Biomass Power Generation Market Size, Share & Industry Analysis, By Feedstock (Agricultural Residues, Forest Residues, Municipal Solid Waste (MSW), Animal Waste, and Others), By Technology (Combustion, Gasification, Anaerobic Digestion, Pyrolysis, and Others), By Application (Residential, Commercial, Industrial), and Regional Forecast, 2026-2034

Biomass Power Generation Market Size

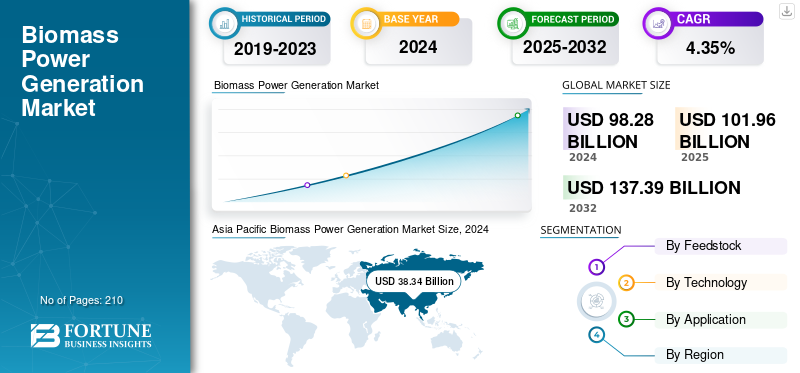

The global biomass power generation market size was valued at USD 101.96 billion in 2025 and is expected to reach USD 105.8 billion in 2026. Furthermore, the market is projected to reach USD 152.68 billion by 2034, exhibiting a CAGR of 4.69% during the forecast period of 2026-2034. Asia Pacific dominated the biomass power generation market with a market share of 39.15% in 2025.

Moreover, Asia Pacific accounts for the largest market revenue share owing to the increasing energy demand from industrialization and urbanization, abundant biomass resources, supportive government policies, and the global push for clean energy and emissions reduction.

Biomass power generation is the process of generating electricity from organic matter such as crop residues, forestry waste, and municipal solid waste. This is done by burning the biomass to create steam, which drives a turbine, or by converting it into a gas that can be used to generate power. This method is considered a renewable energy source because the biomass can be replenished relatively quickly.

The major drivers for the biomass power generation market include government policies and incentives aimed at reducing greenhouse gas (GHG) emissions and achieving net-zero targets. Other major drivers are the need for energy security and grid stability, especially as a reliable, dispatchable alternative to intermittent renewables, including solar and wind. The global push for a circular economy, improved waste management through waste-to-energy conversion, and volatile fossil fuel prices are also significant factors.

- According to the International Energy Agency, Modern bioenergy currently constitutes the largest renewable energy source worldwide, representing nearly 55% of renewable energy (excluding traditional biomass use) and over 6% of the total global energy supply. The Net Zero Emissions by 2050 (NZE) Scenario projects a substantial escalation in bioenergy utilization to replace fossil fuels by 2030, underscoring its critical role in the global energy transition and decarbonization efforts.

Drax Group plc is a prominent player in the biomass power generation market, primarily because it operates the world's largest biomass power station by installed capacity. The company positions itself as a leader in the transition to net-zero energy among other market players.

Download Free sample to learn more about this report.

BIOMASS POWER GENERATION MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 101.96 billion

- 2026 Market Size: USD 105.80 billion

- 2034 Forecast Market Size: USD 152.68 billion

- CAGR: 4.69% from 2026–2034

- Asia Pacific dominated the biomass power generation market with a 39.15% share in 2025.

- The Municipal Solid Waste (MSW) segment held the largest feedstock share at 31.79%.

- The combustion segment led the technology segment with a 61.02% share in 2026.

Asia Pacific

Asia Pacific accounted for USD 39.92 billion and 39.15% of the global market in 2025.

Europe

Europe reached USD 34.77 billion, representing 34.11% of the global market in 2025.

North America

North America generated USD 14.26 billion, accounting for 13.98% of the global market in 2025.

U.S.

The biomass power generation market is projected to reach USD 12.23 billion by 2026.

