Low-Cost Attritable Aircraft (LCAA) Market Size, Share & Industry Analysis, By Weight Class (Small (Less than 1,500 kg MTOW), Medium (1,500–4,500 kg MTOW), and Large (More than 4,500 kg MTOW)), By Application (Intelligence, Surveillance & Reconnaissance (ISR), Strike & Offensive Effects, Electronic Warfare, Decoy & Saturation Operations, & Others), By Autonomy Level (Remote Piloted, Mission Autonomy, & High Autonomy), By Range (Short, Medium Large Range (Less than 500 km, 500 km to 1,500 km & More than 1,500 km)), By End User (Army, Navy, & Airforce), and Regional Forecast, 2026-2034

Low-cost Attritable Aircraft Market Size and Future Outlook

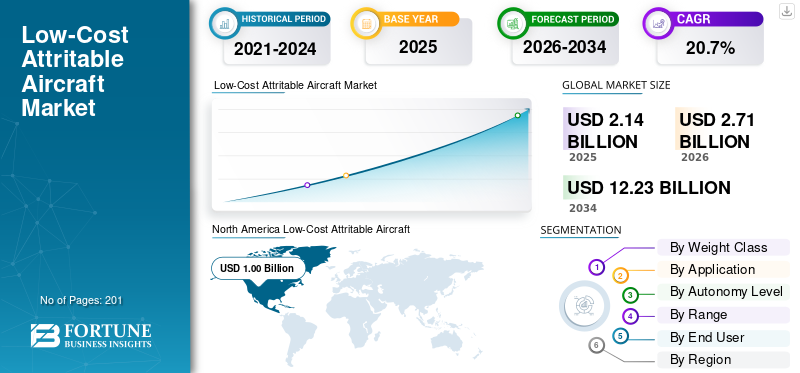

The low-cost attritable aircraft market (LCAA) size was valued at USD 2.14 billion in 2025. The market is projected to grow from USD 2.71 billion in 2026 to USD 12.23 billion by 2034, exhibiting a CAGR of 20.7% during the forecast period. North America dominated the low-cost attritable aircraft market with a market share of 46.73% in 2025.

Low-cost attritable aircraft are expendable, unmanned aerial vehicles designed for affordability and mass production, enabling deployment in high-risk environments where losses are acceptable. Their primary applications include intelligence, surveillance, reconnaissance (ISR), electronic warfare, strike missions, and swarm operations to overpower adversaries while protecting high-value assets. The global market is experiencing strong growth, driven by increasing demand for collaborative combat aircraft systems, rising geopolitical tensions necessitating swarm tactics and force multiplication, and the proliferation of autonomous unmanned systems across air forces for high-risk missions.

- For instance, in December 2025, the U.S. Air Force designated Northrop Grumman's Project Talon as the YFQ-48A LAAC under the Collaborative Combat Aircraft (CCA) program, advancing designs for autonomous wingman capabilities paired with NGAD and F-35 platforms.

Prominent players such as Lockheed Martin Corporation, Northrop Grumman, General Atomics, Kratos Defense & Security Solutions, and Boeing are focused on innovations such as modular open architectures for rapid upgrades, low-observable composites for survivability, and AI-driven autonomy for swarm operations.

Download Free sample to learn more about this report.

LOW-COST ATTRITABLE AIRCRAFT MARKET TRENDS

Autonomy and AI Integration is a Prominent Trend Observed in Market

The shift toward modular autonomy and AI-driven swarm capabilities is accelerating in LAAC platform for air forces and unmanned operations, driven by surging demand for rapid deployment in contested airspace, enhanced force multiplication through manned-unmanned teaming, scalable production for attritional losses, and seamless integration with next-generation fighters such as NGAD and F-35. Defense forces collaborate with major aircraft manufacturers for the development of low cost attritable aircraft technology to fly alongside manned jets for tasks including reconnaissance, electronic warfare, strikes, or decoys.

- For instance, in January 2020, US Air Force awards USD 400 million contracts to Boeing, General Atomics, Kratos, and Northrop Grumman for Skyborg program to develop AI-enabled "loyal wingman" attritable aircraft. These autonomous, low-cost UAVs aim to generate massed combat power for manned-unmanned teaming.

Impact of Russia Ukraine War

Russia Ukraine War Surged the Adoption of Attritable Drone Strategies in High-Intensity Conflict

The Russia-Ukraine war significantly strengthens the LCAA market by validating attritable drone strategies in high-intensity conflict. Ukraine's use of inexpensive UAVs for reconnaissance, strikes, and swarm operations has accelerated U.S. DoD prioritization of LCAA programs such as Collaborative Combat Aircraft (CCA).

