Intraocular Lens (IOL) Market Size, Share & Industry Analysis, By Type (Monofocal and Premium {Multifocal, Toric, and Others}), By Material (Polymethylmethacrylate (PMMA) and Foldable {Hydrophobic Acrylic, Hydrophobic Acrylic, and Silicone & Collamer}), By End-user (Hospitals & Ambulatory Surgery Centers, Specialty Clinics, and Academic & Research Institutes), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

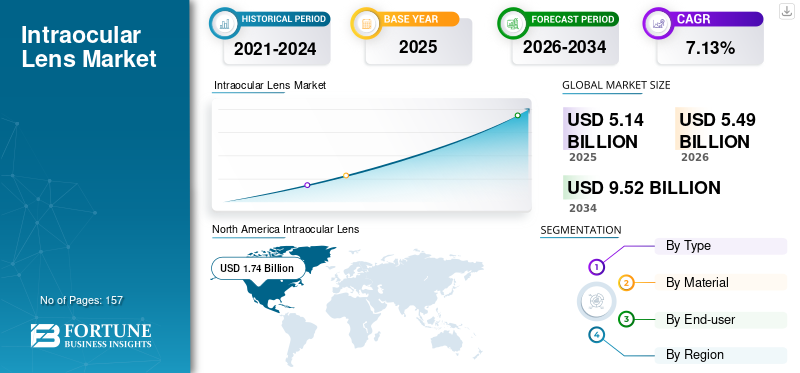

The global intraocular lens (IOL) market size was valued at USD 5.14 billion in 2025 and is projected to grow from USD 5.49 billion in 2026 to USD 9.52 billion by 2034, exhibiting a CAGR of 7.13% during the forecast period (2026-2034). North America dominated the intraocular lens market with a market share of 33.76% in 2025. Moreover, the U.S. intraocular lens market size is projected to grow significantly, reaching an estimated value of USD 2.44 billion by 2032, driven by rising prevalence of cataracts.

Intraocular Lens (IOL) is an artificial lens implanted in the eye during cataract and glaucoma surgeries. The increasing prevalence of cataracts has surged the demand for these procedures, coupled with significantly advanced product launches, collectively contributing to market growth. Additionally, the market is anticipated to expand over time due to the increasing demand for cataract intervention devices driven by unmet needs.

- For instance, according to the data published by the World Health Organization (WHO) in 2023, approximately 2.2 billion people suffer from near or distant vision impairment, and an estimated 94.0 million people suffer from cataracts globally. In that, only 17% of people with cataracts received the necessary intervention.

Furthermore, rising government support and favorable reimbursement policies have provided an impetus for patients to undergo cataract surgery. This scenario has spurred the adoption of these products. Rising initiatives to decrease the backlog of cataract surgeries and surge in eye care awareness in key countries are projected to drive market growth during the forecast period.

The COVID-19 pandemic negatively impacted the market, and the decrease in the surgical procedures associated with glaucoma and cataracts augmented the global drop in 2020. Also, the pandemic negatively affected sales, leading to a significant decline in the sales of intraocular products. The market returned to the pre-pandemic level with an increase in the number of patient visits to ophthalmologists and an upsurge in the sales of products in the international market in 2022. The market was stabilized in 2023, and it is expected to attain stable growth during the forecast period of 2024-2032.

Download Free sample to learn more about this report.

Intraocular Lens Market Key Takeaways

- 2025 Market Size: USD 5.14 billion

- 2026 Market Size: USD 5.49 billion

- 2034 Forecast Market Size: USD 9.52 billion

- CAGR: 7.13% from 2026-2034

- North America dominated the intraocular lens (IOL) market with a 33.76% share in 2025.

- The monofocal segment is projected to lead the market with a 64.41% share in 2026.

- The foldable segment is projected to account for an 87.59% share in 2026.

North America

North America accounted for USD 1.74 billion in 2025 and is projected to reach USD 1.85 billion in 2026.

