LNG & Gas Processing Equipment Market Size, Share & Industry Analysis, By Equipment Type (Gas Pre-Treatment Equipment, Liquefaction Equipment, Storage Equipment, Regasification Equipment, and Others), By Process Stage (Upstream Gas Processing, Midstream LNG Infrastructure, and Downstream Regasification & Distribution), By Application (Onshore LNG Terminals, Offshore LNG (FLNG & FSRU), Gas Processing Plants, and Small-Scale LNG Plants), and Regional Forecast, 2026 – 2034

LNG & Gas Processing Equipment Market Size and Future Outlook

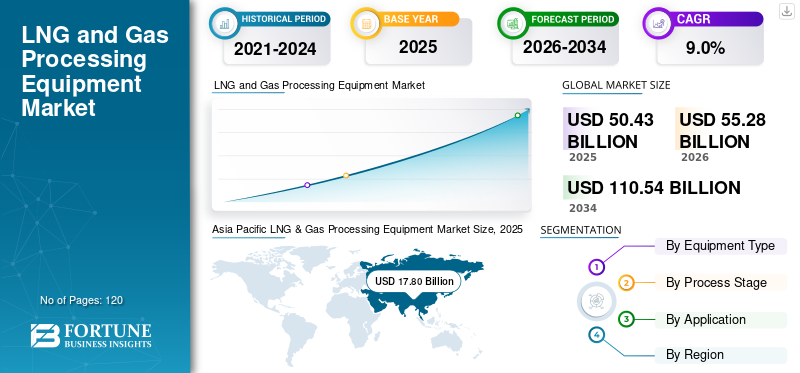

The global LNG & gas processing equipment market size was valued at USD 50.43 billion in 2025. The market is projected to grow from USD 55.28 billion in 2026 to USD 110.54 billion by 2034, exhibiting a CAGR of 9.0% during the forecast period. Asia Pacific dominated the LNG & gas processing equipment market with a market share of 35.29% in 2025.

LNG & gas processing equipment includes systems used for gas pre-treatment, liquefaction, storage, regasification, and transportation across the natural gas value chain. These systems are essential for converting natural gas into LNG, enabling efficient storage, transport, and distribution across global markets.

The market is witnessing strong growth driven by rising global energy demand, increasing LNG trade, and the transition toward cleaner fuels. LNG is increasingly being adopted as a transition fuel due to its lower carbon emissions compared to coal and oil. In addition, geopolitical shifts and energy security concerns are accelerating investments in LNG infrastructure, including liquefaction terminals, regasification units, and gas processing facilities.

Major players such as Air Products and Chemicals Inc., Linde plc, Baker Hughes Company, Siemens Energy AG, Chart Industries Inc., Technip Energies N.V., Honeywell International Inc., Mitsubishi Heavy Industries, Wärtsilä Corporation, and McDermott International are actively expanding LNG equipment portfolios.

- For instance, in November 2023, Baker Hughes secured a contract to supply liquefaction technology for Venture Global’s LNG projects in the U.S., strengthening its presence in LNG infrastructure development.

Download Free sample to learn more about this report.

LNG & GAS PROCESSING EQUIPMENT MARKET TRENDS

Expansion of LNG Infrastructure and Floating LNG Solutions Pose as Key Trends

A key trend shaping the market is the increasing development of LNG terminals and floating LNG (FLNG) solutions to support flexible gas supply chains. Offshore LNG infrastructure is gaining traction due to its ability to monetize remote gas reserves. Additionally, technological advancements in liquefaction efficiency and modular LNG systems are enhancing project feasibility and reducing operational costs.

- For instance, in 2024, Technip Energies was awarded contracts for multiple LNG projects globally, focusing on modular liquefaction solutions.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising LNG Demand and Energy Transition Driving Market Growth

The increasing global demand for cleaner energy sources is driving LNG adoption across power generation, industrial, and transportation sectors. LNG plays a key role in reducing carbon emissions while ensuring energy security. Additionally, rising cross-border LNG trade and expansion of import/export terminals are significantly boosting equipment demand.

- For instance, in 2024, QatarEnergy continued expansion of its North Field LNG project, driving large-scale demand for liquefaction and processing equipment.

MARKET RESTRAINTS

High Capital Costs and Project Complexity Limiting Market Expansion

LNG infrastructure projects require substantial capital investment and long development timelines. Equipment such as liquefaction systems and storage tanks involve high engineering complexity. Moreover, fluctuations in natural gas prices and regulatory uncertainties may impact investment decisions.

