Ophthalmic Disease Therapeutics Market Size, Share & Industry Analysis, By Drug Class (Anti-inflammatory, Anti-infectives, Anti-VEGF, Anti-glaucoma {Beta Blockers, Prostaglandins Analogs, Alpha Adrenergic Agonists}), By Dosage Form (Solid, Liquid, & Semisolid), By Disease Indication (Glaucoma {Open Angle Glaucoma, Angle Closure Glaucoma}, Dry Eye Disease, Retinal Diseases {Diabetic Macular Edema, Macular Degeneration}, Allergy & Infections), By Distribution Channel (Hospital Pharmacies and Retail & Online Pharmacies), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

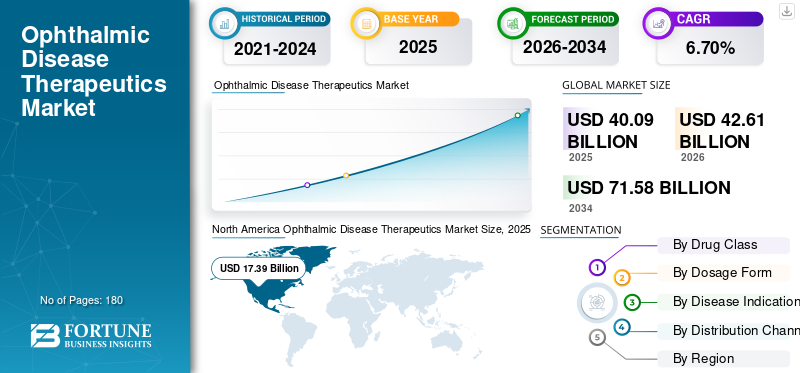

The global ophthalmic disease therapeutics market size was USD 40.09 billion in 2025. The market is projected to grow from USD 42.61 billion in 2026 to USD 71.58 billion by 2034, exhibiting a CAGR of 6.70% during the forecast period. North America dominated the global market with a share of 43.37% in 2025. Moreover, the U.S. ophthalmic disease therapeutics market size is projected to grow significantly, reaching an estimated value of USD 25.72 billion by 2034, driven by rising approvals and introduction of innovative therapies.

Ophthalmic disease therapeutics include drugs and therapies for the treatment of several ocular conditions such as glaucoma, dry eye disease, retinal diseases, and others. The increasing prevalence of these conditions among the population along with rising healthcare burden caused due to these conditions is expected to boost the demand for novel therapies and approaches for the management of these diseases.

- According to a 2021 article published by Bright Focus Foundation, there are 80 million people worldwide suffering from glaucoma, and the number is projected to increase over 111 million by 2040.

- Also, there are more than 3 million Americans living with glaucoma and the condition cost represents around 2.86 billion economic burden every year on the country.

Along with this, increasing research & development activities among market players to develop novel therapies and effective drugs for the ophthalmic disease therapeutics is expected to spur the ophthalmic disease therapeutics market growth.

However, the lack of awareness regarding the conditions along with limited availability of effective drugs and novel therapies for the treatment of ophthalmic disease is expected to restrain the growth of the market.

The COVID-19 impact on the market growth was negative during the forecast period. The temporary shutdown of the orthopedic clinics, higher focus of healthcare providers toward COVID-19 patients is one of the major factors responsible for the slower growth of the market during the pandemic. The lockdown restrictions imposed by the government authorities across the regions resulted in cancellation or postponement of services associated with several ophthalmic conditions and resulted in reduced number of patient visits to the hospitals and clinics. This led to decreased demand for ophthalmic disease therapeutics among the patient population globally.

- For instance, according to a 2021 article published by BMC Ophthalmology, there was more than 75% reduction of in-person clinic visits in the U.S. as a result of rescheduling of routine ocular examinations and limited procedures associated with non-urgent services.

The major players operating in the market witnessed a decline in their revenues owing to the demand gap due to the COVID-19 pandemic. However, with the uplifting of lockdown restrictions, the number of ophthalmic clinic visits significantly increased in 2021 recovering the missed and canceled appointments for various indications. This resulted in a slow recovery of the market in 2021 globally. The market is projected to witness steady growth prospects over the forecast period of 2026-2034.

