Ion Implanter Market Size, Share & Industry Analysis, By Product Type (High Current Ion Implanters, Medium-Current Ion Implanters, High Energy Ion Implanters, Low Energy or Specialty Implanters), By End-Use (Integrated Device Manufacturers (IDMs) and Foundries, OSAT (Outsourced Semiconductor Assembly and Test), By Application (Semiconductor Manufacturing, Solar Cell Production, and Research and Development/ Academia), Regional Forecast, 2026-2034

Ion Implanter Market Size and Future Outlook

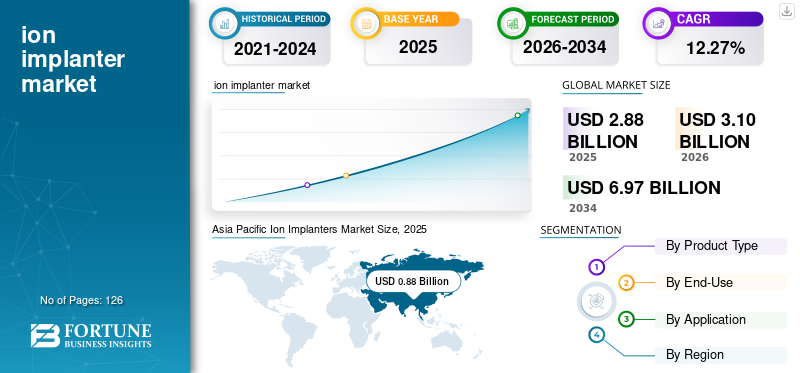

The global ion implanter market size was valued at USD 2.88 billion in 2025. The market is projected to grow from USD 3.10 billion in 2026 to USD 6.97 billion by 2034, exhibiting a CAGR of 12.27% during the forecast period. Asia Pacific dominated the ion implanter market with a market share of 30.56% in 2025.

The ion implanter market is the global industry focused on the development and supply of ion-implantation equipment used in semiconductor manufacturing to precisely introduce dopant ions into silicon wafers. The rapid growth of the semiconductor industry and rising demand for sophisticated electronic devices are the main drivers of market expansion. As technologies such as electric vehicles (EVs), artificial intelligence (AI), 5G communication, and high-performance computing continue to evolve, chip manufacturers require increasingly precise and efficient semiconductor fabrication processes. Ion implantation is a key step in semiconductor production, enabling precise wafer doping to enhance device performance and support continued miniaturization.

Ion implanter technology plays a critical role in semiconductor manufacturing by enabling precise dopant implantation into silicon wafers. Modern ion implanters incorporate advanced beam control systems, ultra-low energy implantation capabilities, and AI-driven process optimization to meet the requirements of advanced logic nodes such as 3nm and 2nm. Demand for ion implanters is rising due to semiconductor fab expansions, AI chip development, and increasing electric vehicle production. Additionally, advanced logic nodes and wide bandgap materials such as SiC and GaN require highly precise and high-energy implantation systems. Ion beams are used in ion implanters, which are critical tools in semiconductor manufacturing. The growth of ion beam technology is directly linked to the rapid expansion and advancement of the semiconductor industry.

In February 2026, the U.S. Department of Commerce's Bureau of Industry and Security (BIS) found that Applied Materials had exported ion implanter systems and associated semiconductor production equipment to China's SMIC without the required necessary permits, resulting in a USD 252 million civil penalty. Between 2020 and 2022, the claimed exports included 56 shipments of ion implanter equipment, which are essential for implanting dopants during chip manufacturing.

Applied Materials is widely recognized as an industry leader due to its broad and integrated semiconductor equipment portfolio. The company supplies high-current, medium-current, and high-energy ion implantation systems that support cutting-edge logic, memory, and foundry applications, making it one of the world's top providers of wafer fabrication equipment.

Download Free sample to learn more about this report.

ION IMPLANTER MARKET TRENDS

Expansion of AI, 5G, and High Performance Computing is Driving Market Growth

The ion implanter market is growing as AI, 5G, and High-Performance Computing (HPC) technologies continue to advance. These applications require extremely advanced, densely packed, and high-performance semiconductor chips, each of which depends heavily on precise ion implantation during manufacturing to achieve accurate dopant profiles.

The need for extreme performance, power efficiency, and miniaturization is high for high-performance computing (HPC) chips and artificial intelligence (AI) processors. Chipmakers use complex transistor designs such as FinFET and GAA, along with modern nodes (5nm, 3nm, and smaller), to meet these requirements. Due to the need for very accurate dopant placement and tight process control, the number and complexity of ion implantation procedures per wafer increase with these modern designs.

