Injection Pen Market Size, Share & Industry Analysis By Type (Conventional and Smart), By Usage (Disposable and Reusable), By Application (Diabetes, Autoimmune Diseases, Hormonal Diseases, and Others), By End User (Hospitals & ASCs, Specialty Clinics, Homecare Settings, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

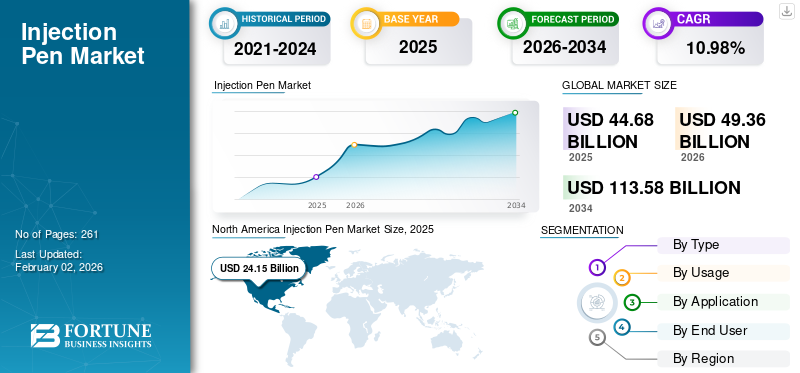

The global injection pen market size was valued at USD 44.68 billion in 2025. The market is projected to grow from USD 49.36 billion in 2026 to USD 113.58 billion by 2034, exhibiting a CAGR of 10.98% during the forecast period. North America dominated the injection pen market with a market share of 54.06% in 2025.

Injection pen refers to a device designed to deliver injectable medications under the skin to a patient population. The rising prevalence of chronic diseases such as diabetes, autoimmune diseases, and others is resulting in a growing demand for drug delivery devices such as injector pens. The growing number of patients and the technological advancements, such as Bluetooth connectivity and others, are further boosting the demand for these products, thereby contributing to their adoption rate.

- For instance, according to 2025 data published by the International Diabetes Federation (IDF), about 589 million adults have diabetes globally.

Moreover, the increasing aging population and favorable reimbursement policies, especially in developed regions, are some of the additional factors contributing to the growing demand for these devices. This, coupled with increasing R&D activities among prominent players, such as Eli Lilly and Company, Novo Nordisk A/S, and others, is anticipated to contribute to the global market growth.

Download Free sample to learn more about this report.

Injection Pen Market Key Takeaways

- 2025 Market Size: USD 44.68 billion

- 2026 Market Size: USD 49.36 billion

- 2034 Forecast Market Size: USD 113.58 billion

- CAGR: 10.98% from 2026–2034

- North America dominated the injection pen market with a market share of 54.06% in 2025.

- The conventional segment is projected to dominate the market with a share of 94.39% in 2026.

- The disposable segment is expected to account for 87.90% of the market in 2026.

North America

North America generated USD 24.15 billion in 2025 and is expected to reach USD 26.73 billion in 2026, supported by strong healthcare infrastructure and growing demand for medication delivery devices.

Europe

Europe accounted for USD 11.52 billion in 2025 and is projected to reach USD 12.73 billion in 2026, driven by expanding healthcare investments and rising adoption of injectable therapies.

Asia Pacific

Asia Pacific stood at USD 5.85 billion in 2025 and is expected to grow to USD 6.45 billion in 2026, supported by improving healthcare access and increasing chronic disease prevalence.

U.S.

The market reached an estimated value of USD 24.44 billion in 2026, driven by the high prevalence of chronic diseases and strong adoption of advanced injection technologies.

Japan

The market is expected to witness steady growth during the forecast period, supported by an aging population, increasing healthcare expenditure, and rising demand for self-administration drug delivery solutions.

Read More

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Conditions to Drive Market Growth

The surging prevalence of chronic conditions, such as autoimmune disorders, hormonal diseases, and others, is resulting in rising admission of patients who require accurate, frequent, and lifelong injections. This is subsequently driving the adoption rate of these devices.

- For instance, according to 2022 data published by Pfizer Inc., about 1.5 million people were reported to have rheumatoid arthritis in the U.S.

Moreover, the increasing geriatric population is a vital factor supporting the growing patient pool, further boosting the demand for these devices globally. This, along with the soaring focus of key players on research and development activities to launch innovative prefilled GLP-1 and insulin injections, is likely to support its adoption rate.

