Short-wave Infrared (SWIR) Imaging Market Size, Share & Industry Analysis, By Technology (Cooled and Uncooled), By Wavelength Range (0.9 – 1.7 μm and 1.7 – 2.5 μm), By Application (Surveillance & Security, Imaging & Inspection, Hyperspectral Imaging, Crop & Food Quality Monitoring, and Others), By Component (Sensors, Optics, Electronics, and Other Systems) By Vertical (Aerospace and Defense, Automotive, Healthcare, Industrial, and Others), and Regional Forecast, 2026-2034

Short-wave Infrared (SWIR) Imaging Market Size and Future Outlook

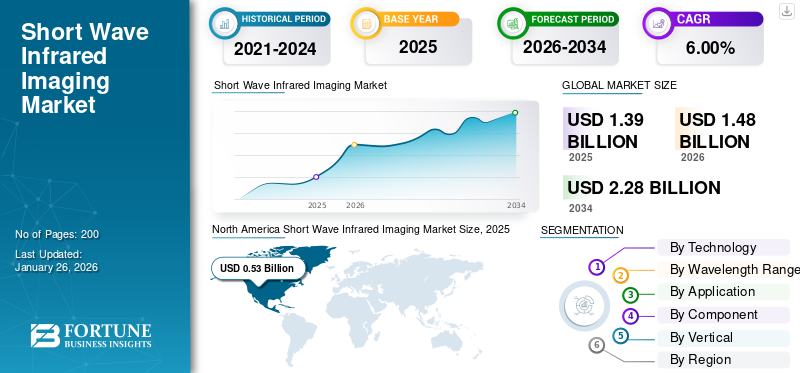

The global short wave infrared imaging market size was valued at USD 1.39 billion in 2025 and is projected to grow from USD 1.48 billion in 2026 to USD 2.28 billion by 2034, exhibiting a CAGR of 6.00% during the forecast period. North America dominated the short wave infrared imaging market with a market share of 37.60% in 2025.

Short-wave infrared (SWIR) imaging is a technique that captures images using infrared light in the 0.9 to 1.7-micron wavelength range, which is invisible to human eye. It can be used for various applications such as surveillance, inspection, and quality control. Infrared imaging is able to penetrate materials and operate in low-light conditions. Thus, it is used for various applications in different industries such as biomedicine and healthcare for surgical guidance and diagnostics, military for night vision and surveillance, and industry for material inspection and agricultural monitoring. SWIR imaging is widely used in fields such as scientific research, biological studies, and semiconductor inspection.

Key government & space agencies involved in the market include NASA, the European Space Agency (ESA), and DARPA, which fund various projects and missions leveraging SWIR technology for applications such as planetary exploration, environmental monitoring, and defense imaging. Moreover, private key players such as Teledyne Imaging, Sensors Unlimited, and FLIR Systems are developing advanced SWIR cameras and sensors for industrial inspection, agriculture, security, and scientific research.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Increase in Demand for SWIR Imaging in Defense Sector for Surveillance & Target Detection Drives Market Growth

Short wave infrared (SWIR) imaging is very essential in modern defense applications. It is increasingly being used in defense sectors as it offers various benefits for surveillance, target detection, and operational efficiency.

Moreover, SWIR provides other advantages over visible light imaging such as its ability to operate in the 1000–2000 nm wavelength range. Such ability allows it to penetrate challenging environments such as fog, haze, smoke, and dust. This capability is particularly valuable for military operations in adverse weather conditions or low-visibility scenarios. Thermal imaging applications are gaining traction in defense sectors, providing superior visibility in challenging conditions, which increases their demand.

One of SWIR's key benefits in defense is its ability to deliver high-contrast images. In addition, SWIR technology is versatile across defense platforms, comprising drones, helicopters, tanks, and surveillance systems used for border monitoring and battlefield reconnaissance and other applications.

- For instance, in February 2023, the U.S. Air Force, through its AFWERX office, awarded Princeton Infrared Technologies a USD 749,961 SBIR Phase II contract to develop extended-wavelength shortwave infrared (SWIR) sensors for hyperspectral imaging aboard unmanned aerial vehicles (UAVs).

Additionally, recent advancements in materials such as HgCdTe and InGaAs have improved the efficiency, compactness, and performance of SWIR systems for military applications which is probable to drive the short-wave infrared (SWIR) imaging market growth.

