Inspection Drone Market Size, Share & Industry Analysis, By Drone Type (Rotary-Wing Drone, Fixed Wing Drone, & Hybrid Drones), By Range (Short, Medium, & Long Range), By Application (Infrastructure Inspection, Energy & Utilities Inspection, Oil & Gas Inspection, Construction & Real Estate Monitoring, Mining & Quarrying, Marine Platforms, Smart City Utilities, & Others), By Component (Drone Platform, Payloads, Communication & Data Links, Software & Analytics, & Support Systems), By Autonomy Level (Manual/Semi-Autonomous, Fully Autonomous, & Adaptive AI Autonomy), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

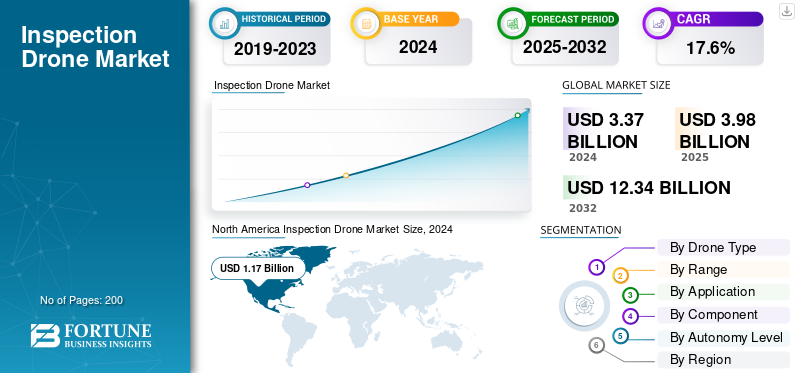

The global inspection drone market size was valued at USD 4.00 billion in 2025. The market is projected to grow from USD 4.7 billion in 2026 to USD 16.00 billion by 2034, exhibiting a CAGR during the forecast period of 16.60%. North America dominated the Inspection Drone Market with a market share of 34.50% in 2025.

Inspection drones are unmanned aircraft equipped with professional sensors, such as EO/IR cameras, LiDAR, ultrasonic detectors, or gas sensors. They collect data on assets such as power lines, pipelines, solar farms, bridges, mines, and ports. The market is growing as drones reduce inspection and monitoring real time and risk, provide better data ready for AI, and allow for routine checks at a lower cost. This growth is driven by stricter safety regulations, BVLOS pilots extending operating corridors, and the emergence of “drone-in-a-box” stations. Furthermore, improved 4G/5G and SATCOM connections is driving the market growth

Key players in market such as DJI, Skydio, Flyability, Percepto, American Robotics/Airobotics, Quantum-Systems, Emesent’s Hovermap, Parrot/ANAFI Ai and Auterion are continuously developing cost effective and more reliable inspection and monitoring drone for various application. For instance, DJI Enterprise is expanding rugged platforms and thermal/zoom payloads, and offering the DJI Dock for unattended missions. Skydio, focuses on vision-based autonomy, obstacle avoidance, and automated 3D capture.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

BVLOS Regulatory Opening is Driving Market Growth

The biggest unlock for global inspection drones is routine Beyond Visual Line of Sight (BVLOS). When regulators move from one-off waivers to clear, performance-based rules, asset owners can finally scale grid and pipeline patrols run from remote ops centers, “drone-in-a-box” units watch sites without sending trucks, and flight hour’s shift from pilots to software. That cuts per-kilometer inspection costs, boosts frequency and data quality, and turns ad-hoc pilots into multi-year platform and service procurements across utilities, oil & gas, rail, and telecom, resulting in the inspection drone market growth.

- For instance, in August 2025, the FAA published its BVLOS Notice of Proposed Rulemaking (proposed Part 108) to normalize routine BVLOS with performance-based requirements for operations, aircraft, separation/UTM services, and security creating a formal path to scalable inspection programs in the U.S.

MARKET RESTRAINTS

Origin-based Restrictions and Procurement Bans are Restraining Market Growth

Inspection programs need predictable fleets and parts pipelines. When governments tighten country-of-origin rules or expand border security-driven covered-lists, buyers hit pause: public agencies face forced retirements of non-compliant airframes, private utilities delay RFPs, and integrators must requalify payloads, radios, and software with alternative vendors. That uncertainty adds migration and training costs, introduces stranded-asset risk if approvals are pulled, and slows the shift from pilots to scaled, routine real time inspections especially in markets that rely on a few dominant suppliers.