- For instance, in July 2025, a new U.K.-Ukraine joint venture, Skyeton Prevail Solutions, formed between Prevail Partners and Skyeton to scale production of the proven Raybird UAS for U.K. and NATO forces. The low-cost, attritable drone NATO Class 1 has 28-hour endurance, ISR capabilities, and up to 2,500km range.

Geopolitical tensions increase the demand for disposable platforms, enabling manned forces protected by autonomous cost-effective advanced aircrafts in contested airspace.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increase in Demand for Attrition-Tolerant Systems in Modern Warfare to Drive Market Growth

The escalating demand for attrition-tolerant systems in modern warfare is propelling market growth for LAAC technologies. High-threat environments dominated by advanced air defenses and peer-level threats expose traditional high-value manned platforms to unsustainable losses, necessitating affordable expendable unmanned systems. These systems enable deployment of large swarms in roles such as intelligence, surveillance, reconnaissance, electronic warfare, suppression of defenses, and decoy operations, preserving expensive assets while overwhelming adversaries through sheer numbers. Modular chassis designs facilitate rapid variant development and manufacturing, complemented by AI-driven autonomy for collaborative tactics alongside manned forces.

MARKET RESTRAINTS

Regulatory Export Controls to Limit Market Expansion

One key restraint for the market industry is stringent export regulations such as ITAR and EAR, which classify advanced UAV tech as sensitive defense articles. These rules require extensive licensing for any international transfer, often taking months or years, delaying deals and increasing costs. The development of such aircrafts face hurdles shipping components from without waivers, risking proliferation to adversaries. Smaller innovators face de-facto bans on exports without state/commerce exemptions which restrains the market growth.

MARKET OPPORTUNITIES

Rise in Defense Budget and Expansion of Low-Cost Development Programs Presents Market Growth Opportunities

Rising global defense budgets along with expanded LAAC programs, represent a significant growth opportunity for the market. U.S. DoD FY2026 funding exceeds USD 850 billion overall, with dedicated autonomy and unmanned systems lines reaching USD 13.4 billion, a first-time standalone category including USD 9.4 billion for aerial vehicles to counter threats.

This supports low-cost initiatives such as the USAF's Low Cost Attritable Strike Demonstration (LCASD), yielding platforms such as Kratos' XQ-58A Valkyrie for swarm tactics, opening pathways for joint ventures and collaborations for attritable expendable aircraft manufacturing, which is expected to present significant opportunities for market growth.

MARKET CHALLENGES

Supply Chain Vulnerabilities Act as a Challenge for Market Growth

A critical market challenge is persistent supply chain disruptions, which undermine the low-cost, high-volume production model essential for scalability. Shortages of specialized components such as semiconductors, composites, and propulsion systems have delayed prototypes such as the XQ-58A Valkyrie and inflated costs creating challenges for the market growth.

Segmentation Analysis

By Weight Class

Geopolitical Demands for Attritable Force Multipliers Propels Medium Weight Class LCAA Segmental Growth

Based on the weight class, the market is divided into small (less than 1,500 kg MTOW), medium (1,500–4,500 kg MTOW), and large (More than 4,500 kg MTOW).

Medium (1,500–4,500 kg MTOW) segment is anticipated to account for the largest Low-Cost Attritable Aircraft (LCAA) market share over the forecast period. The medium (1,500–4,500 kg MTOW) segment leads market due to optimal balance of payload capacity, range, and production scalability for Collaborative Combat Aircraft (CCA) roles. Geopolitical demands for attritable force multipliers drive rapid market expansion, as medium MTOW supports swarm lethality without high-end costs.

- For instance, in January 2026, Northrop Grumman secured contract to integrate autonomous Prism software, sensors, and expand production of Kratos' XQ-58 Valkyrie for USMC MUX TACAIR "loyal wingman" program. The low-cost, risk-worthy UAV featuring short takeoff, 3,000nm range enhances F-35B operations in Indo-Pacific against China.

Therefore, increase in DoD budget accelerate the development of medium MTOW platforms for EW, strikes, and ISR application.

Large (more than 4,500 kg MTOW) segment is anticipated to rise with a steady growth rate with a CAGR of 16.7% over the forecast period.

By Application

Increasing Demand for Persistent, Real-Time Battlefield Awareness to Propel Intelligence, Surveillance & Reconnaissance (ISR) Segmental Growth

By application, the market is segmented into Intelligence, Surveillance & Reconnaissance (ISR), strike & offensive effects, Electronic Warfare (EW), decoy & saturation operations, and others.

Intelligence, Surveillance & Reconnaissance (ISR) segment held largest market share in 2025. The segment grows due to increasing demand for persistent, real-time battlefield awareness in contested environments where manned platforms face unacceptable risks. Low-cost attritable designs enable mass deployment of sensor-equipped drones for wide-area coverage. There is an increase in demand for attritable aircrafts and UAVs designed for high-risk operations which are dangerous for manned or high-end unmanned aircraft.

