Coconut Water Market Size, Share & Industry Analysis, By Nature (Organic and Conventional), By Flavor (Non-Flavored and Flavored), By Packaging Type (PET Bottles, Cans, Glass Bottles, and Tetra Packs), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail / E-commerce, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

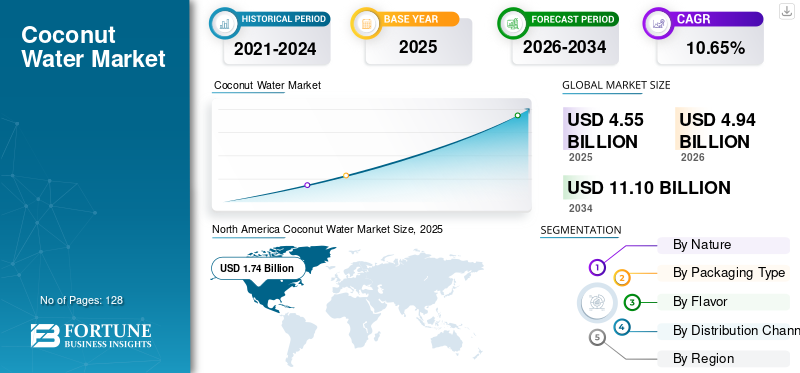

Coconut Water Market Size and Future Outlook

The global coconut water market size was valued at USD 4.55 billion in 2025. The market is projected to grow from USD 4.94 billion in 2026 to USD 11.10 billion by 2034, exhibiting a CAGR of 10.65% during the forecast period. North America dominated the coconut water market with a market share of 38.24% in 2025.

Coconut water represents a fast-expanding natural hydrating category positioned between traditional bottled water and functional beverages. Extracted from young green coconuts, it contains naturally occurring electrolytes such as potassium, sodium, magnesium, and calcium, making it widely perceived as a plant-based isotonic drink. The global coconut water market is driven by rising demand for clean-label beverages, increasing consumer preference for plant-based products, sports and fitness trends, and sugar-reduction initiatives that are replacing carbonated soft drinks with naturally sourced hydration solutions.

The global coconut water market is led by major players, including Vita Coco Company, Inc., PepsiCo, Inc. (ONE / O.N.E. Coconut Water), The Coca-Cola Company (ZICO), Thai Coconut Public Company Limited, and Celebes Coconut Corporation.

Download Free sample to learn more about this report.

Coconut Water MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.55 billion

- 2026 Market Size: USD 4.94 billion

- 2034 Forecast Market Size: USD 11.10 billion

- CAGR: 10.65% from 2026–2034

- North America dominated the coconut water market with a 38.24% share in 2025.

- Conventional segment led the market with USD 3.76 billion in 2025.

- Supermarkets/hypermarkets segment led the distribution channel with USD 2.43 billion in 2025.

North American

North America held USD 1.74 billion in 2025, driven by strong plant-based beverage adoption and sports hydration demand.

Europe

Europe was valued at USD 0.81 billion in 2025, supported by rising demand for clean-label and organic beverages.

Asia Pacific

Asia Pacific reached USD 1.46 billion in 2025 and is projected to grow at the fastest CAGR globally.

U.S.

Valued at USD 1.52 billion in 2025, driven by high retail penetration and increasing imports of coconut-based beverages.

Japan

Stable demand supported by growing preference for functional and natural hydration beverages in urban consumer segments.

Read More

Coconut Water Market Trends

Rising Consumer Preference for Natural Electrolyte Beverages to Shape Industry Trends

Consumers are increasingly replacing synthetic sports drinks and high-sugar beverages with coconut water due to its natural electrolyte profile and perceived health benefits. The shift is particularly visible among millennials, Gen Z consumers, and fitness-focused urban populations who associate coconut water with clean-label, minimally processed hydration. Coconut water is widely recognized for its high potassium content and low-fat profile, positioning it as a natural alternative to artificially formulated sports drinks. The expansion of gym memberships, endurance sports participation, and wellness-driven lifestyles is structurally supporting demand.

- According to the U.S Health & Fitness Consumer Report, around 77 million Americans were members of gyms, studios, and other fitness facilities. Facilities served nearly 96 million total customers, indicating many users participate without formal membership.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Expanding Global Coconut Production and Plant-Based Beverage Adoption to Support Market Development

The growth in coconut cultivation across Southeast Asia (Indonesia, Philippines, India, Thailand) has strengthened the raw material supply base for coconut water processing. Rising global preference for plant-based beverages further accelerates category penetration in North America and Europe. Coconut-producing countries are increasing export volumes of tender coconuts and processed coconut liquids, enabling large-scale commercial bottling operations.

- According to the European Union, in 2023, more than 70% of the world's coconut-producing area is concentrated in the Philippines (29%), Indonesia (25%), and India (17%).

