Fats & Oils Market Size, Share & Industry Analysis by Type (Vegetable Oils [Sunflower Oil, Palm Oil, Soybean Oil, Canola/ Rapeseed Oil, Coconut Oil, and Others], and Fats [Butter, Tallow, Lard, Fish Oil, and Others]), By Source (Plant-based and Animal-based), By Form (Solid and Liquid), By Distribution Channel (B2B and B2C), By End-Use (Food [Food & Beverage Processing and Foodservice/ Culinary], and Non-Food [Nutraceuticals & Supplements, Cosmetics & Personal Care, Biofuels and Others]), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

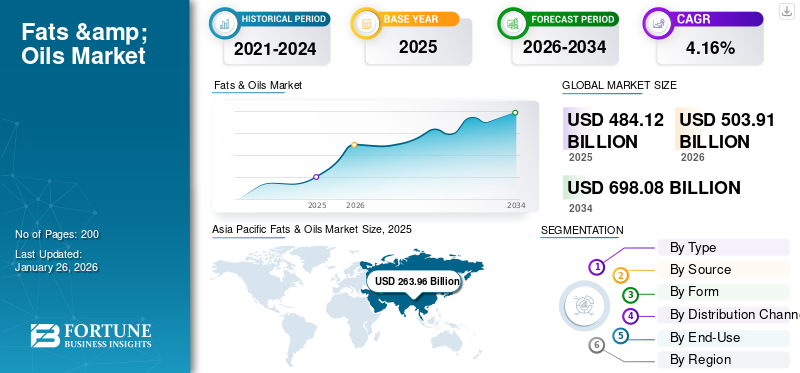

The global fats & oils market size was valued at USD 484.12 billion in 2025 and is projected to grow from USD 503.91 billion in 2026 to USD 698.08 billion by 2034, exhibiting a CAGR of 4.16% during the forecast period. Europe dominated the fats & oils market with a market share of 13.27% in 2025.

Fats and oils are both lipids that serve as significant sources of energy and essential fatty acids in human nutrition. In general, the industry exhibits strong growth catalyzed by the rising demand from household as well as industrial applications and growing regional production. Asia Pacific is the largest region, led by palm oil production in Indonesia and Malaysia and strong demand in large economies such as China and India.

Furthermore, the market encompasses several major players with Wilmar International Limited, Cargill Incorporated, Archer-Daniels-Midland (ADM), Bunge Limited, and Fuji Oil Holdings Inc. at the forefront.

Download Free sample to learn more about this report.

Fats and Oils Market Key Takeaways

- 2025 Market Size: USD 484.12 billion

- 2026 Market Size: USD 503.91 billion

- 2034 Forecast Market Size: USD 698.08 billion

- CAGR: 4.16% from 2026–2034

- Asia Pacific dominated the fats & oils market with a 54.52% share in 2025.

- The vegetable oils segment is projected to account for 90.53% market share in 2026.

- The liquid segment held 60.45% market share in 2025.

North America

North America accounted for 22.91% share in 2025, valued at USD 110.91 billion.

Asia Pacific

Asia Pacific held a 54.52% share in 2025, valued at USD 263.96 billion.

Europe

Europe contributed 13.27% share in 2025, valued at USD 64.25 billion.

U.S.

The market in the U.S. is driven by rising demand for organic and specialty fats & oils along with growing processed food consumption.

Japan

The market in Japan is supported by increasing edible oil demand and expanding food processing applications.

Read More

MARKET DYNAMICS

Market Drivers

Increase in Global Food Demand and Rising Disposable Incomes to Drive Market Growth

Fats & oils play a key role in cooking, including essential fatty acids, flavor, texture, and mouthfeel. As the production of food increases to sustain a growing global population, the demand for oils and fats also increases. Rising incomes particularly in developing countries encourage consumers to diversify and expand the market, raising edible oil usage as they add a greater range of culinary fats to everyday cooking. As families shift from subsistence diets to more protein-based meals, convenience foods, and processed snacks, the per-capita consumption of edible oils and specialty fats rises. Urban consumers and affluent households also purchase more packaged, ready-to-eat, and indulgent products that use vegetable oils, palm oil derivatives, and formulated fats for texture, shelf stability, and flavor, further increasing volume and product demand, driving fats & oils market growth.

- According to the National Bureau of Statistics of China, the national per capita disposable income increased by USD 3,055 per person in the first half of 2025.

Market Restraints

Volatile Raw Material Supply & Prices to Impede Market Growth

Major vegetable oils such as coconut and palm oil markets are dominated by strong price volatility driven by supply constraints such as weather impacts, mature plantations, and regulatory changes, and disseminating demand from food, cosmetic, and biofuel sectors. These drivers have led to the prices of coconut oil almost doubling in some export hubs. On the other hand, palm oil's fall as an affordable staple signals a broader shift in edible oils worldwide.

