Automotive Electric Power Steering Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback, Sedan, SUVs, LCVs, and HCVs), By Vehicle Propulsion (ICE, HEV, PHEV, and BEV), By Steering Architecture (Column-Assist EPS (CEPS), Pinion-Assist EPS (P-EPS), Rack-Assist EPS (R-EPS), and Steer-by-Wire (SbW)), By Component (Motor, ECU/Controller, Sensors, Rack/Column Mechanical Assembly, and Software & Calibration) and Regional Forecast, 2026-2034

Automotive Electric Power Steering Market Size and Future Outlook

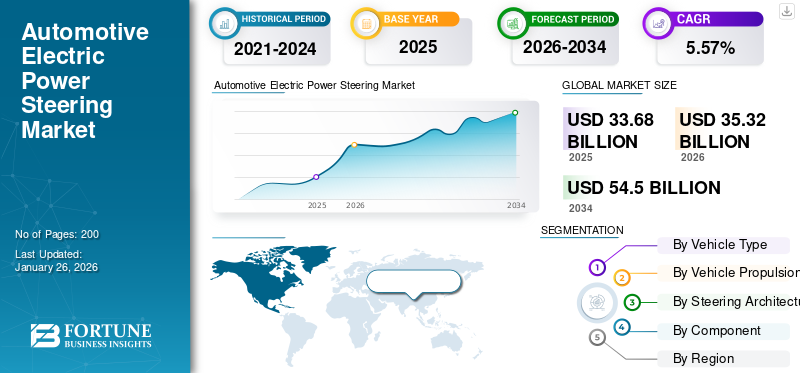

The global automotive electric power steering market size was valued at USD 33.68 billion in 2025 and is projected to grow from USD 35.32 billion in 2026 to USD 54.5 billion by 2034, exhibiting a CAGR of 5.57% during the forecast period. Asia Pacific dominated the automotive electric power steering market with a market share of 58.42% in 2025.

Automotive electric power steering (EPS) systems replace traditional hydraulic setups with electric motors and sensors, providing steering assistance based on driving conditions. Widely adopted in passenger cars and commercial vehicles, EPS enhances fuel efficiency, reduces emissions, and improves handling. The market is driven by stringent fuel efficiency and emission standards, growing demand for advanced features such as lane keeping assist and automated driving, and increasing production of electric and hybrid vehicles. Advancements in sensor technologies, integration with Advanced Driver Assistance Systems (ADAS), and lightweight designs further support growth. Electric power steering also enables steer-by-wire innovations, positioning it as a critical component in autonomous and next-generation mobility solutions.

Key players in the market include JTEKT Corporation, Robert Bosch GmbH, Nexteer Automotive, ZF Friedrichshafen, and NSK Ltd. These companies emphasize innovations in steering sensors, control algorithms, and integration with ADAS to enhance vehicle safety and performance. Strategic partnerships with OEMs, investments in lightweight and energy-efficient designs, and advancements in steer-by-wire technology position them strongly in supporting electric, hybrid, and autonomous vehicle adoption worldwide.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rising Demand for Reducing Carbon Emission Drives EPS Adoption

Automotive electric power steering systems are increasingly replacing hydraulic steering due to their energy-efficient design. Unlike hydraulic systems, EPS consumes power only when steering input is required, directly contributing to improved fuel economy and reduced carbon emissions. Growing regulatory pressures for lower CO₂ emissions and higher fuel efficiency, particularly in Europe, North America, and Asia Pacific, further accelerate adoption. As automakers shift focus to sustainable mobility, EPS emerges as a critical enabler for meeting stringent standards while improving performance. The demand for lightweight and eco-friendly steering solutions positions automotive electric power steering as a vital component in global automotive transformation. In September 2025, Knorr-Bremse unveiled its first electric power steering system for buses at Busworld 2025, emphasizing its power-on-demand feature. The innovation aims to enhance steering safety, reduce vehicle emissions, and align with sustainable mobility goals. The launch highlights electric power steering as a crucial enabler of efficiency and compliance in next-generation commercial vehicles.