MARKET RESTRAINTS:

High Cost Associated with SWIR Technology Implementation to Restrict Market Expansion

The manufacturing of SWIR image sensors and cameras involves intricate processes that require specialized materials, such as Indium Gallium Arsenide (InGaAs) and Mercury Cadmium Telluride (MCT), which are both expensive. This complexity leads to higher production costs, making SWIR systems considerably costlier than traditional imaging technologies. As a result, the high price point can deter potential buyers, especially in price-sensitive sectors such as consumer electronics and small-to-medium enterprises.

Many organizations may find it challenging to justify the investment in SWIR technology when cheaper alternatives are available. Consequently, this financial barrier limits the broader adoption of SWIR imaging solutions across various industries. Until advancements in manufacturing techniques decrease costs, the high expense will continue to hinder market growth and accessibility.

MARKET OPPORTUNITIES:

Increase in Adoption in Precision Agriculture to Create Lucrative Growth Opportunities

The use of shortwave infrared (SWIR) imaging in agriculture is expected to drive market growth due to its ability to optimize farming practices and improve crop yields. SWIR technology enables farmers to monitor plant health by detecting water stress, nutrient deficiencies, and diseases early, allowing for timely interventions. Its capability to analyze soil moisture and salinity further enhances resource allocation, reducing water usage and promoting sustainable farming. SWIR imaging systems can distinguish subtle differences in crop conditions, even under low-light or adverse weather conditions, providing continuous monitoring of large agricultural areas.

- For instance, in 2024, the Indian Space Research Organization (ISRO) and the French Space Agency (CNES) are collaboratively developing the TRISHNA (Thermal Infrared Imaging Satellite for High-resolution Natural Resources Assessment) mission. It aims to provide high-resolution thermal and shortwave infrared data for global natural resource monitoring, including applications in agriculture.

MARKET CHALLENGES:

Integration and Compatibility Issues with Existing Systems to Hamper Market Growth

A significant challenge faced by SWIR market is the integration of SWIR sensors and imaging technologies with existing infrastructure and data processing systems. Numerous industries, such as defense, industrial inspection, and medical imaging, are dependent on legacy hardware and software optimized for visible or thermal imaging. The incorporation of SWIR devices in already installed systems needs customized interfaces, new calibration standards, and updated analytical tools. Therefore, this is expected to increase the complexity and deployment time. Thus, decreasing the speed of adoption because of integration & compatibility issues is anticipated to hinder market expansion.

SHORT-WAVE INFRARED (SWIR) IMAGING MARKET TRENDS:

Miniaturization of SWIR Cameras is a Significant Market Trends

A major trend in the SWIR market for defense is the miniaturization of SWIR cameras, making them lighter, more compact, and energy-efficient. This allows easy integration into handheld devices, soldier helmets, UAVs, and vehicle-mounted systems, providing troops with advanced night vision, surveillance, and target detection capabilities even in challenging conditions such as smoke, dust, or fog. The ability to deploy SWIR imaging across diverse platforms enhances real-time situational awareness and mission flexibility, driving strong market growth as militaries seek to modernize and equip forces with cutting-edge, portable sensing technologies.

Download Free sample to learn more about this report.

Segmentation Analysis

By Technology

Affordability, Compact Designs, and Energy Efficiency of Uncooled Infrared Imaging Contributes to Segmental Growth

Based on technology, the market is divided into cooled infrared imaging, and uncooled infrared imaging.

The uncooled infrared imaging segment accounted for the larger share of the market in 2024. Uncooled shortwave infrared (SWIR) imaging is gaining traction primarily due to its cost-effectiveness as these cameras eliminate the need for expensive cooling systems, making them more accessible across various industries. Their portability and flexibility allow for its integration into compact platforms such as drones and handheld devices, enhancing their usability.

Moreover, the cooled infrared imaging is expected to grow with highest CAGR during the forecast period. Cooled shortwave infrared (SWIR) imaging is experiencing growth due to its superior image sensitivity, which enhances detector performance in low-light or long-range conditions. This capability makes cooled SWIR cameras essential for advanced military applications, such as surveillance and reconnaissance, where detecting distant objects and hidden threats is critical. Additionally, their high thermal sensitivity supports various scientific and industrial applications.

For instance, in October 2023, Omron Automation announced the launch of a new SWIR camera series featuring advanced shortwave infrared technology that enhances precision in manufacturing inspections across industries such as food, commodities, and semiconductors. The camera is equipped with fanless Peltier cooling design which is used to dissipate heat and provide cooling.

