Prothrombin Complex Concentrate (PCC) Market Size, Share & COVID-19 Impact Analysis, By Product (3-factor PCC and 4-factor PCC), By Application (Acquired Coagulation Factor Deficiency and Congenital Coagulation Factor Deficiency), By End User (Hospitals & Ambulatory Surgical Centers, Specialty Clinics and Others), and Regional Forecast, 2026-2034

Prothrombin Complex Concentrate PCC Market Size and Industry Overview

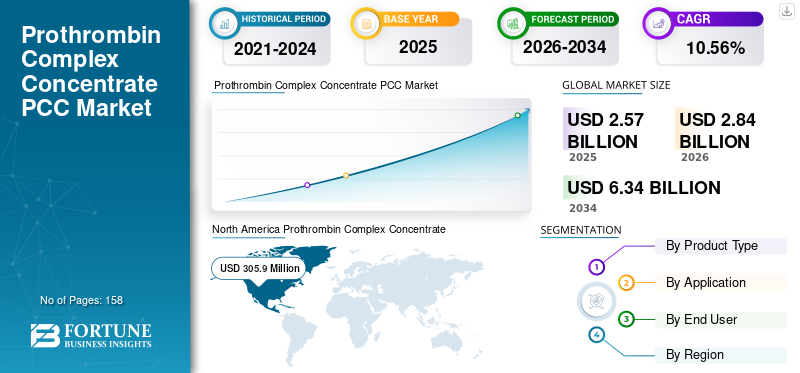

The global prothrombin complex concentrate market size was valued at USD 2.57 billion in 2025. The market is projected to grow from USD 2.84 billion in 2026 to USD 6.34 billion by 2034, exhibiting a CAGR of 10.56% during the forecast period. North America dominated the prothrombin complex concentrate market with a market share of 44.% in 2025.

Prothrombin complex concentrate is a treatment comprising blood clotting factors II, IX, and X. Also known as factor IX complex; it is extensively used when excessive bleeding requires emergency anticoagulation reversal. Increasing prescription of anticoagulants, especially warfarin, as well as the rising prevalence of bleeding disorders, is expected to augment the market. Additionally, PCC offers various advantages over Fresh-frozen plasma and others, making it a more suitable option for life-threatening conditions. According to the World Federation of Hemophilia, 68,703,141 I.U. of plasma-derived Factor IX were used in 2018 in Europe. Thus, increasing usage of factor IX complex is likely to favor the growth of this market during the forecast period. Apart from this, active government support for using 4-factor PCC products such as Kcentra and positive recommendations are anticipated to provide considerable momentum to the market.

The COVID-19 pandemic has resulted in a sudden increase in the demand for blood and plasma products. Major PCC manufacturers have reported changes in the buying patterns of plasma-derived products, which favors the growth of the prothrombin complex concentrate market. Furthermore, pharmaceutical giants such as Grifols and CSL are witnessing an increase in segmental revenue owing to increased productivity from plasma centers and the double-digit growth of Kcentra. This is expected to have a positive impact on the overall market.

Download Free sample to learn more about this report.

Prothrombin Complex Concentrate (PCC) Market Takeaways

- 2025 Market Size: USD 2.57 billion

- 2026 Market Size: USD 2.84 billion

- 2034 Forecast Market Size: USD 6.34 billion

- CAGR: 10.56% from 2026–2034

- North America dominated the prothrombin complex concentrate market with a 44.0% share in 2025.

- 4-factor PCC was the leading product segment, generating USD 945.2 million in revenue by 2025.

- Hospitals & ASCs accounted for the largest end-user share at 74.2% in 2025.

North America

The regional market was valued at USD 305.9 million in 2025, supported by high adoption of PCC therapies and advanced healthcare infrastructure.

Europe

The market is anticipated to grow at a 10.5% CAGR during the forecast period, driven by increasing treatment adoption for bleeding disorders.

Asia Pacific

The region is expected to witness remarkable growth due to rising warfarin prescriptions, increasing Kcentra usage, and improving access to essential therapies in China.

U.S.

Approximately 29,000 warfarin-associated bleeding cases are reported annually in emergency departments, supporting strong demand for prothrombin complex concentrates.

Japan

The prothrombin complex concentrate market is expected to reach USD 40.6 million by 2025, driven by growing Kcentra prescriptions and increasing demand for bleeding disorder therapies.

Read More

Prothrombin Complex Concentrate Market TRENDS

Download Free sample to learn more about this report.

Significant Investment to Acquire Plasma Centers to Boost the Market

One of the important market trends is the increased focus on expanding the network of plasma centers. Increasing uptake of PCC has resulted in the adoption of different methods to improve the manufacturing of these products. This paved the way for major players' acquisition of domestic companies to benefit from their plasma centers and enhance manufacturing capacity. In January 2019, Grifols S.A. acquired the U.S. branch of Biotest Pharmaceuticals Corporation. As a result of this acquisition, Grifols S.A. will likely gain access to Biotest’s plasma collection centers and increase its supply of plasma proteins for therapeutic purposes. A significant increase in the manufacturing and supply of factor IX complex, especially during the COVID-19 pandemic when hospitals are making bulk purchases of essential medicines, is expected to boost this market significantly.

