IoT in Defense Market Size, Share, & Industry Analysis By Offering (Hardware, Software, & Services), By Hardware (Sensors, Positioning & Timing, Edge Compute, Communications Modules, Gateways & Routers, Power Batteries, & Others), By Deployment Mode (On-premises, & Cloud-based), By Connectivity (Tactical & Mesh, Cellular (4G & 5G), Wi-Fi & PAN, SATCOM, Legacy & Long-Range RF, & Others), By Platform (Dismounted Soldier/Warfighter, Ground Vehicles, Aircrafts, Naval Vessels, Unmanned Systems, Satellites & Ground Platform, & Others), By Application, By End User, and Regional Forecast 2026-2034

IoT in Defense Market Size and Industry Overview

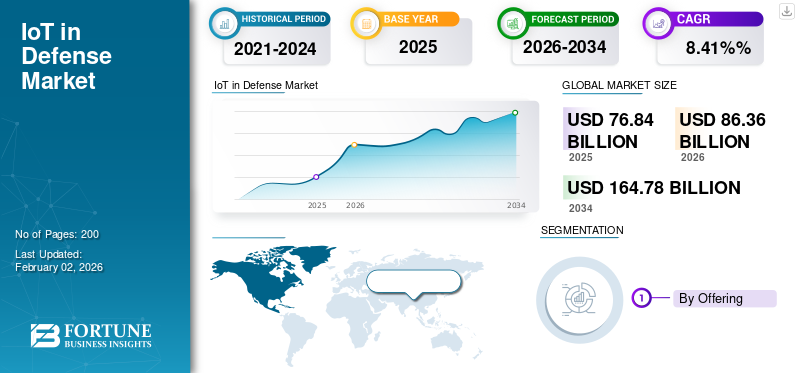

The global IoT in defense market size was valued at USD 76.84 billion in 2025 and is projected to grow from USD 86.36 billion in 2026 to USD 164.78 billion by 2034, exhibiting a CAGR of 8.41% during the forecast period. North America dominated the iot in defense market with a market share of 37.09% in 2025.

The Internet of Things (IoT) in the military, or the Internet of Military Things (IoMT) or Internet of Battlefield Things (IoBT), is a paradigm shift to conventional military operations through networked devices, sensors, and systems that share real-time data. IoT in defense covers an extensive range of interconnected devices such as unmanned aerial drones, ground sensors, wearable soldier biometrics, autonomous vehicles, weapon systems, and command centers. All these devices come together to form an integrated system that turns the traditional style of military operations into data-based, wise systems that can react fast and make predictive analysis.

This technology networks physical resources, people, and equipment in battlefield environments to improve decision-making, situational awareness, and operational effectiveness.

Moreover, IoT technology is inherently revolutionizing defense operations by enabling integrated, smart military systems that make decisions in real time and make predictions. Existing adoption exhibits considerable advantages in aspects such as battlefield awareness, monitoring of soldier health, predictive maintenance, and logistics management. Large defense contractors and military organizations globally are actively adopting IoT solutions, although issues concerning cybersecurity, interoperability, and standardization are still some of the existing concerns in the market.

Among the top defense contractors Lockheed Martin, Boeing, BAE Systems, Raytheon, and Northrop Grumman are actively embedding IoT solutions within military systems. Boeing has deployed Enterprise Sensor Integration (ESI) to over 50 locations, saving more than USD 100 million in the first year itself through better asset management and supply chain optimization. BAE Systems has been successfully applying RFID-based IoT technology to auto-track more than 200,000 assets and 30,000 components.

Download Free sample to learn more about this report.

IoT in Defense Market Key Takeways

- 2025 Market Size: USD 76.84 billion

- 2026 Market Size: USD 86.36 billion

- 2034 Forecast Market Size: USD 164.78 billion

- CAGR: 8.41% from 2026–2034

- North America dominated the IoT in defense market with a 37.09% share in 2025.

- The hardware segment accounted for the largest market share of 53.06% in 2026.

- The edge compute segment is projected to witness the fastest growth with a 10.9% CAGR during the forecast period.

