Kidney Stone Management Market Size, Share, Trends & COVID-19 Impact Analysis, By Type (Lithotripsy, Ureteroscopy, and Percutaneous Nephrolithonomy (PCNL) By End User (Hospitals, Specialty Clinics, and Ambulatory Surgical Centers), and Regional Forecast, 2026-2034

Kidney Stone Management Market Size & Share

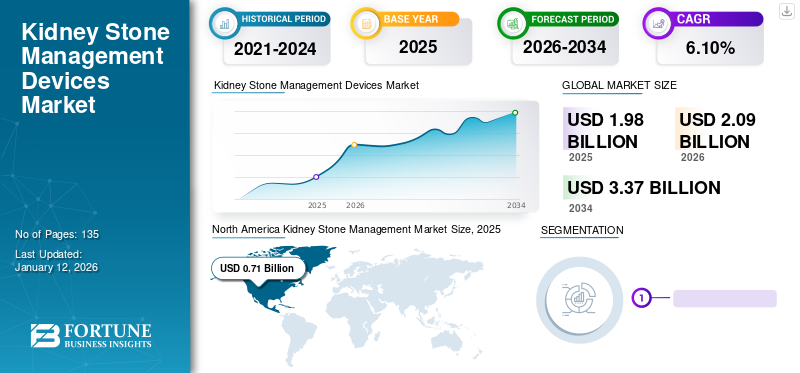

The global kidney stone management market size was valued at USD 1.98 billion in 2025. The market is projected to grow from USD 2.09 billion in 2026 to USD 3.37 billion by 2034, exhibiting a CAGR of 6.10% during the forecast period. North America dominated the kidney stone management market with a market share of 36.03% in 2025.

The market for kidney stone management devices is growing due to the rising preference for minimally invasive surgeries, fewer complications, less post-surgical pain, and a lower recurrence rate of kidney stones. Moreover, increase in the prevalence of kidney stones is further driving the market. According to the Journal of the American Society of Nephrology 2018, kidney stone disease or nephrolithiasis, occurs worldwide, with a prevalence percentage of 7% in adults, and a more than 30% recurrence rate within 10 years. In addition, technological advancements in ureteroscopes such as fiber optics flexible ureteroscopes, are likely to drive the market shortly.

Download Free sample to learn more about this report.

Global Kidney Stone Management Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 1.98 billion

- 2026 Market Size: USD 2.09 billion

- 2034 Forecast Market Size: USD 3.37 billion

- CAGR: 6.10% from 2026–2034

Market Share:

- Region: North America dominated the market with a 36.03% share in 2025. This is due to a higher prevalence and incidence of stone diseases, favorable reimbursement policies, rising patient awareness of new treatment options, and the availability of advanced medical devices.

- By Type: The Ureteroscopy segment held the dominant market share. The segment's leadership is attributed to the minimally invasive nature of the procedure, its high success rate, and a lower recurrence rate of kidney stones, which are major factors driving its adoption.

Key Country Highlights:

- Japan: As a key country in the fast-growing Asia Pacific market, growth is driven by growing patient awareness of advanced medical devices and a large, underpenetrated patient pool, which is attracting major industry players.

- United States: The market is fueled by a high prevalence of kidney stone disease, affecting over 10% of the population in high-standard-of-life countries. The market is also supported by the rapid adoption of minimally invasive surgical techniques for stone removal.

- China: Growth is propelled by an increasing patient pool, growing awareness of advanced medical devices, and the underpenetrated nature of the market, which is attracting significant investment and expansion from global companies.

- Europe: The market is advanced by a rising incidence of kidney stones in countries such as Germany and Spain. The high acceptance of technologically advanced products, increasing healthcare expenditures, and favorable reimbursement policies are key growth factors.

KIDNEY STONE MANAGEMENT MARKET LATEST TRENDS

Download Free sample to learn more about this report.

Innovations in Kidney Stone Treatment to Fuel the Market

The introduction of new techniques and devices in stone disease treatments is revolutionary for healthcare providers as well as for patients. Some of the new stone braking innovations includes miniaturized surgery, holmium laser technologies, and disposable ureteroscopes. In March 2020, Lumenis announced the clinical evidence and advantages in lithotripsy and benign prostatic hyperplasia (BPH) treatments using the MOSES Technology. This technology uses a highly energized laser to destroy kidney stones. MOSES is user friendly and helps doctors to rupture the stones without injuring the surrounding tissues with minimum bleeding.

