Less-Than-Truckload (LTL) Market Size, Share & Industry Analysis, By Freight (General Freight, Specialized Freight, Hazardous Materials, and Temperature Controlled Freight), By Shipment Size (Light LTL, Medium LTL, and Heavy LTL), and By Mode of Transportation (Domestic LTL and International/Cross-Border LTL), By Industry (Manufacturing & Industrial Goods, Retail & E-commerce, Automotive, Food & Beverages, and Others), and Regional Forecast, 2026-2034

Less-Than-Truckload (LTL) Market Size and Future Outlook

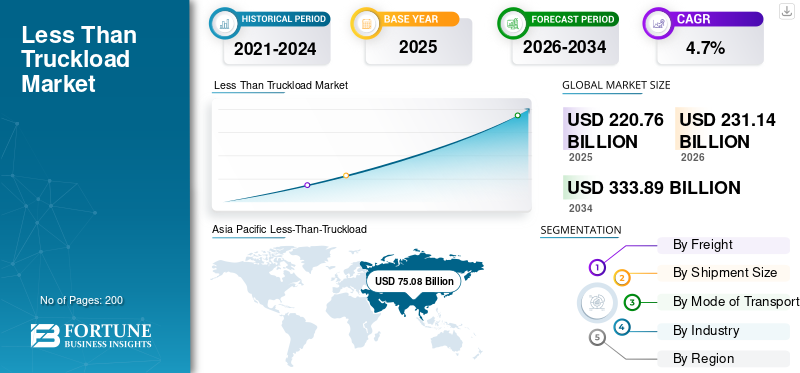

The global less-than-truckload market size was valued at USD 220.76 billion in 2025. The market is projected to grow from USD 231.14 billion in 2026 to USD 333.89 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the global less-than-truckload (LTL) market with a 34.0% market share in 2025.

The less-than-truckload (LTL) market represents freight services that consolidate multiple smaller shipments into shared trucks, enabling cost-efficient regional and long-distance transport. Over the next several years, the market is expected to evolve through wider adoption of digital freight platforms, denser distribution networks, and greater use of data-driven routing. Demand will be supported by steady e-commerce expansion, rising expectations for predictable delivery timelines, and growing interest in sustainable transport solutions. Investments in automation, real-time tracking, and cross-border connectivity will further strengthen competitiveness, positioning LTL carriers to handle increasing shipment volumes with improved speed, transparency, and operational efficiency.

Key players in the market include Old Dominion Freight Line, FedEx, DSV, XPO Inc., DACHSER, and Kuehne+Nagel. Leading carriers are strengthening their positions through targeted terminal expansions, disciplined pricing, and technology that improves visibility and load planning. Many are investing in automated docks, advanced telematics, and data-driven routing to cut dwell time and boost on-time performance. Others are widening their portfolios with expedited, cross-border, and customized solutions to secure higher-margin freight. Strategic acquisitions, selective fleet modernization, and sustainability initiatives also shape the landscape, helping carriers differentiate while responding to shippers’ expectations for speed, transparency, and consistent service quality.

Download Free sample to learn more about this report.

Less-Than-Truckload (LTL) Market KEY TAKEAWAYS

- 2025 Market Size: USD 220.76 Billion

- 2026 Market Size: USD 231.14 Billion

- 2034 Forecast Market Size: USD 333.89 Billion

- CAGR: 4.7% from 2026–2034

- Asia Pacific dominated the global less-than-truckload (LTL) market with a 34.0% share in 2025.

- The general freight segment holds the largest market share during the forecast period.

- The medium LTL segment is expected to dominate the market.

Asia Pacific

Asia Pacific leads growth with manufacturing, e-commerce, and logistics expansion.

North America

North America holds the second-largest share, driven by e-commerce growth, manufacturing activity, and cross-border trade.

Europe

Europe is expected to grow steadily, driven by intra-EU trade, e-commerce expansion, and logistics investments.

U.S.

E-commerce, JIT manufacturing, regional distribution, and trade drive LTL market growth.

Japan

Logistics networks, e-commerce shipments, and freight demand support LTL growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Expansion of E-Commerce to Propel LTL Market Growth

The rapid rise of e-commerce continues to push more mid-sized shipments into LTL networks, creating steady demand for carriers that can handle frequent, time-sensitive last-mile deliveries. As online retailers face growing shipment volumes and fluctuating order sizes, LTL providers benefit from overflow freight that doesn’t fit traditional parcel networks. Carriers with dense regional terminals, strong last-mile partnerships, and reliable transit times are especially well-positioned. This trend is reinforced by consumer expectations for faster, timely deliveries and retailers’ desire to optimize logistics costs. Together, these factors make e-commerce growth a lasting driver of LTL demand across both domestic and cross-border routes.

