Hyperspectral Imaging Market Size, Share, Industry Analysis, and Russia-Ukraine War Impact Analysis, By Application (Process Control, Manufacturing, Quality Assurance, Military Surveillance, Remote Sensing, and Others), By Technology (Pushbroom/Line Scan, Snapshot, and Other Technologies), By Product (Cameras, and Accessories), By End-Use (Food & Beverages, Healthcare & Pharmaceutical, Defense, Chemical, and Others), and Regional Forecast, 2026-2034

Hyperspectral Imaging Market Size and Future Outlook

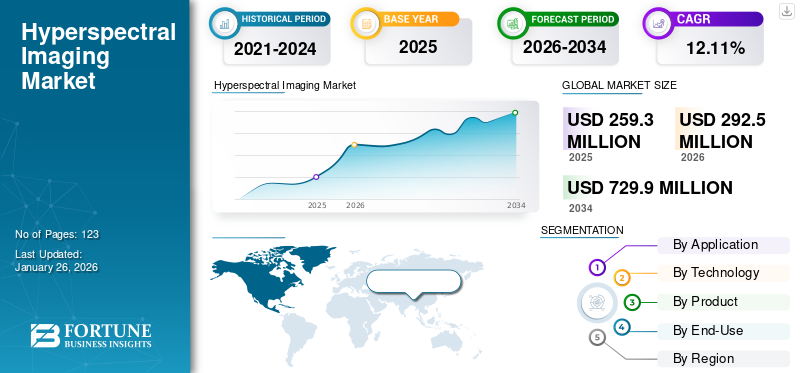

The global hyperspectral imaging market size was valued at USD 259.3 million in 2025 and is projected to grow from USD 292.5 million in 2026 to USD 729.9 million by 2034, exhibiting a CAGR of 12.11% during the forecast period. North America dominated the hyperspectral imaging market with a market share of 33.19% in 2025.

The hyperspectral imaging (HSI) market is experiencing rapid growth as industries and defense agencies increasingly recognize the value of spectral intelligence in decision-making, monitoring, and automation. Unlike traditional imaging, which captures visual color bands, HSI collects hundreds of narrow wavelength bands across the electromagnetic spectrum enabling precise material identification, chemical composition analysis, and object detection. This capability makes it invaluable for aerospace and defense, agriculture, food inspection, healthcare, and environmental monitoring. In defense, it is used for target recognition, camouflage detection, and terrain mapping, while in agriculture, it supports precision farming and crop health monitoring.

Technological advancements such as SWIR (short-wave infrared) and snapshot imaging are improving speed and miniaturization, enabling deployment on UAVs, satellites, and handheld systems. Additionally, the integration of AI and machine learning for spectral data analysis has transformed hyperspectral imaging from a research-oriented technique to a real-time operational tool. Despite challenges such as high equipment costs and large data-processing demands, the market continues to expand due to growing applications in defense modernization, smart manufacturing, and medical diagnostics. The global market share is expected to maintain double-digit growth over the next decade as miniaturization, AI integration, and edge computing make spectral sensing more affordable and accessible.

Key players driving innovation in hyperspectral imaging include Headwall Photonics, Specim (Spectral Imaging Ltd.), Resonon, Corning Incorporated, BaySpec Inc., IMEC, and Cubert GmbH. These companies are leading advancements in compact sensor design, AI-based spectral analytics, and defense-grade imaging solutions. Additionally, aerospace giants such as Lockheed Martin and Northrop Grumman are incorporating HSI into reconnaissance and spaceborne observation systems, while startups are developing affordable drone-based platforms for industrial and agricultural use.

Download Free sample to learn more about this report.

IMPACT OF RUSSIA-UKRAINE WAR

Russia-Ukraine War Accelerated Defense Modernization and Surveillance Investments Using Hyperspectral Imaging

The Russia-Ukraine war has significantly accelerated the adoption of hyperspectral imaging (HSI) technologies within the global aerospace and defense ecosystem. The conflict exposed critical gaps in conventional surveillance and target identification systems, emphasizing the need for advanced spectral analytics capable of detecting hidden, camouflaged, or electronically masked threats. Both NATO and allied forces have increased investments in airborne and satellite-based hyperspectral payloads to enhance situational awareness and real-time battlefield monitoring. HSI systems have proven valuable in distinguishing between decoys and active weapon systems, monitoring troop movements, detecting thermal and chemical signatures, and assessing infrastructure damage. The war also pushed the development of small satellite constellations equipped with hyperspectral sensors, providing persistent and wide-area coverage over conflict zones.

