Air Pollution Control Systems Market Size, Share & Industry Analysis, By Technology (Electrostatic Precipitators, Fabric Filters, Scrubbers, Selective Catalytic Reduction, Thermal & Catalytic Oxidizers, and Others), By Pollutant Type (Particulate Pollutants, Gaseous Pollutants, Organic & Toxic Pollutants, and Others), By Industry (Power Generation, Cement & Metal Processing, Chemical & Petrochemical, Oil & Gas, Waste Incineration/WtE, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

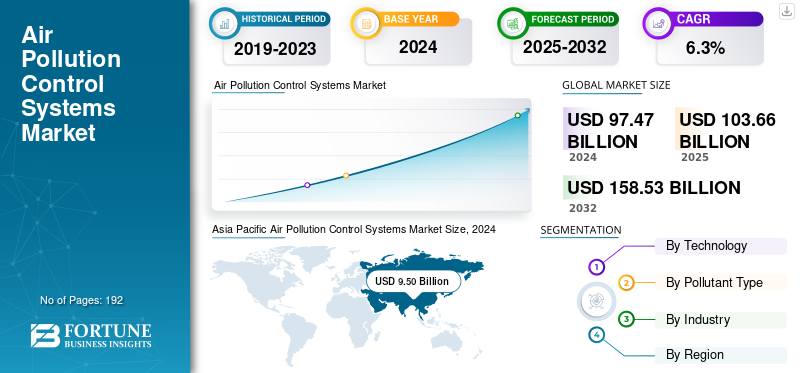

The global air pollution control systems market size was valued at USD 103.66 billion in 2025. The market is projected to grow from USD 110.12 billion in 2026 to USD 179.21 billion by 2034, exhibiting a CAGR of 6.30% during the forecast period. Asia Pacific dominated the air pollution control systems market with a market share of 38.20% in 2025.

Air pollution control systems consist of devices and technologies used to reduce or remove pollutants before being released into the atmosphere from a facility or industrial facility. Examples of common types are baghouses and electrostatic precipitators designed to capture airborne particulate matter, and scrubbers and catalytic converters for controlling gaseous pollutants.

The major forces behind the growth of the market are strict government regulations, rising public health concerns due to alarming pollution levels, and increasing industrialization in emerging economies. The growth can also be attributed to technological advancements in control systems and increased emissions from industries such as power generation, cement manufacturing, and chemicals.

The top firms in the industry are Mitsubishi Heavy Industries, Ltd., General Electric Company (GE Vernova), Babcock & Wilcox Enterprises, Inc., Siemens Energy AG, Thermax Limited, and Fujian Longking Co., Ltd.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Regulatory Pressure and Industrial Modernization Fuels Growth

Strict emission regulations across various industries such as power, cement, and manufacturing are driving air pollution control systems market growth. As governments impose strict quality standards, industries respond by incorporating advanced pollution control technologies. Industrial growth in the Asia Pacific region, along with retrofit demand in the regions of Europe and North America, also supports the market’s growth. The increasing emphasis on environmentally friendly, clean air initiatives and waste-to-energy projects is speeding up investment in high-efficiency air pollution control technologies, thus creating strong incentives for modernization globally.

Market Restraints

High Costs and Maintenance Complexity Hinder Growth

While APCS has its advantages, system installation and operation involve a considerable initial capital investment and lifecycle costs, particularly for multi-layered pollution control units, ultimately creating a significant barrier for the market. Technology is becoming increasingly complex to manage, requiring skilled staff to maintain treatment and operations. The complexity makes it less attractive for smaller firms or those with lower-cost options, potentially leading to varied system choices that further complicate their management requirements. In addition, the inconsistent enforcement of regulations, especially in developing countries, also limits possibilities due to cost and budget-related challenges.

Market Opportunities

Hybrid Systems and Carbon-Neutral Solutions Drive Growth, Creating Opportunities

Trends in the air pollution control market are increasingly related to hybrid systems that utilize both filtration and scrubbing technologies, allowing for more flexible and scalable pollution control solutions. Digital retrofits and aftermarket service models have substantial growth opportunities by improving the efficiency and longevity of the systems. In response to global decarbonization goals and environmental concerns, manufacturers are also increasingly offering carbon capture capability and energy-efficient designs. These innovations address many of the concerns, and opportunities are likely to increase, especially in fast-industrializing regions such as the Asia Pacific, the Middle East, and Latin America, where the air quality standards are being increased and new industrial infrastructure is being established.