MARKET RESTRAINTS

Rising Operating Costs and Network Inefficiencies May Restrain Market Growth

A major restraint in the LTL market is the steady increase in operating costs, particularly for labor, fuel, and equipment. As LTL networks rely on numerous handling points and coordinated transfers, any inefficiency, such as dock congestion, driver shortages, or aging terminal infrastructure, can erode margins quickly. Carriers must also reduce costs from compliance, maintenance, and insurance, which limits pricing flexibility in competitive lanes. These pressures make it challenging for smaller or under-capitalized operators to sustain service quality. As expenses climb faster than freight rates in some regions, the overall profitability of LTL operations can tighten, slowing investment and network expansion.

MARKET OPPORTUNITIES

Digitalization and Advanced Freight Visibility Solutions to Offer Lucrative Market Opportunities

A significant opportunity in the LTL market lies in deeper digital integration across the shipping lifecycle. Shippers increasingly expect real-time updates, predictive delivery windows, and transparent pricing capabilities that many carriers are still developing. Companies that invest in modern transportation management systems, automated dock operations, and AI-driven load optimization can differentiate themselves with faster planning and fewer service failures. Enhanced visibility tools also strengthen collaboration with brokers and 3PLs, opening access to higher-value freight. As supply chains prioritize data-rich partnerships, carriers that digitize their networks can improve efficiency, strengthen customer retention, and capture new business in both domestic and cross-border lanes.

Less-Than-Truckload (LTL) MARKET TRENDS

Shift Toward Regionalized and High-Density LTL Networks to Propel Market Growth

The move toward regionalized, high-density networks that emphasize faster transit times and tighter service windows is one of the significant less-than-truckload (LTL) market trends. Shippers increasingly prioritize predictable delivery over long-haul coverage, prompting carriers to expand or upgrade terminals in metropolitan clusters where freight flows are strongest. This approach supports more efficient linehaul planning, better trailer utilization, and fewer touchpoints, reducing damage rates and boosting reliability. As e-commerce and nearshoring reshape distribution patterns, carriers with strong regional footprints gain an advantage. The trend also encourages partnerships between national and regional players to create hybrid networks with broader reach and greater agility.

MARKET CHALLENGES

Balancing Capacity with Volatile Freight Demand Challenges Market Development

A key challenge in the LTL market is maintaining the right balance between available capacity and shifting shipment volumes. LTL networks are complex, and mismatches, whether sudden surges or unexpected slowdowns, can quickly strain terminals, linehaul schedules, and labor resources. Overcapacity leads to underutilized assets and margin pressure, while tight capacity causes service delays and missed pickups. Seasonal spikes, economic uncertainty, and disruptions in adjacent modes add further unpredictability. Carriers must continuously adjust staffing, routing, and equipment allocation, which requires strong forecasting tools and disciplined operations. Achieving this balance is essential to delivering consistent service without eroding profitability.

Download Free sample to learn more about this report.

Segmentation Analysis

By Freight

Cost-Effective Transportation for Mixed-Size Shipment Boosts General Freight Segment Growth

Based on freight, the market is divided into general freight, specialized freight, hazardous materials (HazMat), and temperature-controlled freight.

General freight holds the largest market share during the forecast period. General freight in the LTL market is growing as companies seek dependable, cost-effective transport for routine, mixed-size LTL shipments. Demand is lifted by steady manufacturing output, expanding regional distribution networks, and rising shipment frequency among small and mid-sized businesses. Enhanced routing technology, improved freight consolidation, and stronger service reliability also attract shippers. These elements collectively reinforce the steady rise of general freight volumes across multiple industries and geographies.

The temperature-controlled freight is expected to grow at the fastest CAGR during the forecast period. Growth in cold-chain distribution, stricter product-handling standards, and expanding regional fulfillment networks all support this segment. Companies increasingly rely on LTL providers with validated equipment, real-time monitoring, and consistent transit performance, making temperature-controlled services essential for safeguarding product quality across shorter, more frequent shipments.