For instance, in February 2026, the top materials engineering company in the semiconductor sector, Applied Materials, Inc., unveiled new deposition, etching, and materials-altering solutions that improve the performance of cutting-edge logic chips at 2nm and above. Through atomic-scale enhancements to the transistor, the most basic electronic component, the technologies revolutionize AI computing. Gate-All-Around (GAA) transistors represent a significant industry inflection point and a crucial enabler of the energy-efficient computing required to produce more powerful AI chips. The company is unveiling novel material innovations to improve next-generation GAA transistors for angstrom nodes as 2nm-class GAA chips reach volume manufacturing this year. A large portion of the overall improvement in energy efficiency during GAA process node transitions is due to the cumulative impact of the new chip manufacturing systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Automotive Electronics to Drive Market Growth

Ion implanter sales are increasing due to growing demand for automotive electronics, as modern cars require an ever-increasing number of semiconductors, and ion implantation is an essential step in the production of these chips.

Modern cars, especially Electric Vehicles (EVs), hybrid vehicles, and advanced driver-assistance systems (ADAS), have far more electronic parts than conventional internal combustion engine vehicles. These include Microcontrollers (MCUs), power management ICs, sensors, infotainment processors, battery management systems, and radar chips. Ion implanters are used for the precise doping procedures required to manufacture all of these semiconductor devices.

For instance, in January 2026, China announced the creation of its first locally produced high-energy hydrogen ion implanter, aimed at the center of the semiconductor manufacturing sector, including power semiconductors. Power devices are essential to electric vehicles and renewable energy systems, and this achievement strengthens regional chip production capacities within EV chip supply chains.

MARKET RESTRAINTS

High Capital Investment to Hamper Market Growth

High capital expenditures are a key constraint in the ion implanter industry, as ion implantation machines are among the most technologically advanced and equipment tools used in semiconductor production, posing operational and financial challenges for chip producers.

Ion implanters incorporate complex subsystems such as cutting-edge high-voltage acceleration systems, vacuum chambers, precise beam control, contamination-control mechanisms, and complex automation software. Therefore, a single sophisticated ion implantation instrument might cost millions of dollars. Many high-current, medium-current, and high-energy implanters are frequently needed by factories for cutting-edge nodes, resulting in a substantial increase in total capital expenditures (CapEx).

MARKET OPPORTUNITIES

Growth in Oil and Gas Mining Operations to Drive Market Growth

Ion implantation is widely used in the production of semiconductor devices, which are necessary for the sophisticated power electronics, sensors, and industrial automation systems that are essential to the expanding oil and gas and mining industries, hence indirectly boosting the ion implanter market growth. Advanced machinery used in contemporary oil and gas exploration and mining includes high-reliability communication devices, drilling control systems, downhole sensors, power management systems, and automation controls. Microcontrollers, analog integrated circuits, memory chips, and power semiconductors are the foundation of these systems. As ion implantation accurately regulates electrical characteristics by introducing dopants, it is a crucial process in the manufacture of these semiconductor devices.

For instance, in February 2026, the Purion H6 high-current ion implanter, developed by Axcelis Technologies, Inc., a leading provider of ion implantation solutions for the semiconductor industry, was unveiled to meet the needs of next-generation semiconductor devices with unparalleled purity, accuracy, and productivity. The Purion H6 incorporates new technologies to support the most cutting-edge device production currently available, building on the success of the well-established Purion H product line.

MARKET CHALLENGES

Technological Complexity to Restrain Market Growth

The market for ion implanters is constrained by technological complexity, as these systems require highly advanced engineering capabilities, ongoing innovation, and significant development costs to keep up with evolving semiconductor manufacturing requirements.

Sophisticated transistor designs, such as FinFET and Gate-All-Around (GAA), are used in modern semiconductor devices manufactured at cutting-edge nodes, such as 5nm, 3nm, and smaller. These advanced designs demand extremely accurate dopant placement accuracy, rigorous beam control, minimal contamination, and sophisticated process monitoring. The complex high-voltage systems, vacuum technology, beamline engineering, thermal power, and sophisticated software integration necessary for such precision are essential for the design of ion implantation devices.

Segmentation Analysis

By Product Type

Medium-Current Ion Implanters Segment Dominated due to their Widespread Use in the Production of Sophisticated Logic

Based on product type, the market is classified into high-current ion implanters, medium-current ion implanters, high-energy ion implanters, and low-energy or specialty implanters. The medium-current ion implanters segment held the largest ion implanter market share of 45.13% in 2025. The main driver of growth in medium-current ion implanters is their widespread use in the production of sophisticated logic, foundry, and memory devices, all of which are in high demand. In CMOS devices, medium-current implanters are primarily used for threshold voltage adjustment, channel doping, and well formation. Accurate dopant control is becoming increasingly essential as semiconductor companies shift to smaller nodes (7nm, 5nm, 3nm, and below).

