Inhaled Biologics Market Size, Share & Industry Analysis, By Drug Class (Anti-IgE agents, Anti-IL-5 agents, Anti-IL-5 receptor agents, Anti-IL-4/IL-13 pathway agents, Anti-IL-4/IL-13 pathway agents, Anti-TSLP agents, Anti-IL-33 agents, & Others), By Disease Indication (Asthma, COPD, Allergic Rhinitis/Upper Airway Allergy, Chronic Rhinosinusitis, Respiratory Viral Infections, & Others), By Device Type (Intranasal Spray/Drops, Dry Powder Inhaler, Metered Dose Inhaler (MDI / pMDI), & Others), By Age Group (Pediatric and Adults), By Distribution Channel, and Regional Forecast, 2026-2034

Inhaled Biologics Market Size and Future Outlook

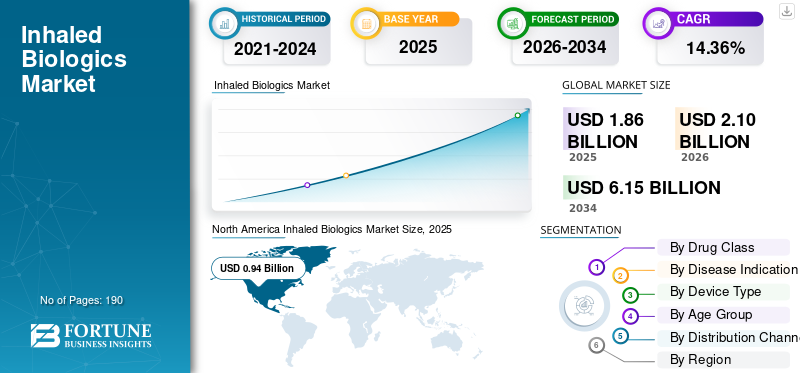

The global inhaled biologics market size was valued at USD 1.86 billion in 2025. The market is projected to grow from USD 2.10 billion in 2026 to USD 6.15 billion by 2034, exhibiting a CAGR of 14.36% during the forecast period. North America dominated the inhaled biologics market with a market share of 50.53% in 2025.

The global market is anticipated to grow exponentially in the coming years due to increasing respiratory disorders. As drug developers develop large-molecule therapies for lung diseases, the global demand for inhaled biologics also increases. Increasing use of these inhalation devices, such as nebulizers and dry powder inhalers, can potentially achieve higher concentrations at the site of airway or lung pathology, resulting in improved effectiveness. It enables faster and localized responses and assists in overcoming challenges related to drug stability, dose consistency, and drug–device combination requirements.

Furthermore, innovative techniques and inhaled biologics technologies that deliver more sensitive results drive market growth.

- For instance, in January 2025, Iconovo AB collaborated with Lonza to develop spray-dried formulations of an intranasal biologic for Iconovo's proprietary intranasal device, ICOone Nasal.

Leading players in the industry, such as F. Hoffmann-La Roche Ltd, Inhalon Biopharma, Inc., Shanghai Novamab Biopharmaceuticals Co., Ltd., and Aridis Pharmaceuticals, Inc., are directing their resources toward research and development, expanding their offerings, and strengthening their market positions.

Download Free sample to learn more about this report.

INHALED BIOLOGICS MARKET TRENDS

Shift Toward High-Payload Dry Powder Inhalers (DPI) Platforms is a Significant Market Trend

The prominent market trend observed is the growing adoption of high payload DPI inhalers. Biologics typically require higher delivered doses than traditional inhaled small-molecule drugs, and patients are less likely to adopt products that require frequent inhalations or long administration times. When dry powder inhaler engines reliably produce more powder per use with consistent lung deposition, developers move from feasibility programs to patient-friendly dosing that fits home use and chronic therapy routines. This reduces the need for nebulization in certain use cases, lowers treatment burden, and improves the commercial case for inhaled biologics by supporting improved adherence and increasing prescriber confidence.

