Isocyanates Market Size, Share & Industry Analysis, By Type (MDI, TDI, and Aliphatic), By Application (Polyurethane Foams, Paints & Coatings, Adhesives & Sealants, Elastomers, and Others), and Regional Forecast, 2026-2034

ISOCYANATES MARKET SIZE AND FUTURE OUTLOOK

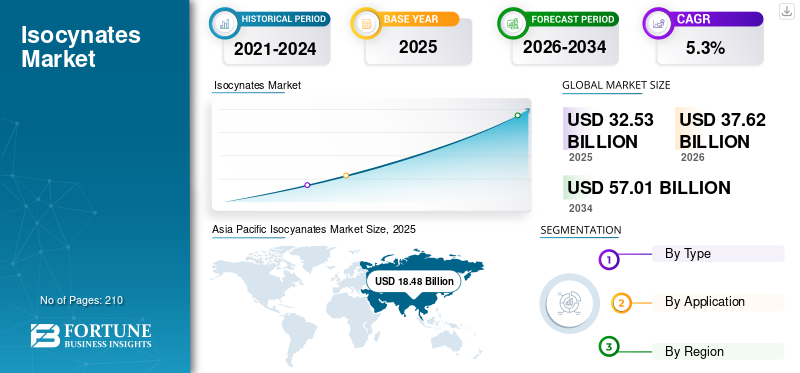

The global isocyanates market size was valued at USD 32.53 billion in 2025. The market is projected to grow from USD 37.62 billion in 2026 to USD 57.01 billion by 2034 at a CAGR of 5.3% during the forecast period. Asia pacific dominated the isocyanates market with a market share of 56.80% in 2025.

Isocyanates are highly reactive organic compounds containing the NCO functional group and are primarily used as key building blocks in the production of polyurethanes, including rigid and flexible foams, coatings, adhesives, sealants, and elastomers. The most commercially important types are MDI, TDI, and aliphatic isocyanates. Their importance stems from their ability to impart insulation, cushioning, durability, and chemical resistance across different industries. A major demand driver for the product is the growing need for polyurethane insulation in construction and refrigeration, supported by urbanization, infrastructure development, and increasing energy-efficiency requirements in buildings and cold-chain applications.

Wanhua Chemical, BASF, Covestro, Huntsman, and Dow are the key players operating in the market.

Download Free sample to learn more about this report.

ISOCYANATES MARKET Key Takeaways

- 2025 Market Size: USD 32.53 billion

- 2026 Market Size: USD 37.62 billion

- 2034 Forecast Market Size: USD 57.01 billion

- CAGR: 5.3% from 2026–2034

- Asia Pacific dominated the isocyanates market with a market share of 56.80% in 2025.

- The aliphatic segment is anticipated to rise at a CAGR of 6.1% over the forecast period.

- The elastomers segment is anticipated to rise at a CAGR of 6.0% over the forecast period.

Asia Pacific

Asia Pacific remains the leading market, supported by strong demand for polyurethane foams across construction, furniture, appliances, refrigeration, and transportation sectors.

North America

North America benefits from growing polyurethane foam consumption in insulation, bedding, furniture, appliances, and automotive interior applications.

Europe

Europe’s market growth is driven by increasing demand for polyurethane foam insulation and energy-efficient building materials, alongside expanding specialty polyurethane applications.

U.S.

The market was valued at approximately USD 5.21 billion in 2025, accounting for around 16.0% of global sales, supported by strong construction and consumer goods demand.

Japan

The market reached approximately USD 1.33 billion in 2025, representing around 4.1% of global sales, driven by steady demand from industrial and advanced manufacturing sectors.

Read More

ISOCYANATES MARKET TRENDS

Gradual Shift from Purely Commodity-Driven Demand Toward More Performance-Oriented Applications Boosts Market Growth

The major global market trend is the gradual shift from purely commodity-driven demand toward more performance-oriented applications. While MDI and TDI continue to dominate mainstream polyurethane usage, demand for specialty isocyanates is steadily increasing in applications that require superior durability, weather resistance, UV stability, and finish quality. This is especially visible in coatings, adhesives, sealants, elastomers, and other advanced materials. Customers are increasingly evaluating products on price and on lifecycle performance, application efficiency, and sustainability considerations. As a result, the industry is witnessing a steady move toward higher-value formulations and more customized solution offerings.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Energy-Efficient Buildings to Drive Market Growth

The primary driver for the industry remains strong underlying demand from construction, building insulation, refrigeration, appliances, furniture, and automotive applications. Isocyanates are essential components of polyurethane systems that provide insulation, cushioning, structural strength, and durability. As economies continue to urbanize and invest in infrastructure, the need for energy-efficient buildings, cold-chain systems, and modern consumer goods continues to rise. In particular, insulation applications remain highly important as they align with both cost-saving objectives and sustainability goals. This makes construction-linked and energy-efficiency-driven demand one of the most stable and influential long-term growth drivers for the market globally.