Europe

Europe generated USD 1.48 billion in 2025 and is expected to reach USD 1.58 billion in 2026.

Asia Pacific

Asia Pacific represented USD 1.49 billion in 2025 and is projected to grow to USD 1.61 billion in 2026.

U.S.

The intraocular lens market is projected to reach USD 1.63 billion by 2026.

Japan

The intraocular lens market is projected to reach USD 0.68 billion by 2026.

Read More

Intraocular Lens (IOL) Market Trends

Product Launches of Extended Depth of Focus Products to Boost Market Growth

In recent years, the global market has witnessed several technologically advanced product offerings. The rising prevalence of cataracts has led to an intense need for these products. For the first time, in July 2016, the extended depth of focus products received U.S. FDA approval. The increase in initiatives by key players to launch products with new technology facilitates the growth of the market.

- For instance, in January 2024, Alcon Inc. announced the commercial launch of the state-of-the-art product name AcrySof IQ VivityTM IOL (Vivity), an intraocular lens with extended depth of focus in the U.S. market.

Furthermore, numerous advanced studies are being undertaken to explore the benefits of these newer technologies. For instance, as of May 2022, according to an ongoing study published by the ClinicalTrails.gov (U.S. National Library of Medicine), U.S.-based SightMD sponsored a study to evaluate the impact of a novel extended depth of focus IOL on visual and lifestyle enhancement. Such key trends are predicted to contribute significantly to the global intraocular lens market growth.

Download Free sample to learn more about this report.

Intraocular Lens (IOL) Market Growth Factors

Increase in the Number of Cataract Surgeries to Drive Market Growth over the Forecast Period

The global demand for cataract surgery is rising as it is one of the most commonly performed ophthalmic procedures globally. Market growth is driven by the increasing prevalence of cataracts and the associated visual impairments.

- According to the data published in August 2023 by the National Programme for Control of Blindness and Visual Impairment (NPCBVI), around 83,44,824 cataract surgeries were performed in India in FY 2022-2023 and such trends is estimated to drive the global market revenue during the forecast period.

Additionally, the increasing geriatric population leading to the growing number of age-related cataracts has also played a significant role in driving the market growth.

According to Association for Research in Vision and Ophthalmology, in 2020, an estimated 15.2 million people aged 50+ years were blind and a further 78.8 million had cataracts, which is expected to favor the market growth during the forecast period. Hence, the factors above mentioned are prominent drivers for the global market to flourish over the forecast period.

Launch of Several Government Initiatives for Cataract Elimination to Surge Product Demand

The rising prevalence of cataracts poses an economic and healthcare burden in numerous countries. This has led to the launch of several initiatives by various governments aimed at eliminating cataracts. Vision 2020 is a global initiative launched by the International Agency for the Prevention of Blindness (IAPB), intending to eliminate the leading causes of avoidable blindness worldwide. Vision 2020 involves the active participation of governments of 53 countries to accomplish the target of Vision 2020 through favorable reimbursement policies, eye checkup camps, and other measures.

Additionally, the Union Health Ministry of India is running a campaign, Netra Jyoti Abhiyan, to perform cataract surgeries in India and to clear the backlog of cataract surgeries by allotting a yearly target to the State and Union Territory. Thus, the development of such initiatives will firmly propel the global market growth over the forecast period.

RESTRAINING FACTORS

Absence of Reimbursement Policies for High-End Products in Different Countries Impedes Growth Opportunity

The global demand for cataract procedures remains high, but the lack of reimbursement policies for premium products poses a significant barrier to market growth, particularly in emerging countries. These premium products are highly beneficial for addressing issues, such as cloudy vision, age-related vision loss, nearsightedness, farsightedness, and astigmatism. However, the limited availability of reimbursement for these products hampers their adoption and restricts the growth of the market.