Therefore, the factors above, along with the growing focus of major companies on R&D activities to launch novel devices, are expected to boost the adoption rate, thereby supporting the global injection pen market growth. The rising adoption of biologics and biosimilars administered via pen injectors is further anticipated to propel industry expansion.

Market Restraints

High Cost Associated with Advanced Devices to Hamper the Market Growth

There is a growing demand for these medication delivery systems due to their advantages, including accuracy, accessibility, and self-injectability, among others. However, the high cost associated with technologically advanced devices is anticipated to hamper the adoption rate of these devices, especially in developing nations such as Mexico, South Africa, India, and others.

The integration of smart features such as Bluetooth connectivity, reusable cartridges, and dose tracking, and premium materials in these advanced devices is resulting in their increasing costs, further limiting the adoption rate of these products.

- For instance, according to 2025 data published by The diaTribe Foundation, it was reported that the price of the InPen smart insulin pen system costs about USD 549.0.

Furthermore, limited awareness, inadequate reimbursement policies, pricing barriers, and other factors further delay the market penetration of advanced devices, especially in emerging countries. The increasing cost of these products further increases therapy costs among patients, particularly among patients who require life-long injections.

Therefore, inadequate reimbursement policies, increasing costs, among others, are some of the vital factors anticipated to hinder market growth.

Market Opportunities

Technological Advancements in these Products to Create Lucrative Opportunities

There is a growing emphasis on incorporating technological advancements into these products in the injection pen industry. The surging preferential shift toward home care-based treatment therapies among patients is spurring research and development activities to develop novel devices. The technological advancements, including smart injection pens that integrate with EHRs, track patient history, and others, are expanding accessibility and penetration rates for these devices among the patient population.

These technologically advanced products are presenting lucrative opportunities for prominent players who are emphasizing the integration of connected care and software analytics. Such steps are further anticipated to fuel the adoption rate for these devices.

- In March 2022, Novo Nordisk A/S launched smart insulin pens with the aim of catering to the growing patient population suffering from diabetes in the U.K.

Market Challenges

Alternative Delivery Methods to Hinder the Market Expansion

There is an escalation in the number of benefits associated with injector pens, such as accessibility, self-injectability, and others, among the patient population. However, the emergence of alternative medication delivery systems such as oral therapies, implantable systems, transdermal therapies, and others is presenting a major challenge to conventional products in the market.

The growing focus of pharmaceutical manufacturers on developing alternative products to improve patient adherence and comfort for a wide variety of applications has shifted patient preference from traditional pens to oral-based therapies and others. Furthermore, technological advancements in non-invasive medication systems, such as patches, are also contributing factors leading to a shift toward these alternative products.

- For instance, according to 2025 data published by Dove Medical Press Ltd., it was reported that about 75% – 100% of patients currently on injection therapies prefer switching to an oral medication.

Other Prominent Challenges

- Stringent regulatory requirements and long product-approval timelines

- Supply chain disruptions affecting device production and distribution logistics

Injection Pen Market Trends

Shifting Preference for Homecare Settings to Fuel Devices Demand

There is an increasing shift in preference from hospitals and clinics to home care settings due to the benefits of convenience, enhanced comfort, personalized care, cost-effective treatment therapies, and others.

This shift is boosting the demand for these devices, thereby augmenting the focus of prominent players on the development of technologically advanced devices, such as remote monitoring products, self-injectable devices, and others. This is further expected to boost the adoption of injector pens in home care settings worldwide.

- For instance, in October 2025, PharmaJet initiated the development of a needle-free injection portfolio, including a suite of proprietary, needle-free, self-injector pens for home use.

Download Free sample to learn more about this report.

Other Prominent Trends

- Expansion of contract manufacturing partnerships between pharma companies and device developers for integrated drug-device solutions

- Regulatory focus on user-centric design and safety features such as dose-lock mechanisms and ergonomic grips

SEGMENTATION ANALYSIS

By Type

Increasing Chronic Disease Prevalence to Drive Conventional Segment’s Dominance

Based on type, the market is classified into conventional and smart.

The conventional segment held the largest market share in 2024. The growth is due to the increasing prevalence of chronic conditions, including diabetes and others, among patients, resulting in a soaring demand for these products globally. This, along with the escalating focus of key players toward research and development activities to launch innovative devices, is further anticipated to support the segmental growth. The conventiol segment is projected to dominate the market with a share of 94.39% in 2026.

- In September 2025, Wuxi NEST Biotechnology Co., Ltd., launched the NEST TSA disposable pen injector with an aim to strengthen its product portfolio.