MARKET RESTRAINTS

Strong Exposure to Cyclical Sectors to Restrain Market Growth

A key restraint in the industry is its strong exposure to cyclical sectors such as construction, furniture, and automotive. When these sectors slow, demand for the product tends to reduce quickly, creating pricing pressure and weaker capacity utilization across the value chain. This exposure makes the market vulnerable to broader economic uncertainty, interest rate pressure, and weaker industrial sentiment. Even when long-term demand fundamentals remain positive, short-term volatility can affect purchasing behavior, delay restocking, and reduce profitability. This creates a market where strong long-term demand fundamentals are often offset by uneven short-term operating conditions across regions, limiting the isocyanates market growth in tandem.

MARKET OPPORTUNITIES

Rising Need for Safer and Higher-Value Solutions Could Unlock Premium Growth Opportunities

A major opportunity for the isocyanates market lies in the development of safer, lower-emission, and more value-added product systems. Customers are increasingly looking for solutions that improve worker safety, reduce environmental impact, and deliver better application performance. This creates room for innovation in low-monomer systems, specialty formulations, advanced coatings chemistry, and more sustainable polyurethane solutions. Suppliers that can combine performance with regulatory readiness and technical support are well-positioned to strengthen their competitive advantage. In addition, premium applications in transportation, industrial coatings, electronics, and advanced materials offer opportunities to move beyond volume-led competition and capture better margins through differentiated offerings.

MARKET CHALLENGES

Rising Complexity of Regulatory Compliance to Limit Market Growth

A major challenge faced by the global market is the increasing complexity of regulatory compliance, product stewardship, and worker safety requirements. Isocyanates are highly effective industrial intermediates, yet they also require careful handling, user training, and strict process discipline. As regulations become tighter across regions, manufacturers and downstream users must invest more in compliance systems, labeling, training, and workplace controls. This creates cost and operational pressure, especially for smaller players and converters. Over time, compliance is becoming not just a legal requirement but a strategic capability, with companies needing to balance growth, safety, customer support, and regulatory alignment more effectively than before.

SEGMENTATION ANALYSIS

By Type

MDI Segment to Lead, Driven by its Critical Role in Rigid Polyurethane Foam

Based on type, the market is segmented into MDI, TDI, and Aliphatic.

The MDI segment is anticipated to hold the dominant isocyanates market share during the forecast period. A major factor driving demand for MDI is its critical role in rigid polyurethane foam used for building insulation, refrigeration, and cold-chain infrastructure. MDI-based systems offer strong thermal efficiency, structural performance, and versatility, making them highly suitable for energy-efficient construction and appliance applications. As urbanization, infrastructure development, and sustainability priorities continue to expand globally, demand for better insulated buildings and temperature-controlled systems is rising, which directly strengthens the growth outlook for MDI across both developed and emerging markets.

The aliphatic segment is anticipated to rise at a CAGR of 6.1% over the forecast period. Demand for aliphatic isocyanates is increasing due to high-performance requirements for coatings, adhesives, sealants, and elastomers that offer superior UV stability, weather resistance, and long-term durability. Unlike aromatic isocyanates, aliphatic grades are preferred in applications where appearance retention and outdoor performance are critical, such as automotive industry coatings, industrial finishes, construction sealants, and specialty materials. As end users increasingly prioritize product longevity, premium finish quality, and lifecycle performance, aliphatic isocyanates are gaining stronger traction in value-added applications globally.

By Application

To know how our report can help streamline your business, Speak to Analyst

Polyurethane Foams Segment to Dominate due to Their Widespread Use in Insulation

Based on application, the market is segmented into polyurethane foams, paints & coatings, adhesives & sealants, elastomers, and others.