On the industrial side, the heightened defense budgets across Europe and North America have revived R&D funding for compact, ruggedized hyperspectral sensors suitable for drones, ground vehicles, and aircrafts. Ukraine’s need for rapid intelligence gathering has led to collaborations between defense tech startups and Western sensor developers, fast-tracking field-deployable imaging solutions. However, supply chain disruptions especially in semiconductor components and optical materials sourced from Eastern Europe have temporarily slowed production. Overall, the Russia-Ukraine war has redefined hyperspectral imaging as a strategic defense enabler, shifting its perception from a scientific tool to a core element of 21st-century ISR (Intelligence, Surveillance, and Reconnaissance) architecture focused on precision, autonomy, and resilience in modern warfare.

Hyperspectral Imaging Market Trends:

Growing Integration of Hyperspectral Imaging in Next-Generation Defense and Space Systems to Accentuate Market Growth

In the aerospace and defense sector, the hyperspectral imaging market growth is evolving rapidly as forces globally integrate spectral intelligence into surveillance, reconnaissance, and space-based observation platforms. HSI provides unique capabilities by detecting subtle spectral signatures of materials allowing operators to distinguish between real and camouflaged targets, identify chemical or explosive residues, and track environmental changes. The trend is strongly shaped by the deployment of spaceborne and airborne hyperspectral sensors mounted on UAVs, satellites, and manned aircraft, which offer continuous situational awareness across large territories.

Advances in SWIR (Short-Wave Infrared) and MWIR (Mid-Wave Infrared) sensors are expanding spectral coverage, improving target identification in low-visibility or night-time operations. Militaries are also integrating HSI with AI-based target recognition and automatic threat classification systems, reducing reliance on manual image interpretation. Parallelly, civil space agencies (such as NASA, ESA, and ISRO) are launching high-resolution hyperspectral satellites for earth observation, disaster response, and mineral mapping, technologies that often spill over into defense applications. The trend thus points to multi-domain integration combining air, space, and ground-based hyperspectral sensing to enable real-time, data-driven situational intelligence.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET OPPORTUNITIES

Expansion into Spaceborne Surveillance, Smart Warfare, and Predictive Maintenance to Accentuate Market Growth

The aerospace and defense hyperspectral imaging market holds immense opportunity in the integration of HSI into next-generation satellite constellations, unmanned systems, and predictive maintenance ecosystems. Spaceborne hyperspectral sensors are increasingly used for continuous global monitoring detecting missile launches, oil spills, or illegal mining through unique spectral emissions. The opportunity expands as governments and private players deploy small satellites and CubeSats equipped with miniaturized HSI payloads, offering cost-effective surveillance and reconnaissance. In smart warfare, HSI can be integrated into autonomous UAVs and combat analytics systems to provide machine-vision-level threat assessment in real-time.

Another emerging opportunity lies in aerospace manufacturing, where hyperspectral imaging can detect micro-defects in composite materials, fuel leaks, or corrosion before failures occur enhancing aircraft reliability and mission safety. The defense sector’s shift toward AI-enabled, sensor-fused networks aligns perfectly with HSI’s strengths in multi-domain awareness and data fusion. As advancements in AI, sensor miniaturization, and spectral computing continue, hyperspectral imaging is set to become a cornerstone of modern aerospace surveillance and operational readiness.

MARKET DRIVERS

Rising Need for Advanced Intelligence, Surveillance, and Reconnaissance (ISR) Capabilities to Boost Market Growth

The main driver for hyperspectral imaging adoption in aerospace and defense is the increasing need for real-time, high-fidelity intelligence in complex combat and border environments. Unlike conventional imaging, which relies on shape and color, hyperspectral imaging identifies materials based on their spectral signatures, enabling detection of concealed objects, disturbed soil (indicative of hidden explosives), or disguised military vehicles. Modern conflicts emphasize asymmetric and hybrid warfare, where HSI can detect threats that evade traditional sensors.