- According to the International Coconut Community, the prices for coconut oil rose from USD 1,126/MT to USD 1,610/MT during January-August 2024, roughly a 43% upsurge, reflecting tight supply and higher demand.

Market Opportunities

Expansion of Biodiesel Production in Asia Pacific and North America to Unlock New Growth Opportunities

The increase in biodiesel production in Asia Pacific and North America is transforming the market for the fats & oils industry by opening up new streams and breaking traditional consumption habits previously seen as focused on food and feed use. Additionally, increasing environmental pressure and climate policies further promote the adoption of biofuels, focusing more on the industrial market for biodiesel.

- Indonesia, for example, has expanded to the world's biggest biodiesel program, with the B35 blend mandate (35% palm biodiesel in diesel) propelling output to close to 13 billion liters in 2024.

Fats & Oils Market Trends

Growing Focus on Sustainability and Ethical Sourcing

The global market is witnessing a revolutionary change with sustainability at the center. Sustainability has become the central focus of sourcing actions in the global industry. Companies and organizations are implementing a range of measures to ensure that their supply chains are both environmentally and socially responsible. With the growing demand for certified sustainable palm oil, transition to regenerative agriculture techniques is being considered to reduce the carbon intensity of oilseed farming. Brands are making investments in sustainable certification, transparency programs, and biodegradable packaging.

- For instance, in March 2024, a fully owned subsidiary of Cooke Inc., Bioriginal Food & Science Corp., launched a sustainable line of omega-3 fish, plant-based, and algal oil with technology from POS Biosciences.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Widespread Use in Food Sector and Price Competitiveness Led to the Vegetable Oil Segment’s Highest Market Share

On the basis of type, the market is segmented into vegetable oils and fats.

The vegetable oils segment by type is projected to reach USD 456.21 billion, accounting for 90.53% of the market share in 2026. Vegetable oils such as palm, soybean, sunflower, and canola are readily available and comparatively inexpensive than animal fats as oilseeds such as soybean, palm, sunflower, and rapeseed are grown on a commercial scale, producing hundreds of liters of oil from a hectare of land at comparatively low labor expense. Moreover, vegetable oils are less expensive to store, transport, and handle as they are in liquid form and have a longer shelf life. These have boosted yields and decreased costs, making vegetable oils accessible to an increasingly large number of consumers across the globe. The food processing and fast-food businesses lead to a huge demand for vegetable oils as major components. Moreover, the biofuel industry also increasingly depends on vegetable oils such as palm oil and soybean oil for the production of biodiesel, thus increasing market growth further.

The fats segment is expected to grow significantly over the forecast period, with a CAGR of 4.53%.

By Source

Rising Demand for Healthier Options to Drive the Plant-Based Segment’s Dominant Market Share

On the basis of source, the market is segmented into plant-based and animal-based.

The plant-based segment dominates the global fats & oils market share. Plant-based oils such as olive oil, coconut oil, and others are often perceived as healthier alternatives due to their unsaturated fatty acid profile, driving demand among health-conscious consumers. The global plant-based diet food movement is further boosting product demand. Consumers increasingly seek vegan, vegetarian, and sustainable options, aligning with plant-based oils.

- According to the OECD-FAO Agricultural Outlook 2023, the global vegetable oil production was around 219 million metric tons in 2022, compared to less than 30 million metric tons for animal fats.

The animal-based segment is expected to grow significantly with a CAGR of 4.45% over the forecast period.

By Form

Higher Consumption in the Food Industry and Wider Industrial Applications to Lead Liquid Segment Growth

On the basis of form, the market is segmented into solid and liquid.

The liquid segment held the largest market share of 60.45% in 2025. Edible oils (vegetable oils such as soybean, sunflower, palm, canola, olive, and others) are the most commonly consumed form among the fats & oils industry as part of regular diets globally. In addition, oils are a pantry staple for frying, cooking, baking, and making salads, and are thus a necessity in household and foodservice operations. Besides food and beverage applications, liquid oils play a critical role in biofuels, cosmetics, and pharmaceuticals, providing a wider range of applications than solid fats.

The solid segment is expected to grow significantly at a CAGR of 4.37% over the analysis period.

By Distribution Channel

Health-Conscious Household Spending Fuels B2C Market Leadership

On the basis of distribution channel, the market is segmented into B2B and B2C.

To know how our report can help streamline your business, Speak to Analyst

The B2C segment is expected to hold a major share of the global market. Edible oils and fats are the mainstay ingredients used in everyday cooking in the majority part of the world; where oil consumption is high per capita. In addition, increased awareness regarding cholesterol, trans fats, and a rise in obesity has propelled consumers to seek for the low-fat, fortified, or specialty oils, including omega-3 enriched oils, cold-pressed oils, and organic oils. This trend is stronger in B2C, since end-consumers buy directly based on health perception. This segment is estimated to have held a share of 81.53% in 2025.