DRIVING FACTORS

Increase Prevalence of Kidney Stone Diseases to Accelerate Growth

The recurrence and prevalence of kidney stone diseases are increasing globally. There are limited options of adopting effective drugs to treat the disease. Urolithiasis is estimated to affect an estimated 12% of the world population at some point in their lifetime. According to a data published by the European Association of Urology and the National Kidney Foundation in 2019, in countries with a high standard of living, such as the U.S., Canada, and Sweden, the prevalence of this disease has been reported to be more than 10%. Moreover, some other diseases such as obesity, diabetes, and high blood pressure may increase the risk for kidney stones.

Growing Adoption of Minimally Invasive Stone Removal Procedures To Drive the Market Growth

Surgeons have rapidly adopted minimally invasive surgical (MIS) techniques for a wide range of applications. High adoption of minimally invasive techniques in general surgery and their minimal side effects compared to open surgical procedures are likely to drive the demand for advanced procedures for kidney stone management in the near future. According to the Journal of Advances in Chronic Kidney Diseases, minimally invasive treatments that have been adopted mainly for three stone diseases in the United States market include extracorporeal shock wave lithotripsy, ureteroscopic lithotripsy, and percutaneous nephrolithotomy. Surgeons are using minimally invasive surgical techniques to conduct procedures that were earlier performed as an open surgery. These changing market dynamics are propelling the demand for the kidney stone management devices.

RESTRAINING FACTORS

Side Effects Related with Shock Wave Lithotripsy to Hamper Growth

Despite the increasing incidence of stone diseases, there are certain factors that are limiting the adoption of its treatment. One of the major factors obstructing the growth of the market is its side effects such as bleeding around kidneys, blockage of urine due to broken stones, infections, and increase in the arterial blood pressure, among others. related to the shock wave lithotripsy. According to the American Journal of Kidney Diseases, shock wave lithotripsy may pose side effects such as rise in the arterial blood pressure, reduction in renal function, and stone recurrence. Together these complications are expected to hinder the market growth during the forecast period.

Impact of COVID– 19 on Kidney Stone Management Devices

The COVID-19 pandemic made an adverse impact on the kidney stone management sector, resulting in the drop in revenue. The lockdown caused by the pandemic resulted in the sluggish diagnosis rate forkidney stone disease. Many small hospitals and nursing homes were forced to temporarily shut their operations because of the Lockdown. This was done to break the transmission of infections and diversion of healthcare resources to manage COVID-19 patients. According to the Johns Hopkins University Carey Business School 2020, poor supply chain management, limited availability of raw materials, sluggish medical device manufacturing rate, and slowdown in the economy are major factors hampering the kidney stone treatment devices market.

KIDNEY STONE MANAGEMENT MARKET SEGMENTATION ANALYSIS

By Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Ureteroscopes Segment Held Dominating Share Owing to High Success Rates of Procedures

Based on type, the market is segmented into lithotripsy, ureteroscopy, and percutaneous Nephrolithonomy (PCNL).

Among these, the ureteroscopy segment is projected to dominate the market with a share of 51.59% in 2026. Minimally invasive ureteroscopes, high success rate, and low recurrence rate are the major factors contributing to the dominance of this segment. Moreover, ureteroscopes is expected to record a significantly high CAGR due to the advantages offered by the segment.

By End User Analysis

Early Adoption of Innovative Technologies by Hospitals to Dominate Segment

Based on end-user, the market segments include hospitals, specialty clinics, and ambulatory surgical centers.

Among them, the hospitals segment is expected to lead the market, contributing 55.89% globally in 2026. Growing number of patients with kidney stones and adoption of advanced technologies by hospitals are diving this segment. Moreover, satisfactory reimbursement provided by hospitals is the major factor responsible for growth of this segment. However, the specialty clinics segment is projected to register highest growth during the forecast period. Growing number of skilled surgeons, coupled with favorable reimbursement policies offered by the specialty clinics, will augment the growth of the specialty clinics segment.