Global Ophthalmic Disease Therapeutics Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 40.09 billion

- 2026 Market Size: USD 42.61 billion

- 2034 Market Size: USD 71.58 billion

- CAGR: 6.70% from 2026–2034

Market Share:

- Region: North America dominated the market with a 43.37% share in 2025. This is driven by the growing prevalence of various ophthalmic disorders, higher diagnosis and treatment rates, significant healthcare expenditure on eye care, and an increasing number of regulatory approvals for new drugs.

- By Disease Indication: Retinal diseases held the largest market share. The segment's dominance is attributed to the rising prevalence of conditions such as diabetic macular edema and macular degeneration, a growing patient population, and increased awareness initiatives that are leading to higher diagnosis rates.

Key Country Highlights:

- Japan: The market is driven by a strong focus on innovation and new product launches. For instance, Santen Pharmaceutical Co., Ltd. launched DIQUAS LX Ophthalmic Solution 3% for the treatment of dry eye, which is a key growth factor in the Asia Pacific region.

- United States: Market growth is fueled by a high prevalence of ophthalmic conditions, with around 3.0 million Americans suffering from glaucoma and an estimated 35.0 million from dry eye disease. The market is also supported by a robust pipeline of drugs and consistent new product approvals from the U.S. FDA.

- China: As part of the fastest-growing Asia Pacific market, China is seeing increased commercialization of advanced therapies. Strategic collaborations, such as the partnership to commercialize BRIMOCHOL PF and Carbachol PF eye drops for presbyopia, are expanding the availability of innovative treatments.

- Europe: The market is advanced by a high prevalence of eye diseases, particularly in the geriatric population. For example, in Germany, around 22.4% of the population is aged 65 and above, which increases the burden of age-related ophthalmic conditions. Regulatory approvals, such as the European Commission's authorization for Vabysmo to treat diabetic macular edema, are also driving growth.

Download Free sample to learn more about this report.

Ophthalmic Disease Therapeutics Market Trends

Rising Technological Advancements in Drug Delivery Options

The focus of research & development activities by various healthcare agencies and market players is shifting toward the development of innovative drug delivery systems. The challenges of the current ocular drug delivery systems owing to the anatomy and physiology of the eye is one of the major factors contributing to the shifting focus of the market players.

- For instance, according to a 2021 article published by National Center for Biotechnology Information (NCBI), an innovative drug delivery system using a dexamethasone-encapsulated cholesterol-Labrafac lipophile nanostructured lipid carrier-based ophthalmic formulation, which can be developed as an eye drop to treat dry eye disease (DED) and other infections.

Also, research institutes are increasing their focus to develop and introduce novel approaches for drug delivery and this is leading to increasing clinical studies. According to a 2021 report published by the Department of Ophthalmology of Penn Medicine, the researchers discovered that the use of an engineered, artificial protein coating can improve the ophthalmological drug uptake.

Similarly, the increasing focus on novel therapies and expansion of product portfolio are some of the major factors contributing to the shifting preference of the patient population.

- In March 2022, Johnson & Johnson Services Inc. received the U.S. FDA approval for ACUVUE Theravision with Ketotifen which is considered to be the world’s first and only drug eluting contact lens.

Furthermore, in the recent years, the focus toward the development of nanotechnology-based formulations for ophthalmic drug delivery has increased. According to data provided by the Bulletin of the National Research Centre in October 2023, in situ gel technology and nanotechnology improves the bioavailability and extended-release ocular medication delivery methods. This method enhances the management of ocular conditions and improves patient outcomes.

Also, the rising partnerships and collaborations among market players and research organizations to develop innovative and more effective gene therapies for the conditions is expected to support the shifting preference of the patient population toward novel therapies.

Download Free sample to learn more about this report.

Ophthalmic Disease Therapeutics Market Growth Factors

Rising Prevalence of Ophthalmic Conditions to Surge the Demand for Innovative Drugs

The growing prevalence of ophthalmic conditions such as glaucoma, retinal diseases, dry eye disease, and others among the population is one of the major factors contributing to the rising patient population globally. The prevalence of these ophthalmic conditions is found to be higher in the geriatric population.