North America

North America held a 37.09% market share in 2025 and was valued at USD 28.5 billion, supported by advanced defense modernization initiatives.

Europe

Europe accounted for approximately 23.91% of the global market and is expected to register the fastest regional growth with a 12.2% CAGR during the forecast period.

Asia Pacific

Asia Pacific is projected to be the second-fastest-growing region with a 10.9% CAGR, driven by investments in autonomous systems and cybersecurity capabilities.

U.S.

U.S. The IoT in defense market is projected to reach USD 29.64 billion by 2026.

Japan

Japan The IoT in defense market is projected to reach USD 3.01 billion by 2026.

Read More

Market Dynamics

Market Drivers

Enhanced Operational Efficiency and Cost Reduction Requirements Drives the Market Growth

More and more military groups are perceiving the potential of IoT, know-how in providing important operational efficiency gains and cost savings in various applications. Predictive maintenance projects of the U.S. Army with IoT-empowered diagnostics record 40% savings in maintenance expenditure while maintaining equipment readiness rates. GPS-powered IoT sensor-based real time data asset monitoring reduces losses by 30% and ensures on-time supply delivery of key supplies in intricate operational landscapes.

IoT-based logistics management provides automated material resupply, inventory optimization, and fleet management, which minimizes human error and optimizes military supply chain operations. These savings in costs and improvements in efficiency are key drivers of sustained growth as defense organizations look to maximize resource utilization and operational readiness within limited budgets.

- For instance, in March 2025, Boeing won the Next Generation Air Dominance (NGAD) fighter contract, F-47, which includes cutting-edge IoT integration for autonomous wingmen coordination of drones and sophisticated sensor networks.

The use of IoT devices in predictive maintenance applications has significant return on investment in the form of decreased unplanned downtime and asset lifecycles extended. The use in other similar military applications indicates similar benefit, with analysis of IoT sensor data anticipating component failure prior to onset, allowing proactive scheduling of maintenance and avoiding expensive equipment failure.

Market Restraints

Unwanted Cybersecurity Vulnerabilities and Data Protection Concerns Can Hamper the Market Growth

The widespread adoption of IoT devices within defense platforms dramatically increases the vulnerability, posing serious cybersecurity issues that can limit the adoption. Military IoT networks are exposed to advanced cyberattacks in the form of denial of service attacks, malware infection, passive wiretapping, and zero-day exploits that render sensitive defense data vulnerable. 60% of IoT security incidents are caused by unpatched firmware, with most defense-grade devices not having strong security measures as they are deployed due to sense of urgency.

Security agencies need to install multi-layered security systems for every technology's vulnerabilities, such as sophisticated authentication methods, real-time data validation strategies, and secure communication channels. The complexity and expense of rolling out extensive security protocols pose major impediments to widespread application of IoT in defense, thus it can hamper the IoT in defense market growth.

Market Opportunities

Increasing Use of Autonomous Systems Integration and AI-Powered Analytics to Offer Growth Opportunities

The intersection of IoT with autonomous platforms offers unparalleled potential for paradigm-shifting defense capabilities, with autonomous vehicles, drones, and weapon systems increasingly integrated into integrated IoT networks. Edge AI processing allows real-time intelligence on the battlefield to occur directly on sensors, drones, and vehicles, removing latency problems and enhancing autonomous decision-making abilities. The Internet of Battlefield Things (IoBT) facilitates the drone swarming capabilities that will be primary weapons of warfare in the future across various operational environments. AI-based biometric wearables using IoT connectivity extend real-time language interpretation, augmented reality visualization, and sophisticated health monitoring for improved soldier performance.

Integration of digital twin technology with IoT networks provides virtual copies of military assets for real-time tracking, predictive maintenance, and strategic planning purposes. Military organizations are building autonomous convoy programs and unmanned supplies that communicate on secure IoT networks, minimizing personnel risk while maximizing operating efficiency.

- For instance, in June 2025, RTX and Northrop Grumman demonstrated successful tests of U.S. Army Next-Generation Short-Range Interceptor IoT-enabled rocket motor systems, showcasing next-generation sensor integration.