- For instance, in October 2025, the U.S. Federal Communications Commission voted to tighten equipment-authorization rules, enabling the agency to block sales or revoke prior approvals of devices that include components from companies on its national-security Covered List, increasing procurement uncertainty for commercial drone operators.

MARKET OPPORTUNITIES

Methane & Leak-detection Mandates are Driving Market Growth

As methane and pipeline-leak rules tighten, operators need frequent, auditable surveys over vast assets, well pads, gathering lines, transmission lines, storage, and LNG sites. The inspection drones provides fast coverage, repeatable flight plans, and the ability to carry optical gas imaging or laser methane sensors. For vendors, that means sticky, high-margin inspection and monitoring programs rather than one-off site visits.

- For instance, in January 2025, the U.S. Department of Transportation’s PHMSA issued its final Advanced Leak Detection and Repair rule, adding performance-based LDAR requirements across gas transmission, distribution, regulated gathering lines, storage, and LNG facilities and explicitly accommodating methods such as remote sensing and aerial surveys, paving the way for drone-based programs.

INSPECTION DRONE MARKET TRENDS

Docked Autonomy and Remote Operations are Shaping Market

Inspection workflows are moving from field teams to “drone-in-a-box” bases managed from remote ops centers. Fixed and vehicle-mounted docks now handle launch, recovery, charging, and self-health checks so asset owners can schedule routine patrols, trigger on-demand flights after alarms, and stream data straight into maintenance systems. The result is higher real time inspection frequency at a lower marginal cost per flight, with fewer site visits and faster issue detection exactly what utilities, oil & gas, rail, and telecom want from mature programs.

- For instance, in February 2025, DJI launched Dock 3, a vehicle-mountable, 24/7 “drone-in-a-box” system paired with new Matrice airframes signaling mainstream vendor commitment to remote, automated inspections.

MARKET CHALLENGES

GNSS jamming and RF interference is challenging Market Growth

Routine inspection ops depend on two things with clean positioning and a solid command-and-control link. In and around conflict zones and wherever counter-UAS defenses are active, GNSS spoofing/jamming and RF congestion trigger dropouts, bad fixes, and forced aborts. That raises the bar for hardware (multi-band GNSS & RTK/INS fusion), comms, and ops, adding cost, weight, and training time especially for remote dock deployments. Aviation authorities have flagged the rise in interference, which keeps risk owners conservative on wide-area BVLOS inspection rollouts.

- For instance, in October 2025, the ICAO assembly formally rebuked satellite-navigation interference after widespread GPS jamming reports across Europe underscoring that GNSS disruption is now a mainstream aviation risk, not an edge case.

Russia Ukraine War Impact

The Russia–Ukraine war is reshaping inspection-drone demand and design surging grid damage is expanding urgent aerial survey workloads, while GNSS interference and border security hardening are forcing tougher, more redundant systems.

Repeated strikes on Ukraine’s power network have turned line patrols, substation assessments, and thermal scans into time-critical tasks. In high-frequency and high-risk environments, drones are faster and safer than dispatching crews. Resulting flight hours, docking stations, and analytics capacity are all pulled forward.

Across Europe, the conflict has also pushed governments to treat renewable energy corridors, ports, and digital backbones as important assets, with new EU guidance formalizing a coordinated approach to protect critical infrastructure nudging utilities and operators toward routine remote inspections rather than ad-hoc surveys. Moreover, GNSS jamming beyond the front line has become an important safety issue, driving enterprise buyers to specify multi-band GNSS with INS/visual odometry fallback, resilient C2 links, and geofenced contingency playbooks before they’ll green-light BVLOS scale-ups.

Net effect is a two-speed market immediate driving grid, pipeline, and site-damage inspection demand, paired with stricter technical baselines and operational policies that raise the bar for platforms, sensors, and software.

- For instance, in October 2025, Russia launched one of the largest drone-and-missile waves against Ukraine’s energy system, causing widespread blackouts that triggered large-scale inspection and repair cycles across the grid.

Download Free sample to learn more about this report.

Segmentation Analysis

By Drone Type

Close-proximity Maneuverability and Hover Precision, Rotary-wing Drones Dominate Market

In terms of drone type, the market is categorized into rotary-wing drones, fixed-wing drones, and hybrid VTOL drones.

