Floating LNG (FLNG) Market Size, Share & Industry Analysis, By Component (Liquefaction Infrastructure, Upstream Offshore Infrastructure, Marine & LNG Logistics, and Operations & Maintenance (O&M) Services), By Deployment Type (Newbuild FLNG Facilities, Converted FLNG Units, and Modular FLNG), By Water Depth (Shallow Water, Deepwater, and Ultra-Deepwater), and Regional Forecast, 2026-2034

Floating Liquified Natural Gas Market Overview

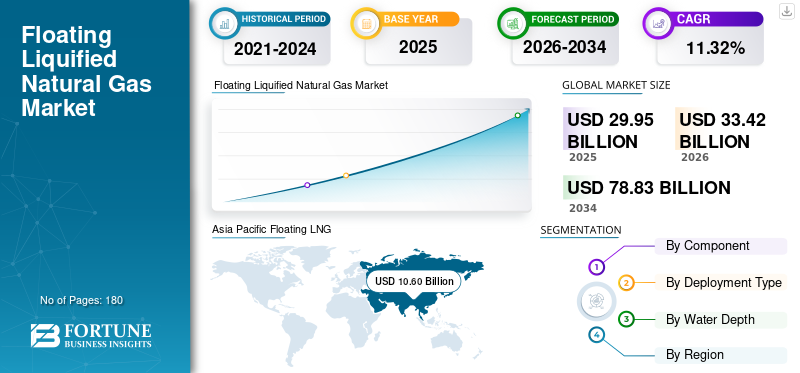

The global floating LNG (FLNG) market size was valued at USD 29.95 billion in 2025 and is expected to reach USD 33.42 billion by 2026. The market is projected to reach USD 78.83 billion by 2034, with a CAGR of 11.32% over 2026-2034. Asia Pacific dominated the floating lng market with a market share of 35.39% in 2025.

Asia Pacific is expected to dominate the market driven by energy security concerns and rising demand for cleaner energy, China, Indonesia, and Malaysia are deploying FLNG to unlock stranded offshore gas, with large-scale projects and floating regasification (FSRUs) driving development.

- The South Korean government is preparing to provide over USD 1 billion in export guarantees for Samsung Heavy Industries’ Louisiana FLNG project in the U.S., valued at USD 4.7 billion. The project will build a floating LNG plant off the Louisiana coast with an annual production capacity of 4.4 million tons. It is expected to be included as the first project under the USD 150 billion Korea-U.S. shipbuilding cooperation framework.

FLNG refers to a specialized offshore facility that processes, liquefies, stores, and offloads natural gas directly above a subsea reservoir. By integrating full-scale, land-based LNG plant functions onto a floating vessel, FLNG technology eliminates the need for long subsea pipelines to the shore and conventional land-based LNG terminals, making it a key solution for developing remote or marginal offshore gas fields.

Shell holds a commanding position in the market, largely driven by its pioneering development of the Prelude FLNG facility, the world's largest floating offshore structure. PETRONAS and Eni S.p.A. are leading in 2026 through the rapid deployment of floating units and strategic partnerships in Southeast Asia and Africa, supported by other players such as Golar LNG, Shell, and Excelerate Energy.

Download Free sample to learn more about this report.

FLOATING LNG (FLNG) MARKET TRENDS

Shift toward Modular and Standardized FLNG Designs to Boost Market Growth

The market is witnessing a transition from complex, large-scale, first-generation facilities such as Prelude toward modular, standardized, and redeployable FLNG units. Companies are increasingly adopting smaller, cost-efficient designs that reduce construction timelines and capital intensity. This trend is driven by the need to monetize smaller offshore gas reserves and improve project economics. Standardization also enables faster replication across regions, particularly in Africa and Southeast Asia.

Additionally, modular FLNG systems allow flexibility in deployment and relocation, making them suitable for dynamic energy demand scenarios. This evolution is expected to significantly enhance scalability and accelerate global FLNG adoption.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Monetization of Stranded Offshore Gas Reserves to Boost Market Growth

A key driver is the increasing need to commercialize remote and stranded offshore gas reserves that are expensive for onshore LNG infrastructure. FLNG eliminates the requirement for extensive pipeline networks and onshore liquefaction facilities, reducing both cost and environmental footprint. With growing global demand for the natural gas market as a transition fuel, oil & gas companies are actively exploring offshore fields in deepwater and ultra-deepwater regions.

- In March 2026, Eni announced plans for a floating LNG solution for Venezuela’s large offshore Perla gas field, suggesting a FLNG vessel could be deployed after 2030 to monetize gas and enable LNG exports, leveraging the company’s previous FLNG experience in Congo and Mozambique.

FLNG provides a flexible and efficient solution for such developments, particularly in West Africa, Southeast Asia, and Latin America. This capability is significantly expanding the addressable market for offshore gas production.

