Diabetes Devices Market Size, Share & Industry Analysis, By Device Type (Blood Glucose Monitoring Systems, Treatment), By Distribution Channel (Institutional Sales, Retail Sales), and Regional Forecast, 2026-2034

Diabetes Devices Market Size and Industry Overview

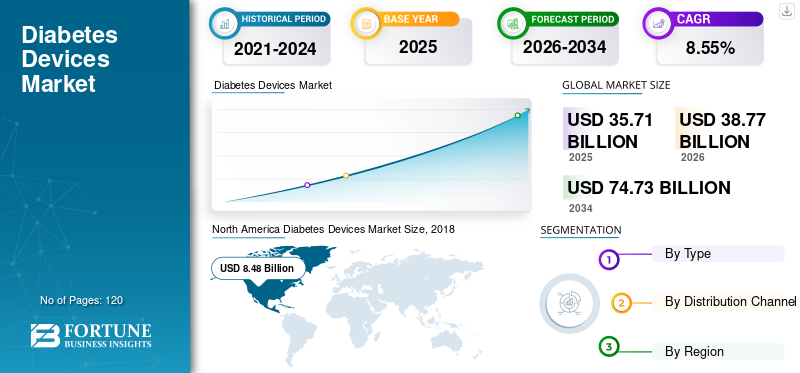

The global diabetes devices market size was valued at USD 35.71 billion in 2025. The market is projected to grow from USD 38.77 billion in 2026 to USD 74.73 billion by 2034, exhibiting a CAGR of 8.55% during the forecast period. North America dominated the global market with a share of 40.54% in 2025.

The diabetes devices market demand is sustained by the chronic nature of diabetes, long treatment durations, and the need for continuous disease management. The current diabetes devices market size reflects broad penetration across developed healthcare systems, alongside accelerating adoption in emerging economies where diagnosis rates and access to care are expanding.

Historically, market growth was anchored in basic blood glucose monitoring devices and insulin delivery tools. Over time, the market transitioned from episodic monitoring toward continuous, technology-enabled management. This shift moved the industry from an early scaling phase into a more advanced, yet still expanding, maturity stage. While some product categories show signs of saturation in high-income regions, innovation continues to unlock new growth vectors.

Short-term diabetes devices market growth is supported by rising diabetes prevalence, increased screening, and stronger reimbursement coverage for advanced devices. Mid-term expansion is expected to accelerate as connected monitoring systems, automated insulin delivery, and digital health integration gain wider clinical acceptance. Over the long term, market momentum remains favorable as diabetes care increasingly emphasizes outcomes, adherence, and personalized treatment pathways.

Key inflection points include the rapid uptake of continuous glucose monitoring, growing patient self-management, and the integration of devices with digital health platforms. These indicators signal a market evolving toward higher value, technology-driven solutions rather than simple volume expansion.

An increase in the incidence rate of diabetes caused by a sedentary lifestyle and rapid urbanization is the major factor driving the growth of the global diabetes care devices market. Technologically advanced blood glucose monitoring systems and minimally invasive insulin delivery devices have increased the number of diabetes patients diagnosed annually worldwide.

For instance, in September 2017, Abbott received Food and Drug Administration approval for the FreeStyle Libre Flash Glucose Monitoring System. This device uses a small sensor attached to the upper arm for the monitoring of blood glucose levels.

Nevertheless, increasing funding from private and government organizations, along with a rising number of research and development activities for diabetes control and treatment solutions, is slated to offer opportunities for market players, thereby contributing to market expansion. These factors are anticipated to drive the growth of the diabetes management devices market during the forecast period.

Download Free sample to learn more about this report.

diabetes devices market key takeaways

- 2025 Market Size: USD 35.71 Billion

- 2026 Market Size: USD 38.77 Billion

- 2034 Forecast Market Size: USD 74.73 Billion

- CAGR: 8.55% from 2026–2034

- North America dominated the diabetes devices market with a 40.54% share in 2025.

- The Blood Glucose Monitoring Systems segment accounted for the largest market share in 2025.

- The retail sales segment is projected to grow at the highest CAGR during the forecast period.

Asia Pacific

Asia Pacific is expected to register the fastest growth due to the rising diabetic population and increasing adoption of advanced monitoring and insulin delivery devices.

North America

North America held the largest share of the global diabetes devices market in 2025.

Europe

Europe maintains strong adoption of advanced diabetes monitoring devices, supported by public healthcare systems.

U.S.