Underscoring these advantages, many key companies are increasingly investing in inhaled biologics and participating in strategic collaborations.

- For instance, in November 2024, Aptar Pharma announced an exclusive collaboration agreement with Cambridge Healthcare Innovations (CHI) to commercialize and promote the Quattrii DPI platform, which is positioned to enable the delivery of large volumes of biologic molecules via dry powder inhalation.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Burden of Chronic Respiratory Diseases Drive demand for Targeted Therapies

One of the significant factors driving the market growth is the increased rates of chronic respiratory diseases. Patients and clinicians increasingly need targeted therapies that act directly in the lungs rather than systemic treatments. As conditions become more persistent and difficult to manage, delivering a biologic by inhalation increases drug concentration at the disease site while potentially reducing whole-body exposure—these advantages support a better benefit-to-risk profile. The local delivery approach can also improve symptom control and reduce complications for select long-duration respiratory conditions.

Recognizing these advantages, vendors are intensifying research and development efforts to expand inhaled biologic production and address significant gaps in chronic disease treatment.

- For instance, in June 2024, Savara announced that molgramostim (an inhaled GM-CSF) met statistical significance on the primary endpoint and multiple secondary endpoints in its pivotal Phase 3 IMPALA-2 trial in autoimmune pulmonary alveolar proteinosis (aPAP), reinforcing momentum for inhaled biologics in the treatment of chronic/rare respiratory diseases.

MARKET RESTRAINTS

Complex Drug–Device Combination Development is Increasing Costs and Hampering Market Growth

A key restraint for the global inhaled biologics market growth is the high complexity of developing biologics as drug–device combinations. Product success depends not only on the molecule, but also on the delivery device and its performance. Since biologics are sensitive, companies must prove consistent aerosol generation, reliable lung deposition, and stable product quality across real-world use conditions. When regulators demand additional device performance data or clarifications, programs can face clinical holds, delayed enrollment, increased CMC burden, and higher development costs, which slow time-to-market and reduce near-term adoption. As a result, inhaled biologics can progress slower than expected, thereby limiting the pace of market growth.

- For instance, in November 2025, BiomX reported that the U.S. FDA placed a clinical hold on the U.S. portion of its BX004 Phase 2b trial while the agency reviewed information related to the third-party nebulizer device used for administration—highlighting how device/CMC requirements can delay inhaled biologic development and hamper the market's growth potential.

MARKET OPPORTUNITIES

New Stabilization and Particle-Engineering Technologies to Improve Shelf Life and Offer Lucrative Opportunity

Increasing research and development for new stabilization and particle-engineering technologies offers a significant growth opportunity. These developments address one of the biggest blockers for inhaled biologics, including loss of activity when formulated into an aerosol and during storage. When companies are enabled with particles that stay stable, disperse consistently, and protect the molecule from moisture and mechanical stress, they can extend shelf life, improve dose reliability, and reduce batch failures. This directly lowers CMC risk and makes it easier to scale programs from clinical to commercial supply. Enhanced stability also reduces reliance on stringent cold-chain logistics, thereby facilitating wider access and enabling broader global distribution.

- For instance, in March 2024, Lonza announced it expanded its spray-dried biologics service offering for pulmonary delivery, positioning shelf-stable dry powder inhalers to improve access by reducing reliance on cold-chain logistics—a direct example of stabilization/particle-engineering enabling inhaled biologics.

MARKET CHALLENGES

High Formulation and Stability Challenges for Biologics during Aerosolization and Storage to Obstruct Market Growth

Formulation and stability challenges pose a significant hindrance to the market because biologics are highly sensitive to stress during manufacturing, aerosolization, and storage. When a biologic is converted into an inhalable form, it can aggregate, lose potency, or exhibit inconsistent aerosol performance, making it harder to deliver a reliable dose to the lungs consistently. This forces companies to increase the frequency of analytical testing, undertake stability studies, and implement stricter device formulation controls, thereby increasing development costs and extending project timelines. Consequently these factors limit the market's scaling potential.