DRIVING FACTORS

Rapid Uptake of Vitamin K Antagonists to Drive the Market

The introduction of various Vitamin K antagonist products, especially warfarin, is poised to increase PCC use. The use of warfarin as an anticoagulant is relatively widespread, resulting in an increasing number of prescriptions for warfarin. According to the National Action Plan for Drug Event Presentation, more than 30 million prescriptions are written for warfarin annually. However, this medicine is associated with adverse drug events, requiring urgent reversal, for which prothrombin complex concentrate is the most preferred therapy owing to its fast action and minimal risk of viral transmission. Thus, increasing warfarin prescription is estimated to fuel the PCC market growth during the forecast period.

Furthermore, positive government recommendations and guidelines for using factor IX complex during urgent warfarin reversal are also anticipated to favor the market.

Advantages of PCC over Other Anticoagulation Reversal Therapies to Foster Market Growth

When compared to other alternative anticoagulation-reversal therapies such as FFP (Fresh Frozen Plasma), Vitamin K1, and others, they have more advantages, which is responsible for its widespread use in urgent warfarin-reversals. One of the major advantages of PCC is that it eliminates the need for blood matching and thawing, which is required in the case of FFP, thus reducing the total time of administration. Moreover, it offers shorter penetration time, higher efficiency, and is required in less volume. Also, it has minimal risk of viral or pathogen transmission. All these advantages have resulted in increasing preference for the product, which is likely to contribute to the expansion of the market.

RESTRAINING FACTORS

Risk of Thrombotic Complications Associated with PCC to Hinder Market Growth

One of the key factors restricting prothrombin concentrate complex market growth is the thrombotic complications resulting from the use of PCC. The blood clots may result in complications such as venous thromboembolism, microvascular thrombosis, disseminated intravascular coagulation (DIC), and myocardial infarction. According to a market study on “Thromboembolic Events after Vitamin K Antagonist Reversal with 4-Factor Prothrombin Complex Concentrate”, the percentage of patients with thromboembolic events post 4-factor-PCC administration was 7.3%. Furthermore, according to the UPMC System Pharmacy and Therapeutics Committee Formulary Review, the thromboembolic events reported after the use of Kcentra was 2.9%. This raises a safety concern with the use of factor IX complex products, which is expected to hinder the progress of the market.

SEGMENTATION Analysis

By Product Type Analysis

To know how our report can help streamline your business, Speak to Analyst

4-factor PCC to Generate Maximum Revenue

Based on product type, the market segments include 3-factor PCC and 4-factor PCC. The 4-factor segment accounted for the maximum PCC market share in 2026. Improved penetration of 4-factor PCC brands such as Kcentra & Beriplex in emerging countries and their clinically proven efficacy for urgent warfarin reversal are the primary factors attributable to the dominant share of the segment. Additionally, active government support to decrease the warfarin-associated adverse events is likely to boost the segment. The 3-factor segment is poised to surge owing to the rising prevalence of hemophilia and increasing demand for Profilnine SD and Bebulin.

- By product type, the 4-factor PCC segment is projected to generate USD 945.2 million in revenue by 2025.

Furthermore, the increasing demand for plasma products by hospitals during the coronavirus pandemic is expected to augment the segment.

By Application Analysis

Increasing Cases of Warfarin-associated Bleeding to Augment the Acquired Coagulation Factor Deficiency Segment

On the basis of application, the market is segmented into acquired coagulation factor deficiency and congenital coagulation factor deficiency. The acquired coagulation factor deficiency segment generated the maximum revenue in 2026 and is projected to witness remarkable growth during the forecast period. Increasing cases of life-threatening bleeding associated with the use of warfarin, rising incidence of induced coagulation factor deficiency during surgical procedures, and new product launches are expected to fuel the segment. According to the Hemophilia Federation of America, the emergency departments in the U.S. witness approximately 29,000 cases of warfarin-associated bleeding per year. This is projected to augment the growth of this segment by the end of 2034. Moreover, the segment is expected to gain significant momentum owing to the increasing sales of Kcentra amid the COVID-19 crisis. On the other hand, active government measures to bring innovative therapies for the treatment of bleeding disorders such as Hemophilia B is likely to favor the congenital coagulation factor deficiency segment.

