Isoprene Market Size, Share & Industry Analysis, By Grade (Polymer Grade and Chemical Grade), By End-use (Polyisoprene Rubber, Butyl & Halobutyl Rubber, SIS & Isoprene-based Block Copolymers, and Others), and Regional Forecast, 2026-2034

Isoprene Market Size & Future Outlook

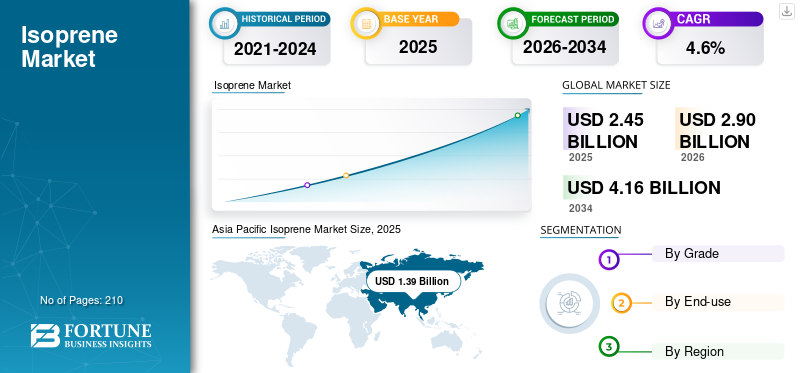

The global isoprene market size was valued at USD 2.45 billion in 2025. The market is projected to grow from USD 2.90 billion in 2026 to USD 4.16 billion by 2034, exhibiting a CAGR of 4.6% during the forecast period. Asia Pacific dominated the isoprene market with a market share of 56.73% in 2025.

Isoprene is a volatile C5 hydrocarbon monomer, chemically known as 2-methyl-1,3-butadiene, primarily used as a key building block for synthetic elastomers such as polyisoprene rubber, butyl and halobutyl rubber, and SIS block copolymers. Commercially, it is mainly recovered from C5 streams generated during naphtha steam cracking and is consumed both captively by integrated rubber producers and through merchant sales. The major demand driver for isoprene is the growing tire and automotive rubber industry, where isoprene-based elastomers provide elasticity, durability, air retention, and fatigue resistance required in tires, inner liners, seals, hoses, and industrial rubber components.

SIBUR Holding PJSC, Togliattikauchuk LLC, Shell, Kuraray, and ZEON CORPORATION are the key players operating in the market.

Download Free sample to learn more about this report.

ISOPRENE MARKET TRENDS

Growing Preference for Integrated C5 Value-chain Development is a Key Market Trend

The global isoprene industry is increasingly shifting toward integrated C5 value chain development, as producers seek to extract greater value from mixed hydrocarbon streams. Instead of treating isoprene as a standalone monomer, leading players are positioning it within broader platforms covering synthetic rubber, SIS block copolymers, hydrocarbon resins, adhesives, and specialty chemicals. This trend favors companies with access to cracker streams, separation technology, and downstream polymerization capabilities. As supply chains become more complex, integrated producers are better positioned to manage feedstock volatility, improve margins, and serve both captive and merchant demand. Thus, in turn, it benefits and drives the isoprene market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rise in Tire and Synthetic Rubber Demand Boosts Market Growth

The major demand driver for isoprene is its critical role in synthetic rubber production, especially polyisoprene rubber, butyl rubber, halobutyl rubber, and SIS block copolymers. These materials are widely used in tires, inner liners, seals, hoses, footwear, medical products, adhesives, and industrial rubber goods. Growth in vehicle production, tire replacement demand, logistics activity, and industrial manufacturing continues to support global isoprene consumption. Emerging markets are particularly important, as expanding automotive fleets, infrastructure development, and consumer goods production increase demand for durable elastomers and rubber-based materials.

MARKET RESTRAINTS

Feedstock Dependence Limits Supply Flexibility, Restraining Market Growth

A key restraint for the market is its dependence on C5 feedstock availability from petrochemical cracking operations. Isoprene supply is closely linked to cracker feedstock mix and operating conditions, which means producers cannot always increase output independently in response to market demand. Regions that rely heavily on lighter cracker feedstocks often produce fewer C5 streams, limiting local isoprene availability. This creates structural supply constraints, reduces liquidity in the merchant market, and exposes buyers to price volatility. As a result, downstream users without integrated supply can face higher procurement risk and reduced flexibility during tight market conditions.

MARKET OPPORTUNITIES

Bio-based and Low-Carbon Isoprene Development to Create Sustainable Growth Opportunities

A major opportunity for the industry lies in the development of bio-based, low-carbon isoprene. Tire, automotive, healthcare, and consumer goods companies are increasingly seeking lower-carbon materials without compromising performance. Bio-based isoprene offers the potential to replicate the performance of conventional petrochemical isoprene while improving sustainability positioning. This is especially attractive for premium applications such as high-performance tires, medical-grade synthetic rubber, specialty adhesives, and branded consumer products. If production costs and scalability improve, bio-based isoprene could open a differentiated market segment and support long-term decarbonization of synthetic rubber value chains.