By Wavelength Range

Strong Industrial Adoption Fuels Growth of 0.9 – 1.7 μm Segment

In terms of wavelength range, the market is categorized into 0.9 – 1.7 μm, and 1.7 – 2.5 μm.

The 0.9 – 1.7 μm segment captured the largest share of the market in 2024. The wide adoption of the 0.9 to 1.7 μm in industrial inspection, semiconductor manufacturing, and food processing drives the segment growth. The following range has the ability to penetrate silicon which enables wafer inspection and its importance in quality control in agriculture and packaging. Such factors are driving the dominance of this segment in the market.

The 1.7 – 2.5 μm segment is expected to record fastest CAGR during the forecast period. Its capability to detect water absorption bands and gases makes it highly effective for defense surveillance, hyperspectral imaging, and environmental monitoring. This range supports mineral exploration, chemical detection, and climate observation, which aligns with growing government and commercial investments in remote sensing technologies.

By Application

Rise in Defense Investment to Strengthen Defense Capabilities Propelled Segment Growth

Based on application, the market is segmented into surveillance & security, imaging & inspection, hyperspectral imaging, crop & food quality monitoring, and others.

The surveillance & security segment accounted for the largest short-wave infrared (SWIR) imaging market share due to rise in demand for SWIR cameras for border security, military surveillance, and critical infrastructure monitoring. The SWIR cameras are used in military to capture high resolution images in low-light and harsh weather situations. Government across the world are increasingly investing in advanced vision systems to improve defense capabilities & situational awareness and threat detection.

- For instance, in April 2023, Quantum Imaging launched its next-generation SWIR camera, MIRA 02Y-E, at the SPIE Defense + Commercial Sensing conference. The camera is optimized for defense applications.

In 2024, crop & food quality monitoring segment is expected to grow with the fastest CAGR in the market, due to increasing use of SWIR technology for detection of moisture levels, ripeness, and contamination in crops and packaged food. It is extensively used in food industry to ensure the quality and safety standards are upheld. Moreover, as there is increasing emphasis on sustainable farming and food security, this is expected to push the adoption of SWIR-based inspection systems across agriculture and processing industries.

- For instance, in March 2024, Tomra Food introduced an upgraded optical sorting platform integrating SWIR sensors to detect defects and foreign materials in fruits and vegetables.

To know how our report can help streamline your business, Speak to Analyst

By Component

Rise in Demand for Advanced Imaging Capabilities Is Expected to Drive Segment Growth

Based on component, the market is divided into sensors, optics, electronics, and other systems. The sensors segment is further classified into Indium gallium arsenide, indium antimonide, lead sulfide, mercury cadmium telluride, and others.

The sensors segment holds the largest share in 2024 due to rise in demand for high performance sensors with the expansion of surveillance, semiconductor inspection, and food monitoring. The sensors are the critical component of SWIR systems. It allows imaging across various sectors including defense, industrial, and others by capturing detailed information beyond the visible spectrum. In addition, the increase in design and development of SWIR sensors with advanced features is expected to propel segment growth.

- For instance, in September 2023, Lynred France-based infrared detectors manufacturer announced the development of a new generation of SWIR sensors with enhanced sensitivity and reduced pixel pitch, precisely designed for defense and industrial machine vision applications.

The optics segment holds the second largest share in the market. Optics, including specialized lenses and filters, are essential for ensuring image clarity, wavelength selectivity, and system efficiency in SWIR cameras. With growing adoption in defense targeting systems, hyperspectral imaging, and industrial inspection, the need for high-precision optics is increasing.

- For instance, in September 2025, Edmund Optics expanded its SWIR imaging portfolio, offering a complete in-stock ecosystem of cameras, optics, illumination, filters, and accessories from a single supplier.

By Vertical

Rise in Demand in Aerospace for Atmospheric Sensing & Increase in Defense Modernization Programs Is Expected to Drive Segment Growth

Based on vertical, the market is divided into aerospace & defense, automotive, healthcare, industrial, and others.

The aerospace & defense segment holds the largest share in 2024 driven by the ability of SWIR technology to penetrate atmospheric conditions such as fog, haze, and smoke, ensuring clear imaging for satellites and aircraft. SWIR sensors are used in hyperspectral imaging to detect gases, chemicals, and materials on the Earth's surface. The segment growth is driven by expanding application of short wave infrared imaging in atmospheric sensing, and driving adoption in both space exploration and commercial sectors.