The high-energy ion implanters are the second-largest segment. High-energy ion implanters are designed to implant ions deep into the wafer substrate, which is necessary for creating buried layers, deep wells, and high-voltage device architectures. These features are especially crucial for power semiconductors such as IGBTs and silicon carbide (SiC) devices, which are widely used in industrial motor drives, renewable energy systems, and electric vehicles (EVs). The high-energy ion implanters segment is projected to grow at a CAGR of 12.21% during the forecast period.

By End-Use

OSAT Segment Leads due to its Ability to Handle High-Volume Semiconductor Packaging

By end-use, the market is divided into integrated device manufacturers (IDMs) and foundries, and OSAT (Outsourced Semiconductor Assembly and Test). The OSAT (Outsourced Semiconductor Assembly and Test) segment dominates the market, accounting for 76.18% in 2025. As OSAT firms handle high-volume semiconductor packaging and testing, which require specialized implantation processes for sophisticated packaging, power devices, and compound semiconductors, particularly as demand for automotive, AI, and consumer electronics applications increases, the ion implanter market is dominated by the outsourced semiconductor assembly and test (OSAT) sector.

Integrated device manufacturers (IDMs) and foundries are the second-largest segment of the market and will grow at a CAGR of 11.14% during the forecast period (2026-2034). The second-largest sector in the ion implanter industry is integrated device manufacturers (IDMs), which produce semiconductors in-house and require significant investment in wafer-processing equipment, including ion implantation systems.

By Application

Increased Investment in Next-Generation Semiconductor Technologies Boosted Research And Development/Academia Segment Growth

By application, the market is categorized into semiconductor manufacturing, solar cell production, and research and development/Academia. The research and development/academia segment dominated the market, accounting for 49.86% of the market share in 2025. Due to rising investments in cutting-edge semiconductor research, novel materials (such as SiC and GaN), and next-generation device development at universities and national laboratories, the R&D/academic sector is expanding in the ion implanter industry.

The semiconductor manufacturing segment is the second-dominating segment in the market. The segment is expected to grow at a CAGR of 10.99% during the forecast period. Since ion implantation is a crucial, high-volume process step in wafer production, necessary for the manufacturing of logic, memory, power, and analog semiconductor devices across all advanced technology nodes, the semiconductor manufacturing sector accounts for the majority of the ion implanter market.

To know how our report can help streamline your business, Speak to Analyst

Ion Implanter Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific held the dominant share of the ion implanter market in 2025, valued at USD 0.88 billion, and also led in 2026, with USD 0.94 billion. The market is expanding due to the region's robust semiconductor manufacturing infrastructure, rising factory investments in countries such as China, Taiwan, South Korea, and Japan, and growing demand for chips used in consumer electronics, EVs, and artificial intelligence.

Asia Pacific Ion Implanters Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China Ion Implanter Market

In 2025, China’s market reached USD 0.25 billion. Due to government backing for indigenous semiconductor production, expanding investments in new fabs, growing demand for EV and AI chips, and initiatives to localize semiconductor equipment amid export restrictions, the market for ion implanters in China is expanding.

In June 2023, the CETC stated that its subsidiary, the China Electronics Technology Group Corporation (CETC), had completed the 28-nanometer complete manufacturing process for ion implanters. The most important piece of equipment in chip production is the ion implanter. Currently, the 28-nanometer production method is a well-established process with the broadest applicability in the chip application industry.

India Ion Implanter Market

The Indian ion implanter market in 2025 is estimated at around USD 0.18 billion, accounting for roughly 20.52% share 2025 of the global market. The Indian market for ion implantation is expanding due to rising demand for automotive and electronic chips, increased government support for the local semiconductor industry, and increased investment in modern manufacturing and packaging plants.

North America

North America was valued at roughly USD 0.79 billion in 2025 and about USD 0.85 billion in 2026. The market is expanding due to increased demand for high-tech chips, government subsidies, and significant investments in semiconductor production.

The U.S. CHIPS and Science Act has spurred the construction of new fabs and the expansion of capacity at firms such as Intel, TSMC, Samsung, Micron, and GlobalFoundries. These fabs need cutting-edge wafer manufacturing machinery, such as medium- and high-energy ion implanters.

U.S. Ion Implanter Market

The U.S. market can be analytically approximated at around USD 0.67 billion in 2025. Due to increased investment in domestic semiconductor production, significant government support under the CHIPS and Science Act, and growing demand for sophisticated chips utilized in electric cars, data centers, AI, and defense, the U.S. ion implantation market is expanding

Europe

Europe stood at USD 0.64 billion in 2025 and about USD 0.68 billion in 2026. The increasing demand for semiconductors in the automotive and industrial sectors, growing semiconductor investments, and strong government backing through the EU Chips Act are all contributing to the expansion of the European ion implantation sector.