AIR POLLUTION CONTROL SYSTEMS MARKET TRENDS

Integrated Emission Control and Smart Compliance Technologies Emerges as a Major Market Trend

The industry for air pollution control is shifting from traditional stand-alone devices to multi-pollutant control systems that utilize the connectivity of devices. Advancements in IoT sensors and AI-based process control enable real-time data collection for emissions, maintaining enhanced system performance for energy and regulatory purposes. Additionally, hybrid designs of scrubbers, filters, and catalytic converters provide a unified treatment of particulates, gases, and Volatile Organic Compounds (VOCs). The designs greatly improve performance and contribute to Environmental, Social, and Governance (ESG) targets through sustainability and carbon capture readiness. As this air pollution control industry transitions toward integrated smart pollution management, it also meets regulatory expectations for environmental sustainability.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Technology

Widespread Use in Controlling SO₂ Boosts Scrubbers Segment Growth

Based on the technology, the market is segmented into electrostatic precipitators, fabric filters, scrubbers, selective catalytic reduction, thermal & catalytic oxidizers, and others.

The scrubbers segment held the largest revenue share of 32.09% in the overall global market in the year 2026. The segment’s growth is attributable to their widespread use in controlling SO₂ and acid gas emissions across power generation, waste incineration, and marine sectors.

Of all the segments, selective catalytic reduction holds the highest CAGR of 7.9% in the global market. The growth is mainly due to the tightening global NOₓ emission standards and rapid adoption in industrial and utility boiler retrofits.

By Pollutant Type

Particulate Pollutants Segment Leads Market Owing to Its Extensive Use

Based on pollutant type, the market is divided into particulate pollutants, gaseous pollutants, organic & toxic pollutants, and others.

The particulate pollutants segment dominates with a market share of 40.68% in 2026. The segment continues to generate the major revenue due to extensive use of particulate control equipment such as baghouses and electrostatic precipitators across power, cement, and metal industries, supported by strict dust emission norms and large installed bases all over the globe.

Organic & toxic pollutants hold the highest CAGR of 7.4% in the global market. The segment’s growth is due to escalating VOC and hazardous pollutant regulations, rapid industrial diversification, and increasing adoption of advanced oxidizers and adsorption systems in chemical, pharmaceutical, and coating applications.

To know how our report can help streamline your business, Speak to Analyst

By Industry

Extensive Deployment in Biomass Power Plants Augments the Power Generation Segment Growth

Based on the industry, the market is divided into power generation, cement & metal processing, chemical & petrochemical, oil & gas, waste incineration/WtE, and others.

The power generation segment accounted for the largest air pollution control systems market share with 26.62% in 2026. The segment’s growth is attributable to the extensive deployment of large-scale emission control systems in coal, gas, and biomass power plants, alongside continuous retrofit programs aimed at meeting stringent global air quality and decarbonization mandates.

Waste Incineration / WtE represents the largest CAGR at 8.1% in the global market. The segment’s growth is attributable to rapid expansion of waste-to-energy facilities and stricter dioxin and acid gas emission norms, encouraging the adoption of high-efficiency multi-pollutant control technologies and hybrid systems across developed and emerging economies.

AIR POLLUTION CONTROL SYSTEMS MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

Asia Pacific Air Pollution Control Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 22.28 Billion in 2025, representing 21.50% of the global market landscape, and is expected to reach USD 23.49 Billion in 2026. The region’s growth is attributable to stricter environmental regulations and rising industrial activities in sectors such as power generation, chemicals, and manufacturing.

The U.S. is at the forefront of the North American market, with expected revenue of USD 17.58 billion in 2026. The growth is attributable to strict regulations, industrial growth, and a focus on public health.

Europe

Europe contributed 25.70% to the global market in 2025, with a valuation of USD 26.69 Billion, and is projected to reach USD 28.45 Billion in 2026. This growth is due to stringent environmental regulations, increased industrial activity, and a growing awareness of health impacts.

The U.K., Germany, and Italy are some of the leading contributors to the growth in the market, with the required revenue stake of USD 4.75 billion, USD 6.8 billion, and USD 2.64 billion, respectively, by 2026.

Asia Pacific

Asia Pacific accounted for USD 39.59 Billion in 2025, representing 38.20% of the global market share, and is projected to reach USD 42.4 billion in 2026. The region’s growth is attributable to rapid industrialization, expanding manufacturing bases, and stringent emission norms in China, India, and Southeast Asia. Other factors include large-scale installation of multi-pollutant control systems across power, cement, and chemical sectors.

At the same time, Asia Pacific is also expected to have the highest CAGR of 7.1%, further solidifying the market as the fastest-growing. The region’s growth is attributable to massive infrastructure investments, government-backed clean air programs, and accelerating adoption of advanced emission technologies. The region records the fastest growth as industries modernize and environmental enforcement strengthens across emerging economies.

Japan, India, and China are major contributors to the market growth with an expected revenue share of USD 5.71 billion, USD 8.73 billion, and USD 18.71 billion, respectively, by 2026.

Latin America and Middle East & Africa

In 2025, Middle East & Africa held 9.10% of the global market, reaching a valuation of USD 9.41 billion, and is projected to grow to USD 9.86 billion in 2026. due to increasing industrialization and stricter government regulations, particularly in sectors such as oil and gas and manufacturing.

GCC countries are predicted to have a market share of USD 5.53 billion by 2025.