Japan

The biomass power generation market is projected to reach USD 7.48 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Focus on Waste-to-Energy (WtE) and Circular Economy to Drive Market Growth

The growing global focus on Waste-to-Energy (WtE) and the circular economy is a key driver for the biomass power generation market growth. As urbanization accelerates, municipalities are prioritizing sustainable waste management solutions that convert municipal solid waste (MSW) and organic residues into renewable energy. WtE plants reduce landfill dependence, lower greenhouse gas emissions, and provide stable power and heat. For instance, in July 2025, the Government of Greece announced plans to build six waste-to-energy plants to drastically reduce landfill waste from 80% to 10% by 2035, aligning with EU targets. These incinerators will process 1.19 million tons of waste annually, producing around 1.03 TWh of electricity (2% of national consumption) and generating district heating. The development features mechanical treatment units to produce higher-quality solid fuel, supporting circular waste management.

Governments across Europe, Asia, and the Middle East are implementing policies promoting waste valorization, aligning with zero-waste and decarbonization goals. This shift positions biomass-based WtE systems as a central component of integrated urban sustainability and energy recovery strategies across the globe.

Abundant Availability of Agricultural and Forestry Residues to Fuel the Market Growth

The abundant availability of agricultural and forestry residues is a major driver of the biomass power generation market. Vast quantities of crop residues, such as rice husks, straw, and bagasse, as well as forestry by products, including wood chips and sawdust, provide a sustainable and low-cost feedstock base. These residues are readily accessible in agricultural economies such as those in China, India, Brazil, and Canada, thereby reducing dependence on fossil fuels and imported energy. Utilizing this biomass not only generates renewable power but also mitigates open-field burning and associated carbon emissions. This availability ensures a steady fuel supply, enhances rural income, and supports circular and low-carbon energy systems.

MARKET RESTRAINTS

Competition from Cheaper Renewable Energy Sources to Limit Market Growth

The rapid decline in the cost of solar PV, wind power, and energy storage systems has intensified competition for biomass power generation. These technologies offer lower Levelized Costs of Electricity (LCOE), faster installation timelines, and minimal fuel-related expenses, making them more attractive to investors and utilities.

In contrast, biomass projects face higher capital and operational costs due to the complexity of feedstock logistics and maintenance requirements. As renewable portfolios shift toward cheaper and more scalable options, biomass power often depends on policy incentives, carbon credits, or renewable certificates to remain financially viable and sustain its role in the global energy mix.

MARKET OPPORTUNITIES

Industrial Decarbonization via Biomass CHP (Combined Heat & Power) to Create Lucrative Opportunities

Industrial decarbonization via biomass-based Combined Heat and Power (CHP) systems presents a major growth opportunity in the biomass power generation market. CHP technology enables the simultaneous production of electricity and thermal energy from a single biomass source, achieving efficiencies above 80%. For instance, in July 2025, Valmet secured a contract to supply a biomass boiler and flue gas handling system for a new combined heat and power (CHP) plant in Örtofta, Skåne, Sweden. The facility will replace aging units and nearly double energy capacity, providing up to 25 MW of electricity and expanding district heating, with integration designed for future carbon capture. Construction is scheduled for mid-2026, with commissioning in 2028.

Industries such as pulp and paper, food processing, cement, and chemicals are adopting biomass CHP to reduce fossil fuel dependence and carbon emissions. Supportive policies, carbon pricing, and renewable energy mandates are accelerating this transition. Biomass CHP not only enhances energy efficiency but also provides cost savings and helps industries meet net-zero and sustainability targets across global manufacturing sectors.

MARKET CHALLENGES

Fragmentation of the Supply Chain Creates Challenges the Market Growth.

Feedstock supply chains are a major challenge for the biomass power generation market. Biomass sources such as agricultural residues, forestry waste, and municipal solid waste are often scattered, seasonal, and inconsistent in quality. This geographical dispersion increases transportation, handling, and storage costs, which in turn affect plant reliability and operational efficiency. In many developing regions, the absence of organized collection networks and preprocessing facilities further limits steady fuel availability. Moreover, competing uses for residues such as animal feed, fertilizer, or industrial raw material create supply uncertainty. These challenges make it difficult for biomass power projects to secure stable, long-term, and cost-effective feedstock contracts.

BIOMASS POWER GENERATION MARKET TRENDS

Growing Environmental & Climate Pressure through Governments is emerging as a Key Trend.

Growing environmental and climate pressure from governments is emerging as a key trend driving the biomass power generation market. As nations strengthen their commitments under the Paris Agreement and move toward net-zero emissions, policymakers are prioritizing low-carbon footprint, and renewable energy solutions. Biomass power offers a sustainable pathway to reduce greenhouse gas emissions while effectively utilizing waste and residues. For instance, the EU's net-zero target is to achieve climate neutrality with net-zero greenhouse gas emissions by 2050, which is a legally binding goal outlined in the European Climate Law. To reach this target, the EU has set an intermediate goal of reducing net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels.