- For instance, in July 2024, ExxonMobil and its partners reported cost escalation concerns in the Mozambique LNG project, where rising construction costs, security-related delays, and supply chain disruptions significantly impacted project timelines and overall capital expenditure.

MARKET OPPORTUNITIES

Growth in Floating LNG and Small-Scale LNG Creating New Opportunities

The development of floating LNG (FLNG) and small-scale LNG plants is opening new avenues for global LNG & gas processing equipment market growth. These solutions enable gas processing in remote and offshore locations. Increasing adoption of LNG in marine fuel and heavy transport sectors further supports equipment demand.

- For instance, in 2024, Wärtsilä expanded its LNG solutions for marine and small-scale applications, strengthening its position in emerging LNG markets.

Segmentation Analysis

By Equipment Type

Liquefaction Equipment Dominates Due to Core Role in LNG Conversion Process

The market is segmented by equipment type into gas pre-treatment equipment, liquefaction equipment, storage equipment, regasification equipment, and others.

The liquefaction equipment segment holds the highest market share, as it is the most critical and capital-intensive component in LNG production. The increasing number of LNG export terminals and expansion of liquefaction capacity globally are significantly driving demand for this equipment.

- For instance, Air Products continues supplying large-scale LNG liquefaction technology for global LNG projects, supporting market dominance.

The regasification equipment segment is expected to register the highest CAGR of 10.9% during 2026-2034, driven by increasing LNG import terminals and floating storage regasification units (FSRUs).

By Process Stage

Midstream LNG Infrastructure Leads Due to Expanding Global LNG Supply Chains

The market is segmented by process stage into upstream gas processing, midstream LNG infrastructure, and downstream regasification & distribution.

The midstream LNG infrastructure segment holds the highest market share, as it includes liquefaction plants, storage facilities, and transportation systems that form the backbone of LNG trade. Increasing investments in LNG export/import infrastructure are driving segment growth.

- For instance, multiple LNG export terminal projects in the U.S. and Qatar are boosting midstream infrastructure demand.

The midstream LNG infrastructure segment is also expected to register the highest CAGR of 9.8% during 2026-2034, supported by rising global LNG trade.

To know how our report can help streamline your business, Speak to Analyst

By Application

Onshore LNG Terminals Dominate Due to Large-Scale Infrastructure Investments

The market is segmented by application into onshore LNG terminals, offshore LNG (FLNG & FSRU), gas processing plants, small-scale LNG plants, and others.

The onshore LNG terminals segment holds the highest market share, as large-scale liquefaction and regasification facilities are essential for global LNG trade. Increasing demand for energy security and supply diversification is driving investments in onshore infrastructure.

- For instance, ExxonMobil and QatarEnergy continue expanding large-scale LNG terminal projects globally, reinforcing demand.

The offshore LNG (FLNG & FSRU) segment is expected to register the highest CAGR of 11.4% during 2026-2034, driven by increasing adoption of flexible and cost-efficient LNG solutions.

LNG & Gas Processing Equipment Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific LNG & Gas Processing Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the highest LNG & gas processing equipment market share and is expected to register the highest CAGR during the forecast period. The region is the largest LNG importer, with countries such as China, Japan, and India heavily investing in regasification terminals and gas infrastructure. Rapid industrialization and energy demand growth are driving LNG adoption across power and industrial sectors.

Additionally, government initiatives promoting cleaner fuels and diversification of energy sources are accelerating infrastructure development across the region.

Japan LNG & Gas Processing Equipment Market

Japan’s market in 2026 is estimated at around USD 3.66 billion, representing approximately 6.6% of global revenues. As one of the largest LNG importers, Japan relies heavily on regasification infrastructure. Continuous upgrades of LNG terminals and focus on energy security are supporting equipment demand.

China LNG & Gas Processing Equipment Market

China’s market in 2026 is estimated at around USD 6.65 billion, representing approximately 12.0% of global revenues. Rapid industrial growth and increasing LNG imports are driving demand for regasification and processing equipment. Government investments in gas infrastructure and pipeline networks are further strengthening market growth.

India LNG & Gas Processing Equipment Market

India’s market in 2026 is estimated at around USD 3.53 billion, representing approximately 6.4% of global revenues. Expanding LNG terminal capacity and rising gas consumption are driving equipment demand. Government initiatives to increase the share of natural gas in the energy mix are further boosting growth.