MARKET RESTRAINTS:

High Development Costs and Complex Integration Limit EPS Expansion

Despite strong growth potential, automotive electric power steering systems face restraints due to high development and integration costs. Advanced EPS technologies require sophisticated sensors, electronic control units, and electric motors, which raise manufacturing expenses. This cost challenge is especially significant for price-sensitive markets and low-cost vehicle segments, where adoption remains limited. Additionally, integrating electric power steering with ADAS and steer-by-wire functions demands precise calibration and rigorous safety testing, further escalating R&D expenditure. These factors often deter smaller manufacturers, slowing overall market penetration. The high cost burden is expected to remain a restraint until economies of scale and broader technological standardization are achieved.

MARKET OPPORTUNITIES:

Integration with Autonomous Driving Creates Significant Opportunities

The rapid development of autonomous and semi-autonomous vehicles presents a strong opportunity for automotive electric power steering systems. Automotive electric power steering is central to enabling steer-by-wire technology, which eliminates mechanical linkages and provides precise electronic control for autonomous driving functions. Automakers and suppliers are investing in intelligent steering systems capable of supporting lane-keeping, automated parking, and self-driving navigation. As consumer demand for safer, connected, and automated vehicles rises, electric power steering becomes indispensable for ensuring accuracy and responsiveness. This transition positions EPS as a steering solution and also as a foundation for next-generation mobility, opening significant long-term market opportunities. In March 2025, HIRAIN announced mass production of its 24V electric power steering system for commercial vehicles. The compact, energy-efficient design supports advanced driver assistance functions, is rugged for harsh environments, and integrates with both hydraulic and electronic steering architectures, highlighting industry momentum toward smarter, lighter steering solutions.

MARKET CHALLENGES:

Ensuring Reliability Under Harsh Conditions Poses a Challenge to Product Adoption

One of the major challenges for the automotive electric power steering market lies in ensuring reliability under extreme conditions such as temperature variations, moisture exposure, vibration, and electrical interference. Unlike hydraulic systems, automotive electric power steering depends on sensitive electronic sensors and actuators that require consistent accuracy and durability. Any malfunction can compromise steering safety, posing risks for OEMs and consumers alike. Meeting stringent reliability standards demands extensive testing, durable component design, and redundancy in electronic systems. As vehicles integrate more autonomous features, guaranteeing fault-tolerant EPS operation becomes increasingly critical, making reliability under real-world conditions a persistent market challenge. In February 2025, Tesla initiated a recall involving nearly 380,000 vehicles in the U.S. due to a defect in the electric power steering assist system. The issue may lead to increased steering effort at low speeds. An over-the-air software fix has been rolled out to the impacted 2023 Model 3 and Model Y units.

MARKET TRENDS:

Growing Adoption of Steer-by-Wire Systems Defines Market Trend

A major trend shaping the automotive electric power steering market is the rising adoption of steer-by-wire technology. By eliminating traditional mechanical connections, steer-by-wire allows complete electronic steering control, enabling advanced safety features and flexible vehicle design. This trend aligns with the shift toward autonomous driving and vehicle electrification, where software-based control systems dominate. Steer-by-wire also enhances cabin space, reduces component weight, and supports modular vehicle platforms. Leading EPS manufacturers are focusing on scalable solutions to meet OEM demands for next-generation vehicles. As adoption grows, steer-by-wire becomes a transformative trend driving innovation across global steering system markets. In September 2025, Nexteer Automotive unveiled its Motion-by-Wire™ innovations, including Steer-by-Wire, at MOVE America. The showcase highlighted how software-defined steering architectures can accelerate development, reduce costs and position SbW as a critical enabler for smarter, safer, next-gen mobility.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

High Consumer Preference and Advanced Features Drive SUV Segment Growth

On the basis of vehicle type, the market is classified into hatchback, sedan, SUVs, LCVs, and HCVs.