- According to a 2020 article published by the American Academy of Ophthalmology (AAO), around 3.0 million Americans are suffering from glaucoma, among which 2.7 million Americans are aged 40 years or older.

- According to a 2020 report published by the U.S. Census Bureau, the population aged 65 years and older increased from 39.6 million in 2009 to 54.1 million in 2019 and the number is projected to reach 94.7 million in 2060.

The rising awareness among the general population regarding the ocular conditions owing to increasing number of initiatives carried out by various healthcare agencies, government bodies, and market players is resulting in higher diagnosis and treatment rate among the population.

Along with these factors, the rising healthcare expenditure and increasing number of ophthalmologists in the developed and emerging countries are some other factors that are expected to augment the demand for ophthalmic disease therapeutics in the market.

- According to the 2021 report published by the Welsh Government, the number of ophthalmic practitioners in Wales increased to 961 in March 2021 from 885 in March 2020.

Moreover, several market players are focusing on receiving regulatory approvals as well as the introduction of innovative products due to the growing burden of ophthalmic diseases.

- For instance, in December 2023, Glaukos announced that the U.S. FDA has granted its iDose TR for reducing intraocular pressure for patients suffering from ocular hypertension and open-angle glaucoma.

Thus, these factors coupled with increasing focus of the market players to develop and introduce novel drugs, and therapies for the treatment of the conditions is expected to boost the demand and adoption of these drugs in the market during the forecast period.

Increasing Clinical Trials and Pipeline Candidates for Innovative Drugs and Therapies to Propel the Market Demand

The rising prevalence of ophthalmic disease among the population is one of the factors contributing to the growing demand for effective drugs and treatment for the condition. This is resulting in increasing focus of market players and research organizations to develop and launch innovative therapies for the treatment of the condition.

Furthermore, increasing involvement of operating players in the research and development of novel therapies for the treatment of the condition is expected to exhibit a higher demand for ophthalmic disease therapeutics in the market during the forecast period. The increasing focus and robust efforts of the key players operating in the market to develop and launch novel therapies for catering the unmet demand for the rising patient population is expected to increase the consumption of the ophthalmic drugs.

- According to the ClinicalTrials.gov, there are around 44 pipeline candidates for macular degeneration in phase III clinical trials.

- In November 2022, Santen Pharmaceutical Co., Ltd. launched DIQUAS LX, an ophthalmic solution 3% for the treatment of dry eye.

Thus, increasing patient population undergoing treatment along with rising number of approvals and launches of innovative drugs and therapies are expected to spur the market growth during the forecast period.

RESTRAINING FACTORS

High Cost of Biologics and Overall Treatment Cost is Limiting the Adoption of the Product

There are several clinical benefits of biologics and biosimilars such as higher effectiveness, safety, and others. However, certain limitations such as higher cost of biologics, higher out-of-pocket spending, and others. Higher cost of biologics owing to its several benefits and various costs associated with its development and approvals is a crucial factor limiting the adoption of these drugs in the emerging countries.

- According to 2019 article published by Journal of Pharmacology and Pharmacotherapeutics, a single treatment of Lucentis (ranibizumab) costs around USD 1,950 to USD 2,023 per dose, and Eylea costs around USD 1,850 per intravitreal dose. The annual cost of therapy can range around USD 14,000 to USD 23,500 for the patients.

Other challenges for the healthcare system especially in the emerging countries such as China, Brazil, Mexico, and African countries is lower awareness of the conditions among the population resulting in lower rate of diagnosis of the conditions. Therefore, the increasing gap between the patient population and treatment for the conditions along with higher out-of-pocket expenditure is expected to slow the adoption of ophthalmic disease therapeutics.

- According to a 2019 article published by Nigerian Journal of Clinical Practice, the average cost per visit to primary healthcare providers in South Africa costs around USD 30-40, whereas in Kenya the cost ranges around USD 100-200 which makes the treatment less affordable in the developing countries.