The polyurethane foams segment is anticipated to hold the dominant market share during the forecast period. A major factor driving demand for polyurethane foams is their widespread use in insulation, refrigeration, appliances, furniture, and bedding, where they deliver strong thermal efficiency, cushioning, and structural performance. In particular, rising focus on energy-efficient buildings, cold-chain expansion, and modern housing continues to strengthen demand for rigid and flexible foam systems. As construction activity, appliance ownership, and comfort-oriented consumer spending increase, polyurethane foams remain the largest and most reliable segment for the product globally.

The elastomers segment is anticipated to rise at a CAGR of 6.0% over the forecast period due to the increasing need for durable, abrasion-resistant, and high-performance materials across industrial, automotive, footwear, and specialty consumer applications. Isocyanate-based elastomers are valued for their strength, flexibility, chemical resistance, and long service life, making them suitable for wheels, rollers, belts, shoe soles, and advanced molded parts. As manufacturers increasingly seek materials that improve product durability and performance while reducing maintenance and replacement frequency, elastomers are emerging as one of the fastest-growing value-added applications for the product.

ISOCYANATES MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Isocyanates Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounts for the largest market share and is expected to maintain its dominance during the forecast period. In this region, polyurethane foams are the strongest driver of isocyanates due to their extensive use in construction, refrigeration, furniture, appliances, and transportation. The region’s rapid urban development, expanding manufacturing base, and rising household consumption continue to support strong demand for both rigid and flexible polyurethane foams. Paints & coatings, adhesives & sealants, and elastomers are all gaining traction in the region as industrial activity, infrastructure development, and higher-value manufacturing continue to expand.

Japan Isocyanates Market

Japan’s market reached approximately USD 1.33 billion in 2025, equivalent to around 4.1% of global sales.

China Isocyanates Market

China’s market is projected to be one of the largest worldwide during the study period, with 2025 revenues standing at around USD 10.67 billion, representing roughly 32.8% of global sales.

India Isocyanates Market

India’s market reached approximately USD 2.86 billion in 2025, equivalent to around 8.8% of global sales.

North America

In North America, the most important driver of the product is growing usage of polyurethane foams, particularly in insulation, appliances, bedding, furniture, and automotive interiors. Demand is strongly supported by the region’s focus on comfort, energy efficiency, and product performance across residential, commercial, and industrial end uses. While paints & coatings, along with certain elastomer applications, also contribute to overall demand, foam applications remain the dominant consumption engine due to their broad penetration and large-scale usage. Overall, an increase in construction activity, appliance production, and consumer spending on comfort-oriented products tends to directly strengthen product consumption across the region.

U.S. Isocyanates Market

The U.S. market can be analytically approximated at around USD 5.21 billion in 2025, accounting for roughly 16.0% of global sales.

Europe

In Europe, the key driver of product demand is polyurethane foams, especially in insulation and refrigeration-related applications. The region places strong emphasis on energy efficiency, building performance, and sustainable materials, which makes insulation-led demand particularly important. At the same time, adhesives, coatings, elastomers, and other specialty polyurethane applications provide meaningful support across automotive, furniture, industrial, and consumer end uses. Even so, the primary commercial story remains centered on foam applications, as they are most closely linked to the region’s long-term priorities around energy savings, high-performance construction materials, and efficient equipment systems.

U.K. Isocyanates Market

The U.K.’s market reached approximately USD 0.76 billion in 2025, equivalent to around 2.3% of global sales.

Germany Isocyanates Market

Germany’s market reached approximately USD 1.58 billion in 2025, equivalent to around 4.9% of global sales.

Latin America

In Latin America, the main driver of product demand is polyurethane foams, supported by their use in construction, refrigeration, appliances, furniture, and comfort-related consumer products. Foam applications are the most commercially important as they align closely with the region’s housing needs, growing cold-chain requirements, and increasing penetration of consumer durables. While adhesives & sealants and selected coatings applications can provide additional support, they remain secondary in comparison to the scale and relevance of foams. In essence, the regional demand outlook for isocyanates continues to be driven primarily by insulation, refrigeration, and everyday consumer applications.

Brazil Isocyanates Market

Brazil’s market reached approximately USD 0.74 billion in 2025, equivalent to around 2.3% of global sales.