- For instance, in February 2023, General Atomics Aeronautical Systems (GA-ASI) successfully air-launched its multi-role Eaglet drone from an Army MQ-1C Gray Eagle Extended Range during a demo at Utah's Dugway Proving Grounds.

The strike & offensive effects segment is projected to grow at a steady CAGR of 21.5% over the forecast period.

By Autonomy Level

Effectiveness of Remote Piloted LAAC in GPS-Denied Re-Tasking Drives Segment Growth

Based on autonomy level, the market is segmented into remote piloted, mission autonomy, and high autonomy.

The remote piloted segment holds the largest market share due to its balance of human control reliability and attritable economics, making it ideal for missions requiring precision accountability over full autonomy. Key driving factors include regulatory demands for operator-in-loop lethal actions, enabling faster USAF/USMC certification and deployment than AI-only systems facing ethical hurdles. Remote piloted LCAA excel in GPS-denied re-tasking through secure datalinks, supporting scalable development of attritable drones.

The mission autonomy segment is expected to grow with a fastest growth rate of CAGR of 21.1% over the forecast period.

By Range

Demand of Short Range LCAA During Tactical Missions Supports Segment Growth

Based on range, the market is segmented into short range (1,500–2,500 km), medium range (2,500–3,500 km), and long range (more than 3,500 km).

The short range segment held largest share in market in 2025. This is due to its alignment with tactical mission requirements that prioritize rapid deployment and high-volume operations over extended reach. Cost efficiencies drive adoption, as shorter-range designs leverage simplified propulsion and airframes, enabling scalable production for attritable use in contested environments.

The long range segment is projected to emerge as the fastest-growing at a CAGR of 23.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Increase in Demand for Tactical Unmanned Systems by Army Supports Segment Growth

On basis of end user, the market is segmented into army, navy and airforce.

Army segment is expected to acquire major share in market over the forecast period as there are tactical gaps in divisional maneuver warfare, prioritizing unmanned capabilities at the brigade and squad levels. For instance, in March 2025, U.S. DoD advances low-cost attritable Uncrewed Aerial Systems (UAS) as force multipliers, targeting Group 3 platforms such as V-BAT and RQ-21 Blackjack for missions balancing reusability and affordability over expensive jets such as F-35s. Programs such as Launched Effects and SkyFoundry drive autonomous scouting, EW relays, and loitering munitions are launched from ground vehicles or FVL platforms.

The navy segment is projected to emerge as the fastest-growing at a CAGR of 21.8% over the forecast period.

Low-cost Attritable Aircraft Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Low-Cost Attritable Aircraft (LCAA) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025 with a valuation of USD 1.00 billion, and expected to reach USD 1.26 billion in 2026, fueled by increasing U.S. Air Force and Navy procurement during rise in geopolitical tension and threat postures. Intensified requirements for compact, tube-launched attritable designs compatible with carrier-based operations and F/A-18E/F integration drive demand for lightweight composites in programs such as Boeing's MQ-28 Ghost Bat derivatives and Anduril's Fury variants.

U.S. Low-cost Attritable Aircraft Market

Based on North America’s strong contribution, the U.S. market reached USD 0.96 billion in 2025. The market in the U.S. is projected to experience sustained growth over the forecast period, driven primarily by the Department of Defense’s strategic emphasis on force multiplication, distributed operations, and cost-efficient capability expansion. The U.S. Air Force’s Collaborative Combat Aircraft (CCA) initiative represents a structural shift in procurement philosophy, prioritizing scalable, lower-cost uncrewed platforms designed to operate alongside manned assets.

Europe

Europe is projected to record a growth rate of 18.0% during 2026 to 2034. The market in Europe is expected to grow steadily as European combatant commanders accelerate the shift toward distributed air combat, mass, and cost-efficient force regeneration. As European countries modernize fighter fleets and invest in next-generation combat air programs, there is a parallel requirement for affordable unscrewed aircraft that can be integrated through common mission systems. European governments increase defense allocations and emphasize LCAA programs for focusing on attritable swarms for reconnaissance, EW, and strikes.

- For instance, in October 2025, U.K. Ministry of Defence launched Project VANQUISH RFI for Tier 2 attritable "loyal wingman" drones deployable from Queen Elizabeth-class carriers. The jet-powered FW STOL ACP must enable autonomous short take-off/landing without catapults, supporting F-35B ops for ISR, strike, and refueling in high-risk environments.

U.K. Low-cost Attritable Aircraft Market

The U.K. market in 2025 was at USD 0.09 billion, representing roughly 4.6% of global revenues.

Germany Low-cost Attritable Aircraft Market

Germany market reached USD 0.10 billion in 2025, equivalent to around 4.9% of global sales.