Similarly, some countries have a high dropout rate of patients receiving ophthalmic therapeutics due to the unaffordable costs, leading to a lack of improvement in vision. The overall treatment course includes six to eight injections, and the cost of these injections is very high. Due to these factors, patients are dropping out of the treatment course after the first two or three injections.

- For instance, as per data provided by the Indian Journal of Ophthalmology in October 2020, a retrospective study was conducted in India to determine the rate of compliance and the reasons for the loss of follow-up in patients with several ocular conditions. The study result indicated that around 51.0% of patients were lost to follow-up the treatment with Anti-VEGF injection therapy due to high cost.

The lack of awareness regarding various ophthalmic conditions among the general population in the emerging countries such as Mexico, Saudi Arabia, and other African countries, lack of reimbursement policies in these countries are some of the other factors anticipated to restrain the market growth in these countries during the forecast period.

Ophthalmic Disease Therapeutics Market Segmentation Analysis

By Drug Class Analysis

Anti-VEGF is Expected to Grow in the Market Owing to Rising R&D Activities by Market Players

On the basis of drug class, the market is segmented into anti-inflammatory, anti-infectives, anti-VEGF, anti-glaucoma, and others. The anti-glaucoma is further sub-segmented into beta blockers, prostaglandins analogs, alpha adrenergic agonists, carbonic anhydrase inhibitors, combination drugs, and others.

The Anti-inflammatory segment is anticipated to hold a dominant market share of 23.49% in 2026. owing to factors such as increasing patient pool undergoing treatment of ocular allergies and inflammation. Furthermore, increasing regulatory approvals and product launches for the treatment of an extensive range of ocular diseases is responsible for segmental growth.

- For instance, in August 2023, the U.S. FDA approved Lupin’s new drug application for Bromfenac Ophthalmic Solution. This medication is used to treat inflammation in various ocular diseases.

Anti-VEGF segment is expected to register at a significant CAGR during the forecast period. The increasing prevalence of retinal disorders such as diabetic retinopathy, age-related macular degeneration, and others along with rising diagnosis rate of these conditions among the population is resulting in growing demand for anti-VEGF therapy in the regions.

- According to the CDC, there were around 20.0 million Americans with age-related macular degeneration and the global number is projected to reach 288 million by 2040.

Also, the rising number of approvals and launches of the products is contributing to the growth of the segment globally.

- In January 2022, Genentech, Inc., a subsidiary of F. Hoffmann-La Roche Ltd., received the U.S. FDA approval Vabysmo, a vascular endothelial growth factor, for the treatment of wet, or neovascular, age-related macular degeneration and diabetic macular edema.

On the other hand, the rising prevalence of glaucoma along with increasing R&D focus of the market players, collaborations among these players to develop, and introduce anti-glaucoma therapies to cater the rising demand for these among the patient population is expected to fuel the segmental growth in the market.

- In November 2022, Nicox SA, an international ophthalmology company, collaborated with Ocumension Therapeutics for commercialization of NCX 470, a phase III candidate for the lowering of intraocular pressure in patients with open-angle glaucoma, in the U.S. and China.

The growing diagnosis rate of ocular infections and retinal diseases among the population is an important factor responsible for the rising demand for these drugs.

To know how our report can help streamline your business, Speak to Analyst

By Dosage Form Analysis

Semisolid Segment is Projected to Dominate Owing to Increasing Clinical Benefits of the Products

On the basis of dosage form, the market is segmented into liquid, solid, and semisolid. Semisolid segment is expected to grow at a higher CAGR owing to the rising number of approvals and launches of products such as ointment, suspensions, gels, and others, accounting for 79.59% globally in 2026. Rising applications of ointment including inflammatory conditions, infections, and dry eye due its increased effectiveness is leading to rising adoption of the semisolid products. Unlike liquid dosage forms, semisolid ophthalmic drugs have the advantage of a slower rate of drug elimination, thereby extending the corneal residence time through prolonged surface residence. Along with this, increasing focus of the key players to gain approvals and introduce more products is another factor contributing to the growth of the segment.