Defense organizations are investing in airborne hyperspectral payloads for reconnaissance drones and manned aircraft, providing wide-area spectral coverage for both strategic and tactical missions. Space agencies are integrating HSI sensors into satellites for long-term monitoring of terrain, ocean, and atmospheric conditions that support both civilian and defense planning. In aerospace manufacturing, hyperspectral techniques are increasingly used for composite material inspection, coating uniformity, and defect detection, improving aircraft safety and reducing maintenance costs. Collectively, the demand for high-resolution spectral analytics to strengthen ISR and aerospace quality assurance systems is a powerful growth driver in this domain.

MARKET RESTRAINTS

High Development Cost, Complex Data Interpretation, and Limited Field Deployability to Hamper Market Growth

Despite its promise, hyperspectral imaging adoption in aerospace and defense faces several structural restraints. The high cost of developing ruggedized, military-grade sensors limits deployment, particularly for smaller defense forces or emerging economies. Hyperspectral payloads require precise calibration, temperature control, and vibration resistance to function in harsh aerospace environments, increasing system complexity. Another major restraint lies in the volume and complexity of hyperspectral data; each mission can generate terabytes of spectral information that must be processed rapidly for actionable intelligence.

Current ground-based systems often lack the bandwidth and computational efficiency for real-time analysis, delaying decision-making. Additionally, integrating hyperspectral sensors with existing ISR architectures (such as radar, LiDAR, and thermal imaging) requires substantial software and hardware synchronization. Operational challenges such as atmospheric distortion, sensor drift, and limited onboard processing power also affect data reliability. Until miniaturization, edge computing, and cost-effective production advance further, these constraints will continue to restrict widespread deployment of HSI in frontline aerospace and defense missions.

MARKET CHALLENGES

Standardization, Real-Time Processing, and Secure Data Management Are Major Market Challenges

The market in aerospace and defense faces multiple implementation challenges tied to data standardization, real-time processing, and security management. Different defense contractors and sensor manufacturers use varying calibration techniques, leading to inconsistencies in spectral data across systems. Lack of standardized spectral libraries for materials and camouflage coatings limits interoperability between allied forces or multinational missions. The sheer volume of hyperspectral data makes real-time transmission and analysis challenging, especially from UAVs or satellites operating with limited bandwidth.

Onboard AI-based compression and processing are still under development, making near-instant threat detection difficult in combat environments. Additionally, security concerns around classified hyperspectral datasets hinder collaborative analysis and technology transfer between nations. The challenge also extends to developing durable, lightweight sensors suitable for high-altitude, long-endurance platforms, where size, weight, and power (SWaP) constraints are critical. Addressing these issues will require advances in universal calibration protocols, onboard computing, and secure spectral data frameworks to make HSI a reliable and interoperable defense technology.

SEGMENTATION ANALYSIS

By End-Use

Defense Sector Drives Hyperspectral Imaging Adoption for Surveillance and Target Detection

By end-use, the market is segmented into food & beverages, healthcare & pharmaceutical defense, chemical, and others.

The defense segment led the market accounting for 30.71% market share in 2026. The defense segment drives significant demand for hyperspectral imaging, as militaries use it for target detection, camouflage identification, and battlefield surveillance. Airborne, satellite, and UAV-mounted HSI systems provide real-time intelligence, enhancing situational awareness and strategic planning. Increasing defense modernization programs globally continue to boost segment growth.

The food & beverages segment is expected to grow at a CAGR of 13.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Military Surveillance Fuels Real-Time Hyperspectral Imaging Deployment

The application segment is classified into process control, manufacturing, quality assurance, military surveillance, remote sensing, and others.

The military surveillance segment captured the largest share of 22.93% the market in 2026. The military surveillance segment will account for 22.93% market share in 2026. The military surveillance segment is a key driver of hyperspectral imaging adoption, leveraging high-resolution spectral data for target detection, threat assessment, and reconnaissance missions. UAVs, aircraft, and satellites equipped with HSI sensors enable real-time battlefield monitoring, camouflage detection, and terrain analysis. Growing defense modernization and ISR requirements are fueling demand.