Market Restraints

Price Volatility and Supply Chain Concentration to Limit Market Stability

Coconut water production remains geographically concentrated in tropical regions, exposing the market to climate variability, typhoons, droughts, and crop diseases. Seasonal supply fluctuations can impact pricing and margins for global beverage brands. Additionally, coconut water requires cold-chain logistics or aseptic processing to maintain freshness, increasing processing and transportation costs compared to conventional bottled water.

- According to the Food and Agriculture Organization (FAO), drought-fueled stress, combined with aging trees, led to reports that coconut yields could fall by as much as 20% in specific, severely affected areas in 2024.

Market Opportunities

Expansion of Organic and Value-Added Coconut Water to Create Premium Revenue Streams

The organic coconut water segment is gaining traction as consumer demand for pesticide-free, sustainably sourced beverages grows. Certified organic offerings command higher price points in developed markets. Flavored coconut water variants infused with pineapple, mango, or berry extracts are expanding shelf presence and broadening consumer appeal beyond core hydration occasions.

- For instance, in February 2025, Natural Grocers launched its 100% Pure Organic Coconut Water as the newest addition to its private-label beverage line. This single-ingredient product is made from pure coconut water, with no artificial flavors, additives, preservatives, or synthetic colors.

SEGMENTATION ANALYSIS

By Nature

Conventional Segment Dominated Due to Large-Scale Sourcing and Lower Price Points

Based on nature, the market is segmented into organic and conventional coconut water.

The conventional segment dominated the global coconut water market share, valued at USD 3.76 billion in 2025, supported by strong retail penetration, lower price points, and large-scale sourcing from Southeast Asia. Conventional coconut water benefits from mass-market accessibility across supermarkets and convenience channels, particularly in North America and the Asia Pacific.

The organic segment is projected to grow at the fastest CAGR of 13.65% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Flavor

Non-Flavored Segment Led the Market Due to Natural Electrolyte Positioning and Sports Recovery

Based on flavor, the market is segmented into non-flavored and flavored.

The non-flavored segment dominated, valued at USD 3.07 billion in 2025, reflecting consumer preference for minimally processed, single-ingredient hydration. Core demand is driven by sports recovery, natural electrolyte positioning, and traditional consumption patterns.

The flavored segment is expected to grow at a CAGR of 13.51% during the forecast period, supported by innovation in tropical blends, berry infusions, and low-calorie flavor extensions targeting younger consumers and premium retail segments.

By Packaging Type

PET Bottles Led the Market Due to Lightweight Logistics and Strong Supermarket Presence

By packaging type, the market is fragmented into PET bottles, cans, glass bottles, and tetra packs.

The PET bottles segment dominated the market and was valued at USD 2.06 billion in 2025, driven by lightweight logistics, durability, and strong supermarket presence. PET remains the preferred format for single-serve consumption and impulse purchases.

The glass bottles segment is projected to grow at the fastest CAGR of 14.56% during the forecast period, supported by premium branding, sustainability perceptions, and higher-end retail positioning in Europe and North America.

By Distribution Channel

Supermarkets/Hypermarkets Dominated Due to Organized Retail Expansion and High Product Visibility

Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail/e-commerce, and others.

The supermarkets/hypermarkets segment led, valued at USD 2.43 billion in 2025, supported by organized retail expansion, bulk purchasing behavior, and high product visibility. This channel captures routine hydration purchases.

The online retail/e-commerce segment is the fastest growing, registering a CAGR of 14.53% during the forecast period, driven by subscription beverage models, direct-to-consumer strategies, and growing digital grocery adoption.

Coconut Water Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Coconut Water Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market, accounting for USD 1.74 billion in 2025, driven by strong brand penetration, plant-based beverage adoption, and sports hydration trends. The region is projected to grow at a CAGR of 8.93% during the forecast period.

U.S. Coconut Water Market

The U.S. dominates the region, valued at USD 1.52 billion in 2025, supported by high retail distribution and fitness-oriented consumption. The USDA reports increasing imports of coconut water and related coconut products from Southeast Asia, reflecting growing domestic demand.

Europe

Europe was valued at USD 0.81 billion in 2025, supported by demand for organic beverages and clean-label products. The region is projected to grow at a CAGR of 9.95% during the forecast period. The coconut water industry is experiencing rising popularity due to its appeal as a natural, low-calorie hydration option packed with electrolytes, vitamins, and minerals. This trend aligns with growing consumer demand for healthy, natural beverages and plant-based alternatives to sugary drinks amid the health and wellness boom.

Germany Coconut Water Market

Germany led the market with a value of USD 0.17 billion in 2025, driven by a strong bottled water culture and an expanding organic retail infrastructure. The market benefits from sustainability-driven packaging trends and premium beverage demand.

U.K. Coconut Water Market

The U.K. market was valued at approximately USD 0.19 billion in 2025 and is projected to grow at a CAGR of 9.13% over the forecast period, in line with Europe’s broader clean-label beverage trend. Increasing awareness of health benefits is a key driver in the market, as consumers increasingly seek natural alternatives to sugary sodas and artificial sports drinks.