MARKET RESTRAINTS

High Capital Intensity and Project Financing Complexity Restrains Market Growth

FLNG projects require substantial upfront investment, often ranging from USD 1.5–3.5 billion per mtpa, making them highly capital-intensive. The complexity of integrating liquefaction, storage, and offloading systems on a floating platform further increases engineering and construction risks. Securing financing for such large-scale offshore projects is challenging, particularly in volatile energy markets. Delays, cost overruns, and operational uncertainties—as observed in early projects—have made investors cautious. Additionally, long project development cycles and exposure to LNG price fluctuations can impact return on investment, limiting the pace of new project approvals.

MARKET OPPORTUNITIES

Expansion in Emerging Offshore Gas Regions (Africa & Latin America) is Expected to Create Lucrative Opportunities

Significant opportunities exist in emerging offshore gas hubs, particularly in Africa (Mozambique, Senegal, Nigeria, and Congo) and Latin America (Brazil, Guyana). These regions possess large untapped gas reserves located far from existing infrastructure, making FLNG an ideal development solution. Governments are increasingly supporting offshore gas monetization to boost economic growth and energy exports. Furthermore, advancements in floating technologies and declining costs are improving project feasibility. As global LNG demand continues to rise, these regions are expected to become key floating LNG (FLNG) market growth engines, offering long-term investment opportunities across the value chain.

MARKET CHALLENGES

Operational Complexity and Harsh Offshore Environment Risks Create Challenges for Market Growth

Operating FLNG facilities in offshore environments presents significant technical and operational challenges. These include exposure to extreme weather conditions, deepwater pressures, and complex mooring and offloading requirements. Maintenance and repair activities are more difficult and costly compared to onshore facilities, leading to potential downtime and reduced efficiency. Additionally, safety risks associated with handling cryogenic LNG in a confined floating structure require advanced engineering and strict regulatory compliance. Past operational disruptions in major FLNG projects highlight the importance of reliability and risk management, making operational excellence a critical challenge for market participants.

Segmentation Analysis

By Component

Upstream Offshore Dominates with Efficient Gas Exploration and Production

Based on component, the market is classified into liquefaction infrastructure, upstream offshore infrastructure, marine & LNG logistics, and operations & maintenance (O&M) services.

In 2025, the upstream offshore infrastructure segment dominated with the largest market share of 37.56%, due to its critical role in enabling efficient gas exploration, production, and initial processing at remote offshore fields. This dominance stems from FLNG's flexibility in monetizing stranded gas reserves, reducing the need for extensive onshore pipelines.

Meanwhile, liquefaction infrastructure is the fastest-growing segment with a CAGR of 12.14%, driven by surging global LNG demand, technological advancements in compact liquefaction processes, and investments in modular designs for quicker deployment.

By Deployment Type

Newbuild FLNG Facilities are Highly Preferred Due to their High-Efficiency in Deepwater Environments

Based on deployment type, the market is classified into newbuild FLNG Facilities, converted FLNG units, and modular FLNG.

In 2025, the newbuild FLNG facilities segment dominated with a market share of 56.95%, supported by its tailored design for high-efficiency liquefaction, storage, and offloading in deepwater environments. These purpose-built vessels offer superior reliability, scalability, and integration with upstream operations, attracting major investments from energy giants.

The modular FLNG sub-segment is depicting the fastest-growth over the projected timeframe with a CAGR of 13.83%, fueled by lower capital costs, faster deployment timelines, and adaptability to smaller gas fields amid rising demand for flexible LNG solutions.

To know how our report can help streamline your business, Speak to Analyst

By Water Depth

Deepwater Leads Due to infrastructure supporting large-scale projects

Based on water depth, the market is classified into shallow water, deepwater, and ultra-deepwater.

In 2025, the deepwater segment held the largest floating LNG (FLNG) market share of 48.33%, due to its proven suitability for water depths of 500-1,500 meters, where it excels in accessing vast offshore gas reserves with stable mooring and floating production storage capabilities. This leadership reflects mature technologies and infrastructure supporting large-scale projects.

The ultra-deepwater is the fastest-growing segment with a CAGR of 12.76%, propelled by advanced dynamic positioning systems, rising exploration in depths beyond 1,500 meters, and demand for untapped reserves.

Floating LNG (FLNG) Market Regional Outlook

By geography, the Market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Floating LNG (FLNG) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest share in 2025 at USD 10.60 billion, and in 2026 will hit USD 11.85 billion. The region’s market is a key global hub, driven by robust LNG demand, rising energy needs, and a strong push toward cleaner fuels. Asia Pacific benefits from extensive offshore gas resources, supportive policies, and growing reliance on imported LNG, making floating solutions attractive for quick deployment, supply flexibility, and energy security.

China Floating LNG (FLNG) Market

In 2025, China gained USD 2.20 billion, accounting for roughly 7.36% of the global revenues. China’s market is expanding rapidly as the country seeks cleaner, flexible gas supply options to support its energy transition and reduce coal dependence. Driven by rising industrial and urban demand, supportive policies, and growing offshore and regasification infrastructure, FLNG offers fast‑deploy, scalable solutions along China’s coastal belt and key import hubs.

India Floating LNG (FLNG) Market

India's market revenues were at USD 1.25 billion in 2025, representing approximately 4.17% of the global market.

Japan Floating LNG (FLNG) Market

In 2025, Japan secured USD 1.66 billion, accounting for approximately 5.53% of global revenues.