Rotary-wing drones segments is projecteed to dominate the market with a share of 66.49% in 2026. Due to day-to-day inspections happen inches from energized lines, flare stacks, bridges, rooftops where a steady hover and fine attitude control matter more than range. Multirotors launch anywhere, hold position safely in tight spaces, and swap payloads without changing airframes. That makes them the default choice for utilities, oil & gas, rail, and telecom especially as “drone-in-a-box” programs shift work from field crews to remote ops centers.

For instance, in February 2025, DJI introduced Dock 3, a vehicle-mountable, 24/7 drone-in-a-box system paired with new Matrice 4-series multirotor and positioned for enterprise inspection and remote operations.

Hybrid VTOL drones segment is expected to grow at a fastest CAGR of 18.4% over the forecast period.

By Range

Due to VLOS Rules and Site-centric Workflows, Short Range (<5 km) Dominates Market

On the basis of range, the market is classified into short range (<5 km), medium range (5–25 km), and long range (>25 km).

Most inspection missions take place close to the asset, such as substations, flare stacks, bridge spans, rooftops, and towers resulting in short range (<5 km) segments is projecteed to dominate the market with a share of 60.68% in 2026. In these situations, stable hovering, precise positioning, and quick redeployments are more important than long-range capabilities. Since regulators still require visual line-of-sight for routine commercial flights in many areas, operators organize missions to stay nearby, often using fixed or vehicle-mounted docks. This approach keeps crews, radios, and risks contained, simplifies approvals and training, and reduces per-flight costs. As a result, most flight hours and expenses are focused on short-range operations.

For instance, in September 2025, Volatus Aerospace signed a multi-year agreement with one of North America’s largest power utilities to provide RPAS inspection, mapping, and data services across ~100,000 miles of transmission & distribution assets through August 2028 work that includes tower and substation inspections typically flown as short-range, VLOS multirotor missions from local launch points.

The long range (>25 km) segment is expected to grow at a fastest CAGR of 18.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Compliance-driven, High-frequency Patrols of Critical Assets, Energy & Utilities Inspection Dominates Market

Based on applications, the market is segmented into infrastructure inspections, energy & utilities inspection, oil & gas inspection, construction & real estate monitoring, mining & quarrying, marine & offshore platforms, public infrastructure & smart city utilities, and others.

Energy & utilities inspection segments is projecteed to dominate the market with a share of 31.84% in 2026.. Power and gas networks must need inspection on a schedule and after every storm, heatwave, or alarm. That turns drones into an always-on tool for transmission lines, substations, wind turbines, and solar farms where a steady hover, thermal/zoom payloads, and repeatable flight plans cut truck rolls and speed fault finding. Budgets here are tied to reliability and regulatory penalties, so flight hours convert into multi-year programs, making renewable energy & utilities the largest and most durable application bucket compared with episodic work in construction or mining.

- For instance, in September 2025, the U.K.’s National Grid began rolling out a centralized, autonomous drone inspection system with sees.ai to scale routine grid inspections across its transmission network, an enterprise deployment that underscores utilities’ outsized demand for inspection drones.

The segment of marine & offshore platforms is growing at a CAGR of 19.0% growth across the forecast period.

By Component

Decision-grade Insights and Recurring ROI, Software & Analytics Dominates Market

Based on by component, the market is segmented into drone platform, payloads, navigation & control systems, communication & data links, software & analytics, and support systems.

Software & analytics segments is projecteed to dominate the market with a share of 25.53% in 2026. Hardware plays an important role, but it grows when images become findings, tickets, and compliance records. Buyers prioritize software that automates flight planning, finds defects using AI, measures risk (heat, corrosion, vegetation, leaks), and sends work orders into EAM or CMMS systems. As platforms become widely available, budgets move toward subscriptions for processing, dashboards, and API integrations, particularly in utilities and oil and gas, where audit trails and SLA compliance are important. This change transforms one-time flights into ongoing programs based on analytics, not just airframes.

For instance, in October 2025, Axpo showcased its LINIA software suite at INTERGEO 2025, offering automated flight planning and AI-driven powerline inspection analytics an end-to-end workflow signal that is consolidated around data and insights rather than new airframes alone.

The segment of support systems is set to fastest growth at a CAGR of 18.0% growth across the forecast period.

By Autonomy Level

VLOS Oversight and Human-in-the-loop Risk Controls, Manual/Semi-Autonomous Dominates Market

Based on autonomy level, the market is segmented into manual/semi-autonomous, fully autonomous (pre-programmed), and adaptive AI autonomy.