High diabetes prevalence and widespread adoption of advanced diabetes devices continue to support market growth.

Japan

Growing demand for technologically advanced blood glucose monitoring and insulin delivery devices is driving market expansion.

Read More

What major trends and transformations are redefining the industry?

The diabetes devices market is undergoing a structural transformation driven by digitalization, automation, and data-centric care models. Devices are evolving from standalone measurement tools into integrated platforms that support continuous monitoring, therapy optimization, and clinical decision-making. This shift is redefining how value is created across the diabetes care continuum.

One of the most influential diabetes device market trends is the rapid adoption of connected and automated systems. Continuous glucose monitoring has become a foundational technology, enabling near real-time insights into glycemic patterns. Automated insulin delivery systems increasingly combine sensors, algorithms, and pumps to reduce manual intervention and improve outcomes. These closed-loop approaches are reshaping expectations for both patients and clinicians.

Platform and ecosystem strategies are gaining prominence. Device manufacturers are expanding beyond hardware into software, analytics, and subscription-based services. Integration with mobile applications, electronic health records, and telehealth platforms strengthens patient engagement and supports longitudinal care. This ecosystem orientation increases switching costs and reinforces recurring revenue models.

Artificial intelligence and data analytics are emerging as critical enablers. Predictive alerts, pattern recognition, and personalized therapy recommendations enhance clinical relevance. At the same time, sustainability and access considerations are influencing design priorities, including device longevity and ease of use. Collectively, these shifts signal a diabetes devices market moving toward intelligent, outcomes-driven solutions aligned with modern care delivery models.

Download Free sample to learn more about this report.

What are the strongest growth drivers shaping this market today?

“Introduction of Novel and Technologically Advanced Products is driving the Market Growth.”

Introduction of novel products in diabetes monitoring systems and treatment devices globally is one of the major factors driving the growth of the global diabetes devices market. For instance, in February 2019, Tandem Diabetes Care, Inc., received FDA approval for the marketing of the first insulin pump with interoperable technology for children and adults with diabetes. t: Slim X2 insulin pump is the first device to be classified under a new de novo premarket review pathway.

Additionally, in January 2019, Bigfoot Biomedical entered a partnership with Eli Lilly and Company to develop solutions for optimization of delivery and dosing of insulin using artificial intelligence.

Investment by key market players with an aim to cater to unmet needs in emerging countries. For instance, in October 2018, Amazon launched a medical device brand focusing mainly on diabetes and cardiovascular disease. Choice, the new brand, will initially include blood glucose monitors and blood pressure monitors, accompanied by supporting mobile apps that offer measurement tracking, data mobility, and reminders. These types of initiatives are anticipated to increase awareness among people and propel the demand for diabetes devices globally, hence driving the growth of the market.

“Rising Prevalence of Diabetes Globally is Fueling the Demand for Monitoring and Treatment Devices”

There is an increasing prevalence of diabetes globally, especially in developing economies, including China and India. Various factors, including rapid urbanization and growth in sedentary lifestyles, especially in developing economies, have been responsible for the rapidly rising prevalence of diabetes. The International Diabetes Federation estimated that around 425 million adults were suffering from diabetes in 2017, and it is projected to rise to around 630 million by 2045.

According to these studies, China, India, the U.S., Brazil, and Mexico account for an estimated 55.0% to 60.0% of the global diabetes population. China and India currently account for around 44.0% of the global diabetes population.

Other factors, including obesity and lack of awareness regarding the disease, especially in emerging countries, are also contributing to the increasing incidence and prevalence of diabetes. For example, according to the World Health Organization (WHO), an estimated 1.9 billion adults globally were overweight in 2016, and out of these, an estimated 650 million adults were obese.

Rising obesity, coupled with an increasing number of diabetic patients, is anticipated to fuel the demand for diabetes treatment, hence driving the growth of the diabetes management devices market during the forecast period.

Growth in the diabetes devices market is primarily driven by escalating demand for continuous, patient-centric disease management. Rising global diabetes prevalence, earlier diagnosis, and longer life expectancy have expanded the treated population. Patients and clinicians increasingly favor proactive monitoring and tighter glycemic control, shifting demand toward advanced devices that reduce complications and improve quality of life.

Home-based care, self-monitoring, and remote clinical oversight are now central to diabetes management. Patients expect devices that are accurate, minimally invasive, and easy to integrate into daily routines. Payers and providers increasingly value technologies that improve adherence, reduce acute events, and lower long-term healthcare utilization.