Middle East & Africa

In the Middle East & Africa, the largest demand driver for isocyanates is polyurethane foams, particularly in insulation and cooling-related applications. The region’s climate conditions, infrastructure development, and rising emphasis on efficient building materials fuel foam demand. Rigid foams used in construction and refrigeration are particularly relevant as they support thermal efficiency and system performance. Adhesives & sealants and coatings are likely to make a more significant contribution as construction chemicals and industrial applications continue to expand.

Saudi Arabia Isocyanates Market

Saudi Arabia’s market reached approximately USD 0.18 billion in 2025, equivalent to around 0.6% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Participants Focus on Boosting their Capacity to Serve Higher-Value Specialty Applications

The global isocyanates industry has a highly consolidated and scale-driven competitive landscape, led by a small group of integrated producers with strong positions in MDI, TDI, and selected specialty aliphatic isocyanates. Competition is shaped by capacity scale, feedstock integration, manufacturing footprint, technology strength, and the ability to serve both commodity polyurethane demand and higher-value specialty applications. The market is also marked by aggressive Asian expansion, pricing pressure during weak demand cycles, and continued focus on downstream system solutions and sustainability-led products. A few of the key players operating in the market include Wanhua Chemical, BASF, Covestro, Huntsman, and Dow.

LIST OF KEY ISOCYANATES COMPANIES PROFILED

- Wanhua Chemical Group Co., Ltd. (China)

- BASF (Germany)

- Covestro AG (Germany)

- Huntsman (U.S.)

- Dow (U.S.)

- KUMHO MITSUI CHEMICALS CORP. (South Korea)

- Tosoh Corporation (Japan)

- Hanwha Solutions Chemical Division Corporation (South Korea)

- Cangzhou Dahua Group Co., Ltd. (China)

- Gansu Yinguang Chemical Industry Group Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Covestro expanded annual TDI capacity at its Shanghai plant from 310,000 to 370,000 metric tons through a debottlenecking project. This expansion improves supply reliability across the Asia Pacific and reinforces the company’s position in flexible foam applications, such as furniture, mattresses, and automotive seating.

- December 2025: Kumho Mitsui Chemicals announced plans to expand MDI capacity at its Yeosu plant by 100,000 tons per year, increasing total output to 710,000 tons by 2027. The investment strengthens supply for insulation, mobility, and flame-retardant applications while improving production sustainability through integrated recycling infrastructure, higher energy efficiency, and lower emissions per unit produced.

- August 2025: Covestro agreed to acquire two former Vencorex HDI derivative sites in the U.S. and Thailand. The acquisition expands its specialty isocyanates footprint, strengthening coatings and adhesives capabilities, and supports its long-term regional growth strategy.

- April 2025: Wanhua Chemical acquired Vencorex’s specialty isocyanate business, including its 70,000 TPA HDI facility in France. This acquisition expands its European footprint, strengthens aliphatic isocyanate capabilities, and improves regional supply flexibility and logistics efficiency amid global trade and tariff uncertainties.

- April 2025: Wanhua Chemical announced that its total isocyanate capacity is expected to reach 5.94 million tons per year, supported by major expansions across its MDI and TDI production network at the Fujian complex. This expansion strengthens its global manufacturing scale and enhances its leadership in its ability to meet growing downstream demand.

- February 2024: Huntsman announced the completion of the Shanghai Lianheng Isocyanate Co., Ltd., enabling independent operations of a crude MDI facility in Caojing and a hydrogen chloride recycling unit. The move provides greater operational flexibility, stronger control over key assets, and improved strategic autonomy for its polyurethanes business.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Volume (Kiloton) and Value (USD Billion) |

| Growth Rate | CAGR of 5.3% from 2026 to 2034 |

| Segmentation | By Type, By Application, and By Geography |

| By Type |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 32.53 billion in 2025 and is projected to record a valuation of USD 57.01 billion by 2034.

In 2025, Asia Pacific stood at USD 18.48 billion.

Registering a CAGR of 5.3%, the market will exhibit steady growth during the forecast period.

By application, the polyurethane foams segment is expected to lead the market.

Growing demand for energy efficient buildings are the key factors driving market growth.

Wanhua Chemical, BASF, Covestro, Huntsman, and Dow are the major players operating in the market.

Asia Pacific dominates the market in terms of share.

Shift toward higher-value formulations and more customized solution offerings are expected to drive product adoption.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us