By End User Analysis

Hospitals & ASCs Segment to Dominate the Market

In terms of end user, the market is divided into hospitals & ambulatory surgical centers, specialty clinics, and others. The hospitals and ambulatory surgery segment is estimated to dominate the market throughout the forecast period owing to the increasing preference for prothrombin complex concentrate, positive government recommendations, and increased purchase of plasma products in hospitals owing to the COVID-19 pandemic. The specialty clinics segment is anticipated to grow on account of the increasing number of surgeons and the rising number of privately owned clinics. The others segment, which consists of urgent care centers, emergency trauma centers, physicians’ offices, etc., is likely to propel owing to the rising investment by government and private players for the betterment of healthcare facilities.

- By end user, the hospitals & ASCs segment is expected to hold a 74.2% share in 2025.

REGIONAL Analysis

North America Prothrombin Complex Concentrate (PCC) Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

The market size in North America stood at USD 305.9 million in 2025. The strategic presence of major manufacturers, the green signal from the USFDA for 4-factor PCC, and the increasing sales of Kcentra are key factors attributable to the dominant share of North America. According to the World Federation of Hemophilia, Canada bought 3,728,656 I. U of factor IX in 2018. This is expected to boost the market in North America.

Europe

In Europe, the market is likely to grow owing to the increasing off-label use of 4-factor PCC, such as Cofact & Octaplex, rapid adoption of activated PCC, and favorable health reimbursement. Grifols S.A.'s increased focus on increasing the production and supply of plasma-derived products by continuing the operations of plasma centers in Europe during the COVID-19 crisis is expected to favor the European market.

- Europe is anticipated to grow at a CAGR of 10.5% during the forecast period.

Asia Pacific

Asia Pacific is anticipated to witness remarkable growth owing to the rising prescription rate of warfarin and the increasing number of patients for Kcentra, especially in Japan. Also, active measures by the government to improve the affordability of essential therapies in China are poised to surge the prothrombin complex concentrate market in Asia Pacific.

- The prothrombin complex concentrate market in Japan is expected to reach USD 40.6 million by 2025.

- China is projected to witness a strong CAGR of 11.60% during the forecast period.

Middle East, Africa, and Latin America

The market is estimated to expand in the Middle East, Africa, and Latin America owing to the rising prevalence of bleeding disorders, strengthening of the distribution network in these regions, and improving healthcare spending.

KEY INDUSTRY PLAYERS

CSL Behring and Takeda to Lead the Market

In terms of revenue, CSL Behring accounted for maximum market share owing to the higher sales of Kcentra. In November 2017, CSL Behring announced the launch of Kcentra in Japan, and the number of patients using Kcentra increased to around 2,800 in 2019. This is expected to further strengthen the market position of CSL Behring. Takeda is considered to be the second prominent player in the market primarily due to the strong sales force, expanding distribution network, and increasing focus of rare hematology.

LIST OF KEY COMPANIES PROFILED:

- Grifols, S.A. (Spain)

- CSL Behring (U.S.)

- Octopharma AG (Switzerland)

- Sanquin (Netherlands)

- Kedrion S.p.A (Italy)

- China Biologic Products Holdings, Inc. (China)

- Takeda Pharmaceutical Company Limited (Japan)

- Others

KEY INDUSTRY DEVELOPMENTS:

- Grifols S.A. entered into a strategic agreement to control 26.2 % share of Shanghai RAAS in exchange for non-minority share in Grifols Diagnostic Solutions. This alliance will help Grifols boost its plasma derived products in the Chinese market.

- Grifols S.A. acquired the US branch of Biotest Pharmaceuticals Corporation in order to enhance its presence in North America. As a result of this acquisition, Grifols is likely to gain the access of Biotest’s plasma collection centers, in order to increase the supply of plasma proteins to be used for therapeutic purposes.

- CSL Behring announced the launch of Kcentra in Japan.

REPORT COVERAGE

The prothrombin complex concentrate market report offers a detailed analysis of numerous economic factors and other factors affecting the market. These include growth drivers, threats, opportunities, restraints, and key developments. Apart from this, the report further helps analyze, segment, and define the market based on different segments such as product type, application, and end user. It also provides various key insights such as the prevalence of coagulation factor deficiency for key countries, regulator scenario for key countries, analysis with alternatives to PCC, reimbursement scenarios for key countries, key mergers & acquisition, and others.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD million) |

|

|

By Product Type

|

|

By Application

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

The value of the global prothrombin complex concentrate market was at USD 2.57 billion in 2025.

Fortune Business Insights says that the market is projected to reach USD 6.34 billion by 2034.

The value of the market in North America was USD 305.9 million in 2025.

The market is projected to rise at a CAGR of 10.56% during the forecast period (2026-2034).

4-factor is the leading segment in this market.

Rapid uptake of Vitamin K antagonists and advantages of PCC over other anticoagulation reversal therapies are the key factors driving the market.

CSL Behring and Takeda Pharmaceuticals Company Limited are the top players in the market.

North America is expected to hold the highest market share.

Significant Investment to acquire plasma centers is the key trend of the market.

- 2021-2034

- 2025

- 2021-2024

- 158

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us