to optimize SONAR deployments' performance, efficiency, and operational responsiveness. An increase in demand for advanced multifunctional SONAR software is estimated to drive the market growth.

By End-user

Line Fit Segment to Grow with Highest CAGR Due to Rising Demand for Advance Naval Vessels

By end-user, the market is divided into line fit and retrofit.

The line fit segment is anticipated to showcase fastest growth during the forecast period. This growth is due to the rising demand for advanced SONAR for naval vessels. In the SONAR industry, line fit business development is occurring rapidly, due to increased demand for newly constructed naval and commercial ships with advanced SONAR technology from the beginning. While the navies' modernization worldwide is in full swing and defense expenditure is rising, shipyards are emphasizing on integrating advanced SONAR while constructing ships for operational deployment readiness, alignment with changing security requirements, and unfettered system interoperability.

This focus on the future optimizes the cost of future retrofitting and allows for integrating multi-scan high-performance SONAR technology. The growth is also being encouraged by increasing seaborne commerce, sea threats to maritime security, and technological advances, fueling the need for newbuilds carrying onboard next-generation underwater detection technology.

The retrofit segment is estimated to hold the largest market share during 2025-2032. This growth is attributed to upgrading connected systems for conventional naval ships. The demand for this segment is fueled by the necessity of outfitting future naval and commercial fleets with next-generation SONAR to counter emerging underwater threats and prolong vessel life. Ship operators are refurbishing older vessels to enhance detection capability, operating performance, and regulatory compliance for lower price of acquiring new ships. Module and compatible SONAR technology advancements enable retrofitting as they allow simple interfacing with bases installed to decrease operating downtime to lower levels. Increasing demand for commercial ship refits and competitiveness requirements in the defense and commercial sectors are key factors that increase the demand for retrofit SONAR solutions feasible.

SONAR System Market Regional Outlook

By region, the market is studied across North America, Europe, Asia Pacific, and the rest of the world.

North America

North America SONAR System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 31.35% of the global market share, reaching a valuation of USD 0.85 billion, and is projected to grow to USD 0.94 billion in 2026. This dominance is due to increased naval shipbuilding in the U.S. The North American SONAR system market share is progressing with robust defense expenditure, continued naval modernization, and national ambitions to dominate the seas. The U.S. leads the way with robust defense expenditure on anti-submarine warfare, mine detection, and seabed surveillance, propelled by the reality of defense contractors with high defense expenditure and state-of-the-art research facilities. The commercial world, such as offshore oil and gas exploration and seafloor exploration, also provides a higher demand. Government programs for large-scale ship construction, such as buying aircraft carriers, submarines, and support ships, stimulate demand in the U.S. market for SONAR. Defense upgrading and growing navy shipbuilding activity are the primary drivers, accompanied by strategic investment in future SONAR for defense and commercial applications. The U.S. market is valued at USD 0.85 billion by 2026.

Europe

The market in Europe reached USD 0.71 billion in 2025, representing 25.89% of total market revenue, and is projected to reach USD 0.78 billion in 2026. Europe's SONAR market is moving forward with the modernization of naval forces, the creation of autonomous ship technology, and the integration of advanced threat detection capabilities. Big economies such as the U.K., France, and Germany are investing heavily in sea system modernization and adopting new technology for both military and civilian use. In Europe, retrofitting autonomous ship technologies in vessels and introducing advanced threat detection and identification technologies in naval ships are anticipated to drive the market. In the U.K., increasing investment in upgrading marine systems is expected to propel the market. The UK market is expected to reach USD 0.17 billion by 2026, while the Germany market is assessed at USD 0.12 billion by 2026.

Asia Pacific

Asia Pacific contributed approximately USD 0.78 billion to the global market in 2025, accounting for 28.75% share, and is expected to reach USD 0.87 billion in 2026. Asia Pacific will showcase remarkable growth due to increased spending in the naval sector and a rise in domestic ship production in South Korea and China. The Asia Pacific SONAR market is expanding remarkably due to increasing naval spending, border disputes, and rising indigenous shipbuilding operations in China, South Korea, and Japan. Naval enhancements in the region and securing strategic sea routes drive huge investments in advanced SONAR. The Japan market is forecast to attain USD 0.17 billion by 2026, the China market is set to reach USD 0.20 billion by 2026, and the India market is anticipated to achieve USD 0.16 billion by 2026.

- In May 2025, Adani Defence & Aerospace partnered with Sparton (DeLeon Springs LLC), a prominent subsidiary of Elbit Systems known for its advanced Anti-Submarine Warfare (ASW) systems. The partnership aims to combine the manufacture of ASW systems and sophisticated electronic systems for domestic and international markets.