The SUV segment dominated the automotive electric power steering market in 2026, accounting for 33.73% of the total market share, driven by global popularity, preference for spacious vehicles, and higher adoption of advanced driver-assist features. The heavier body structure of SUVs makes electric power steering essential for maneuverability, comfort, and safety. Automakers are increasingly equipping SUVs with electric power steering integrated with ADAS and steer-by-wire functions, aligning with regulatory and consumer demand. With strong sales growth across North America, Europe, China, and emerging Asian markets, SUVs remain the primary revenue-generating vehicle category for EPS manufacturers. SUVs are also the fastest-growing application due to their expanding demand in emerging economies, coupled with electrification trends. Enhanced steering comfort and safety features accelerate penetration, making SUVs the leading contributor to market volume and growth. In March 2025, China’s Zeekr unveiled its new electric SUV, the Zeekr 9X, featuring Level 3 autonomous driving readiness and a hands-off steering mode, signaling advanced EPS integration.

By Vehicle Propulsion

Widespread Adoption of ICE Vehicles Boosts the Segment Growth

In terms of vehicle propulsion, the market is categorized into ICE, HEV, PHEV, and BEV.

Internal combustion engine (ICE) vehicles dominated the automotive electric power steering market in 2026, accounting for 73.02% of the total market share, supported by their widespread global presence and large installed base. While BEVs are gaining traction, ICE vehicles remain the mainstream choice across developing economies, where affordability and fueling infrastructure favor conventional engines. Automakers are integrating electric power steering into ICE vehicles to improve fuel efficiency, reduce emissions, and comply with stricter regulatory standards. Continuous sales of ICE passenger cars, SUVs, and light commercial vehicles ensure sustained demand, making ICE propulsion the largest segment globally today.

Battery Electric Vehicles (BEVs) represent the fastest-growing segment, driven by global electrification, government incentives, and OEM commitments to zero-emission fleets. Electric power steering supports BEV energy efficiency and ADAS integration, making it critical for next-generation electric mobility. In August 2025, Nexteer Automotive introduced its dual-pinion electric power steering (DPEPS) system for deployment in ICE vehicle programs in China, enhancing steering precision and reliability in performance ICE models.

By Steering Architecture

Proven Reliability and Broad Vehicle Compatibility Lead R-EPS Segment Growth

Based on steering architecture, the market is divided into column-assist EPS (CEPS), pinion-assist EPS (P-EPS), rack-assist EPS (R-EPS), and steer-by-wire (SbW).

The rack-assist EPS (R-EPS) segment dominated the market in 2026, accounting for 51.02% of the total market share, due to its suitability across passenger cars, SUVs, and light commercial vehicles. Offering precise steering control, fuel efficiency, and easy integration with safety systems, R-EPS has become the standard solution for modern vehicles. Automakers favor modular rack assist electric power steering as it provides an optimal balance of performance and cost, and compatibility with ADAS technologies. Its proven reliability and adaptability across multiple platforms ensure its continued dominance in the global automotive EPS landscape.

To know how our report can help streamline your business, Speak to Analyst

Steer-by-Wire (SbW) is the fastest-growing segment, driven by autonomous vehicle development and EV adoption. Its elimination of mechanical linkages enables advanced safety features, design flexibility, and precise control, making it central to next-generation mobility solutions. In May 2025, China Automotive Systems’ subsidiary Jingzhou Henglong secured its first European Rack-Assist EPS (R-EPS) supply contract with a major automaker, marking a strategic entry into Western markets. The move underscores R-EPS's expansion beyond Asia and signals growing confidence in China’s EPS capabilities on a global stage.

By Component

Critical Role of EPS in Steering Assistance Secures Motor Segment Prominence

Based on component, the market is segmented into motor, ECU/controller, sensors, rack/column mechanical assembly, and software & calibration.

The motor segment dominated the automotive electric power steering market in 2026, accounting for 34.68% of the total market share, as it provides primary steering assistance by converting electrical energy into mechanical torque. With the shift from hydraulic to electric systems, demand for high-efficiency motors has surged. OEMs increasingly use compact, lightweight, and high-torque motors to improve performance and fuel efficiency. Additionally, advancements in brushless motor technology enhance durability and reduce maintenance. Given its critical role in steering response and safety, the motor remains the most essential and revenue-generating component.

Software & calibration is the fastest-growing segment, enabling precise steering feel, ADAS integration, and customizable driving modes. As vehicles adopt autonomous features and steer-by-wire systems, advanced software becomes crucial for enhancing safety, comfort, and real-time steering adaptability. In August 2025, Nexteer Automotive introduced its MotionIQ software suite aimed at intelligent motion control, streamlining ECU-sensor calibration and reducing development overhead. The software helps OEMs integrate by-wire steering functions more efficiently, mitigating costs associated with complex sensor and control unit integration.