Additionally, in developed as well as developing countries, a significant proportion of the population is unaware of these premium product options, and there is an abundance of inadequate reimbursement policies. According to an article published by PRISTYN CARE in 2023, health insurance does not cover the cost of premium Intraocular Lens, prescribed eyeglasses, and eye drops or medications in India. The abovementioned factors hamper the adoption of these products, thus restricting the global market growth.

Intraocular Lens (IOL) Market Segmentation Analysis

By Type Analysis

Affordability of Monoclonal Lens Boosted Segment Growth

The market is segmented based on type into monofocal and premium. The premium segment is further sub-segmented into multifocal, toric, and others. The monofocal segment is projected to lead the market with a 64.41% in 2026, as the products are cheaper than premium products. Also, the rising number of government initiatives for utilizing monofocal lenses for cataract surgeries has significantly propelled the segment’s expansion. According to the National Institutes of Health (NIH) article in 2022, monofocal lenses are amongst the most commonly implanted products. Furthermore, as these products are more favorably reimbursed, the popularity of these products amongst the general population also contributes to its growth prospects.

The premium segment is projected to witness growth high growth potential during the forecast period. In the premium segment, the multifocal intraocular lens has more product adoption. The growth of the premium segment is driven by several key advantages it offers in treating complex vision issues, such as presbyopia or astigmatism. Furthermore, ongoing technological advancements in lens production are making them more affordable and accessible to consumers, thereby fueling the growth of this segment.

To know how our report can help streamline your business, Speak to Analyst

By Material Analysis

High Demand for Hydrophobic Acrylic Products Favors the Foldable Segment’s Dominance during 2024-2032

The market is segmented based on material into polymethylmethacrylate (PMMA) and foldable.

The foldable segment is sub-segmented into hydrophobic acrylic, hydrophilic acrylic, and silicone & collamer. The foldable segment is projected to lead the market with a 87.59% in 2026, due to its high refractive index and low water content and boosting its preference. Additionally, the products composed of foldable material can be inserted through small incisions and can be more widely utilized in cataract surgeries. For instance, in January 2023, Rayner Group organized a ‘Peer2Peer: The Podcast’, a clinical education platform for surgeons to educate them about their toric IOLs. Toric IOLs can be composed of foldable material such as Alcon’s AcrySof Toric IOL. Such factors contributed to the segment’s expansion.

The polymethylmethacrylate (PMMA) segment is projected to have the second-largest market position in the forecast period. PMMA was one of the first materials used for the manufacturing of Intraocular Lens. PMMA is significantly used in Europe and the rest of the world due to its significant cost advantage compared to acrylic products. Hence, the cost-effectiveness of PMMA is anticipated to augment the segmental growth in 2024-2032.

By End-user Analysis

Favorable Government Policies to Drive the Growth of Hospitals & Ambulatory Surgery Centers

Based on end-user, the market is segmented into hospitals & ambulatory surgery centers, specialty clinics, and academic & research institutes.

The hospitals & ambulatory surgery centers segment dominates the market and is projected to grow, as hospitals are prime care centers for cataract procedures. Furthermore, favorable government policies for cataract procedures and rise in the number of government hospitals are some of the fundamental reasons for the growth of this segment. According to a news article published by the Hindu in May 2022, the Government of India has proposed a special drive to clear the backlog of cataract surgeries. They will increase the number of cataract surgeries in the financial year 2022-23, 2023-24, and 2024-25 with 7.5 million, 9.0 million, and 10.5 million surgeries, respectively. The number of cataract surgeries will be done under a special campaign to clear the backlog, and all the Indian states shall be given guidance to conduct these procedures. Hospitals & Ambulatory Surgery Centers segment is projected to lead the market with a 57.42% in 2026.

The specialty clinics segment occupies the second-largest market share in the year 2023. The rise in standalone eye clinics in developed and developing regions is projected to contribute to the segment’s growth. The academic & research institutes segment is expected to attain growth prospects due to active government efforts to train ophthalmologists and the increasing number of doctors opting for fellowship programs to learn about the latest medical technologies.