Rest of the World

The Rest of the World market accounted for USD 0.38 billion in 2025, representing 14.01% of the global industry, and is expected to reach USD 0.41 billion in 2026. Rising global sea trade, ship repair, and guarding strategic shipping routes and offshore oil & gas platforms drive the Middle East & Africa SONAR market expansion. Governments are installing new naval gear and fast-speed submersible sensors to respond to regional security risks. The Latin America SONAR market is also expanding as countries endeavor to guard extensive coastlines, seaports, and offshore assets from crime and environmental attacks. Seaborne trade expansion and ship refit, particularly in Brazil and other coastal states, drive the demand for SONAR refit and new installation. The rest of the world will witness moderate growth owing to the increase in maritime trade and ship overhauling in the Middle East & Africa, and Latin America regions. The ROW market is estimated at USD 0.41 billion by 2026.

Competitive Landscape

Key Market Players

Key Players are Focusing on Advanced Technologies and Next Generation SONARs Through Research and Development

Competition in the SONAR system market is high due to competition among new-tech and old-defense giants. The market is expected to grow due to high competition and technological development through innovation. Market leaders include THALES, ThyssenKrupp AG, Lockheed Martin Corporation, General Dynamics Corporation, Northrop Grumman Corporation, L3Harris Technologies, and Kongsberg Gruppen. These firms are operating on the shoulders of creating next-generation technologies such as AI-based signal processing, 3D imaging, sensor fusion, and interaction with autonomous underwater vehicles (AUVs) and autonomous surface vehicles (USVs).

The sector is growing incrementally with rising defense budgets, naval defense needs, and other civilian uses such as offshore natural resource exploration and marine pollution monitoring. Optimal solutions include strategic alliance, uncompromising investment in R&D, scalability, and modularity via a module-based design philosophy.

LIST OF KEY SONAR SYSTEM MARKET PLAYERS PROFILED

- Aselsan A.Ş. (Turkey)

- Atlas Elektronik India Pvt. Ltd. (India)

- DSIT Solutions Ltd. (Israel)

- EdgeTech (U.S.)

- Furuno Electric Co. Ltd. (Japan)

- Japan Radio Co. (Japan)

- Kongsberg (Norway)

- Lockheed Martin Corporation (U.S.)

- L3Harris Technologies Inc. (U.S.)

- NAVICO (Norway)

- Raytheon Technologies Corporation (U.S.)

- SONARDYNE (U.K.)

- Teledyne Technologies Incorporated. (U.S.)

- Thales Group (France)

- Ultra (U.K.)

KEY INDUSTRY DEVELOPMENTS

- In March 2025, Ultra Maritime received a USD 23 million contract by the U.K. Service of Protection (MoD) to supply sonobuoys for the Royal Navy's (RN's) Merlin HM2 maritime helicopter.

- In November 2024, the French Naval force unveiled field SonoFlash on modernized Atlantique ATL2 maritime patrol aircraft and NH90 Caïman helicopters. In the meantime, Thales is parallel venturing into its international marketing endeavors as it seeks to secure early export customers. SonoFlash may be a new-generation A-size sonobuoy created to meet the French Naval force's anti-submarine warfare (ASW) necessity.

- In November 2024, JFD, the submarine rescue and elude training auxiliary of U.K.-based sea designing and vitality company James Fisher and Sons plc, entered a contract to boost the Indian Navy's underwater capabilities. JFD's DSRV has the capacity for a crew of three plus up to 16 rescues.

- In October 2024, the U.S. Naval force unveiled hand-deployment of sonobuoys from a Sikorsky CH-53E Super Stallion as the service investigates new tactics for a potential battle within the Pacific. The test involved a crew member tossing the sonobuoy out of the open cargo entryway within the aircraft's rear.

- In January 2024, the Capability Development, Underwater and Electronic Warfare (CD UEW) Project Team, part of the Ministry of Defence, intends to place a new single-source contract with BAE Systems to provide service support for Sonar 2117.

REPORT COVERAGE

The global SONAR system market research report provides a detailed market analysis. It focuses on key aspects such as leading companies, different platforms, product types, solutions, and applications. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.34% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Application

|

|

|

By Platform

|

|

|

By Solution

|

|

|

By End-user

|

|

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 2.73 billion in 2025 and is projected to reach USD 3.92 billion by 2034.

Registering a CAGR of 3.34%, the market will exhibit steady growth during the forecast period (2026-2034).

Hull-mounted in the product type segment is expected to lead this market during the forecast period due to the increasing focus of defense forces to improve ASW capabilities.

KONGSBERG is the leading player in the global market.

North America dominated the market with a share of 31.35% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 350

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us