The quality assurance segment is expected to grow at a CAGR of 13.8% over the forecast period.

By Technology

Pushbroom/Line Scan Leads in High-Resolution and Large-Area Imaging Applications

The technology segment is classified into pushbroom/line scan, snapshot, and other technologies.

The pushbroom/line scan segment is anticipated to hold a dominant market share of 59.03% in 2026. The pushbroom/line scan segment dominates hyperspectral imaging demand due to its high spectral and spatial resolution, making it ideal for airborne, satellite, and UAV applications. It is widely used in defense reconnaissance, environmental monitoring, and precision agriculture, where large-area imaging and detailed spectral analysis are critical.

The snapshot segment is expected to grow at a CAGR of 13.1% over the forecast period.

By Product

Cameras Segment Leads Due to Hyperspectral Cameras Remain Core to Multi-Sector Data Acquisition

By product, the market is classified into cameras and accessories.

The cameras segment will account for 74.61% market share in 2026. The cameras segment accounts for the largest demand in hyperspectral imaging, as cameras serve as the core sensing component for data acquisition. High-resolution hyperspectral cameras are essential for defense surveillance, aerospace observation, medical diagnostics, and industrial inspection, driving adoption across UAVs, satellites, and laboratory platforms.

The accessories segment is expected to grow at a CAGR of 13.1% over the forecast period.

HYPERSPECTRAL IMAGING MARKET REGIONAL OUTLOOK

In terms of region, the market is divided into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Hyperspectral Imaging Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 33.19% to the global market in 2025, with a valuation of USD 86.1 million, and is expected to reach USD 96.3 million in 2026. North America dominates the hyperspectral imaging market due to strong defense investments, advanced aerospace programs, and growing use in healthcare and agriculture. The U.S. leads demand, driven by intelligence, surveillance, and environmental monitoring needs, alongside active R&D by leading sensor manufacturers and research institutions.

The U.S. exhibits the highest global demand for hyperspectral imaging, driven by defense, aerospace, and healthcare applications. Strong R&D funding from DARPA, NASA, and the Department of Defense supports advanced airborne and satellite HSI systems. Industrial applications in food safety, pharmaceuticals, and environmental monitoring are also rapidly expanding. The U.S. market is valued at USD 79.1 million by 2026.

Europe

Europe accounted for USD 63.7 million in 2025, representing 24.57% of the global market share, and is expected to reach USD 71.9 million in 2026. Europe’s demand for hyperspectral imaging is fueled by environmental monitoring, precision agriculture, and defense modernization programs. Countries such as Germany, France, and U.K. are integrating HSI into satellite observation, food safety, and industrial inspection systems, supported by strong EU initiatives on sustainable resource and security technologies. The UK market is valued at USD 14.1 million by 2026, while the Germany market is valued at USD 18.7 million by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 75.8 million in 2025, capturing 29.23% of global revenue, and is estimated to reach USD 86.5 million in 2026. The Asia Pacific market is expanding rapidly with increasing government investments in remote sensing, agriculture, and defense. China, Japan, and India are deploying hyperspectral systems for spaceborne earth observation, pollution tracking, and smart city applications. The region shows the fastest growth due to industrial digitization and technology localization efforts. The Japan market is valued at USD 17.7 million by 2026, the China market is valued at USD 46.3 million by 2026, and the India market is valued at USD 14.2 million by 2026.

Rest of the World

The Rest of the World region captured 13.01% of the global market in 2025, generating USD 33.7 million in revenue, and is projected to reach USD 37.7 million in 2026. In the Middle East, hyperspectral imaging demand is rising for border surveillance, defense intelligence, and oil exploration. Countries such as the UAE, Israel, and Saudi Arabia are adopting HSI systems for terrain mapping, military reconnaissance, and resource management, driven by defense modernization and security-driven technological diversification. Africa’s hyperspectral imaging adoption is primarily concentrated in agriculture, mining, and environmental conservation. Nations such as South Africa and Kenya are exploring HSI for mineral mapping, crop analysis, and water management. Growing partnerships with European and Asian technology providers are fostering regional research capabilities and pilot deployments. Latin America’s demand is led by Brazil, Chile, and Mexico, focusing on agriculture, forestry, and environmental monitoring. HSI is increasingly used for crop disease detection, deforestation assessment, and mineral exploration. Expanding space research initiatives and government sustainability programs are further driving hyperspectral imaging adoption in the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Expanding Market Growth through Advanced Payload Innovation and Defense Modernization