By Shipment Size

Strong Replenishment Cycles to Influence the Growth of the Medium LTL Segment

In terms of shipment size, the market is divided into light LTL, medium LTL, and heavy LTL.

The medium LTL segment is expected to dominate the market as businesses move more mid-sized, palletized freight that falls between parcel and heavy-haul categories. Steady industrial activity, growing replenishment cycles, and tighter delivery windows encourage shippers to choose reliable mid-range LTL services. Improved consolidation practices, regional network expansion, and better tracking tools further support adoption. These factors collectively make medium LTL an efficient option for routine, time-sensitive shipments across diverse industries.

The heavy LTL segment is expected to exhibit a high CAGR during the forecast period. Growth in construction, machinery, and large consumer goods production supports demand, while shippers seek predictable transit times and cost efficiency for oversized freight. Enhanced terminal handling, specialized equipment, and improved network density also make volume LTL more practical, strengthening adoption across domestic and regional corridors.

By Mode of Transportation

Expanding E-Commerce Activity to Drive the Growth of the Domestic LTL Segment

By mode of transportation, the market is categorized into domestic LTL and international/cross-border LTL.

The domestic LTL segment dominates the market as businesses prioritize frequent, smaller shipments to support regional distribution and tighter inventory cycles. Expanding e-commerce activity, steady manufacturing output, and growing demand for reliable mid-distance transport all contribute to this momentum. Carriers’ investments in denser terminal networks, improved routing technology, and faster transit times further encourage shippers to use domestic LTL. Together, these factors strengthen the segment’s role in modern supply chains.

The international/cross-border LTL segment will grow at the highest CAGR during the forecast period. Companies shipping smaller, frequent loads seek reliable transit, transparent customs processes, and predictable costs, needs well served by specialized LTL carriers. Growth in nearshoring, stronger trade corridors, and improved digital documentation also support smoother cross-border flows. These elements collectively boost demand for cross-border LTL services across North America, Europe, and Asia.

To know how our report can help streamline your business, Speak to Analyst

By Industry

Increasing Reliance on LTL Services to Bolster the Growth of the Manufacturing & Industrial Goods Segment

On the basis of industry, the market is divided into manufacturing & industrial goods, retail & e-commerce, automotive, food & beverages, and others.

The manufacturing & industrial goods segment is expected to dominate the market. Manufacturing and industrial goods increasingly rely on LTL services as firms adopt leaner inventory models and require frequent, palletized shipments to plants and distribution centers. Steady production activity, expanding regional supply chains, and the need for dependable mid-distance transport all fuel demand. Enhanced network density, better consolidation practices, and improved tracking tools also strengthen LTL’s appeal.

The retail & e-commerce segment will grow at a rapid CAGR during the forecast period. Rising online sales, shorter delivery cycles, and the need for dependable regional distribution all strengthen this segment. Carriers offering dense terminal networks, fast transit times, and real-time visibility attract retailers seeking consistency. Together, these dynamics make LTL a preferred mode for managing diverse and rapidly moving merchandise.

Less-Than-Truckload (LTL) Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific captured the largest less-than-truckload market share in 2025 and will grow at the highest CAGR within the forecast period. The market is expanding as regional manufacturing sectors strengthen and cross-border trade within ASEAN countries accelerates. Rising e-commerce penetration, especially in China, India, and Southeast Asia, is generating frequent mid-sized shipments that fit well into LTL networks. Urbanization and the growth of organized retail are also increasing demand for dependable and short-haul distribution. Governments are investing heavily in highways, logistics parks, and digital customs systems, improving transit reliability. At the same time, businesses adopting lean inventories and just-in-time delivery models rely more on LTL carriers, reinforcing the segment’s steady growth across diverse industries.

Asia Pacific Less-Than-Truckload (LTL) Market Size,2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America holds the second-largest less-than-truckload market share as businesses shift toward frequent, smaller shipments to support regional distribution and tighter inventory strategies. Rising e-commerce activity, expanding retail replenishment cycles, and stable manufacturing output continue to lift demand. Investments in terminal modernization, automated sorting, and real-time tracking enhance service reliability and attract shippers seeking predictable transit times. Cross-border trade with Canada and Mexico is also increasing, supported by integrated supply chains and improved customs processes. Together, these factors strengthen the role of LTL carriers in meeting diverse domestic and cross-border freight needs across the region.