Automotive Electric Power Steering Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific Automotive Electric Power Steering Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2025, the Asia Pacific market stood at USD 19.67 billion, representing 58.42% of global demand, and is projected to grow to USD 20.74 billion in 2026. Asia Pacific holds the largest automotive electric power steering market share, led by China, Japan, South Korea, and India. Rising vehicle production, increasing EV adoption, and government incentives for energy-efficient mobility drive rapid growth. Local suppliers and global OEMs invest in high-volume automotive electric power steering production to meet diverse demand across compact cars, SUVs, and commercial vehicles. With strong electrification policies and expanding middle-class ownership, the Asia Pacific dominates the market in terms of volume production. In December 2024, ZF announced the expansion of its electronic power steering system manufacturing in China, adding 3,700 m² of floor space in Anting, Shanghai. This marks the second EPS capacity expansion in two years, with volume production expected by end-2025 underscoring ZF’s commitment to localized steering systems and support for advanced ADAS levels in the Chinese market.

North America

The market in North America reached USD 6.42 billion in 2025, representing 19.06% of total market revenue, and is projected to reach USD 6.69 billion in 2026. North America shows steady automotive electric power steering market growth, fueled by stringent safety and emission regulations, particularly in the U.S. and Canada. The region’s strong demand for SUVs and pickup trucks accelerates product adoption, while automakers increasingly integrate advanced driver-assist systems. Technological innovation, driven by major suppliers and research hubs, supports steer-by-wire and autonomous capabilities. The region remains a key market for premium and high-performance vehicles, ensuring consistent market penetration.

The U.S. dominates the North American market due to its large vehicle production base and consumer preference for advanced safety features. Strong federal regulations for fuel efficiency and emission reduction push automakers toward electric steering solutions. SUVs and light trucks, the top-selling segments, rely heavily on electric power steering for handling and comfort. Rapid expansion of electric vehicle manufacturing further boosts demand, making the U.S. a leading innovation hub for EPS technologies. In March 2025, Ford announced the adoption of a new electric power steering module for its upcoming Mustang Mach-E variant built at its U.S. facility. The supplier-integrated system promises improved steering feedback, reduced energy draw, and enhanced ADAS compatibility, marking one of the first U.S. OEM launches of a next-gen power steering system in its passenger EV lineup.

Europe

Europe contributed approximately USD 6.08 billion to the global market in 2025, accounting for 18.06% share, and is expected to reach USD 6.28 billion in 2026. Europe represents a highly advanced automotive electric power steering market, driven by strict EU emission norms, sustainability goals, and rapid electrification. Automakers across Germany, France, and Italy are prioritizing EPS to enhance vehicle efficiency and integrate ADAS features. The region also leads in steer-by-wire innovation, aligned with autonomous driving development. Growing consumer demand for compact EVs and luxury vehicles further accelerates market adoption. Europe remains a key contributor to premium EPS solutions globally. In July 2024, Mercedes-Benz confirmed to introduce steer-by-wire technology in production vehicles from 2026, becoming the first German OEM to do so. The system eliminates the mechanical link between the steering wheel and axle, enabling greater design flexibility, ADAS integration, and redundancy for safety. ZF has been named as the technology supplier.

Rest of the World

Rest of the World recorded a market size of USD 1.5 billion in 2025, capturing 4.46% of the global market share, and is projected to reach USD 1.61 billion in 2026. The Rest of the World shows decent growth in the market of electric power steering, primarily supported by rising vehicle sales in Brazil, Mexico, and Gulf countries. Economic development and gradual electrification push automakers to adopt electric power steering in passenger cars and SUVs. While market penetration is slower compared to developed regions, increasing safety regulations and demand for fuel-efficient vehicles create opportunities. Investments in automotive assembly plants and regional expansion by global suppliers accelerate adoption in these markets. In July 2024, South Africa’s Enviro Automotive launched the Dayun Yuehu S5 electric SUV, featuring electronic power steering among its standard specifications.