- In November 2021, I-MED Pharma Inc. launched I-DEFENCE, a night time dry eye ointment in the U.S.

Liquid segment dominated the market in 2023 owing to its increasing adoption among the patient population due to several benefits such as easy to use, increased time period of contact between the product and the substance, increased solubility, and others. The rising prevalence of ophthalmic conditions and increasing patient population undergoing treatment with eye drops, eye solutions, and others is expected to spur the segmental growth.

On the other hand, solid segment is expected to grow in the market owing to the rising focus of the market players to develop innovative products including the oral drugs or various ophthalmic conditions.

- For instance, Eli Lilly and Company has its pipeline candidate, LY3009104, an oral drug for ocular infection uveitis in phase III clinical trial.

Thus, the increasing patient population along with rising diagnosis rate and demand for therapies is leading to rising focus of the players to launch drugs with different routes of administration.

By Disease Indication Analysis

On the basis of disease indication, the market is segmented into glaucoma, dry eye disease, retinal diseases, allergy & infections, and others.

Retinal diseases dominated the market accounting for 33.94% market share in 2026. The rising prevalence of retinal diseases such as diabetic macular edema, macular degeneration and diabetic retinopathy, and others among the population is one of the major factors responsible for the growing patient population. This combined with the increasing number of initiatives for rising awareness about these conditions among the population is resulting in growing diagnosis rate of the conditions and higher demand for therapeutic products.

Dry eye disease segment is expected to grow at a higher CAGR during the forecast period owing to the increasing focus of the key players to develop and introduce drugs for the treatment of the condition.

- According to clinicaltrials.gov, there are around 20 pipeline candidates for dry eye disease in phase III clinical trials.

Glaucoma segment is expected to grow due to the rising prevalence of the condition especially in the geriatric population. Due to the growing patient pool suffering from glaucoma across the globe, several companies are introducing new medications for the treatment of glaucoma. This is one of the major factors anticipated to boost the demand for therapies among the patient population.

- For instance, in September 2023, Thea Pharma introduced Iyuzeh (latanoprost ophthalmic solution) in the U.S. market. This medication is used for the treatment of ocular hypertension and open-angle glaucoma.

- According to a 2021 published by Optometric Physician, the estimated global population with Primary Angle-Closure Glaucoma (PACG) in 2020 is 17.14 million among the population aged 40 years and above. The number is projected to rise to around 26.3 million by 2050.

On the other hand, the adoption of treatment for glaucoma, eye allergies & infections, and others is rising among the patient population. This along with increasing prevalence of these conditions is leading to rising focus of the market players to develop and introduce novel and effective therapies for the treatment.

By Distribution Channel Analysis

On the basis of distribution channel, the market is segmented into hospital pharmacies and retail & online pharmacies.

The retail & online pharmacies segment dominated the market share of 89.97% in 2026 and is expected to register a higher CAGR during the forecast period. The rising number of patient visits to the ophthalmology clinics for the treatment of various ophthalmic is one of the major reasons contributing to the growth of the segment. The increasing number of digital users and increasing preference of the patients to procure medications online in both developed and emerging countries is an important factor contributing to the growth of the segment.

- For instance, according to a 2021 study published by National Center for Biotechnology Information (NCBI), 131 respondents were analyzed for their mode of purchasing medication in the UAE. It was found that 31.2% of respondents purchased medication via the internet after the pandemic.

On the other hand, hospital pharmacies segment is expected to grow owing to increasing inpatient admissions for hospitals. This is leading to a rising number of procurement of the drugs from the hospital pharmacies which is anticipated to propel the segmental growth.

REGIONAL INSIGHTS

North America Ophthalmic Disease Therapeutics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America generated USD 17.39 billion, contributing 43.37% to global market revenue, and is projected to grow to USD 18.48 billion in 2026. The region is anticipated to dominate the market in the upcoming years owing to growing prevalence of various ophthalmic disorders along with higher diagnosis and treatment rate. Moreover, growing healthcare expenditure supporting eye care and eye health in the region, presence of adequate reimbursement for various ophthalmic disorders promotes the adoption of advanced, and novel treatment in the key countries in the region. The U.S. market is projected to reach USD 17.15 billion by 2026.