MARKET CHALLENGES

Captive Consumption Keeps the Market Opaque, Limiting Market Growth

A prominent challenge in the industry is limited market transparency, driven by high captive consumption among integrated producers. Many companies produce isoprene internally and consume it directly in synthetic rubber, butyl rubber, SIS copolymers, or other C5 derivatives, leaving only a smaller portion available in the merchant market. This makes it difficult to assess true production, demand, trade flows, and pricing. For independent buyers, limited transparency can increase procurement uncertainty and dependence on long-term contracts. For market participants, this creates challenges in benchmarking, forecasting, and evaluating competitive positioning across regions.

SEGMENTATION ANALYSIS

By Grade

Polymer Grade Segment to Dominate Market Due to Its Ability to Deliver Elasticity

Based on the grade, the market is segmented into polymer grade and chemical grade.

The polymer grade segment is anticipated to hold the dominant isoprene market share during the forecast period. Polymer grade isoprene demand is primarily driven by its critical role as a monomer for synthetic elastomers, including polyisoprene rubber, butyl and halobutyl rubber, and SIS block copolymers. Growth in tire manufacturing, vehicle ownership, replacement tires, medical rubber goods, footwear, adhesives, and industrial rubber products supports sustained consumption. Its ability to deliver elasticity, resilience, tack, fatigue resistance, and air-retention performance makes polymer grade isoprene the dominant grade across high-volume rubber and elastomer applications globally.

The chemical grade segment is anticipated to rise with a CAGR of 4.2% over the forecast period.

Chemical grade isoprene demand is driven by its use in specialty chemical synthesis, where smaller-volume but higher-value applications require controlled purity and reliable quality. It serves as an intermediate for resins, fine chemicals, fragrances, flavors, pharmaceutical intermediates, agrochemical inputs, and performance additives. Growth is supported by rising demand for specialty materials, premium consumer products, healthcare-related chemicals, and customized formulations. Although smaller than polymer grade, chemical grade isoprene benefits from diversification into higher-margin, specification-sensitive end uses.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Rise in Vehicle Ownership to Boost Polyisoprene Rubber Segment Growth

Based on the end-use, the market is segmented into polyisoprene rubber, butyl & halobutyl rubber, SIS & isoprene-based block copolymers, and others.

The polyisoprene rubber segment is anticipated to hold the dominant market share during the forecast period. Polyisoprene rubber demand is primarily driven by its close performance similarity to natural rubber, offering high elasticity, resilience, tensile strength, and fatigue resistance. It is widely used in tires, medical gloves, footwear, rubber bands, seals, hoses, and industrial rubber goods. Growth in vehicle ownership, replacement tires, healthcare products, and latex-alternative medical applications supports sustained consumption. Its ability to deliver consistent quality and reduce reliance on natural rubber makes polyisoprene rubber the major isoprene application globally.

The SIS and isoprene-based segment is anticipated to rise with a CAGR of 4.7% over the forecast period. SIS and isoprene-based block copolymers are the fastest-growing end-use segment due to rising demand for pressure-sensitive adhesives, labels, tapes, packaging, hygiene products, sealants, and elastic films. These copolymers provide strong tack, flexibility, softness, peel strength, and processability, making them well-suited for consumer goods and packaging applications. Growth in e-commerce packaging, disposable hygiene products, medical tapes, and specialty adhesives is increasing consumption. Their versatility across high-value adhesive and elastomeric applications supports faster growth than traditional rubber uses.

ISOPRENE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Isoprene Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest market share and is expected to continue its dominance during the forecast period. The region is expected to remain the strongest demand center for isoprene, driven primarily by tire production, automotive manufacturing, footwear, adhesives, and industrial rubber goods. China, India, Japan, South Korea, and Southeast Asia have large downstream rubber and elastomer industries, driving strong demand for polyisoprene rubber, butyl rubber, halobutyl rubber, and SIS copolymers. Future demand will be supported by vehicle ownership growth, replacement tire demand, infrastructure activity, consumer goods manufacturing, and expanding packaging and hygiene applications, making the region the global growth engine.

Japan Isoprene Market

Japan’s market was valued at USD 0.19 billion in 2025, equivalent to around 7.8% of global sales.

China Isoprene Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 0.66 billion, representing roughly 26.9% of global sales.

India Isoprene Market

India’s market was valued at approximately USD 0.13 billion in 2025, equivalent to around 5.3% of global sales.

North America

In North America, demand for isoprene is primarily driven by growth in specialty adhesives, medical rubber goods, and high-performance elastomer applications. The region has a mature tire and automotive base. Still, future growth is likely to be supported more by value-added applications such as pressure-sensitive adhesives, hygiene products, medical tapes, surgical gloves, pharmaceutical closures, and engineered rubber components. Demand for latex-free medical products and high-quality synthetic rubber alternatives can further support isoprene consumption, especially in applications requiring purity, consistency, elasticity, and reliable performance.