Convergence of artificial intelligence with IoT platforms provides advanced analytical functions that revolutionize military decision-making processes. Machine learning algorithms process high volumes of sensor data to forecast equipment failures, streamline resource allocation, and deliver actionable intelligence for tactical operations.

IoT in DEFENSE MARKET TRENDS

Remarkable Adoption of 5G Connectivity and Network-Centric Warfare Evolution Cater to Market Growth

Convergence of 5G connectivity with military IoT systems marks a paradigm shift towards network-centric warfare solutions that provide ultra-low latency communication and huge device connectivity. 5G networks facilitate IoT-connected autonomous military platforms such as drones, unmanned vehicles, and weapon platforms to form dense and robust battlefield networks with instant situational awareness. Edge AI incorporation with 5G capabilities allows for split-second decision-making based on massive amounts of sensor data to greatly enhance autonomous vehicle navigation and threat reaction systems. Military entities are deploying private 5G infrastructure for last-mile connectivity to enable swift digital transformation on every operational front while ensuring security needs.

5G-based IoT applications provide real-time monitoring, environmental observation, and simultaneous multi-domain operations on land, air, sea, and space platforms. The technology facilitates ubiquitous connectivity for unmanned systems and enables effective remote control functions for various military assets in hostile environments. 5G mesh networks enable wireless electric charging, which removes battery reliance for IoT devices, promoting continuous operation of critical sensors and communication systems.

- For instance, in October 2025, Pacific Defense was awarded a multi-year contract by the U.S. Army to supply C5ISR Modular Open Suite of Standards (CMOSS) Mounted Form Factor systems with IoT integration for communications, command and control, and electronic warfare capabilities starting November 2025.

The shift towards network-centric models of warfare exploits 5G-enabled Internet of Things systems to define integrated command and control frameworks that cut across multiple operational environments. NATO's focus on digitally enabled, multi-domain allied operations demands interoperable IoT systems that operate effectively across various national military platforms. Software-defined networking solutions provide for dynamic reconfiguration of IoT networks according to operational needs and threat environments.

Market Challenges

Major Implementation Complexity and Integration Barriers Can Significantly Impact the Market Growth Negatively

Military institutions are confronted with high implementation complexity when incorporating IoT technologies into current defense infrastructure and operating processes. Integration into current legacy systems is challenging for manufacturers and defense contractors, demanding intricate bridging solutions to promote smooth communication while not compromising critical operations. A lack of in-house expertise within military institutions hinders effective deployment of IoT, as staff need specialized training in integrating hardware, developing software, conducting data analysis, and maintaining systems.

Cultural resistance in military hierarchies tends to inhibit new technology adoption, especially if higher management and administration is not familiar with IoT capabilities and advantages. Complicated procurement processes and long approval cycles in defense institutions prolong IoT implementation timeframes and drive higher costs in adopting technology. Scalability concerns happen when IoT pilot programs are required to be scaled across extensive military organizations with varied operational needs and geographic spread.

Expensive implementation of secure military-grade IoT systems generally exceeds budget projections, especially when end-to-end cybersecurity solutions and redundancy needs are added to deployment strategies. The high knowledge acquisition curve of IoT technology demands tremendous investment in staff training and development initiatives before organizations can efficiently harness new capabilities.

Download Free sample to learn more about this report.

Segmentation Analysis

By Offering

Continuous Requirement for Instruments for Battlespace Integrations to Boost the Hardware Segment’s Dominance

The market is segmented by offering into hardware, software, and services.

The hardware segment is projected to accounted for the largest market with a share of 53.06% in 2026. Key military countries’ integrations of instrument and connect the battlespace procurement of radios (MANET/SDR), rugged edge servers, sensors/HUMS kits, and SATCOM terminals/services anchors most programs. Even as software scales, fleets require continuous recap of terminals, routers, crypto appliances, and assured-PNT devices. The modernization cycle fueled by conflict (Russia/Ukraine war and wider NATO rearmament) accelerated procurement of tactical network encryption kits and multi-orbit SATCOM kit, frequently on multi-year IDIQs.