REGIONAL INSIGHTS

North America Kidney Stone Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, the North America market stood at USD 0.71 billion, representing 36.03% of global demand, and is projected to grow to USD 0.75 billion in 2026. This is characterized by higher prevalence and incidence of stone diseases, coupled with favorable reimbursement policies for health associated disorders. Moreover, the rising awareness among the patient population about new treatment options for stone diseases and the availability of advanced medical devices in the region are aiding in the expansion of the regional market. The U.S. market is projected to reach USD 0.68 billion by 2026.

Europe

The Europe region captured 30.01% of the global market in 2025, generating USD 0.6 billion in revenue, and is projected to reach USD 0.63 billion in 2026. Europe, on the other hand, holds the second largest share due to the rising incidences of kidney stones. Factors such as higher acceptance of technologically advanced products in the region, rising healthcare expenditures, and favorable reimbursement policies are responsible for the share of the market. The UK market is projected to reach USD 0.07 billion by 2026, while the Germany market is projected to reach USD 0.16 billion by 2026.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 0.41 billion in 2025, accounting for 20.65% share, and is expected to reach USD 0.44 billion in 2026. However, the market in Asia-Pacific is anticipated to record a reasonably higher CAGR during the forecast period. Growing patient awareness regarding advanced medical devices, and presence of a large patient pool and being an underpenetrated market are projected to drive the Asia Pacific urinary stone treatment devices market growth during the forecast period. The Japan market is projected to reach USD 0.11 billion by 2026, the China market is projected to reach USD 0.14 billion by 2026, and the India market is projected to reach USD 0.05 billion by 2026.

Latin America and the Middle East & Africa

In 2025, Latin America represented USD 0.15 billion, accounting for 7.40% of the worldwide market, and is projected to grow to USD 0.16 billion in 2026. The Middle East & Africa market accounted for USD 0.12 billion in 2025, representing 5.91% of the global industry, and is expected to reach USD 0.12 billion in 2026. The market in Latin America and the Middle East & Africa are currently in a promising stage. However, the developing healthcare infrastructure in these regions and growing prevalence of stone diseases will boost this market demand during the forecast period.

KEY INDUSTRY PLAYERS

Strong Focus on Partnerships and Acquisition to Strengthen Global Presence of Industry Leaders

The competitive landscape of the urolithiasis management devices market demonstrates the dominance of leading players operating such as Boston Scientific Corporation, Olympus Corporation, KARL STORZ SE & Co. KG, and Richard Wolf GmbH. A diversified & technologically advanced product portfolio and global expansion of such products are prominent factors responsible for the dominance of these companies. Moreover, a strong emphasis on partnerships and acquisition strategies in the market is likely to help attract high market revenue in the forthcoming years.

LIST OF TOP KIDNEY STONE MANAGEMENT COMPANIES:

- Cook Medical Inc. (US)

- Boston Scientific Corporation (US)

- Olympus Corp. (Japan)

- C.R. Bard Inc. (BD) (US)

- STORZ MEDICAL AG (Switzerland)

- Richard Wolf GmbH (Germany)

- Lumenis (Israel)

- EDAP TMS (France)

- DirexGroup (Germany)

- Other prominent players

KEY INDUSTRY DEVELOPMENTS:

- September 2018 –Boston Scientific Corporation launched the LithoVue Empower Retrieval Deployment Device in the US and Europe for retrieval of kidney stones through flexible ureteroscopy (URS).

- October 2017–Lumenis launched the MOSES holmium technology for Urology applications in India. This geographical expansion of this product opened the new gateway of lucrative opportunities for the company

REPORT COVERAGE

The global kidney stone management market research report provides a detailed analysis of the market and focuses on key aspects such as leading companies, types, and end-users. Besides this, it offers insights into the market, current trends, and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over the recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.10% from 2021-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global kidney stone management market size is worth USD 3.37 billion by 2034.

In 2025, the market value stood at USD 1.98 billion.

Growing at a CAGR of 6.10%, the market will exhibit steady growth in the forecast period (2026-2034).

Lithotripter segment is the leading segment in this market during the forecast period.

Increase in the prevalence of kidney stone disease and minimally invasiveness of the surgeries are the key factors driving the market.

Scientific Corporation, Olympus Corporation, KARL STORZ SE & Co. KG, Richard Wolf GmbH are the top players in the market.

North America dominated the kidney stone management market with a market share of 36.03% in 2025.

Continuous innovation in kidney stone treatment and increasing mergers and acquisitions are the major trends of the market .

- 2021-2034

- 2025

- 2021-2024

- 135

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us