COMPETITIVE LANDSCAPE

Key Industry Players:

Technological Advancements and OEM Collaborations Define Competitive Landscape

The global automotive electric power steering market is highly competitive, driven by leading Tier-1 suppliers and specialized regional players focusing on advanced technologies, ADAS integration, and steer-by-wire development. Key companies such as JTEKT Corporation, Robert Bosch GmbH, Nexteer Automotive, ZF Friedrichshafen, and NSK Ltd. dominate through strong OEM collaborations and extensive global supply chains. Competition revolves around innovations in energy-efficient motors, sensor precision, and software calibration. Growing emphasis on autonomous readiness, cost optimization, and lightweight designs intensifies rivalry, with R&D investments and strategic partnerships shaping long-term competitive differentiation. In May 2022, Nexteer and Continental’s joint venture CNXMotion expanded its Brake-to-Steer (BtS) software functions, integrating safety layers applicable across EPS variants, underscoring deeper collaboration on steering/vehicle control systems. In February 2025, ZF began series production of steer-by-wire technology with Chinese OEM NIO, delivering the first production steer-by-wire systems that remove the mechanical shaft while providing redundant actuation and safety layers, a milestone for by-wire commercialization and OEM acceptance of software-centric steering.

LIST OF KEY AUTOMOTIVE ELECTRIC POWER STEERING COMPANIES PROFILED:

- JTEKT Corporation (Japan)

- Robert Bosch GmbH (Germany)

- Nexteer Automotive (U.S.)

- ZF Friedrichshafen AG (Germany)

- NSK Ltd. (Japan)

- Showa Corporation (Hitachi Astemo) (Japan)

- Thyssenkrupp AG (Germany)

- Mando Corporation (Halla Group) (South Korea)

- Hyundai Mobis Co., Ltd. (South Korea)

- Mitsubishi Electric Corporation (Japan)

- Denso Corporation (Japan)

- Valeo SA (France)

- Continental AG (Germany)

- GKN Automotive (Melrose Industries) (UK)

- KYB Corporation (Japan)

- Magna International Inc. (Canada)

- ATS Automation Tooling Systems (Canada)

- Infineon Technologies AG (Germany)

- Texas Instruments (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In October 2025, Knorr-Bremse introduced its EPS system for buses at Busworld 2025, promoting power-on-demand steering to lower energy use and CO₂ emissions in commercial vehicle fleets.

- In August 2025, FORVIA HELLA commenced series production of steering sensors for by-wire systems, rolling out three series launches with premium OEMs in Germany and China during 2025.

- In June 2025, Bosch reaffirmed its strategic alliance with startup Arnold NextG to accelerate steer-by-wire commercialization, targeting mid-decade large-scale production. The partnership combines Bosch system integration and supplier scale with Arnold’s specialized by-wire technology, creating a go-to systems route for OEMs planning software-defined steering on new EV platforms.

- In March 2025, JTEKT confirmed its next-generation steer-by-wire backup power (Libuddy) and steer-by-wire components were installed in the Lexus RZ, indicating supplier capability to meet OEM functional-safety and backup-power requirements for production BEVs with full drive-by-wire architectures.

- In May 2023, NSK formed a joint venture (49.9 % NSK / 50.1 % JIS) for its steering business, delegating management to improve steering unit competitiveness.

REPORT COVERAGE

The global automotive electric power steering market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAIL |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.57% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, By Vehicle Propulsion, By Steering Architecture, By Component, and Region |

| By Vehicle Type |

|

| By Vehicle Propulsion |

|

| By Steering Architecture |

|

|

By Component |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 33.68 billion in 2025 and is projected to reach USD 54.5 billion by 2034.

In 2025, the market value stood at USD 19.67 billion.

The market is expected to exhibit a CAGR of 5.57% during the forecast period (2026-2034).

The Rack-Assist EPS (R-EPS) segment leads the market by steering architecture.

Rising demand for fuel efficiency and emission reduction is a key factor driving EPS adoption.

Key companies such as JTEKT Corporation, Robert Bosch GmbH, Nexteer Automotive, ZF Friedrichshafen, and NSK Ltd. dominate the market.

Asia Pacific holds the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us