Governments worldwide are implementing carbon pricing, renewable portfolio standards, and bioenergy incentives to acceleratethe deployment of these technologies. This regulatory momentum encourages both public and private investment in biomass-based electricity and CHP systems, positioning biomass as a reliable component of long-term climate and energy transition strategies.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS ON THE GLOBAL BIOMASS POWER GENERATION MARKET

Tariffs negatively impact the global biomass power generation market by increasing production and operational costs for equipment and materials, which can slow market growth and deter investment. This can lead to higher prices for consumers, reduced profit margins, and a shift in market dynamics as countries may try to incentivize domestic production. However, tariffs can also create opportunities for innovation and the development of domestic markets to absorb products previously destined for export.

SEGMENTATION ANALYSIS

By Feedstock

Rising Urbanization and Waste Generation to Lead Municipal Solid Waste (MSW) Segment’s Growth

Based on feedstock, the market is segmented into agricultural residues, forest residues, Municipal Solid Waste (MSW), animal waste, and others.

Municipal Solid Waste (MSW) accounted for the largest market revenue share of 31.79% in 2024, due to rapid urbanization, increasing waste volumes, and government-backed waste-to-energy (WtE) initiatives. For instance, in May 2025, U.S. government patent authorities granted WastAway a patent covering its MSW-to-fuel process, which converts waste into Cellulate, RNG, and SE3 fuels in 30 minutes, achieving 85% landfill diversion and 400 tons per day.

Meanwhile, agricultural residues are expected to emerge as the fastest-growing segment with a CAGR of 5.50%, particularly in Asia and Latin America, driven by abundant crop waste and efforts to promote sustainable rural energy generation.

The agricultural residues segment is expected to account for 31.71% of the market in 2026.

By Technology

Combustion Segment Dominated the Market Due to the Global Shift Toward Low-Carbon Energy Solutions

Based on technology, the market is segmented into combustion, gasification, anaerobic digestion, pyrolysis, and others.

Combustion accounted for the largest market revenue share of 61.02% in 2026 due to its proven efficiency, scalability, and lower operational complexity in large-scale plants.

Furthermore, gasification is expected to grow at a significant CAGR of 10.70% due to its higher energy conversion efficiency, cleaner emissions, and ability to integrate with CHP and advanced bioenergy systems, especially in developed and emerging economies.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rising Biomass Cogeneration in Manufacturing Fueled the Industrial Segment’s Growth

Based on the application, the market is segmented into residential, commercial, and industrial.

Residential dominated the biomass power generation market share in 2026 with a revenue of 27.13%, driven by the extensive use of biomass cogeneration systems for cost-efficient heat and power in manufacturing.

- In November 2024, Drax Group announced that the company is pursuing energy supply agreements with data centers, recognizing the increasing demand for 24/7 power fueled by the growth of AI. Its Selby biomass plant generates 2.6GW, 4% of UK dispatchable capacity. Drax plans to deploy carbon capture technology and aims to co-locate data centers with biomass generation, thereby optimizing power reliability and sustainability.

However, the commercial segment is the fastest-growing, driven by rising urbanization, the increasing adoption of biomass for heating and power in commercial buildings, and supportive government policies that promote a clean energy transition in urban centers.

BIOMASS POWER GENERATION MARKET REGIONAL OUTLOOK

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Biomass Power Generation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 39.15% of the global market, reaching a valuation of USD 39.92 Billion, and is projected to grow to USD 41.6 Billion in 2026. Rapid industrialization, expanding urban populations, and abundant agricultural residues are fueling biomass power adoption in the Asia Pacific. Countries including China, India, and Japan are investing in biomass-to-energy projects to enhance energy security and manage waste sustainably. For instance, in August 2024, POWERCHINA successfully connected its first biomass power project in the Asia-Pacific region, a 12 MW biomass power plant in Bangka, Indonesia, to the grid, marking the start of commercial operations.

The Japan market is projected to reach USD 7.48 billion by 2026, the China market is projected to reach USD 16.77 billion by 2026, and the India market is projected to reach USD 7.34 billion by 2026.

Europe

After Asia Pacific, the Europe market was valued at USD 34.77 billion in 2025, capturing 34.11% of global revenue, and is estimated to reach USD 36.07 billion in 2026. Europe leads the biomass power generation market due to its stringent climate goals, carbon neutrality & renewable energy targets, as well as the EU Renewable Energy Directive (RED II). The U.K. market is projected to reach USD 7.42 billion by 2026, while the German market is projected to reach USD 6.32 billion by 2026.