The software segment is estimated to be the fastest growing sub-segment during the forecast period with highest CAGR of 11.8%. The segment growth is driven by the transition from point solutions to data-driven architectures that include sensors, radios, SATCOM and platforms. Initiatives projects such as the DoD's JADC2 and JWCC build a scalable landing space for telemetry, streaming analytics, and digital twins enabling licenses for event processing, fusion middleware, and mission apps. Moreover, governments are converging on open interfaces (DDS, CoT, STANAG formats), and therefore integration spend is shifting to reusable software layers rather than custom hardware gateways. After Ukraine, the requirement for ISR velocity and robust C2 is working out to fast fielding of AI/ML, CBM+ analytics, and zero-trust agents at the edge software that can be deployed faster than new hardware cycles fuel the segmental growth.

- For instance, in April 2024, U.S. DoD reported approximately USD 1 dillion in JWCC task orders, supporting cloud/edge platforms for data-intensive IoT and C2 workloads.

By Hardware

New Edge Technologies in New Computers for Modern Battlefield Capabilities Drives the Segmental Growth of Edge Compute

The market is, by hardware is segmented into sensors, positioning & timing, edge compute, communications modules, gateways & routers, power batteries, and others.

The edge compute is estimated to the fastest growing during the forecast period with highest CAGR of 10.9%. Edge compute is expanding as commanders require decisions on-scene when links are jammed or deteriorated; that drives AI/ML inference to rugged SBCs/VPX blades at the sensor's side. The simultaneous emergence of private 5G and LEO SATCOM doesn't eliminate local processing requirements instead, increased bandwidth allows units to push models and telemetry updates while time-critical functions remain on edge. Security patterns and trusted execution enhance forward deployment of sensitive analytics. Expansion in CBM+ and digital twins fuels sensor-to-edge-to-cloud loops in loops around telemetry crunch at the platform. The Sensors segment is estimated to be the fastest growing with a share of 14.61% in 2026.

- For instance, in March 2025, Lockheed Martin–Nokia–Verizon embeds 5G in 5G.MIL Hybrid Base Station, proving out tactical 5G + edge compute styles.

The communications modules segment held dominating market share with 27.76% share in 2024. Tactical SDR/MANET radios and SATCOM user equipment communications modules continue to be the largest hardware line because IoT sensors and edge nodes rely on strong, contested-environment connections. In January 2025, the U.S. Army's purchased the HMS manpack/leader radios from L3Harris for USD 300 million. Outside line of sight, long-tail initiatives such as Iridium EMSS support narrowband sat-IoT, and contracts such as Viasat's USD 568 million worth IDIQ contract by GSA to fund SATCOM terminal and ground system installations for multi-year. In addition, PNT programs will fuel integrated comms/PNT kits at platform scale.

By Deployment Mode

Growing Integration of Cloud-Based Platform for Data and Services Provider Drives the Segmental Growth

The market, by deployment mode, is segmented into on-premises and cloud-based.

The cloud-based segment is estimated to be the fastest growing sub-segment with a highest CAGR of 11.4% during the forecast period. Cloud-based deployments are compounding with enterprise landing zones that offer certified environments for mission data and analytics throughout components’ connectivity. Digital backbones wherein cloud is default deployment mode for data and AI services with coalition interoperability pressures is driving common cloud constructs for schema, identity, and monitoring. Both these forces account for the consistent year-on-year share gains of cloud segment across all regions.

- For instance, in July 2025, U.S. Department of Defense (DoD) releases DTM 25-003 to drive enterprise-wide adoption and solidify cloud-ready controls of Zero Trust.

The on-premises segment held largest market share in 2024 with valuation of USD 41.90 billion. The on-premises segment held market with a share of 66.49% in 2026. The segment remains larger since numerous mission threads demand tight latency constraints, deterministic responses, and air-gapped operation particularly for weapon-system adjacencies and ICS/OT. Hardware-anchored accreditation cycles and platform integration tests remain optimized for on-premise footprints, and numerous navy/air applications demand offline modes for safety and doctrine.