- For instance, in May 2025, Savara announced it received an FDA Refusal to File (RTF) letter for the BLA of MOLBREEVI (molgramostim inhalation solution), with the FDA requesting additional Chemistry, Manufacturing, and Controls (CMC) data—a clear example of how formulation/CMC requirements can slow inhaled biologics commercialization.

Segmentation Analysis

By Drug Class

Others Segment Holds the Largest Share Supported by New Product Launches

Based on drug class, the market is categorized into Anti-IgE agents, Anti-IL-5 agents, Anti-IL-5 receptor agents, Anti-IL-4/IL-13 pathway agents, Anti-TSLP agents, Anti-IL-33 agents, Anti-GM-CSF agents, Anti-TNF agents, Cytokine/Chemokine pathway inhibitors, and others.

Among these, the others segment accounted for the largest inhaled biologics market share in 2025. Others segment comprises inhaled enzymes and microbial peptides, which are not limited to cytokine-pathway antibodies but also include non-cytokine large molecules, for which inhaled delivery already has proven demand. When these products have existing prescriptions, distribution pathways, and patient familiarity, they generate recurring revenue and early adoption that are still scaling clinically. Furthermore, as research and development increase, key companies are directing their resources toward new product launches and the subsequent regulatory approvals that align with inhaled biologics workflows.

- For instance, in January 2026, MannKind Corporation received approval from the U.S. FDA for the Afrezza (insulin human) inhalation powder label, supporting broader use and reinforcing the ongoing commercial contribution of other innovative inhaled biologics.

The Anti-IL-33 agents segment is expected to grow at a CAGR of 19.64% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Increasing Patient Pool for Asthma to Lead Segmental Growth

Based on disease indication, the market is segmented into asthma, COPD, allergic rhinitis/upper airway allergy, chronic rhinosinusitis, respiratory viral infections, cystic fibrosis, bronchiectasis/chronic airway infection, pulmonary fibrosis/ILDs, and others.

In 2025, asthma accounted for the largest share of the market by disease indication due to a large diagnosed population and a well-defined pathway for stepping up therapy when patients remain uncontrolled on standard inhalers. In chronic and common conditions such as asthma, key companies invest in developing specialized inhaled biologics due to their commercial upside. This drives more pipeline concentration and earlier adoption potential in asthma. Over time, the larger number of asthma candidates progressing through trials increases the likelihood of approvals and reinforces asthma's share of leadership.

Additionally, as the population grows, key companies are expanding their pipelines of inhaled biologics to offer better patient care and innovative solutions.

- For instance, in February 2021, Amgen, in collaboration with AstraZeneca, showcased positive results from the pivotal NAVIGATOR Phase 3 trial, which showed the potential of tezepelumab as a first-in-class medicine for severe asthma.

The respiratory viral infections segment is projected to grow at a CAGR of 19.93% during the forecast period.

By Device Type

Increasing Use and Easy Delivery of Intranasal Spray/ Drops to Fuel the Segmental Growth

Based on device type, the market is segmented into Intranasal SPRAY/DROPS, Dry Powder Inhaler (DPI), Metered Dose Inhaler (MDI/pMDI), Nebulized/Aerosolized Delivery, Soft Mist Inhaler (SMI), and others.

Intranasal spray/drops dominated the market in 2025 as they offer a simple, rapid, and needle-free administration, with devices that facilitate outpatient and community use. Such facilitated use and targeted delivery is easy and does not require a long administration session. These advantages reduce barriers to uptake and enable broader distribution through routine healthcare touchpoints. As a result, intranasal formats can capture higher volumes earlier than more technically demanding lung-deposition devices for large molecules. Additionally, new product launches by key players to expand nasal spray/ drops reinforce the segment's dominance.

- For instance, in September 2022, Bharat Biotech announced iNCOVACC (BBV154), an intranasal vaccine, which received emergency-use approval in India, reinforcing commercial momentum for intranasal biologic delivery formats in devices.