U.S. Isoprene Market

The U.S. market was valued at around USD 0.29 billion in 2025, accounting for roughly 11.8% of global sales.

Europe

In Europe, the major demand driver for isoprene is the shift toward high-performance, sustainable elastomer solutions across automotive, adhesives, specialty chemical, and healthcare applications. While the region is mature, demand is supported by premium tires, low-emission mobility, medical-grade synthetic rubber, and specialty adhesives. Future growth is likely to come from bio-based or lower-carbon isoprene routes, as European buyers increasingly prioritize sustainability, traceability, and regulatory compliance. This creates opportunities for differentiated isoprene grades used in advanced rubber, sealants, tapes, and high-value polymer systems.

U.K. Isoprene Market

The U.K.’s market was valued at USD 0.03 billion in 2025, equivalent to around 1.2% of global sales.

Germany Isoprene Market

Germany’s market was valued at USD 0.07 billion in 2025, equivalent to around 2.9% of global sales.

Latin America

In Latin America, market growth is mainly driven by tire replacement, automotive rubber components, footwear, adhesives, and industrial rubber goods. Brazil and Mexico are the key consuming markets due to their automotive manufacturing bases and broader rubber-processing industries. Future growth is expected to be supported by rising vehicle ownership, road transportation activity, mining, construction, and consumer goods production. Although the region has a smaller isoprene base than Asia or Europe, demand is likely to expand steadily as local manufacturing and aftermarket tire consumption strengthen over time.

Brazil Isoprene Market

Brazil’s market was valued at USD 0.06 billion in 2025, equivalent to around 2.4% of global sales.

Middle East & Africa

In the Middle East & Africa, market expansion is attributed to the gradual expansion of downstream petrochemical conversion, industrial rubber, construction adhesives, tire replacement, and automotive aftermarket demand. Saudi Arabia and other Gulf markets are seeking to move further downstream from basic petrochemicals into specialty polymers and elastomers. At the same time, African demand is supported by infrastructure, mining, transport, and industrial applications.

Saudi Arabia Isoprene Market

Saudi Arabia’s market was valued at USD 0.05 billion in 2025, equivalent to around 2.0% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

C5 Feedstock Access and Downstream Integration Shape Market Leadership

The global isoprene industry is moderately concentrated and shaped by access to C5 feedstocks, extraction technology, and downstream integration into synthetic rubber, butyl rubber, SIS block copolymers, and specialty chemicals. Leading producers typically benefit from captive consumption, long-term customer relationships, and proximity to naphtha-cracker or petrochemical complexes. Competition is strongest among integrated players, while merchant supply remains relatively limited and less transparent. Differentiation is driven by purity, reliability, logistics reach, and downstream elastomer integration. Key players in the market include SIBUR Holding PJSC, Togliattikauchuk LLC, Shell, Kuraray, and ZEON CORPORATION, among others.

LIST OF KEY ISOPRENE COMPANIES PROFILED

- Kuraray (Japan)

- LOTTE Chemical CORPORATION (South Korea)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Ningbo Jinhai Chenguang Chemical Corporation (China)

- Shell (U.K.)

- SIBUR Holding PJSC (Russia)

- SINOPEC Baling Petrochemical Co., Ltd. (China)

- Togliattikauchuk LLC (Russia)

- ZEON CORPORATION (China)

- Zibo Luhua Hongjin New Material Group Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Zeon Corporation announced that it will invest in a new facility at its Mizushima Plant to raise dicyclopentadiene capacity by around 20% by September 2028. The project supports growth in COP and optical films, while strengthening its C5 business, which also includes isoprene, piperylene, and other key derivatives.

- February 2026: Kuraray Co., Ltd. received ISCC PLUS certification for seven isoprene chemical products manufactured at its Kashima Plant in Japan, including MMB, IPD, isoprenol, prenol, citral, MPD, and ND. The certification supports Kuraray’s sustainability goals under PASSION 2026 and reinforces responsible supply-chain management through the mass-balance approach.

REPORT COVERAGE

The global isoprene market report provides a detailed analysis of the market. It focuses on key aspects such as the profiles of leading companies, product types, and leading end-uses. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Volume (Kiloton), Value (USD Billion) |

| Growth Rate | CAGR of 4.6% during 2026-2034 |

| Segmentation | By Grade, By End-use, and By Region |

| By Grade |

|

| By End-use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 2.45 billion in 2025 and is projected to record a valuation of USD 4.16 billion by 2034.

In 2025, the market in Asia Pacific stood at USD 1.39 billion.

Registering a CAGR of 4.6%, the market will exhibit steady growth during the forecast period.

The polyisoprene rubber segment is expected to lead this market during the forecast period.

A rise in tire and synthetic rubber demand is boosting market growth.

SIBUR Holding PJSC, Togliattikauchuk LLC, Shell, Kuraray, and ZEON CORPORATION are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us