By Connectivity

Growing 5G Strategy Implementation Plan Across all Defense Platforms Drives the Segmental Growth of Cellular (4G & 5G)

By connectivity segment, the market is categorized into tactical & mesh, cellular (4G & 5G), Wi-Fi & PAN, SATCOM, legacy & long-range RF, and others.

The cellular (4G & 5G) sub-segment is estimated to be the fastest growing during the forecast period highest CAGR of 12.2%. The growth is attributed to as there are applications being transitioned from pilots to platform deployments rapidly. OEMs then validated tactical-grade cellular for instance, in September 2025, Nokia–KONGSBERG established a European defense 5G partnership aimed at deployable solutions for allied militaries. Private 4G/5G can extend MANET by providing high spectral efficiency in semi-fixed or convoy configurations, with network slicing to isolate traffic classes. 5G serves as mid-band backhaul connecting sensors/edge compute to SATCOM gateways, in alignment with Zero-Trust policy enforcement and coalition identity control. The market is categorized into tactical & mesh is projected to be the fastest growing with a share of 30.48% in 2026.

The SATCOM segment was the dominant segment in 2024with 34.05%. The segment hold the largest share due to the fact that beyond-line-of-sight is not negotiable for expeditionary C2, ISR backhaul, and logistics telemetry. Capacity is increasing with LEO constellation expansion such as Eutelsat/OneWeb ordered Airbus in December 2024 to manufacture 100 more satellites, and EU sovereignty programs (e.g., IRIS²) underpin multi-orbit aspirations. These terminal programs have high unit cost and integration tails, which keep SATCOM's leading share even as cellular wi fi satellite communication and radio frequency.

By Platform

Increasing Adoption UAVs for Various Military Operations Catalyze Segment Growth

The market, by platform segment is categorized into dismounted soldier/warfighter, ground vehicles, aircrafts, naval vessels, unmanned systems, satellites & ground platform, and others.

The unmanned systems are projected to be the fastest growing segment during the forecast period with a highest a compound annual growth rate of 12.7%. Unmanned systems are experiencing accelerated usage towards massed, aerial platforms that provide ISR and strike at a sustainable cost. Programs emphatically highlight autonomy with onboard compute doing navigation, perception, and teaming so that systems can persist across different mission’s capabilities. Ongoing counter-UAS contests fuel fast avionics, sensor, and datalink upgrades, increasing IoT content per vehicle. Training pipelines, spares, and field repair kits are catching up, converting pilot swarms into lasting fleets, driving the segment growth.

- For instance, in June 2024, Eviden (Atos) contracted for SICS ALAT to embed SCORPION combat information system into French Army light aviation by 2026 (air/land digital spine).

The ground vehicles segment held the highest market share in the market with 29.72% share in 2024. Ground vehicles continue to be the biggest platform due to armies owning the deepest fleets and standardizing HUMS/CBM+ kits, rugged gateways, and secure radios as baseline fit. Assured PNT is being provided in big volume across vehicles and watercraft adding even more IoT content per platform. Export programs and localized manufacturing further expand volume fleets, making ground vehicles the leading platform through 2025.

By Application

C4ISR & Situational Awareness Dominated as Data Backbones in Defense Countries Have Significantly Grown

By application, the market is segmented into C4ISR & situational awareness, autonomy & teaming, logistics & supply, soldier health & performance, electronic warfare, border/coastal surveillance, CBRNE & environmental monitoring, and others.

The C4ISR & situational awareness held the largest market share in 2024 with 31.90%. C4ISR is still the largest portion as data backbones have become formal programs in all the significant defense countries. The ongoing developing innovations for sensor fusion, COP, and mission applications on all defense platforms. These components gather feeds from EW, PNT, and autonomy nodes, making IoT to flow through C4ISR services and tool chains. As cloud-edge orchestration becomes the norm, C4ISR's share expands instead of contracting, remains the largest application.