• For instance, in April 2024, Princeton Infrared Technologies, Inc. (PIRT) was awarded a Phase I SBIR contract by NASA to develop an advanced shortwave infrared (SWIR) imager with a 640x512 resolution array and a 24-bit linear high dynamic range (HDR), capable of detecting wavelengths from 400 to 3000 nm.

The automotive segment held the second-largest share of the SWIR market in 2024. Automakers are adopting SWIR cameras for advanced driver-assistance systems (ADAS), autonomous vehicle navigation, and quality inspection during manufacturing.

- For instance, in June 2023, Coherent and TriEye jointly developed a laser-illuminated shortwave infrared (SWIR) imaging system for automotive and robotic applications, combining TriEye’s SEDAR platform with Coherent’s SWIR semiconductor laser.

Short-wave Infrared (SWIR) Imaging Market Regional Outlook

By Geography

The Market is Categorized into North America, Europe, Asia Pacific, and Rest of the World.

North America

In 2025, North America represented USD 0.53 billion, accounting for 37.60% of the worldwide market, and is projected to grow to USD 0.55 billion in 2026. SWIR imaging is widely adopted for military and border security applications in North America due to its ability to provide high-resolution images in low-light conditions, penetrate fog and smoke, and detect distant targets. This is mainly crucial for night-time vision and covert operations such as military IR laser spotting and tracking. Moreover, the U.S., with the largest defense budget globally, heavily invests in SWIR technology for surveillance, target acquisition, and reconnaissance.

- For instance, in February 2024, Leonardo DRS selected Quantum Imaging’s MIRA SWIR camera, featuring the SWIFT-EI detector, for the US Army’s Joint Effects Targeting System II (JETS II) during its engineering and manufacturing development phase.

Europe

The Europe market generated USD 0.26 billion in 2025, representing 26.90% of the global market landscape, and is expected to reach USD 0.17 billion in 2026. SWIR imaging is widely used in European industries for detecting surface defects, inspecting electronic components, and assessing moisture content in raw materials. For example, Germany, with its robust industrial base, leads the adoption of SWIR for automation and quality assurance in manufacturing processes. The increasing industrial production across the EU has created a growing demand for advanced technologies such as SWIR to improve efficiency and safety in manufacturing.

- For instance, in October 2023, Omron Automation launched a new SWIR camera series featuring Sony Pregius sensors and fanless Peltier cooling, enabling precision inspection in food, commodity, and semiconductor industries by overcoming challenges such as ambient lighting and intrusive post-manufacturing inspections.

Asia Pacific

Asia Pacific contributed 24.10% to the global market in 2025, with a valuation of USD 0.15 billion, and is projected to reach USD 0.18 billion in 2026. SWIR imaging is increasingly used in industries such as electronics and semiconductors for quality control and defect detection. Countries such as China, Japan, and South Korea, known for their advanced manufacturing sectors, are adopting SWIR cameras to enhance precision and efficiency.

For instance, in July 2024, Sony Semiconductor Solutions (Japan) announced advancements in its CMOS-based SWIR image sensors, expanding industrial inspection applications in semiconductor and electronics manufacturing.

This advancement makes SWIR imaging more accessible for sectors such as manufacturing and security, driving market growth through affordability and adaptability in imaging solutions. In addition, SWIR technology is increasingly being utilized for monitoring and quality control in chemical manufacturing and agriculture, motivating growth of SWIR imaging market in the region.

During the forecast period, SWIR imaging adoption in Latin America is gaining traction, particularly in agriculture, food quality monitoring, and mining industries. Countries in the region such as Brazil, Chile, and Mexico are making use of SWIR cameras to improve crop inspection, detect moisture levels, and support mineral exploration in the mining sector. Moreover, there is an growing focus on the improvement of food export standards and usage of hyperspectral imaging for resource extraction. All these factors are expected to drive the growth of market in the Latin America region.

Middle East & Africa

In the Middle East & Africa, SWIR adoption is being driven by defense modernization, oil & gas inspection, and infrastructure security. Countries such as UAE, Saudi Arabia, and South Africa are investing in SWIR-based surveillance systems for border control, facility monitoring, and industrial safety.

- For instance, in March 2025, the UAE’s EDGE Group announced trials of SWIR-enabled surveillance systems integrated into unmanned aerial vehicles (UAVs) for border security and critical infrastructure protection.