The B2B segment is anticipated to grow at the fastest CAGR of 4.14% during the forecast period.

By End-Use

Expanding Food Service Industry Secures Food Segment’s Market Leadership

Based on end-use, the market is segmented into food and non-food.

The food segment dominates the global market and held a 70.79% share in 2024. The food segment further consists of food & beverage processing and foodservice/culinary. Increasing population, urbanization, and changing dietary patterns are driving the higher consumption of edible oils and fats in cooking, frying, baking, and processed food production. Growing foodservice, such as the restaurant and bakery industries, further drives the demand for cooking oils and fats.

- According to the U.S. Census Bureau, in July 2025, spending at Food Services & Drinking Places in the U.S. experienced a 5.6% increase compared to July 2024.

The non-food segment is expected to grow significantly at a CAGR of 4.60% over the forecast period.

Fats & Oils Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, the Middle East, and Africa.

Asia Pacific

Asia Pacific Fats & Oils Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held a dominant share in 2024 and was valued at USD 253.62 billion. Asia Pacific accounts for a huge population of over 4.3 billion, with densely populated nations such as China and India. The huge consumer base translates into high demand for fats & oils. Urban lifestyle and increased incomes in the region are realigning plant-based diets toward increased edible oil and food processing consumption.

Asia Pacific is the world's largest palm oil-producing region, led by Indonesia and Malaysia. Low cost, versatility, and extensive use in food, biofuels, and industries give palm oil its dominance. This dominance led manufacturers to adopt various business strategies to boost palm oil demand. The Asia Pacific region captured 54.52% of the global market in 2025, generating USD 263.96 billion in revenue, and is projected to reach USD 274.66 billion in 2026.

- For instance, in January 2025, Hindustan Unilever Limited (HUL) acquired the palm undertaking of Vishwatej Oil Industries Private Limited, as a part of HUL’s Palm localization strategy. This acquisition is a key part of HUL’s Palm localization strategy aimed at building supply chain resilience for palm derivatives through backward integration.

Europe

Other regions, such as Europe and North America, are anticipated to witness notable growth in the coming years. During the forecast period, North America is projected to record a growth rate of 3.86%, which is the second highest amongst all the regions, and touch a valuation of USD 110.91 billion in 2025. This is primarily fueled by health trends, processed food consumption, and specialty oil consumption over the forecast period. The growing demand for organic and specialty fats & oils driven by consumer preference for traceable, pesticide-free, and sustainably sourced products is one of the significant factors driving the growth of oils and fats market in the U.S. Moreover, the increasing consumption of processed and convenience foods, which require frying and cooking oils, further boosts the demand from food processors and manufacturers, driving market growth. In 2025, the Europe market stood at USD 64.25 billion, representing 13.27% of global demand, and is projected to grow to USD 67.96 billion in 2026.

North America

In Europe, the U.K. is expected to have recorded a valuation of USD 14.00 billion; Germany, USD 19.12 billion; and France, USD 10.26 billion, in 2025. The growth is benefited from trends toward healthier, plant-based fat alternatives and increased consumption in the bakery, confectionery, and processed food sectors. North America contributed approximately USD 110.91 billion to the global market in 2025, accounting for 22.91% share, and is expected to reach USD 115.05 billion in 2026.

Latin America

Over the forecast period, South America and the Middle East & Africa regions would witness a moderate growth. The South America market, in 2025, is estimated to have recorded a valuation of USD 29.71 billion. Rapid urbanization and growing populations are driving the demand for convenience foods rich in oils and fats in these regions. In the Middle East & Africa, the UAE is anticipated to have touched a value of USD 7.95 billion in 2025. Latin America recorded a market size of USD 29.71 billion in 2025, capturing 6.14% of the global market share, and is projected to reach USD 30.41 billion in 2026.

Middle East & Africa

In 2025, Middle East & Africa generated USD 15.29 billion, contributing 3.16% to global market revenue, and is projected to grow to USD 15.82 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Strategic Mergers & Acquisitions and Joint Ventures to Support Market Growth

The global fats & oils market is moderately consolidated with the activities of large multinational players who hold dominant shares of global production, refining, and distribution of edible oils and fats. The industry has been experiencing constant mergers, acquisitions, and joint ventures for upgrading processing plants and supply chains. However, with aggressive competition from country and regional level producers, the consolidation has remained moderate rather than high. Key players operating in the market are Wilmar International Limited, Cargill Incorporated, Archer-Daniels-Midland (ADM), Bunge Limited, and Fuji Oil Holdings Inc.