In addition, soft mist inhaler (SMI) is projected to grow at a CAGR of 16.62% during the study period.

By Age Group

Adults Age Group Dominates as they are prioritized for Initial Development of Inhaled Biologics

Based on age group, the market is segmented into pediatric and adult.

In 2025, the adult segment dominated the market based on age group. Most inhaled biologics are initially developed and validated in adult populations, where diagnostic pathways are standardized, and safety monitoring is more defined and well-structured. Prioritizing adults in pivotal studies and real-world adoption accelerates confidence- building among payers and clinicians, leading to faster utilization relative to pediatrics. Owing to these factors, adult patients account for the larger share until pediatric labels and routine prescribing expand. Underscoring these advantages, many key companies are also focusing on research and development for cancer diagnostics and treatment.

- For instance, in January 2023, Aridis Pharmaceuticals, Inc. showcased top-line results from the AR-301-002 Phase 3 study, which evaluated the superiority of adjunctive use of the investigational monoclonal antibody candidate AR-301 with standard of care (SOC) antibiotics versus SOC antibiotics alone, for the treatment of VAP caused by Gram-positive bacteria Staphylococcus aureus in adults.

In addition, the pediatric segment is projected to grow at a CAGR of 15.88% during the study period.

By Distribution Channel

Vast Distribution Network of Drug Stores and Retail Pharmacies Makes it the Leading Distribution Channel

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

The drug stores & retail pharmacies dominate the market by distribution channel as most inhaled therapies are used and refilled in these settings. It also provides vast access through its distribution networks. As inhaled biologics gain approvals, the ability to move through retail channels becomes a key driver of facilitating uptake. Strategic collaboration among these operating entities and retail pharmacies to advance distribution is projected to drive the segment's growth.

- For instance, in December 2024, Cipla received regulatory approval for the exclusive distribution and marketing of Afrezza (insulin human) inhalation powder in India, demonstrating how retail-focused distribution partnerships help scale inhaled biologics beyond hospital settings.

The online pharmacies segment is projected to grow at a CAGR of 19.14% over the study period.

Inhaled Biologics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Inhaled Biologics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, at USD 0.84 billion, and maintained its leading position in 2025 with USD 0.94 billion. North America is expected to grow significantly over the forecast period, driven by strong biologics R&D funding and a large base of asthma/COPD and rare lung disease patients in the region. Additionally, higher adoption of home-based care further supports uptake.

U.S. Inhaled Biologics Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 0.97 billion in 2026, accounting for roughly 46.22% of the global market.

Europe

Europe is projected to grow at 12.43 % over the coming years, the second-highest among all regions, and reach a valuation of USD 0.50 billion in 2026. The area is expected to experience robust growth driven by substantial public research funding and large multi-center biomedical programs.

U.K. Inhaled Biologics Market

The U.K. market is estimated at around USD 0.10 billion in 2026, representing roughly 4.85% of the global market.

Germany Inhaled Biologics Market

Germany is projected to reach approximately USD 0.12 billion in 2026, equivalent to around 5.66% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.46 billion in 2026 and secure the position of the third-largest region. The area is witnessing rising respiratory disease burden, increased exposure to urban air pollution, and expanding diagnostic rates, which are driving demand for advanced therapies.

Japan Inhaled Biologics Market

Japan is estimated to reach at around USD 0.08 billion by 2026, accounting for approximately 3.70% of the global market.

China Inhaled Biologics Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.15 billion, representing approximately 7.30% of global sales.

India Inhaled Biologics Market

The market in India in 2026 is estimated at around USD 0.06 billion, accounting for roughly 2.70% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa are expected to witness moderate growth during the forecast period. Latin America is set to reach a valuation of USD 0.07 billion in 2026. The region’s market growth is driven by rising investments in healthcare infrastructure and specialty pharmacy networks. In the Middle East & Africa, the GCC is set to reach USD 0.01 billion in 2026.