Asia Pacific

Asia Pacific was valued at USD 1.46 billion in 2025 and is projected to grow at the fastest CAGR of 12.46% over the forecast period. The regional growth is supported by abundant raw material availability and rising domestic consumption, particularly in India, China, and Southeast Asia.

China Coconut Water Market

China represents the largest market in the Asia Pacific, valued at approximately USD 0.36 billion in 2025, and is projected to grow at a CAGR of 13.67% during the forecast period, outpacing the regional average.

South America and the Middle East & Africa

South America reached USD 0.38 billion in 2025, driven by Brazil’s coconut cultivation and expanding domestic beverage processing industry. The region is projected to grow at a CAGR of 10.47% during the forecast period.

The Middle East & Africa market was valued at USD 0.16 billion in 2025, growing at a CAGR of 13.89% during the forecast period, driven by high bottled beverage dependency and rising demand for premium imported coconut water brands.

UAE Coconut Water Market

The UAE market in 2025 accounted for USD 0.04 billion, supported by strong retail infrastructure, tourism-driven demand, and premium beverage consumption trends.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Organic Certifications and Sourcing to Maintain a Competitive Advantage

Key players focus on sourcing partnerships in Southeast Asia, aseptic packaging technologies, organic certifications, and retail expansion strategies to maintain a competitive advantage. Vertical integration in coconut sourcing and investment in sustainable farming practices are emerging differentiators. Brands are also increasingly innovating in the global coconut water market to cater to diverse consumer preferences, offering formats such as pure, flavored, organic, and functional blends. This strategy broadens appeal across demographics, from fitness enthusiasts to families seeking kid-friendly options.

Key Players in the Market

|

Rank |

Company Name |

|

1 |

The Vita Coco Company, Inc. |

|

2 |

PepsiCo, Inc. |

|

3 |

The Coca-Cola Company |

|

4 |

Thai Coconut Public Company Limited |

|

5 |

Celebes Coconut Corporation |

List of Key Coconut Water Companies Profiled

- The Vita Coco Company, Inc. (U.S.)

- PepsiCo, Inc. (U.S.)

- The Coca-Cola Company (U.S.)

- Thai Coconut Public Company Limited (Thailand)

- Celebes Coconut Corporation (Philippines)

- PT Pulau Sambu (Indonesia)

- Edward & Sons Trading Co., Inc. (U.S.)

- C2O Pure Coconut Water (U.S.)

- Goya Foods, Inc. (U.S.)

- GraceKennedy Group (Jamaica)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Karma Water launched its Pineapple Coconut Probiotic Water, reviving a popular 2011 flavor with added gut health benefits. This probiotic water contains 2 billion CFU of BC30 probiotics for digestive and immune support, plus 100% daily value of vitamins A, B3, B5, B6, B12, and E.

- October 2025: CocoGen, an Australian-founded functional coconut water brand, launched in Australia following a successful debut in Singapore. It positions itself as the world's first functional organic coconut water, targeting health-conscious consumers with enhanced hydration benefits.

- July 2025: Community Foods launched Bonsoy Sparkling Coconut Water in the U.K, marking it as the first sparkling variant of its kind in the market. This move taps into rising demand for low-sugar, functional hydration options amid 17% growth in the non-alcoholic drinks sector over five years.

- July 2024: Yu, an Indian omni-channel consumer food brand, entered the hydration category with the launch of 100% natural coconut water and fruit juices. This marked its second category, following instant foods, emphasizing zero preservatives, no added sugar, and no concentrates under the rebranded Yu Foods Co.

- March 2024: Indian entrepreneur Arjun Talwar launched Bervera, a premium pure coconut water brand, in the U.K, Bevera emphasizes a "Pure & Simple" tagline, offering exceptionally clean-tasting coconut water with natural electrolytes for hydration, post-workout recovery, and as a healthy mixer in cocktails or mocktails. It comes in both glass and plastic bottles to balance consumer preferences and sustainability.

REPORT COVERAGE

The global coconut water market report analyzes the market in depth and highlights key aspects, including global coconut water market trends, market dynamics, prominent companies, investment in research and development, and end-use. In addition, the report provides insights into the global coconut water market and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.65% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Nature

|

|

By Flavor

|

|

|

By Packaging Type

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 4.55 billion in 2025 and is anticipated to reach USD 11.10 billion by 2034.

At a CAGR of 10.65%, the global market will grow significantly over the forecast period.

By flavor, the non-flavored segment led the market.

North America held the largest market share in 2025.

Expanding global coconut production and plant-based beverage adoption to support market expansion.

Vita Coco Company, Inc., PepsiCo, Inc. (ONE / O.N.E. Coconut Water), the Coca-Cola Company (ZICO), Thai Coconut Public Company Limited, and Celebes Coconut Corporation are the leading companies in the market.

Rising consumer preference for natural electrolyte beverages is shaping industry trends.

- 2021-2034

- 2025

- 2021-2024

- 128

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us