The autonomy & teaming sub-segment is estimated to be the fastest growing segment during the forecast period with highest CAGR of 12.9%. Autonomy & teaming grows the fastest because high number of defense customers are now executing it at large scale. Major number of governments plans to field several thousands of attritable systems, converting pilot swarms to persistent capability and driving the use of autonomy software, sensors, and comms into each unit. This shift places emphasis on ISR speed and low-cost strike, where teaming enables attritable systems to take risk while manned assets maintain stand-off. Russia/Ukraine war affects mass drones, quick targeting, contested spectrum drive TTP evolution, and autonomy budgets. Autonomy expenditures increase in all areas without cannibalizing C4ISR, since it is mission-additive and now supported by top-down efforts.

To know how our report can help streamline your business, Speak to Analyst

By End User

Need for Real-Time Flight Data Analysis Makes Air Forces Segment To Be The Fastest Growing

The market, by end user is divided into land forces, air forces, and naval forces.

The air forces is estimated to be the fastest growing during the forecast period with a CAGR of 11.7%. The growth is attributed due to the urgent requirement for sophisticated predictive maintenance and real-time flight data analysis. Advanced combat and transport aircraft produce enormous amounts of sensor data ranging from engine health metrics to structural stress readings, when analyzed at the edge, allow maintenance personnel to predict component failures and schedule interventions prior to costly groundings.

- For instance, in March 2025, The Indian Air Force finalized an agreement with IG Defense for a BLE tool-tracking system aimed at improving safety at airbases. This BLE-based tool-tracking solution transforms existing process by incorporating AI-powered inventory oversight and industrial internet of things (IIoT) technology, which minimizes operational downtime and guarantees precise tool accountability while also being highly cost-efficient.

The land force segment dominated the market share in 2024 with 43.35% market share. The growth is attributed to the high-scaled usage of ground-based of armored and wheeled vehicles and in vast fleet sizes. Tanks, infantry fighting vehicles, mobile artillery, and logistics trucks are being fitted with IoT sensors retroactively to support engine diagnostics, fuel-consumption, tire-pressure notification, and geofencing as a means to increase survivability on the battlefield.

IoT in Defense Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, Africa, and Latin America

North America

North Americ IoT in Defense Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America dominated the global IoT in defense market share in 2026 with 37.09% share. The region was valued USD 28.5 billion in 2025 and is projected to reach USD 31.89 billion in 2034. In addition, the region is expected to grow at compound annual growth rate of 9.8% during forecast period.

The region's leadership stems from mature defense ecosystems, substantial R&D investments, and active collaborations between the Department of Defense and premier defense contractors. The regional advantage is further strengthened by extensive technological infrastructure, established defense industrial bases, and comprehensive government support for advanced military technologies. Canada also contributes significantly to regional growth, particularly through Arctic surveillance programs, secure logistics applications, and collaborative defense initiatives with allied nations that drive continued IoT adoption across North American defense establishments.

The U.S. represents the epicenter of global military IoT innovation and deployment, accounting for 87.53% of the regional market and leading worldwide implementation of connected battlefield technologies. American defense organizations demonstrate the highest IoT adoption rates globally, driven by comprehensive modernization initiatives across all service branches and sustained funding for advanced technology integration programs. The U.S. market is valued at USD 29.64 billion by 2026.

Europe

Europe region is estimated to be the fastest growing region during the forecast period with the highest CAGR of 12.2%. Europe represents the second-largest regional market for IoT in defense applications, accounting for approximately 23.91% of global market share driven by comprehensive modernization programs and increased security concerns. The European IoT in aerospace and defense market demonstrates robust expansion potential, with regional values expected to experience significant compound annual growth rates as defense budgets reach historic levels. The UK market is projected to valued at USD 3.01 billion by 2026, and the Germany market is projected to valued at USD 4.23 billion by 2026.

The European defense IoT landscape is characterized by robust regulatory frameworks, comprehensive cybersecurity initiatives, and substantial investments in interoperability standards that differentiates the region from its global competitors. European governments demonstrate unprecedented commitment to defense IoT through comprehensive funding mechanisms, strategic partnerships, and regulatory frameworks designed to accelerate technology adoption while maintaining security requirements. The European Commission invested around USD 910 million under the 2024 European Defense Fund to create strong and innovative defense industries, bringing total EU funding for collaborative defense R&D.