Continuous innovation in sensor accuracy, miniaturization, and device interoperability has improved clinical performance while enhancing user experience. Investment in digital health infrastructure has enabled seamless data sharing between devices, mobile applications, and care teams. Strong capital inflows and specialized talent pools continue to support rapid product iteration and clinical validation.

Regulatory agencies increasingly provide clear approval pathways for connected and automated devices, reducing time-to-market uncertainty. Reimbursement frameworks are evolving to recognize the long-term economic value of advanced monitoring and treatment systems. Broader innovation waves in artificial intelligence, mobile health, and data analytics amplify these effects, embedding diabetes devices more deeply into modern care pathways rather than positioning them as standalone tools.

What are the constraints and structural challenges?

Despite sustained diabetes devices market growth, several structural challenges continue to shape competitive outcomes and adoption pace. High barriers to entry remain a defining feature. Device development requires substantial clinical validation, regulatory approval, and manufacturing scale, which limits participation to well-capitalized firms. These barriers protect incumbents but slow diversification in some segments.

Regulatory and compliance risks are significant. Diabetes devices are subject to stringent safety, accuracy, and post-market surveillance requirements. Regulatory divergence across regions increases complexity for global launches and lifecycle management. Any changes in approval standards or reimbursement criteria can materially affect product viability and market access.

Operational constraints also influence scalability. Advanced devices rely on complex supply chains, including specialized sensors, electronics, and consumables. Disruptions in component availability or quality can impact production continuity. Talent constraints, particularly in software engineering, data science, and clinical affairs, add further execution risk.

SEGMENTATION ANALYSIS

By Type Analysis

“The Monitoring Devices Segment is anticipated to grow at a Faster Pace during the forecast period.”

On the basis of type, the global market can be segmented into monitoring devices and treatment devices.

To know how our report can help streamline your business, Speak to Analyst

Monitoring devices accounted for the largest share of the global diabetes care devices market in 2018. An increasing number of regulatory approvals for continuous blood glucose monitoring systems and technological advancements in insulin delivery devices, such as smart insulin patches, insulin inhalers, closed-loop pump systems, and other pipeline devices, are some of the major driving factors for the growth of the global diabetes care devices market.

Blood Glucose Monitoring Systems remain the largest and most strategically important segment. This category includes traditional self-monitoring blood glucose devices and continuous glucose monitoring systems. While conventional monitoring devices are widely adopted, they face margin pressure due to commoditization and competitive pricing. In contrast, continuous glucose monitoring represents the highest-growth and highest-value subsegment. These systems deliver continuous data streams, support predictive alerts, and integrate with digital platforms. Their recurring sensor replacement cycles and subscription software components generate durable revenue and stronger margins.

Growing adoption of insulin patches, wearable continuous blood glucose monitoring systems, and smart insulin pumps for self-management of diabetes is also one of the factors propelling the growth of the global diabetes care devices market.

Treatment Devices include insulin delivery systems such as pens, pumps, and automated insulin delivery platforms. Basic insulin delivery tools remain essential but show slower growth in mature markets. Advanced insulin pumps and closed-loop systems capture a growing share of the diabetes devices market growth due to their ability to automate dosing and improve clinical outcomes. These products benefit from high switching costs, long patient lifecycles, and strong reimbursement support in developed healthcare systems.

By Distribution Channel Analysis

“Retail Sales Segment is expected to hold the Highest Share among the Distribution channels.”

On the basis of distribution channel, the market for a diabetes device can be segmented into institutional sales and retail sales.

Retail Sales play a critical role in basic monitoring and self-care devices. While volumes are high, margins are lower. Value increases when retail channels support connected ecosystems and ongoing consumable sales. The retail sales segment is projected to grow at a higher CAGR during the forecast period due to increased penetration of private-label brands in retail outlets at discounted prices, which are some of the factors likely to propel the growth of the retail sales segment. Explanation of retail sales segments for various key market players with an aim to achieve more sales in the different regions globally.

The rising prevalence of chronic disorders and the rising number of surgeries are likely to increase demand for blood glucose meters, as blood glucose monitoring is mandatory while performing invasive surgeries, which will further fuel the growth of institutional sales during the forecast period. Institutional Sales dominate advanced device adoption. Hospitals, clinics, and integrated health systems drive uptake of high-value technologies, supported by reimbursement pathways and clinician endorsement. This channel favors premium products and long-term supplier relationships.

Overall, the diabetes devices market is shifting toward integrated, recurring, and data-driven solutions. Companies that align device innovation with service models and clinical outcomes capture a disproportionate share of long-term economic value.