The hyperspectral imaging (HSI) market is transforming industries through its ability to capture detailed spectral information across hundreds of wavelengths, enabling precise detection, identification, and analysis of materials and surfaces. Originally used in scientific research, HSI is now widely adopted in defense, aerospace, agriculture, healthcare, and industrial inspection. Its integration with AI and machine learning has accelerated applications in real-time monitoring, quality control, and reconnaissance. Growing demand for non-destructive testing, environmental monitoring, and advanced surveillance systems continues to drive market expansion. Technological progress in miniaturized sensors, SWIR imaging, and onboard spectral computing is enhancing accessibility and deployment flexibility. As global industries move toward intelligent and data-driven operations, hyperspectral imaging stands out as a key enabler of precision, automation, and situational awareness.

LIST OF KEY HYPERSPECTRAL IMAGING COMPANIES PROFILED:

- Headwall Photonics, Inc. (U.S.)

- Specim, Spectral Imaging Ltd. (Finland)

- Resonon Inc. (U.S.)

- IMEC (Belgium)

- BaySpec Inc. (U.S.)

- Cubert GmbH (Germany)

- Corning Incorporated (U.S.)

- Telops Inc. (Canada)

- Norsk Elektro Optikk AS (NEO) (Norway)

- Surface Optics Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2025 - Pixxel has signed the iDEX SPARK Grant Agreement to create Hyperspectral and MWIR Payloads for the Indian Air Force.

- June 2025 - Pixxel, a hyperspectral imaging and Earth observation firm based in India, has secured a contract from NASA as part of its USD 476 million Commercial SmallSat Data Acquisition Program. Pixxel is the most recent company in a cohort of established firms.

- February 2025 - HySpex has obtained a contract for hyperspectral cameras with the European Space Agency. The objective is to enhance the accessibility of methane detection technology through a readily available satellite imaging payload.

- December 2023 - The National Reconnaissance Office has declared that it has entered into agreements with five commercial suppliers of electro-optical satellite imagery, which includes four startups that are in the initial stages of developing their constellations. Airbus U.S. Space and Defense, Albedo Space, Hydrosat, Muon Space, and Turion Space have been chosen for the NRO’s Strategic Commercial Enhancements program.

- March 2023 - The National Reconnaissance Office has entered into five-year contracts with six commercial suppliers of hyperspectral satellite imagery, as announced by the agency. The chosen companies include BlackSky Technology, HyperSat, Orbital Sidekick, Pixxel, Planet, and Xplore, representing a combination of well-established firms in the remote-sensing industry and emerging startups.

REPORT COVERAGE

The research report regarding the expansion of the hyperspectral imaging market provides an in-depth analysis by identifying the key companies, product categories, and main applications within the industry. Additionally, the report highlights market trends and notable developments in this field. In conjunction with the aforementioned aspects, the report includes several factors that have contributed to the rapid market growth witnessed in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.11% from 2026-2034 |

| Unit | Value (USD Million) |

|

Segmentation |

By Application

|

|

By Technology

|

|

|

By Product

|

|

|

By End-Use

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 292.5 million in 2026 and is estimated to reach USD 729.9 million by 2034.

The market is growing at a CAGR of 12.11% during the forecast period.

The defense segment is estimated to be the leading end-use sub-segment in this market during the forecast period.

The pushbroom/line scan segment is estimated to be the leading technology sub-segment in this market during the forecast period.

Headwall Photonics, Inc. (U.S.), Specim, Spectral Imaging Ltd. (Finland), Resonon Inc. (U.S.), IMEC (Belgium), BaySpec Inc. (U.S.), and Cubert GmbH (Germany) are some of the leading players in the market.

North America is projected to be the largest shareholder in the market.

- 2021-2034

- 2025

- 2021-2024

- 123

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us