Manual / semi-autonomous segments lead the market. Most inspection programs still put a pilot and often a visual observer in charge as it shortens approvals, fits today’s operating rules, and keeps liability and change-management simple. Semi-autonomous features auto-hover, waypoint holds, orbit, terrain follow speed repeatable work without removing the human supervisor regulators expect. Until routine BVLOS and higher-order autonomy are fully normalized at scale, enterprises default to manual/semi for day-to-day tower, substation, plant, and rooftop inspections.

Others segment consisting of adaptive AI autonomy is set to grow at a rate of 19.4% growth across the inspection drone market forecast period.

Inspection Drone Market Regional Outlook

BVLOS Regulatory Momentum and Utility-scale Budgets, North America Dominates Market

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Inspection Drone Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, the North America market stood at USD 1.37 Billion, representing 34.45% of global demand, and is projected to grow to USD 1.61 Billion in 2026. The region continues to lead due to the rapid integration of drone-based inspection solutions across energy, utilities, infrastructure, telecommunications, and industrial sectors. The United States accounted for over 90.59% of the regional market in 2024, reflecting its advanced regulatory environment and high level of commercial drone adoption. Regulatory developments, particularly the Federal Aviation Administration’s (FAA) efforts to establish Beyond Visual Line of Sight (BVLOS) operational frameworks, are providing greater clarity for large-scale deployments. Canada is also supporting market growth through progressive RPAS regulations that facilitate commercial drone operations without extensive case-by-case approvals. Growing demand for cost-effective, safe, and data-driven inspection solutions continues to support regional expansion. The U.S. market is valued at USD 1.46 billion by 2026.

Europe

The Europe region captured 27.44% of the global market in 2025, generating USD 1.09 Billion in revenue, and is projected to reach USD 1.29 Billion in 2026. Europe is expected to witness strong growth during the forecast period, registering a CAGR of 17.1%. positioning Europe as a key growth hub for inspection drone technologies. Growth is being driven by increasing adoption of drones for infrastructure monitoring, renewable energy asset inspections, and industrial maintenance activities. Harmonized regulatory frameworks across several European countries are improving operational efficiency and encouraging broader commercial adoption. The U.K. market is valued at USD 0.20 billion by 2026, while the Germany market is valued at USD 0.22 billion by 2026, supported by growing investments in automation, digital inspection technologies, and smart infrastructure initiatives.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 1.25 Billion in 2025, accounting for 31.40% share, and is expected to reach USD 1.49 Billion in 2026. Asia Pacific is anticipated to record significant market growth, supported by expanding industrial activities and proactive regulatory efforts aimed at accelerating drone integration. Countries such as China, India, Australia, and Japan are increasingly utilizing inspection drones across oil & gas, utilities, transportation, mining, and construction sectors. Regulatory authorities are actively supporting pilot programs and unmanned traffic management (UTM) initiatives to facilitate wider commercial deployment. The Japan market is valued at USD 0.23 billion by 2026, the China market is valued at USD 0.52 billion by 2026, and the India market is valued at USD 0.22 billion by 2026. Continued investments in industrial automation, infrastructure development, and advanced aerial data collection technologies are expected to strengthen regional demand.

Latin America

In 2025, Latin America represented USD 0.13 Billion, accounting for 3.32% of the worldwide market, and is projected to grow to USD 0.16 Billion in 2026. Latin America accounted for approximately 3.29% of the global market in 2024 and is expected to experience steady growth throughout the forecast period. Increasing investments in energy, mining, and infrastructure projects are creating favorable conditions for inspection drone adoption. Regulatory authorities across the region are gradually developing frameworks that support commercial drone operations, enabling organizations to improve asset monitoring and operational efficiency. Rising demand for cost-effective inspection methods in remote and challenging environments is expected to drive market expansion.