REGIONAL INSIGHTS

Based on region, the global market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

In 2025, North America represented USD 1.74 billion, accounting for 33.76% of the worldwide market, and is projected to grow to USD 1.85 billion in 2026 and this region is anticipated to lead the global market during the forecast period. The region’s market dominance is owing to the substantial demand for novel products such as custom cataract lenses, rapid adoption of these products, and favorable insurance policies. Moreover, regulatory approvals for these innovative products contribute to the region’s growth prospects. The U.S. market is projected to reach USD 1.63 billion by 2026.

North America Intraocular Lens (IOL) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

The Europe market generated USD 1.48 billion in 2025, representing 28.88% of the global market landscape, and is expected to reach USD 1.58 billion in 2026. The growth is due to the increasing number of cataract surgeries, rising adoption of femtosecond lasers to transect hydrophobic and hydrophilic acrylic lenses for cataract surgeries, and the increased preference for toric lenses. As per an article published by the National Institutes of Health (NIH) in 2020, Europe has an estimated 64.0% cataract prevalence for the population over 70 years, and it increases with age, with higher rates in Germany and Italy. Thus, the growing patient pool favors global market growth. The UK market is projected to reach USD 0.18 billion by 2026, and the Germany market is projected to reach USD 0.39 billion by 2026.

Asia Pacific

Asia Pacific contributed 29.07% to the global market in 2025, with a valuation of USD 1.49 billion, and is projected to reach USD 1.61 billion in 2026. Rising geriatric population is a common contributor to the overall prevalence of cataracts in the region since the aged population is more prone to cataracts. According to an article published by the Multidisciplinary Digital Publishing Institute (MDPI) (Basel, Switzerland) in 2021, per eight years of the study, the incidence rate for IOL dislocation was 360 per 1,000,000 person-years in South Korea. Thus, the rising cases of eye disorders in key countries in the rest of Asia Pacific region contribute to the overall region’s growth. The Japan market is projected to reach USD 0.68 billion by 2026, the China market is projected to reach USD 0.14 billion by 2026, and the India market is projected to reach USD 0.42 billion by 2026.

Latin America

The market in Latin America reached USD 0.27 billion in 2025, representing 5.31% of total market revenue, and is projected to reach USD 0.29 billion in 2026. According to an article published by the National Institutes of Health (NIH) in 2021, a study was conducted in an ophthalmology referral center to check awareness amongst Mexican patients with and without glaucoma diagnosis. It was found that the awareness and knowledge of glaucoma in subjects attending an ophthalmology referral center is predominantly moderate or poor. Such studies to check the eye care awareness ratio favors the creation of new market growth opportunities in the near future.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.15 billion in 2025, capturing 2.97% of global revenue, and is estimated to reach USD 0.16 billion in 2026.The Middle East & Africa is predicted to grow slower due to the lack of public awareness and reimbursement policies in the developing countries in these regions.

List of Key Companies in Intraocular Lens (IOL) Market

Robust Product Launches and Global Presence of Alcon and J&J to Lead the Market with their Peak Positions in 2023

In terms of the competitive landscape, the market represents a consolidated structure with some major players accounting for a dominant proportion of the global market. Alcon Inc., acquired a peak market position with a robust portfolio for Intraocular Lens, which includes their ACRYSOF product portfolio and an established geographical presence. Also, novel product launches and emphasis on strategic initiatives have been some of the prominent driving factors for Alcon Inc. to capture a higher market share. Furthermore, the second leading players in the global market are Johnson & Johnson Vision Care, Inc. and Johnson & Johnson Surgical Vision, Inc. due to their strong market presence in key regions coupled with robust distribution networks. For instance, according to a survey published by Jobson Medical Information LLC in 2021, the two most popular monofocal lens choices on the survey were the Alcon IQ Aspheric with 43.0% and the Johnson & Johnson Vision Tecnis 1-piece with 36.0%.