North America

North America accounted for USD 14.26 Billion in 2025, representing 13.98% of the global market share, and is projected to reach USD 14.68 Billion in 2026, driven by increasing demand for biomass power, decentralized renewable energy, government tax credits, and strong emphasis on waste management and landfill diversion. The U.S. market is projected to reach USD 12.23 billion by 2026.

Latin America

The Latin America region captured 7.22% of the global market in 2025, generating USD 7.36 Billion in revenue, and is projected to reach USD 7.63 Billion in 2026. The market for biomass power generation in Latin America is driven by abundant sugarcane bagasse, agricultural residues, and growing demand for renewable rural electrification. Countries such as Brazil and Mexico are utilizing biomass cogeneration in agro-industrial sectors including sugar, ethanol, and pulp.

Middle East & Africa

Furthermore, Middle East & Africa contributed approximately USD 5.64 Billion to the global market in 2025, accounting for 5.53% share, and is expected to reach USD 5.82 Billion in 2026. While still emerging, the biomass power market in the Middle East & Africa is gaining traction due to growing waste-to-energy initiatives, rural electrification projects, and efforts to reduce dependence on fossil fuels.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strategic Collaboration and Campaigns by the Major Key Players To Fuel Market Share

The competitive landscape is fragmented, with key competitive players including E.ON Energy, Ameresco, Babcock & Wilcox Company, Engie, Indus Green Bio Energy Pvt. Ltd., and Ørsted A/s. For instance, in August 2025, Breakthrough Energy announced a partnership with Japan to advance biomass and low-carbon hydrogen technologies. The collaboration supports Japan’s 2050 net-zero target by funding and providing expertise for projects commercializing biofuels and renewable hydrogen. Such developments are expected to foster market growth over the forecast period.

List of the Key Biomass Power Generation Companies Profiled

- ENGIE (France)

- Xcel Energy Inc. (USA)

- ABB (Switzerland)

- Siemens (Germany)

- General Electric (USA)

- Nexans (France)

- Schneider Electric (France)

- Ørsted A/S (Denmark)

- Drax Group (UK)

- ACCIONA (Spain)

- EDF (France)

- Vattenfall (Sweden)

- Veolia (France)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, Voltalia announced the start of commissioning its 10.5 MW biomass power plant in Sinnamary, French Guiana, which will provide up to 8% of the territory’s electricity needs and support regional energy diversification.

- In September 2025, Taihei Dengyo announced plans to develop a 2 MW biomass power plant in Murakami City, Japan. Construction is scheduled to begin in March 2026, with commissioning expected by the end of 2027. The plant, using woody biomass, will generate about 13,000 MWh annually, supporting local renewable energy supply and Japan’s decarbonization efforts.

- In February 2024, Seiko Epson Corporation announced development plans for its first biomass power plant in Iida City, Nagano Prefecture, Japan, aiming for operation in fiscal 2026. The plant will use unused wood, tree bark, and pallets to generate renewable electricity, supporting Epson's carbon-negative goal under Environmental Vision 2050.

- In August 2024, the Ozu Biomass Power Plant in Japan, owned by Ozu Biomass Power Corp., commenced commercial operation. It is a biomass-only power plant using imported wood pellets, producing about 350 million kWh annually and supporting Japan’s renewable energy goals through a 20-year Feed-in tariff scheme.

- In March 2023, the Asian Development Bank (ADB) and SAEL Industries Limited signed a USD 91 million loan agreement to fund five 14.9 MW biomass power plants in Rajasthan, India. These plants will use agricultural residue to generate approximately 544 GWh annually, reduce carbon emissions by 487,200 tons yearly, increase local farmers' income through crop residue sales, and improve air quality by reducing agricultural waste burning.

REPORT COVERAGE

The Global Biomass Power Generation Market report delivers a detailed insight into the market. It focuses on key aspects, such as leading companies in the Biomass Power Generation market. Besides, the report offers regional insights and global market trends & technology, and highlights key industry developments. In addition to the factors above, the report encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.69% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Feedstock

|

|

By Technology

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 105.8 billion in 2026.

The market is likely to grow at a CAGR of 4.69% over the forecast period (2026-2034).

The Industrial segment is expected to lead the market over the forecast period.

The market size of the Asia Pacific stood at USD 39.92 billion in 2025.

Growing focus on Waste-to-Energy (WtE) and circular economy to drive market growth.

Some of the top players in the market are E. ON Energy, Ameresco, Babcock & Wilcox Company, Engie, Indus Green Bio Energy Pvt. Ltd., and Ørsted A/s, among others.

The global market size is expected to reach USD 152.68 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us