The smart segment is expected to grow at a CAGR of 12.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Usage

Disposable Segment Dominated in 2024 with Benefits of Dosing Accuracy and Ease of Use

Based on usage, the market is divided into disposable and reusable categories.

The disposable segment dominated the market in 2024. In 2025, the segment is anticipated to dominate with an 87.9% share. The dominant share is attributed to the benefits of disposable products such as ease of use, improved patient adherence, and dosing accuracy, among others. This, coupled with increasing focus among major players toward research and development activities to launch advanced products, is likely to contribute to the disposable injection pens segment growth. The disposable segment is expected to account for 87.90% of the market in 2026.

- In February 2023, Philips Medisize launched a disposable pen injector with the aim of accelerating the delivery of multiple drug therapies.

The reusable segment is expected to grow at a CAGR of 10.4% over the forecast period.

By Application

Surging Prevalence of Diabetes Led to the Dominance of the Segment

On the basis of application, the market is subdivided into diabetes, autoimmune diseases, hormonal diseases, and others.

The diabetes segment dominated the global market in 2024, holding an 88.2% share. The growth is primarily driven by an increasing prevalence of diabetes among the patient population, resulting in a growing demand for novel products in the market. This, along with the growing focus of key players on developing specific injector pens for diabetic patients, is also expected to support the segmental expansion. The diabetes segments is anticipated to hold a dominant market share of 88.41% in 2026.

- For instance, according to 2025 statistics published by the International Diabetes Federation (IDF), about 13.7% of adults have diabetes in the U.S.

The hormonal diseases segment is poised for growth, with an estimated rate of 9.9% over the analysis period.

By End-user

Increasing R&D Funding for Home-based Products Led to the Homecare Settings Segment’s Dominance

By end user, the market is divided into hospitals & ASCs, specialty clinics, homecare settings, and others.

The homecare settings segment led the market in 2024. The increasing prevalence of chronic conditions, a rising patient pool, and an escalating preference for treatment in homecare settings are some of the crucial factors supporting the growth of the segment. Additional factors bolstering segmental expansion comprise the rising research and development funding initiatives among key players. Furthermore, the segment is estimated to have acquired an 82.5% share in 2025. In 2026, the homecare settings segment is projected to lead the market with a 79.67% share.

- For instance, in October 2025, Indomo received a funding of USD 25.0 million for the development of ClearPen, an at-home investigational injectable therapeutic solution for inflammatory acne.

In addition, the specialty clinics end user segment is projected to grow at a CAGR of 10.5% during the study period.

Injection Pen Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Injection Pen Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 24.15 billion in 2025, representing 54.06% of total market revenue, and is projected to reach USD 26.73 billion in 2026. The region's dominance is attributed to several key factors, including the growing prevalence of chronic disorders, increasing demand for medication delivery devices, robust healthcare infrastructure, adequate reimbursement policies, strong adoption of digital health technologies, and a rising number of product launches by prominent players, among others. In 2026, the U.S. market is estimated to have reached USD 24.44 billion.

- For instance, according to 2025 statistics published by the Cleveland Clinic, about 1 in 4,000 to 10,000 children are suffering from growth hormone deficiency in the U.S.

Europe and Asia Pacific

Other regions, such as Europe and the Asia Pacific, are expected to witness considerable growth over the forecast period. In 2025, the Asia Pacific market stood at USD 5.85 billion, representing 13.09% of global demand, and is projected to grow to USD 6.45 billion in 2026. During the study period, the Europe contributed approximately USD 11.52 billion to the global market in 2025, accounting for 25.79% share, and is expected to reach USD 12.73 billion in 2026. This is due to the increasing development of healthcare infrastructure, surging prevalence of diseases, growth in biosimilar-driven injectable therapies, and the rising focus of key players on product launches and strengthening their distribution networks in the region. Fueled by these factors, countries in the region are anticipated to depict considerable valuation in 2025. For instance, the U.K. is expected to record a valuation of USD 2.07 billion, Germany, a value of USD 2.41 billion in 2026, and France, a value of USD 1.61 billion, in 2025.