North America

North America represents a major LNG exporting region, driven by shale gas production and large-scale liquefaction projects in the U.S. The region is witnessing strong investments in export terminals and midstream infrastructure.

Additionally, increasing global demand for LNG exports is strengthening equipment demand across the value chain.

U.S. LNG & Gas Processing Equipment Market

The U.S. market in 2026 is estimated at around USD 10.47 billion, representing approximately 18.9% of global revenues. Expansion of LNG export terminals and shale gas production is driving market growth. Advanced liquefaction technologies and infrastructure investments further support demand.

Europe

Europe is rapidly expanding LNG infrastructure to reduce dependence on pipeline gas and enhance energy security. Increasing investments in LNG import terminals and FSRUs are driving equipment demand.

U.K. LNG & Gas Processing Equipment Market

The U.K. market in 2026 is estimated at around USD 2.23 billion, representing approximately 4.0% of global revenues. Established LNG infrastructure and continued investments in energy security support demand. Upgrades of existing terminals are further boosting equipment requirements.

Germany LNG & Gas Processing Equipment Market

Germany’s market in 2026 is estimated at around USD 2.66 billion, representing approximately 4.8% of global revenues. Expansion of LNG import terminals is driving demand for regasification equipment. Energy diversification strategies are further supporting market growth.

South America and Middle East & Africa

Both these regions are witnessing increasing investments in LNG export projects and gas monetization strategies. The Middle East, particularly Qatar and the GCC region, is a major LNG exporter, while South America is gradually expanding LNG infrastructure.

Additionally, rising demand for cleaner fuels and energy diversification are supporting long-term growth across these regions.

GCC LNG & Gas Processing Equipment Market

The GCC market in 2026 is estimated at around USD 4.84 billion, representing approximately 8.8% of global revenues. Large-scale LNG export projects and gas processing investments are driving equipment demand. Expansion of mega LNG projects in Qatar and UAE further strengthens market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Large-Scale Project Execution Strengthening Competitive Positioning

The LNG & gas processing equipment market is highly competitive, with leading players focusing on technological advancements in liquefaction, storage, and regasification systems. Companies are investing in modular LNG solutions, floating LNG systems, and energy-efficient technologies to enhance competitiveness. Strategic partnerships and participation in large-scale LNG projects remain key differentiators in the market.

LIST OF KEY LNG & GAS PROCESSING EQUIPMENT COMPANIES PROFILED

- Air Products and Chemicals Inc. (U.S.)

- Linde plc (Ireland)

- Baker Hughes Company (U.S.)

- Siemens Energy AG (Germany)

- Chart Industries Inc. (U.S.)

- Technip Energies N.V. (France)

- Honeywell International Inc. (U.S.)

- Mitsubishi Heavy Industries (Japan)

- Wärtsilä Corporation (Finland)

- McDermott International (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Technip Energies was awarded a major EPC contract for a new LNG liquefaction facility in the Middle East, including deployment of modular liquefaction technologies aimed at improving efficiency and reducing emissions.

- January 2025: Baker Hughes Company secured multiple contracts to supply gas turbine and liquefaction solutions for LNG projects in North America and the Middle East, supporting global LNG capacity expansion.

- October 2024: Air Products and Chemicals Inc. announced its participation in a large-scale LNG project in the U.S., supplying cryogenic equipment and liquefaction technology for high-capacity LNG production.

- July 2024: Chart Industries Inc. expanded its LNG equipment manufacturing capacity in the U.S. to support growing demand for storage and transport systems in LNG infrastructure projects.

- March 2024: Siemens Energy AG signed agreements to supply compression and energy solutions for LNG projects in Asia and Europe, supporting midstream infrastructure development.

REPORT COVERAGE

The global LNG & gas processing equipment market analysis includes a comprehensive study of market size & forecast across all key segments included in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence physiotherapy equipment market growth over the forecast period. The report also covers technological advancements, product innovation, regulatory considerations, and key strategic developments such as partnerships and acquisitions. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Equipment Type, Process Stage, Application, and Region |

| By Equipment Type |

|

| By Process Stage |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 50.43 billion in 2025 and is projected to reach USD 110.54 billion by 2034.

In 2025, the market value stood at USD 17.80 billion.

The market is expected to exhibit a CAGR of 9.0% during the forecast period.

By application, the onshore LNG terminals segment is expected to lead the market.

The rising LNG demand and energy transition are the key factor driving the market growth.

Air Products and Chemicals Inc., Linde plc, Baker Hughes Company, and Siemens Energy AG are among the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us