Asia Pacific

The Asia Pacific market is projected to be the second fastest growing region during the forecast period with growing 10.9% CAGR. The defense IoT landscape of the region is characterized by diverse national approaches, comprehensive cybersecurity initiatives, and substantial investments in autonomous systems that differentiates the region through unique technological sovereignty requirements. South Korea demonstrated leadership in post-quantum IoT development through the establishment of specialized R&D centers with SEALSQ, positioning the country as a global hub for quantum-resistant semiconductor and IoT technologies. The Japan market is projected valued at USD 3.01 billion by 2026, the China market is projected valued at USD 7.85 billion by 2026, and the India market is valued at USD 4.49 billion by 2026.

The region's IoT adoption benefits from established electronics manufacturing capabilities, advanced 5G infrastructure deployment, and comprehensive academic research programs supporting both civilian and military technology deployment mode. Australia's AUKUS partnership represents trilateral cooperation involving nuclear-powered submarines and advanced capabilities including undersea systems, quantum technologies, artificial intelligence, and electronic warfare. These regional dynamics create favorable conditions for continued IoT growth while addressing unique challenges related to interoperability, cybersecurity, and technology sovereignty requirements across diverse political and economic systems.

Middle East & Africa

Middle East & Africa market growth is accelerated by ongoing conflicts, territorial disputes, and comprehensive defense cooperation frameworks that drive sustained IoT adoption across military platforms. The region benefits from substantial oil revenues, established defense industrial partnerships, and strong governmental support for technology sovereignty initiatives that create favorable conditions for IoT integration.

Middle East & Africa defense IoT adoption is characterized by diverse national approaches, substantial cybersecurity investments, and strategic partnerships with global technology providers that differentiate the region through unique operational requirements. Israel demonstrates world-leading capabilities in AI-driven military systems, including the first AI-assisted military operations utilizing programs such as Gospel and Lavender for autonomous threat detection and response.

Latin America

Latin American military organizations are comprehensively integrating IoT through modernization programs, emphasizing communication systems, border security, and autonomous platform development across diverse operational environments. Brazil's military modernization includes inclusive communication integration through Motorola Solutions' federal network enabling seamless collaboration between Army, Federal Highway Patrol, and Military Police using IoT-enabled platforms.

Regional military services lead in innovative IoT applications through collaborative programs leveraging both national capabilities and international partnerships for enhanced operational effectiveness. Latin American defense cooperation addresses interoperability challenges through standardized communication systems, shared intelligence platforms, and coordinated response capabilities. Regional military programs emphasize dual-use technology development where civilian IoT applications provide cost-effective pathways to military deployment while maintaining stringent national security and performance requirements for defense-specific operational environments.

Rest of the World

The Rest of the World market generated USD 3 billion in 2025, representing 3.90% of the global market landscape, and is expected to reach USD 3.22 billion in 2026.

COMPETITIVE LANDSCAPE

Key Market Players

Growing Research and Development of Advanced Technological Products by Major Key Players is Reshaping the Competition Dynamics

Lockheed Martin, Boeing, Raytheon Technologies, Northrop Grumman, and General Dynamics collectively command over largest share of the global IoT in defense sector, with each investing heavily in connected sensors, autonomous platforms, and C4ISR integrations. Lockheed Martin’s IoT-enabled F-35 and C-130J digital communications networks position it as the market leader in airborne solutions, while Boeing’s Enterprise Sensor Integration (ESI) program delivered over USD 100 million in first-year savings through asset tracking. Raytheon’s AMRAAM Telemetry Systems and Northrop Grumman’s sensor-integrated B-21 designs focus on real-time data fusion, capturing significant market share in missile and surveillance systems. These established OEMs leverage global service networks, decades-long defense relationships, and proprietary IoT platforms to maintain market leadership.