REGIONAL ANALYSIS

North America

North America represents the most advanced and innovation-driven regional market. High diagnosis rates, strong reimbursement coverage, and rapid uptake of connected technologies support sustained demand for premium devices. Continuous glucose monitoring and automated insulin delivery systems are widely adopted, driven by clinician endorsement and patient awareness. Competitive intensity is high, but pricing power remains relatively strong due to demonstrated clinical value and payer acceptance.

North America generated a revenue of USD 8.48 billion in 2018 and is anticipated to grow at a moderate CAGR during the forecast period.

Europe

Europe exhibits a more regulated and heterogeneous landscape. Western Europe shows high penetration of monitoring devices and steady adoption of advanced systems, supported by public healthcare funding. However, pricing controls and health technology assessments moderate margin expansion. Central and Eastern Europe present lower penetration but higher relative growth potential as healthcare investment and diabetes screening improve. Regulatory harmonization supports market entry, though procurement cycles are often prolonged.

According to the World Health Organization, in 2015, 60 million people were suffering from diabetes in Europe. The increasing diabetes population in Europe and comparatively lower prices of insulin and insulin delivery devices, subsequently increasing the demand and sales of the insulin delivery devices, are some of the major factors anticipated to drive the growth of the global diabetes care devices market.

North America Diabetes Devices Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

Asia-Pacific

Asia-Pacific represents the fastest-expanding regional opportunity. Rising diabetes prevalence, urbanization, and lifestyle changes are driving demand across large patient populations. Adoption remains uneven, with advanced devices concentrated in higher-income markets and urban centers. Cost sensitivity favors tiered product strategies and localized manufacturing. Over time, this region is expected to contribute a growing share of the global diabetes devices market growth.

Asia Pacific is anticipated to grow at a significantly higher CAGR during the forecast period due to the increasing diabetic population, rising adoption of the technologically advanced blood glucose meters, and higher demand for insulin delivery devices.

Latin America & the Middle East, and Africa

On the other hand, the Middle East, Africa, and Latin America are expected to grow at a significant CAGR during the forecast period of 2019-2026, owing to the increasing diabetic population, rising investment in the healthcare infrastructure, and rising awareness about disease diagnosis and monitoring.

Middle East and Africa region is at an earlier adoption stage. Demand is driven by rising diabetes prevalence and government-led healthcare modernization initiatives. Market access varies widely by country, with premium devices concentrated in private and urban healthcare systems.

Latin America remains an emerging but strategically important market. Growth is supported by improving diagnosis rates and the gradual expansion of reimbursement coverage. Adoption is strongest in private healthcare settings, while public systems often prioritize cost-effective monitoring solutions. Economic volatility can affect short-term demand, but long-term fundamentals remain favorable.

How competitive is the market?

“F. Hoffmann-La Roche Ltd. and Medtronic Account for Highest Market Share in Terms of Revenue”

F. Hoffmann-La Roche Ltd. is a leading player in the global continuous diabetes care devices, owing to its strong portfolio of diabetes care devices and strong distribution network globally. In order to strengthen their market position, key market players are focusing on the introduction of non-invasive and reusable insulin delivery devices in the global market. F. Hoffmann-La Roche Ltd., Medtronic, and Tandem Diabetes Care, Inc., dominated the global diabetes care devices market in 2018. Other players operating in the global Diabetes care devices market are BD, Eli Lilly and Company, Sanofi, and others.

The diabetes devices market is highly competitive and innovation-intensive, with a small group of global incumbents holding significant market influence alongside emerging challengers. Competitive advantage is shaped by clinical credibility, regulatory track record, and ecosystem depth rather than scale alone.

Leading incumbents dominate high-value segments such as continuous glucose monitoring and automated insulin delivery. Their strategies emphasize integrated platforms, proprietary consumables, and long-term patient engagement. These firms benefit from strong brand recognition, extensive clinical data, and established reimbursement relationships, reinforcing durable diabetes devices market share.

Challengers focus on targeted innovation, cost optimization, or underserved geographies. Some differentiate through user-centric design, alternative sensor technologies, or software-driven insights. At the same time, these players can disrupt specific niches, and scaling remains constrained by regulatory complexity and capital requirements.

Strategic activity remains active across the industry:

- Partnerships between device manufacturers and digital health platforms

- Acquisitions aimed at expanding software, analytics, or geographic reach

- Investment in closed-loop and next-generation sensing technologies

- Overall, competition is shifting from device performance alone toward platform capability, data integration, and lifecycle value. This evolution continues to reshape competitive positioning within the diabetes devices market.