- According to the American Academy of Ophthalmology (AAO), the U.S. expenditure on eye care comprising direct and indirect cost of treatment for various ophthalmic conditions is around USD 140.00 billion.

Additionally, a conducive environment provided for the research and development of various innovative drugs to cure ophthalmic diseases along with growing approval of new drugs are some other factors contributing to the growth of the market.

- For instance, in February 2021, Akorn Operating Company LLC received the U.S. FDA approval for Loteprednol Etabonate Ophthalmic Gel, 0.5% to treat post-operative inflammation and pain after ocular surgery.

Europe

The Europe market accounted for USD 10.18 billion in 2025, representing 25.40% of the global industry, and is expected to reach USD 10.75 billion in 2026. On the other hand, Europe accounted for the substantial share in the market. Rising launch of biologics and biosimilar intended for the treatment of various eye diseases, rising emphasis on the proper management of ophthalmic conditions, and growing efforts by the key players operating in the market to expand their geographical footprint. The growing burden of eye disorders and launch of new products, among others are some of the few factors primarily contributing to the market growth. The UK market is projected to reach USD 1.59 billion by 2026, while the Germany market is projected to reach USD 2.53 billion by 2026.

- For instance, as per data provided by the NHS England in May 2023, around 130,000 people in the U.K. are suffering from primary angle closure glaucoma.

- In September 2022, F. Hoffmann-La Roche Ltd. received European Commission (EC) approval for faricimab also known as Vabsymo to treat visual impairment owing to diabetic macular edema (DME) and neovascular age-related macular degeneration.

Asia Pacific

Asia Pacific recorded a market size of USD 9.5 billion in 2025, capturing 23.69% of the global market share, and is projected to reach USD 10.23 billion in 2026. Market in Asia Pacific is expected to grow at a comparatively higher CAGR during the forecast period owing to rising prevalence of geriatric population prone to develop various ophthalmic conditions. Growing strategic initiatives by the companies present in the region to increase the penetration of various drugs in the regional market, rising awareness among the patient population regarding new and recent treatments, and others are some factors supporting the market growth. The Japan market is projected to reach USD 4.1 billion by 2026, the China market is projected to reach USD 3 billion by 2026, and the India market is projected to reach USD 0.78 billion by 2026.

- For instance, in May 2022, Visus Therapeutics, Inc., a company focused on developing ophthalmic therapies, collaborated with Zhaoke Ophthalmology Limited to commercialize BRIMOCHOL PF and Carbachol PF in the Greater China, South Korea and select Southeast Asian territories. Both these eye drops are preservative free and are indicated for correction of vision associated with presbyopia.

Latin America

Latin America accounted for USD 1.62 billion in 2025, representing 4.05% of the global market share, and is projected to reach USD 1.7 billion in 2026. Further, Latin America is expected to grow during the forecast period. The rising prevalence of various eye related disorders, the increasing awareness regarding the diseases among the general population, and rising efforts of the key players to introduce new drugs in the region are some of the major factors responsible for the growth of the market in the region.

- In December 2021, according to an article published by BMC Ophthalmology, the prevalence of AMD increases with age, varying from 1.5% to 16.7% in people aged more than 50 years, 15.1% among 60 years aged patients, and 31.5% among 80 years aged patients.

Similarly, improving healthcare infrastructure and growing collaboration and partnerships among the key companies to improve the access of various ophthalmic drugs are a few factors augmenting the market growth of ophthalmic disease therapeutics in Latina America and the Middle East & Africa region.

- In April 2022, Intas and Axantia Ink announced a distribution agreement with an aim to distribute Ranibizumab biosimilar eye drops in several Middle East countries.

Thus, all these factors are expected to augment the growth of the market in these regions.

Middle East & Africa

The Middle East & Africa market generated USD 1.4 billion in 2025, representing 3.48% of the global market landscape, and is expected to reach USD 1.45 billion in 2026.