Middle East & Africa

The Middle East & Africa market accounted for USD 0.13 Billion in 2025, representing 3.39% of the global industry, and is expected to reach USD 0.16 Billion in 2026. Middle East & Africa represented approximately 3.33% of the global market in 2024 and is projected to register the highest CAGR of 19.4% during the forecast period. The region’s growth is primarily driven by increasing adoption of drone technologies across the energy, utilities, and infrastructure sectors. Energy operators are actively implementing large-scale inspection programs in collaboration with global technology providers to improve asset reliability and reduce operational risks. Regulatory bodies are progressively enabling commercial drone operations, supporting broader deployment across critical industries. Continued investments in digital transformation and industrial modernization initiatives are expected to further accelerate market growth across the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Mix of Established Drone OEMs and Fast-moving Autonomy/Analytics Specialists Racing to Industrialize Inspections

The inspection-drone market is becoming more active as BVLOS rulemaking, “drone-in-a-box” deployments, and AI analytics move programs from trials to everyday use. Leading airframe manufacturers such as DJI, Skydio, Parrot, Autel, Freefly, and Inspired Flight make up most fleets. Dock and remote-ops specialists, including DJI (Dock), Percepto, Azur Drones, and American Robotics (Ondas), are working with utilities, oil and gas operators, rail companies, and telecoms to conduct routine patrols from remote operations centers. Compliance and origin rules, such as NDAA and secure supply, keep U.S. and European vendors on parallel tracks in public-sector and critical infrastructure accounts. This situation reinforces close collaboration between OEMs and end-users on safety cases, cybersecurity, and maintenance integration.

At the same time, specialized payload and software companies are capturing a larger share of the value stack. Teledyne FLIR and Workswell lead in thermal imaging. SeekOps and Pergam assist with methane and leak detection. RIEGL, YellowScan, and Ouster provide LiDAR options. Elistair offers tethered, long-endurance site monitoring. Elsight improves multi-link C2 for contested RF environments. On the data side, DroneDeploy, Pix4D, Raptor Maps, Pointivo, and sees.ai turn imagery into valuable findings, tickets, and audit trails that fit into EAM and CMMS. Regional leaders such as Percepto and Elsight (Israel), Parrot, Azur Drones, Elistair (Europe), Autel (China), and an increasing number of U.S. “Blue/Green UAS” suppliers are leveraging local manufacturing, security practices, and sector partnerships to grow their market share.

LIST OF KEY INSPECTION DRONE COMPANIES PROFILED

- DJI (China)

- Skydio (U.S.)

- Parrot (France)

- Autel Robotics (China)

- Freefly Systems (U.S.)

- Inspired Flight Technologies (U.S.)

- Percepto (Israel)

- American Robotics / Ondas (U.S.)

- Azur Drones (France)

- Flyability (Switzerland)

- Elistair (France)

- Teledyne FLIR (U.S.)

- Workswell (Czech Republic)

- RIEGL (Austria)

- YellowScan (France)

- Ouster (U.S.)

- DroneDeploy (U.S.)

- Pix4D (Switzerland)

- Raptor Maps (U.S.)

- Pointivo (U.S.)

- ai (U.K.)

- Volatus Aerospace (Canada)

- Cyberhawk (U.K.)

- Terra Drone (Japan)

- Aerodyne Group (Malaysia)

- Yuneec International (Germany)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Cyberhawk renewed a multi-million-dollar, five-year global agreement with Shell to support drone inspections and iHawk visual data management across energy assets.

- June 2025: Terra Drone and MODEC renewed their joint agreement focused on drone inspections inside FPSO crude-oil storage tanks, extending offshore inspection capability.

- March 2025: Transport Canada published SOR/2025-70, amending the Canadian Aviation Regulations to permit some BVLOS and medium-sized RPAS operations without an SFOC moving a key bottleneck for routine utility inspections.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.60% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By Drone Type

By Range

By Application

By Component

By Region North America (By Drone Type, By Range, By Application, By Component, By Autonomy Level, and By Country)

Europe (By Drone Type, By Range, By Application, By Component, By Autonomy Level, and By Country)

Asia-Pacific (By Drone Type, By Range, By Application, By Component, By Autonomy Level, and By Country)

Middle East & Africa (By Drone Type, By Range, By Application, By Component, By Autonomy Level, and By Country)

Latin America (By Drone Type, By Range, By Application, By Component, By Autonomy Level, and By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.7 billion in 2026 and is projected to reach USD 16.00 billion by 2034.

In 2025, the market value stood at USD 1.37 billion.

The market is expected to exhibit a CAGR of 16.60% during the forecast period.

The rotary-wing segment led the market by drone type.

BVLOS regulatory opening is driving the market growth

DJI (China), Skydio (U.S.), Parrot (France), Autel Robotics (China), Freefly Systems (U.S.), Inspired Flight Technologies (U.S.), Percepto (Israel), American Robotics/Ondas (U.S.), Azur Drones (France), and Flyability (Switzerland), among others are the top companies in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us