Europe

Europe was valued at USD 4.68 billion in 2025 and is growing steadily as the region prioritizes energy diversification, security, and cleaner‑fuel transition. Driven by strong regulatory support and rising demand for flexible import, floating storage and regasification solutions, FLNG infrastructure such as FSRUs and floating terminals is expanding along key coastal hubs to enhance supply resilience and grid connectivity.

Germany Floating LNG (FLNG) Market

Germany accounted for USD 0.83 billion and is projected to reach USD 0.92 billion in 2026, representing approximately 2.76% of the global revenues.

North America

North America achieved USD 3.87 billion in 2025. North America’s market is driven by extensive offshore gas resources, strong export ambitions, and advanced maritime infrastructure. Flexible FLNG solutions support faster project deployment, enhance supply security, and help integrate cleaner natural gas into regional energy systems.

U.S. Floating LNG (FLNG) Market

With North America's strong contribution and the U.S.’s dominance in the region, in 2025 the U.S. market acquired USD 2.92 billion in 2025, accounting for roughly 9.74% of the global market.

Latin America

Latin America is expected to witness moderate growth and is estimated for a market revenue of USD 3.54 billion for 2026. The region is gaining traction as countries seek flexible, cost‑effective ways to monetize offshore gas and meet rising energy demand with cleaner fuels.

Brazil Floating LNG (FLNG) Market

Brazil's market gained approximately USD 1.68 billion in 2025, accounting for a minor share of the global market.

Middle East & Africa

The Middle East & Africa accounted for a market share of 24.23% in 2025 with a revenue of USD 7.26 billion and is expected to witness significant growth during the forecast period. The Middle East & Africa market is expanding as countries leverage offshore gas reserves and floating infrastructure to boost exports, diversify energy supply, and support regional energy‑transition goals.

GCC Floating LNG (FLNG) Market

The GCC market’s valuation was at USD 2.07 billion in 2025, accounting for around 6.93% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Players are focused on Various Growth Strategies to Gain Market Share

The global market is consolidated, featuring a mix of major global players and numerous regional players. Few top names include Shell plc, PETRONAS, and Eni S.p.A. among others. For instance, in September 2024, Exmar has secured the FLNG marine operations and predictive maintenance role for Cedar LNG’s hydro‑powered floating LNG project in Kitimat, British Columbia, supporting the world’s first Indigenous‑majority‑owned, low‑carbon‑intensity LNG facility powered largely by renewable electricity.

LIST OF KEY FLOATING LNG (FLNG) COMPANIES PROFILED

- Shell plc (U.K.)

- PETRONAS (Malaysia)

- Eni S.p.A. (Italy)

- Exmar NV (Belgium)

- Technip Energies (France)

- Samsung Heavy Industries (South Korea)

- Hyundai Heavy Industries (South Korea)

- Daewoo Shipbuilding & Marine Engineering (Hanwha Ocean) (South Korea)

- SBM Offshore (Netherlands)

- Saipem S.p.A. (Italy)

- Baker Hughes Company (U.S.)

- Black & Veatch (U.S.)

- MODEC, Inc. (Japan)

- JGC Holdings Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Exmar awarded the FLNG marine operations and maintenance contract for Cedar LNG’s unit megúgu in Kitimat, British Columbia, supporting the world’s first Indigenous‑majority‑owned LNG facility during construction, pre‑operations and onward operations.

- January 2026: Eni and its partners have launched the Coral North FLNG hull in South Korea, marking a major milestone for the Mozambique offshore gas project. The new state‑of‑the‑art floating LNG facility will unlock the northern Coral reservoir, significantly boosting Mozambique’s LNG output and economic impact.

- January 2026: The Coral Norte FLNG project successfully launched its hull in South Korea, marking a key milestone toward the integration of topside modules for Mozambique’s second floating LNG facility, which will monetize gas from the Rovuma Basin and support regional energy development.

- January 2026: Samsung Heavy Industries successfully launched the Coral North FLNG hull for Eni’s Mozambique project, marking a major construction milestone for the second floating LNG unit in the Rovuma Basin, set to significantly expand regional LNG output.

- January 2026: Wison New Energies has launched the Genting FLNG hull at its Nantong yard in China, marking completion of the hull phase and moving the project into topsides integration and system installation ahead of deployment offshore West Papua as Indonesia’s first floating LNG unit.

REPORT COVERAGE

The global floating LNG (FLNG) market analysis provides an in-depth study of the market size & forecast by all the segments included in the report. It contains details on the market dynamics and industry trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The report also encompasses a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Market Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.32% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment Type, Water Depth, and Region |

| By Component |

|

| By Deployment Type |

|

| By Water Depth |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 29.95 billion in 2025 and is projected to reach USD 78.83 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 10.60 billion.

The market is expected to exhibit a CAGR of 11.32% during the forecast period of 2026-2034.

The deepwater sub-segment led on the basis of water depth.

Rising demand for monetization of stranded offshore gas reserves drive market growth.

Shell plc, PETRONAS, and Eni S.p.A, are some of the prominent players.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us