List of Key Companies in Ophthalmic Disease Therapeutics Market

Regeneron Pharmaceuticals Inc. to Lead the Market with Strong Product Portfolio

This is a consolidated market comprising a few players with a range of products, including prescription products as well OTC products. The increasing sales of the drug EYLEA in the U.S. and other markets is one of the major reasons contributing to the growing ophthalmic disease therapeutics market share of Regeneron Pharmaceuticals Inc. Also, the rising R&D expenditure of the market player for the ophthalmic product is another factor contributing to the higher market share of the company.

- In 2021, Regeneron Pharmaceuticals Inc. increased its R&D expenses for EYLEA by around 41.6% in 2021 as compared to the previous year. The direct R&D expenses for EYLEA in 2021 was around USD 102.2 million and it was USD 72.2 million in 2020.

Santen Pharmaceutical Co. Ltd., is increasing its focus on the approval and introduction of the products globally with strategic mergers and acquisitions. This along with strong emphasis on R&D to develop and launch novel therapies for various ophthalmic conditions to cater to the rising demand from the population is expected to contribute to the company’s market hold.

- In November 2022, Santen Pharmaceutical Co., Ltd., launched DIQUAS LX Ophthalmic Solution 3% in Japan for the treatment of dry eye.

The growing investment of other players in research and development activities for the development of novel drugs and therapies for the condition is resulting into increasing number of pipeline candidates for the treatment of ophthalmic disease. These factors are expected to increase the market share of these companies in the future.

- For instance, Ocuphire Pharma Inc. has its product candidate, APX3330, twice-a-day oral tablet for diabetic retinopathy and diabetic macular edema in Phase II clinical trial.

LIST OF KEY COMPANIES PROFILED:

- Regeneron Pharmaceuticals Inc. (U.S)

- AbbVie Inc. (U.S.)

- Santen Pharmaceutical Co. Ltd. (Japan)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Viatris Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2023 – The U.S. FDA approved Genentech’s ophthalmic drug, Vabysmo, for the treatment of diabetic macular edema.

- September 2022 - Santen Pharmaceutical Co., Ltd. and UBE received approval from the U.S. FDA for Omlonti (omidenepag isopropyl ophthalmic solution) 0.002% eye drops for reduction of elevated IOP in patients with primary open-angle glaucoma or ocular hypertension.

- June 2022 - F. Hoffmann-La Roche Ltd. received authorization for Vabysmo, from Health Canada for the treatment of neovascular (wet) Age-related Macular Degeneration (AMD) and Diabetic Macular Edema (DME).

- March 2022 - Novartis AG received approval from the European commission for Beovu, an ophthalmic medicine for the treatment of visual impairment caused due to diabetic macular edema.

- February 2022 - Viatris Inc. received approval for Cyclosporine Ophthalmic Emulsion 0.05%, the first generic version of Allergan’s Restasis, for the treatment of ocular inflammation.

- December 2021 - AbbVie Inc. received approval from the U.S. FDA for Vuity, a pilocarpine Hcl ophthalmic solution for the treatment of presbyopia.

REPORT COVERAGE

The research report covers a detailed analysis and overview. It focuses on key aspects such as competitive landscape, drug class, dosage form, disease indication, distribution channel, and region. Besides this, it offers insights into the market drivers, market trends, market dynamics, COVID-19 impact on the market, and other key insights. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.70% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Drug Class

|

|

By Dosage Form

|

|

|

By Disease Indication

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 42.61 billion in 2026 and is projected to reach USD 71.58 billion by 2034.

In 2025, the market value stood at USD 40.09 billion.

The market will exhibit steady growth at a CAGR of 6.70% during the forecast period (2026-2034).

Currently, anti-inflammatory segment is leading by drug class. Anti-VEGF segment will lead the market during the forecast period.

Rising prevalence of ophthalmic disease, increasing diagnosis of the condition, increasing research and development activities by the major market players, and rising number of approvals and launches of ophthalmic disease therapeutics products are the key drivers of the market.

Regeneron Pharmaceutical Inc., AbbVie Inc., Santen Pharmaceutical Co. Ltd., and Novartis AG are the major players in the market.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us