South Africa Inhaled Biologics Market

South Africa is projected to reach approximately USD 0.002 billion in 2026, accounting for roughly 0.10% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Increased Focus on Pipeline Expansion by Key Players Propel Market Progress

The global market is highly consolidated, with companies such as F. Hoffmann-La Roche Ltd., Inhalon Biopharma, Inc., Shanghai Novamab Biopharmaceuticals Co., Ltd., and Aridis Pharmaceuticals, Inc. holding significant market share. Strategic partnerships, expanding pipelines, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in February 2025, Inhalon Biopharma, Inc. completed its IND-enabling studies for its Respiratory Syncytial Virus (RSV) candidate, IN-002, and plans to advance its inhaled-antibody therapy into a human challenge study in 2026.

Other notable players in the global market include AptarGroup, Inc., Cambridge Healthcare Innovations, and Resyca B.V. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions.

LIST OF KEY INHALED BIOLOGICS COMPANIES PROFILED

- Hoffmann-La Roche Ltd (Switzerland)

- Inhalon Biopharma, Inc. (U.S.)

- Shanghai Novamab Biopharmaceuticals Co., Ltd (China)

- Aridis Pharmaceuticals, Inc. (U.S.)

- AptarGroup, Inc. (U.S.)

- Cambridge Healthcare Innovations (U.K.)

- Resyca B.V. (Netherlands)

- Inaedis (U.S.)

- Nanopharm Limited (U.K.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Synairgen Research Limited partnered with Aerogen Ltd. to develop and deliver a custom aerosol device for Synairgen's investigational therapy, SNG001 (inhaled interferon-beta). The collaboration brought together Aerogen's aerosol platform and manufacturing expertise with Synairgen's drug development programme, providing targeted respiratory treatment for patients with severe viral infections.

- October 2025: MannKind Corporation received approval for its supplemental biologics license application (sBLA) from the U.S. FDA for Afrezza (insulin human) Inhalation Powder in children and adolescents living with type 1 or type 2 diabetes.

- September 2025: AstraZeneca launched AstraZeneca Direct, an online platform designed to create a simple, convenient way for eligible patients to access their prescribed medications at a transparent cash price with home delivery. AstraZeneca Direct supports people living with chronic conditions such as asthma, diabetes, heart failure, and chronic kidney disease, and people seeking flu protection.

- August 2025: Shilpa Medicare collaborated with Alveolus Bio to accelerate the development of inhaled microbiome therapeutics for lung disease. The partnership accelerated the growth of Alveolus Bio's live biotherapeutics platform toward Phase 2 trials and redefining treatment for COPD and other chronic lung diseases.

- May 2025: AstraZeneca received approval in the U.K. for Trixeo Aerosphere (budesonide/glycopyrronium/formoterol fumarate or BGF), indicated for the treatment of chronic obstructive pulmonary disease (COPD) in adults.

- March 2023: Stevanato Group S.p.A., a provider of drug containment, drug delivery, and diagnostic solutions, collaborated with Resyca BV to support the development and production of pre-fillable syringes for use in Resyca's soft mist inhalers.

REPORT COVERAGE

The global inhaled biologics market analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including pipeline analysis, new product launches, and the regulatory landscape. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape, including market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.36% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Device Type, Age Group, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Device Type |

|

| By Age Group |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.86 billion in 2025 and is projected to reach USD 6.15 billion by 2034.

In 2025, North Americas market value stood at USD 0.94 billion.

The market is expected to grow at a CAGR of 14.36% over the forecast period of 2026-2034.

By drug class, the others segment is expected to lead the market.

Rising burden of chronic respiratory diseases drive demand for targeted therapies drive market growth.

F. Hoffmann-La Roche Ltd, Inhalon Biopharma, Inc., Shanghai Novamab Biopharmaceuticals Co., Ltd, Aridis Pharmaceuticals, Inc., and AptarGroup, Inc. are the major market players in the global market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us