What role do innovation and technologies play in shaping future growth?

Innovation is the primary force shaping long-term diabetes devices market growth. Advances in sensor accuracy, miniaturization, and reliability have transformed monitoring from intermittent measurement to continuous insight. These improvements enable earlier intervention, tighter control, and improved patient outcomes.

Artificial intelligence and advanced analytics are increasingly embedded within devices and associated software platforms. Algorithms analyze glucose trends, predict risk events, and support personalized therapy adjustments. Automation reduces cognitive burden for patients and clinicians, improving adherence and clinical efficiency.

Cloud connectivity and data interoperability are also critical. Seamless data exchange between devices, mobile applications, and healthcare providers supports remote monitoring and population-level analytics. This infrastructure enhances scalability while lowering marginal delivery costs.

Innovation is also reshaping cost structures. While advanced devices require higher upfront investment, automation and data-driven care reduce downstream healthcare utilization. Over time, competitive advantage will favor companies that integrate hardware, software, and analytics into secure, clinically validated ecosystems that deliver measurable value.

What are the opportunities for growth?

The most attractive opportunities in the diabetes devices market lie in segments that combine clinical impact with recurring revenue potential. Continuous glucose monitoring and automated insulin delivery platforms remain central growth engines, supported by expanding eligibility and improving reimbursement.

Underserved geographies offer long-term upside, particularly in Asia-Pacific and parts of Latin America, where diagnosis rates are rising, and healthcare access is improving. Tiered product strategies and localized partnerships are critical to unlocking these markets.

White-space opportunities exist at the intersection of devices and digital health. Predictive analytics, remote care integration, and personalized decision-support tools extend value beyond hardware. Adjacent expansion into metabolic health monitoring and chronic disease management platforms also presents diversification potential.

From an investment perspective, short-term opportunities favor companies with strong regulatory momentum and expanding installed bases. Long-term value creation depends on platform scalability, data monetization, and the ability to align innovation with evolving care models. Firms that address affordability, access, and outcomes simultaneously are best positioned to lead the next phase of diabetes device market growth.

List Of Key Companies Covered:

- F. Hoffmann-La Roche Ltd

- Tandem Diabetes Care, Inc.

- B. Braun Melsungen AG

- Medtronic

- BD

- Novo Nordisk A/S

- Abbott

- Sanofi

- Other players

KEY INDUSTRY DEVELOPMENTS:

- May 2021 – Medtronic announced that the company had received European approval for two diabetes management devices. First is InPen, a connected insulin pen designed for consumers requiring multiple daily injections. The latter is the Guardian 4 sensor, designed to be used either as a standalone continuous glucose monitor or with InPen, and both are CE marked.

- March 2021 - Roche announced the launch of the new Accu-Chek Instant system, which has bluetooth connectivity to the mySugr app, that transfers blood glucose results to the mySugr app. This system supports the company’s approach of patient-centered therapy to provide personalized diabetes management.

- June 2020 - Abbott announced that the company had finalized an agreement with Tandem Diabetes Care to develop integrated diabetes solutions that combine its continuous glucose monitoring (CGM) technology with Tandem's innovative insulin delivery systems to supply people with more options to manage their diabetes.

REPORT COVERAGE

Rising awareness about diabetes management and a growing number of health-conscious people leading to high adoption of diabetes monitoring devices are expected to drive the growth of the global diabetes diagnosis and monitoring devices market during the forecast period of 2019-2026.

Along with this, the report provides an extensive analysis of the global market dynamics, competitive landscape, and scenario. Various key insights presented in the report are the prevalence of diabetes, pricing analysis, technological advancements, and recent industry developments, such as mergers & acquisitions. Along with this, other key insights include key strategies adopted by market leaders, the competitive landscape, and company profiles.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type

|

|

By Distribution Channel

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size is valued at USD 38.77 billion in 2026, projected to reach USD 74.73 billion by 2034 at a CAGR of 8.55% during 2026–2034.

Growing at a CAGR of 8.55%, the market will exhibit steady growth in the forecast period (2026-2034)

Blood Glucose monitoring systems segment is expected to be the leading segment in this market during the forecast period.

Rising prevalence of diabetes globally is one of the key factor driving the growth of the market

F. Hoffmann-La Roche Ltd., and Medtronic are among the top players in the market.

North America is expected to hold the highest market share in the market.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us