U.K. Ion Implanter Market

The U.K. market in 2025 stood at around USD 0.11 billion, representing roughly 17.85% of the global ion implanter market. Increasing expenditure in semiconductor R&D, compound semiconductor development, and government initiatives to boost the local chip ecosystem are driving the expansion of the industry.

Germany Ion Implanter Market

The German market in 2025 stood at around USD 0.14 billion, representing roughly 22.15% of the global market.

Latin America & Middle East Africa

Latin America and the Middle East & Africa (MEA) stood at USD 0.13 billion in 2025 and approximately USD 0.45 billion.

GCC Ion Implanter Market

The GCC market in 2025 stood at around USD 0.20 billion, accounting for roughly 45.01% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Innovation to Boost Productivity

As manufacturers continue to introduce technological improvements to keep pace with the rising complexity of semiconductor devices, the market for ion implanters is expanding. Accurate dopant placement and tighter process control have become crucial as chip manufacturers transition to smaller nodes, such as 5nm and 3nm, and use sophisticated transistor designs such as FinFET and Gate-All-Around (GAA). To combat this, manufacturers are creating ion implanters with better beam uniformity, increased energy capacity, sophisticated process control systems, and AI-driven monitoring to boost output and productivity.

In December 2023, Nissin Ion Equipment strengthened its technological footprint in the ion implanter market by developing a high-productivity material modification system (KYOKA), participating in major semiconductor industry events, and earning research accolades for breakthroughs in ion implantation.

LIST OF KEY ION IMPLANTER COMPANIES PROFILED

- Axcelis Technologies (U.S.)

- Applied Materials (U.S.)

- Nissin Ion Equipment (Japan)

- Sumitomo Heavy Industries (Japan)

- ULVAC (Japan)

- Intevac, Inc. (U.S.)

- Ion Beam Services (France)

- Advanced Ion Beam Technology (U.S.)

- Kingstone Semiconductor Joint Stock Company Ltd (China)

- High Voltage Engineering Europa B.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- February 2026: C-Click, an expert in developing electrostatic chucking (an electric chucking), was acquired by Ion Beam Services as its first strategic purchase and a major step in its plan for technological advancement. Acquiring C-Click supports Ion Beam Service's goal of rapidly developing electrostatic chuck technology and providing both integrated products and high-performance e-chucks for ion implantation systems through improved performance, precision, and overall customer satisfaction. Through this acquisition, IBS continues to broaden its R&D capabilities and enhance its product line in the ion implant segment, pursuing long-term growth and technological leadership across the semiconductor equipment industry.

- December 2025: Nissin Ion engineered and delivered an innovative universal iG8 ion implantation system that enables the production of Ultra Large Gen 8.6 flat panel displays for FPD manufacturers. Full-scale production of the iG8 ion implantation system commenced in July 2025.

- September 2025: Axcelis Technologies, Inc. is the leading supplier of enabling ion implantation technology for the semiconductor industry. Axcelis has launched its new Purion Power Series+ ion implant product family to support enhanced power device performance and productivity for next-generation power devices, such as superjunction architectures.

- December 2024: Sumitomo Heavy Industries Ion Technology and its subsidiary SEN (Sense) were officially merged to combine resources such as used equipment sales, relocation services, and parts distribution under one organization. The goal is to improve the lifecycle services and support for ion implanters. Sumitomo is combining ion implantation and laser systems into its mechatronics division as part of a broader restructuring of its semiconductor business to offer more solutions for high-end semiconductor manufacturing.

- March 2022: SurGenTec(SM), a spine and orthopedic technology company that is (partially) owned by the founder of the private equity firm Alliance Genesis, based in Boca Raton, Florida, announced they received FDA clearance for their proprietary standalone spinal fixation implant, the ION screw. This one-of-a-kind device will be used to fix (stabilize) many different types of conditions in the spine from C2 to S1.

REPORT COVERAGE

The global ion implanter market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.27% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, By End-Use, By Application, and Region |

| By Product Type |

|

| By End-Use |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.88 billion in 2025 and is projected to reach USD 6.97 billion by 2034.

The market is expected to exhibit a CAGR of 12.27% during the forecast period (2026-2034).

The research and development/academia segment led the market in terms of application

Rising demand for automotive electronics is the key factor driving market growth.

Applied Materials and Sumitomo Heavy Industries are among the prominent players in the market.

Asia Pacific dominated the market, with the highest share in 2025.

Growth in oil and gas mining operations is the significant factors that is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 126

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us