Rest of the World

Rest of the World contributed approximately USD 0.08 billion to the global market in 2025, accounting for 11.30% share, and is expected to reach USD 0.09 billion in 2026.

North America Short Wave Infrared Imaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

COMPETITIVE LANDSCAPE

Key Industry Players:

Technological Innovation, Product Launches, and Strategic Partnerships Supports Market Expansion of Key Players

The global market is being shaped by increased demand across defense, industrial manufacturing, agriculture, and scientific research applications. The factors for the growth of market are continuous technological innovation in sensors, optics, and camera systems. Moreover, there is increase in public-private collaborations aimed at improving imaging capabilities and reducing costs driving market growth during the forecast period. In addition, the key players in this market include Lynred, Teledyne FLIR, Hamamatsu Photonics, Sensors Unlimited (a Collins Aerospace company), Sony Semiconductor Solutions, Xenics, TriEye, and Allied Vision. These companies contribute to the industry as they are focusing on advanced sensor development, high-performance cameras, and incorporation into mission-critical systems.

Companies are providing a wide range of SWIR solutions, such as InGaAs and CMOS-based sensors, low-SWaP-C cameras, hyperspectral imaging systems, and specialized optics. To expand their market presence, these players are investing heavily in R&D for high-speed detectors, cost-effective CMOS alternatives, AI-enabled image processing, and multi-wavelength imaging technologies. In addition, strategic collaborations between component manufacturers and system integrators are accelerating the commercialization of SWIR imaging.

LIST OF KEY SHORT-WAVE INFRARED (SWIR) IMAGING COMPANIES PROFILED:

- Lynred (France)

- Teledyne FLIR (U.S.)

- Hamamatsu Photonics (Japan)

- Sensors Unlimited (Collins Aerospace) (U.S.)

- Sony Semiconductor Solutions (Japan)

- Xenics (part of Exosens) (Belgium)

- Allied Vision (Germany)

- TriEye (Israel)

- Raptor Photonics (U.K.)

- New Imaging Technologies (NIT) (France)

KEY INDUSTRY DEVELOPMENTS:

- July 2025: Allied Vision introduced its new Goldeye Pro series of SWIR cameras featuring Sony’s IMX992/993 SenSWIR sensors with thermo-electric cooling (TEC1).

- January 2025: Raptor Photonics expanded its SWIR portfolio with the launch of the Owl 2560 Vis-SWIR camera at Photonics West, the highest-resolution InGaAs camera on the market with a 5.2MP back-illuminated sensor covering 400–1700 nm.

- August 2024, Teledyne FLIR IIS launched the Forge 1GigE SWIR camera series, featuring Sony's SenSWIR IMX990 sensor, which captures images across both visible and SWIR spectrums. This new camera excels in applications such as industrial inspection, quality control, and environmental monitoring due to its enhanced anomaly detection capabilities.

- July 2024, Onsemi acquired SWIR Vision Systems, a North Carolina-based startup specializing in short-wave infrared (SWIR) sensors and cameras using colloidal quantum dot (CQD) technology. The acquisition enhances onsemi's sensing portfolio by providing access to low-cost, high-resolution infrared sensors that extend silicon CMOS detection to around 2 μm wavelengths.

- April 2024, NIT (New Imaging Technologies) introduced the NSC2101, a high-resolution SWIR InGaAs sensor designed for demanding applications. Featuring an 8µm pixel pitch, 2MP resolution (1920x1080px), ultra-low noise of 25e-, and a dynamic range of 64dB, it operates within a spectral range of 0.9µm to 1.7µm. Designed and manufactured in France, the sensor is ideal for ISR, semiconductor inspection, and other precision imaging applications.

REPORT COVERAGE

The global market demand analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics, and market trends expected to drive the market in the forecast period. Market analysis includes porters five forces analysis which illustrates the potency of buyer and suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The The market report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forcast Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.00% from 2026-2034 |

| Unit | Value (USD Million) |

|

By Technology

By Wavelength Range

By Application

By Component

By Vertical

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 1.48 billion in 2026 to USD 2.28 billion by 2034

In 2025, the market value stood at USD 0.53 billion.

The market is expected to exhibit a CAGR of 6.00% during the forecast period of 2026-2034.

The uncooled segment led the market by technology.

The key factors driving the market are growth of market are rise in demand for short wave infrared imaging in defense sector for surveillance & target detection.

Lynred (France), Teledyne FLIR (U.S.), Hamamatsu Photonics (Japan) and others are some of the prominent players in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us