Latin America contributed approximately USD 5.69 billion to the global market in 2025, accounting for a 5.50% share, and is expected to reach USD 5.92 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus On Partnerships and Acquisitions to Lead the Industry

The key players in the industry include Mitsubishi Heavy Industries, Ltd., General Electric Company (GE Vernova), Babcock & Wilcox Enterprises, Inc., Siemens Energy AG, Thermax Limited, and Fujian Longking Co., Ltd. The players focus on technological advancements, mergers and acquisitions, and developing effective and cost-efficient products. Companies are concentrating on enhancing existing systems for greater efficiency and leveraging innovations such as IoT, AI, and advanced filtration technologies. Additionally, strategies include expanding into emerging markets, entering strategic partnerships and collaborations, and focusing on product innovation driven by increasingly strict environmental regulations worldwide. Some are also integrating air pollution measures into broader climate strategies.

LIST OF KEY AIR POLLUTION CONTROL SYSTEMS COMPANIES PROFILED

- Mitsubishi Heavy Industries, Ltd. (Japan)

- General Electric Company (GE Vernova) (U.S.)

- Babcock & Wilcox Enterprises, Inc. (U.S.)

- Siemens Energy AG (Germany)

- Thermax Limited (India)

- Fujian Longking Co., Ltd. (China)

- Hamon Group (Belgium)

- Andritz AG (Austria)

- Ducon Technologies Inc. (U.S.)

- GEA Group AG (Germany)

- Alstom SA (France)

- CECO Environmental Corp. (U.S.)

- Tri-Mer Corporation (U.S.)

- Anguil Environmental Systems, Inc. (U.S.)

- FLSmidth & Co. A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- November 2025- Airvoice, a global startup dedicated to air quality control and management products and technologies, officially launched Airvoice Explore, a new-generation indoor air quality system designed not for engineers or building managers, but for everyday individuals and families seeking control over the air they breathe at home.

- June 2025- FLSmidth announced that it has agreed to divest its Air Pollution Control (APC) business to Rubicon Partners, a U.K.-based investment partnership focused on the acquisition of complex industrial businesses. The transaction is expected to close during the second half of 2025 and includes all related assets, including intellectual property, technology, employees and order backlog.

- May 2024- Thermo Fisher Scientific announced the commencement of manufacturing of Air Quality Monitoring System (AQMS) analyzers in India. The analyzers will be engineered, manufactured and validated at Thermo Fisher’s facility at Nasik, Maharashtra.

- October 2021- ABB launched first touch-free smart sensor to reduce indoor air pollution. The new ABB FusionAir® Smart Sensor offers four sensing options for creating optimal conditions for improving indoor air quality, safety and comfort.

- July 2021- Devic Earth, the leader in air pollution control equipment, launched the world’s first-ever “Clean Air as A Service” help improve ambient air quality, in India.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the air pollution control systems market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report covers several others that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2032 |

|

Growth Rate |

CAGR of 6.30% from 2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology, Pollutant Type, Industry, and Region |

|

ByTechnology |

· Electrostatic Precipitators · Fabric Filters · Scrubbers · Selective Catalytic Reduction · Thermal & Catalytic Oxidizers · Others |

|

ByPollutant Type |

· Particulate Pollutants · Gaseous Pollutants · Organic & Toxic Pollutants · Others |

|

By Industry |

· Power Generation · Cement & Metal Processing · Chemical & Petrochemical · Oil & Gas · Waste Incineration / WtE · Others |

|

By Region |

· North America (By Technology, Pollutant Type, Industry and Country/Sub-region) o U.S. (By Pollutant Type) o Canada (By Pollutant Type) o Mexico (By Pollutant Type) · Europe (By Technology, Pollutant Type, Industry and Country/Sub-region) o U.K. (By Pollutant Type) o Germany (By Pollutant Type) o France (By Pollutant Type) o Italy (By Pollutant Type) o Spain (By Pollutant Type) o Rest of Europe · Asia Pacific (By Technology, Pollutant Type, Industry and Country/Sub-region) o China (By Pollutant Type) o Japan (By Pollutant Type) o India (By Pollutant Type) o Australia (By Pollutant Type) o South Korea (By Pollutant Type) o Rest of Asia Pacific · South America (By Technology, Pollutant Type, Industry and Country/Sub-region) o Argentina (By Pollutant Type) o Brazil (By Pollutant Type) o Rest of South America · Middle East & Africa (By Technology, Pollutant Type, Industry and Country/Sub-region) o GCC (By Pollutant Type) o South Africa (By Pollutant Type) o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 110.12 billion in 2026 and is projected to reach USD 179.21 billion by 2034.

The market is expected to grow at a CAGR of 6.30% during the forecast period.

Regulatory pressure and industrial modernization is speeding up the market growth.

Mitsubishi Heavy Industries, Ltd., General Electric Company (GE Vernova), Babcock & Wilcox Enterprises, Inc., Siemens Energy AG, Thermax Limited, and Fujian Longking Co., Ltd. are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 39.59 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 192

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us