The U.S. dominates the market due to companies’ reliance on frequent, smaller shipments to support just-in-time production and regional distribution. Strong e-commerce activity continues to generate steady mid-sized freight volumes, while manufacturing and retail sectors benefit from dependable LTL networks for palletized goods. Investments in automated terminals, telematics, and digital freight platforms are improving routing efficiency and shipment visibility. Additionally, the reshoring of certain industries and rising domestic trade activity are increasing shipment density. These combined forces reinforce long-term growth opportunities for U.S. LTL carriers across diverse commercial corridors.

Europe

Europe regional LTL market will exhibit steady growth during the forecast period. Growing intra-EU trade, supported by harmonized regulations and efficient border processes, drives consistent freight movement. Expanding e-commerce activity and rising delivery expectations further increase demand for mid-sized shipments across dense urban corridors. Logistics providers are investing in advanced routing tools, cross-border hubs, and sustainable fleet upgrades to enhance reliability and meet environmental requirements. These developments collectively strengthen LTL adoption across manufacturing, retail, and distribution sectors throughout the region.

Rest of the World

The less-than-truckload market growth in the Rest of the World, including Latin America and the Middle East & Africa, is driven by the expansion of trade corridors and regional economies. Rising urbanization, development of retail networks, and increasing demand for frequent, smaller shipments are strengthening reliance on LTL services. Major infrastructure investments such as new logistics parks, highways, and port expansions are improving connectivity and shortening transit times. As businesses adopt more flexible distribution models, LTL providers benefit from greater shipment frequency across domestic and cross-border routes in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Shortening of Transit Times and Use of Collaborative toShorten Transit Times

The presence of major players, including Old Dominion Freight Line, FedEx, DSV, XPO Inc., DACHSER, and Kuehne+Nagel, characterizes the competitive landscape. Leading players invest heavily in terminal upgrades, automated handling systems, and data-driven routing to shorten transit times and reduce service variability. Strategic acquisitions are also common, helping carriers expand geographic coverage, strengthen sector-specific capabilities, and diversify freight mixes. Many providers are modernizing fleets to improve fuel efficiency and align with sustainability goals, further enhancing their competitive positioning.

To differentiate themselves, carriers increasingly emphasize real-time visibility, digital booking platforms, and collaborative tools that streamline communication with shippers and logistics partners. Some operators build specialized solutions such as temperature-controlled LTL, expedited lanes, or cross-border consolidation to capture higher-margin segments. Others focus on disciplined pricing, density management, and targeted terminal expansion to maintain profitability. Together, these strategies create a dynamic competitive environment shaped by continuous investment, service innovation, and network optimization.

LIST OF KEY LESS-THAN-TRUCKLOAD COMPANIES PROFILED

- Old Dominion Freight Line (U.S.)

- FedEx (U.S.)

- DSV (Denmark)

- Kuehne+Nagel (Switzerland)

- Transport Corporation of India Ltd. (India)

- XPO Inc. (U.S.)

- Estes Express Lines (U.S.)

- R+L Carriers Inc. (U.S.)

- AAA Cooper Transportation (U.S.)

- DACHSER (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025- Knight-Swift Transportation announced the consolidation of its subsidiary LTL carriers into a unified national LTL brand, a strategic move to streamline operations and improve coast-to-coast service coverage.

- September 2024- DSV completed the acquisition of Schenker, the logistics division of Deutsche Bahn, thereby creating one of the world’s largest integrated logistics companies.

- August 2024- Saia Inc. expanded its footprint with six new terminal openings across the Western U.S.

- June 2025- Warp announced nationwide expansion of the LTL model. This would help modern shippers to avoid delayed deliveries, damage, freight fragmentation, and terminal pricing.

- September 2025- Dayton Freight Lines expanded its network by relocating and enlarging a terminal in Illinois, reflecting the carrier's efforts to grow capacity and improve service coverage even during a weak freight cycle.

REPORT COVERAGE

The global less-than-truckload market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Freight

By Shipment Size

By Mode of Transportation

By Industry

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 220.76 billion in 2025 and is projected to reach USD 333.89 billion by 2034.

In 2025, the market value stood at USD 75.08 billion.

The market is expected to exhibit a CAGR of 4.7% during the forecast period (2026-2034).

The medium LTL segment led the market by shipment size.

Favorable trends associated with e-commerce are the key factors driving market growth.

Key players in the global less-than-truckload market include Old Dominion Freight Line, FedEx, DSV, XPO Inc., DACHSER, and Kuehne+Nagel.

Asia Pacific held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us