Apart from this, other prominent players in the market include AAK AB, Musim Mas Group, IOI Corporation Berhad, and others.

Key Players in the Fats & Oils Market

|

Rank |

Company Name |

|

1 |

Wilmar International Limited |

|

2 |

Cargill, Incorporated |

|

3 |

Archer-Daniels-Midland (ADM) |

|

4 |

Bunge Limited |

|

5 |

Fuji Oil Holdings Inc. |

List of Key Fats & Oils Companies Profiled

- Wilmar International Limited (Singapore)

- Cargill, Incorporated (U.S.)

- Archer-Daniels-Midland (ADM) (U.S.)

- AAK AB (Sweden)

- Bunge Limited (U.S.)

- Musim Mas Group (Indonesia)

- IOI Corporation Berhad (Malaysia)

- Fuji Oil Holdings Inc. (Japan)

- IFFCO Group (UAE)

- Associated British Foods PLC (ABF) (U.K.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Sveda, a U.S.-based cosmetics company, launched its first beef tallow skincare line featuring three tallow-based products: a Whipped Tallow Balm for the face, a solid Hydrating Tallow Balm for full-body use, and a Tallow Lip Balm for dry or chapped lips.

- January 2025: Bayer and Neste announced a partnership for developing novel vegetable oils using regenerative agriculture concepts, with a strong focus on winter canola as a key crop. The collaboration aims to develop a business ecosystem around the production of winter canola in the U.S. The crop will serve as a new rotational crop integrated into regenerative agriculture practices, producing lower-carbon-intensity raw materials for renewable fuels such as sustainable aviation fuel and renewable diesel.

- December 2024: A Canadian collaboration involving Onda, the largest contract research organization specializing in aquaculture research, and the Canola Council of Canada (CCC) aimed at expanding the usage of Canadian canola as an ingredient for sustainable aquaculture feed. The focus is on evaluating canola meal as a sustainable, plant-based protein source for fish feed, especially for species such as salmon.

- March 2023: Corteva Agriscience, Bunge, and Chevron announced a multi-year partnership for introducing proprietary winter canola hybrids which produce a lower carbon profile plant-based oil. The move is aimed at catering to the growing demand for lower-carbon renewable fuels in the U.S.

- February 2022: Dabur Ltd launched its "Virgin Coconut Oil", marking its entry into the coconut oil market with a product that is 100% natural and extracted through cold-press technology. The new product is marketed as suitable for cooking, including deep frying, sautéing, and salad dressings, as well as for traditional uses such as skin and hair care and massage oil.

REPORT COVERAGE

The global market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, and end-use. Besides this, the global market report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 4.16% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Vegetable Oils o Sunflower o Palm o Soybean o Canola/ Rapeseed o Coconut o Others · Fats o Butter o Tallow o Lard o Fish Oil

|

|

By Source · Plant-based · Animal-based |

|

|

By Form · Solid

|

|

|

By Distribution Channel · B2B · B2C |

|

|

By End-Use · Food o Food & Beverage Processing o Foodservice / Culinary · Non-Food o Nutraceuticals & Supplements o Cosmetics & Personal Care o Biofuels o Others |

|

|

By Region · North America (By Type, Source, Form, Distribution Channel, End-Use, and Country) • U.S. (By End-Use) • Canada (By End-Use) • Mexico (By End-Use) · Europe (By Type, Source, Form, Distribution Channel, End-Use, and Country) • Germany (By End-Use) • Spain (By End-Use) • Italy (By End-Use) • France (By End-Use) • U.K. (By End-Use) • Rest of Europe (By End-Use) · Asia Pacific (By Type, Source, Form, Distribution Channel, End-Use, and Country) • China (By End-Use) • Japan (By End-Use) • India (By End-Use) • Australia (By End-Use) • Rest of Asia Pacific (By End-Use) · South America (By Type, Source, Form, Distribution Channel, End-Use, and Country) • Brazil (By End-Use) • Argentina (By End-Use) • Rest of South America (By End-Use) · Middle East & Africa (By Type, Source, Form, Distribution Channel, End-Use, and Country) • South Africa (By End-Use) • UAE (By End-Use) • Rest of the MEA (By End-Use) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 484.12 billion in 2025 and is anticipated to reach USD 646.10 billion by 2032.

The global market will exhibit steady growth at a CAGR of 4.16% over the forecast period.

By distribution channel, the B2C segment is the leading segment in the market.

Asia Pacific held the largest market share in 2025.

The globally rising food demand and disposable incomes are key factors driving the market growth.

Wilmar International Limited, Cargill Incorporated, Archer-Daniels-Midland (ADM), Bunge Limited, and Fuji Oil Holdings Inc. are the leading companies in the market.

Growing focus on sustainability and ethical sourcing is a key trend in the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us