Asia Pacific

Asia Pacific market reached USD 0.66 billion in 2025 and secure the position of the second-largest region in the market. The market is expected to expand at a strong pace, supported by regional security dynamics. Several Asia Pacific countries are building or expanding domestic capability across autonomy software, datalinks, mission payloads, and UAVs manufacturing. Operationally, Asia Pacific’s emphasis on maritime domain awareness, long-range ISR, and distributed operations across islands and remote bases increases the value of attritable platforms and propels the Low-Cost Attritable Aircraft (LCAA) market growth in the region.

Japan Low-cost Attritable Aircraft Market

The Japan market in 2025 was at USD 0.07 billion, accounting for roughly 3.2% of global revenues.

China Low-cost Attritable Aircraft Market

China’s market is projected to be one of the largest worldwide, and its 2025 revenue reached at USD 0.33 billion, representing roughly 15.4% of global sales.

India Low-cost Attritable Aircraft Market

The India market in 2025 was valued at USD 0.13 billion, accounting for roughly 6.0% of global revenues.

Rest of the World

The Latin America market registers modest yet steady growth, driven by regional security concerns and modernization programs. The market in Latin America is expected to remain limited in scale over the near to medium term, primarily due to budgetary prioritization toward fleet sustainment, incremental fighter upgrades, and conventional ISR capabilities. Adoption of CCA-class platforms in the region is therefore increasing with a steady rate. The market in the Middle East & Africa region is growing significantly due to higher-spending in defense industry pursuing advanced airpower modernization. Regional security dynamics, including contested airspace considerations and the need for ongoing investments in next-generation fighters.

COMPETITIVE LANDSCAPE

Key Industry Players

Emphasis on Modular, Open-Architecture Combat Platforms and Scalable Autonomy to Accelerate Market Competition

The global market is evolving around defense primes and emerging unmanned system developers capable of delivering cost-efficient, mission-configurable air vehicles. Competitive positioning is increasingly defined by modular airframe design, open mission systems architecture, and secure communications integration. Leading participants such as General Atomics Aeronautical Systems, Boeing, Lockheed Martin Corporation, Northrop Grumman, and Kratos Defense & Security Solutions are advancing the segment through production-representative prototypes. Ongoing government-backed test and evaluation activity is further strengthening market confidence, signaling transition from conceptual demonstrations to structured manufacturing and testing.

LIST OF KEY LOW-COST ATTRITABLE AIRCRAFT COMPANIES PROFILED

- Kratos (U.S.)

- Boeing (U.S.)

- General Atomics (U.S.)

- DAPRA (U.S.)

- Scaled Composites LLC (U.S.)

- Skyeton (Ukraine)

- Anduril Industries

- Northrop Grumman (U.S.)

- Lockheed Martin Corporation (U.S.)

- Yates Electrospace Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026, U.S. military deployed the Low-Cost Uncrewed Combat Attack System (LUCAS) suicide drone in combat against Iran after its Pentagon unveiling by SpektreWorks. LUCAS drones showcase rapid US adaptation of low-cost, expendable tech for high-threat operations.

- February 2026: General Atomics Aeronautical Systems (GA-ASI) achieved a milestone on February 12th, 2026, by integrating Collins Aerospace's Sidekick Collaborative Mission Autonomy software into the YFQ-42A Collaborative Combat Aircraft for its first semi-autonomous airborne mission.

- February 2026: Kratos Defense & Security Solutions aimed to increase XQ-58 Valkyrie collaborative combat aircraft production from 8 to 40 units annually by 2028, targeting current customers such as the U.S. Marine Corps and a potential sole-source deal.

- September 2025: Boeing and the Royal Australian Air Force successfully demonstrated an air-to-air autonomous weapon engagement from the MQ-28 Ghost Bat, a LAAC designed for loyal wingman operations. The platform operated in coordination with an E-7A Wedgetail and an F/A-18F Super Hornet, showcasing integrated manned-unmanned teaming capability.

- July 2025: Skyeton Prevail Solutions, a new U.K.-Ukraine joint venture between Prevail Partners and Skyeton, was formed on July 2, 2025, to scale production of the battle-proven Raybird UAS for U.K. and NATO operations.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 20.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Weight Class, By Application, By Autonomy Level, By Range, By End User, and Region |

| By Weight Class |

|

| By Application |

|

| By Autonomy Level |

|

| By Range |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.14 billion in 2025 and is projected to reach USD 12.23 billion by 2034.

In 2025, North Americas market value stood at USD 1.00 billion.

The market is expected to exhibit a CAGR of 20.7% during the forecast period of 2026-2034.

By application, the Intelligence, Surveillance & Reconnaissance (ISR) segment is expected to lead the market.

The increase in demand for attrition-tolerant systems in modern warfare is driving market expansion.

Kratos, Lockheed Martin Corporation, Boeing, and General Atomics are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 201

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us