The other market players, such as Carl Zeiss Meditec AG, Bausch & Lomb Incorporated, HOYA, and STAAR Surgical Company, also generated significant sales for these products. Apart from this, a focus on increasing their market presence through advanced launches and strategic initiatives is also anticipated to strengthen the market position of the above-mentioned companies.

LIST OF KEY COMPANIES PROFILED:

- Alcon Inc. (Switzerland)

- Johnson & Johnson Vision Care, Inc. and Johnson & Johnson Surgical Vision, Inc. (U.S.)

- Bausch & Lomb Incorporated (Canada)

- HOYA (Japan)

- STAAR SURGICAL (U.S.)

- Rayner Intraocular Lenses Limited. (U.K.)

- Hanita Lenses (Israel)

- SIFI S.p.A (Italy)

- Biotech (Switzerland)

KEY INDUSTRY DEVELOPMENTS:

- November 2023- Ophtec launched a hybrid acrylic IOL named Precizon Go to provide distance and enhanced intermediate vision.

- October 2023- Bausch & Lomb Incorporated announced the launch of enVista Aspire monofocal and toric intraocular lenses (IOLs) in the U.S. market.

- January 2023- Centricity Vision Inc.’s ZEPTO IOL Positioning System improved the precision and accuracy of cataract surgery and is preferred for office-based surgeries (OBS).

- September 2022: Bausch & Lomb Incorporated entered into an exclusive distribution agreement with Alfa Instruments s.r.l. Intraocular Dyes. Bausch & Lomb will distribute and commercialize the Alfa Instruments line of surgical intraocular dyes globally.

- September 2022: SIFI S.p.A launched Evolux extended monofocal Intraocular Lens. The product is based on a hydrophobic material and a non-diffractive profile to provide better intermediate and equivalent distance vision.

- August 2022: Alcon Inc. entered into a definitive merger agreement with Aerie Pharmaceuticals, Inc. Alcon will acquire commercial products of Aerie to expand its ophthalmic pharmaceutical segment.

- April 2022: Rayner Intraocular Lenses Limited collaborated with Aston University to develop the next generation of lenses that gives patients a high-quality full range of vision.

- March 2022: Alcon Inc. launched the Clareon family of IOL in the U.S. by utilizing the most advanced material.

- January 2022: Alcon Inc. launched AcrySof IQ Vivity IOL (Vivity) in India. It is the first and only presbyopia-correcting intraocular lens (PC-IOL) with wavefront-shaping technology.

- January 2020: HOYA entered into a distributor partnership with GeMax. The organization GeMax is a specialty promotion service provider of Intraocular Lens with a strong market position and a professional reputation in China, covering more than 630 major hospitals in 32 provinces.

REPORT COVERAGE

The global market research report consists of a detailed market overview. The global market is segmented by type, material, end-user, and geography. The market analysis highlights vital aspects such as market dynamics, key industry developments such as mergers, acquisitions, and partnerships, new product launches, an overview of government cataract initiatives, regulatory and reimbursement scenarios, prevalence of cataracts, number of cataract surgeries, key market players, and COVID-19 pandemic effect on the market. Apart from this, the report includes insights into the market trends and industry dynamics contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.13% from 2026 to 2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type

|

|

By Material

|

|

|

By End-user

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.14 billion in 2025 and is expected to reach USD 9.52 billion by 2034.

North America stood at USD 1.74 billion in 2025.

The global market is projected to grow at a CAGR of 7.13% over the forecast period.

The monofocal segment is expected to be the leading segment in this market during the forecast period.

The rise in demand for these cataract procedures, technological advancements, and favorable government initiatives are driving the market growth.

Alcon, Inc., Carl Zeiss Meditec AG, and Bausch & Lomb Incorporated are some of the key players in the global market.

North America dominated the intraocular lens market with a market share of 33.76% in 2025.

Advanced product launches, mounting government initiatives for cataract elimination, and rise in the number of cataract procedures contribute to the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 157

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us