After Europe, the Asia Pacific market is estimated to reach a valuation of USD 6.45 billion in 2026 and secure the position of the third-largest region in the global market. In the region, in 2026, the India market value is estimated to have reached USD 0.78 billion while the China market is estimated to have touched a valuation of USD 2.2 billion.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa markets are expected to witness moderate growth over the forecast period. Middle East & Africa maintained a strong presence in the global market, reaching USD 1.31 billion in 2025, accounting for 2.94% share, and is expected to reach USD 1.44 billion in 2026. The Latin America market accounted for USD 1.84 billion in 2025, representing 4.13% of the global industry, and is expected to reach USD 2.03 billion in 2026. In 2025, the Latin America market is anticipated to have recorded USD 1.84 billion as its valuation. The growing prevalence of chronic conditions, rising R&D funding initiatives, surging awareness of early detection and diagnosis, and adoption of self-injectable products are anticipated to fuel the demand for these products. In the Middle East & Africa, the GCC market is poised to have touched a value of USD 0.78 billion in 2025.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches by Prominent Players to Support their Dominance

A robust product portfolio of technologically advanced products and a strong presence globally are vital factors contributing to the dominance of these players in the market. BD, Eli Lilly and Company, and Novo Nordisk A/S emerged as major players in the market in 2024. The increasing focus of major players on receiving approval from regulatory bodies for their novel devices is likely to support their global injection pen market share.

- For instance, in December 2022, Novo Nordisk A/S received U.S. FDA approval for a smart sensor Mallya. The sensor converts a disposable pen into a smartphone-connected device by directly attaching to insulin pen injectors.

Other key players, including Sanofi, and others, are also growing in the market, primarily owing to their escalating focus on acquisitions and mergers among other players to expand their presence in the market.

List of Key Injection Pen Companies Profiled

- BD (U.S.)

- Sanofi (France)

- Novo Nordisk A/S (Denmark)

- Eli Lilly and Company (U.S.)

- Wuxi NEST Biotechnology Co., Ltd. (China)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Medtronic (Ireland)

- SHL Medical (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- October 2025 – Borealis GmbH, in collaboration with Nemera, presented the sample of their injector pen at K Fair in Germany. The move helped the industry player in strengthening its presence.

- May 2025 – Zydus Lifesciences launched single-pen semaglutide therapy aimed at addressing diabetes and obesity. This helped the company increase its brand presence.

- January 2022 – SHL Medical collaborated with Innovation Zed to launch InsulCheck DOSE, a connected add-on device that transforms traditional pen injectors into smart solutions to support the monitoring of disease among the patient population.

- September 2021 – Owen Mumford launched a new 2-step single-use auto-injector, Aidaptus, for both 1 ml and 2.25 ml pre-filled syringes with an aim to strengthen its product portfolio.

- October 2019 – BD launched the BD Intevi 1mL two-step disposable autoinjector, a device that combines an autoinjector and a pre-fillable syringe in one integrated system. The device was launched with an aim to enhance its product portfolio.

REPORT COVERAGE

The market report provides a detailed global market analysis and focuses on key aspects such as leading companies, type, usage, application, and end user. Besides this, the global report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.98% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type · Conventional · Smart By Usage · Disposable · Reusable By Application · Diabetes · Autoimmune Diseases · Hormonal Diseases · Others By End User · Hospitals & ASCs · Specialty Clinics · Homecare Settings · Others By Region · North America (By Type, By Usage, By Application, By End User, and by Country) o U.S. (By Usage) o Canada (By Usage) · Europe (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o U.K. (By Usage) o Germany (By Usage) o France (By Usage) o Italy (By Usage) o Spain (By Usage) o Scandinavia (By Usage) o Rest of Europe (By Usage) · Asia Pacific (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o China (By Usage) o Japan (By Usage) o India (By Usage) o Australia (By Usage) o Southeast Asia (By Usage) o Rest of Asia Pacific (By Usage) · Latin America (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o Brazil (By Usage) o Mexico (By Usage) o Rest of Latin America (By Usage) · Middle East & Africa (By Type, By Usage, By Application, By End User, and by Country/Sub-region) o GCC (By Usage) o South Africa (By Usage) o Rest of the Middle East & Africa (By Usage) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 44.68 billion in 2025 and is projected to reach USD 113.58 billion by 2034.

In 2025, the North America regional market value stood at USD 24.15 billion.

Growing at a CAGR of 10.98%, the market will exhibit steady growth over the forecast period (2026-2034).

By type, the conventional segment was the leading segment in this market in 2025.

The rising prevalence of chronic conditions is a major factor driving the market growth.

Eli Lilly and Company and Novo Nordisk A/S are the major players in the global market.

North America dominated the market share with a share of 54.06% in 2025.

The growing prevalence of chronic conditions and the rising product launches, among others, are some of the vital factors expected to boost the adoption of these products globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us