In addition, OEMs emphasize R&D spend on next-generation sensors, edge computing, and AI-powered IoT analytics to differentiate offerings. Collaborations such as Airbus-Leonardo-Thales satellite ventures (USD 9.78 billion) and Boeing-BAE Systems logistics alliances create integrated IoT ecosystems across platforms and regions. Firms capitalize on APFIT and DIU programs for accelerated prototyping, partnering directly with DoD to co-develop and co-own IP, reducing procurement barriers.

Increasing convergence of AI, edge computing, and 6G-enabled IoT networks will drive next-generation defense capabilities. Challenger firms with strong software-centric offerings and rapid fielding capabilities are poised to disrupt incumbents’ services revenue through subscription-based analytics and autonomous operations. Traditional OEMs will respond by expanding digital services, forging deeper government partnerships, and integrating open-architecture frameworks to maintain market leadership amid evolving defense IoT demands.

List of Key IoT in Defense Market Companies:-

- Amazon Web Services, Inc. (U.S.)

- C3.ai, Inc. (U.S.)

- Cisco Systems, Inc. (U.S.)

- Curtiss-Wright Corporation (U.S.)

- Elbit Systems Ltd. (Israel)

- Eutelsat Group S.A. (France)

- General Dynamics Mission Systems, Inc. (U.S.)

- Honeywell International Inc. (U.S.)

- Iridium Communications Inc. (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Microsoft Corporation (U.S.)

- Nokia Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Palantir Technologies Inc. (U.S.)

- RTX Corporation (Raytheon) (U.S.)

- Semtech Corporation (U.S.)

- Telefonaktiebolaget LM Ericsson (publ) (Sweden)

- Thales S.A. (France)

- Viasat, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Pacific Defense was awarded a multi-year contract by the U.S. Army to supply C5ISR Modular Open Suite of Standards (CMOSS) Mounted Form Factor systems with IoT integration for communications, command and control, and electronic warfare capabilities starting from November 2025.

- October 2025: General Dynamics Information Technology was awarded a task order to upgrade network infrastructure and deploy AI, machine learning, and cybersecurity solutions for U.S. Army operations in Africa and Europe.

- October 2025: Oshkosh Defense was awarded by the U.S. Army Contracting Command for Palletized Load System A2 vehicles with by-wire capability for autonomous operation and IoT-driven active safety features.

- October 2025: The Missile Defense Agency started awarding contracts for the Multiple Award Scalable Homeland Innovative Enterprise Layered Defense program, which uses IoT-enabled satellite networks and sensor systems.

- August 2025: The Department of War selected five project proposals for Advanced Dynamic Spectrum Sharing Demonstration incorporating IoT communications and sensor networks.

REPORT COVERAGE

The global IoT in defense market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.41% from 2026-2034 |

| Unit | USD Billion |

| Segmentation |

By Offering

By Hardware

By Deployment Mode

By Platform

By Application

By End User

|

| By Region |

North America (By Offering, By Hardware, By Deployment Mode, By Connectivity, By Platform, By Application, By End User, By Country)

Europe (By Offering, By Hardware, By Deployment Mode, By Connectivity, By Platform, By Application, By End User, By Country)

Asia Pacific (By Offering, By Hardware, By Deployment Mode, By Connectivity, By Platform, By Application, By End User, By Country)

Middle East & Africa (By Offering, By Hardware, By Deployment Mode, By Connectivity, By Platform, By Application, By End User, By Country)

Latin America (By Offering, By Hardware, By Deployment Mode, By Connectivity, By Platform, By Application, By End User, By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 86.36 billion in 2026 and is projected to reach USD 164.78 billion by 2034.

In 2025, the market value stood at USD 76.84 billion

The market is expected to exhibit a CAGR of 8.41% during the forecast period.

The Unmanned Systems sub-segment is expected to hold the highest CAGR over the forecast period.

The enhanced operational efficiency and catering cost reduction requirements drives the market growth.

Lockheed Martin, Boeing, Raytheon Technologies, Northrop Grumman, and General Dynamics and among others are top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us