Lunar Surface Infrastructure Market Size, Share & Industry Analysis, By Infrastructure Type (Habitation & Crewed Facilities, Landing & Mobility Infrastructure, Energy Infrastructure, and Others), By Application (Scientific Research & Exploration, Crewed Surface Operations & Habitation, and Others), By Technology (In-Situ Resource-Based Systems, Modular / Prefabricated Systems, and Others), By Autonomy Level (Crew-dependent, Crew-assisted, Teleoperated, and Others), By End User (Civil, Space Agencies, Commercial Lunar Operators, and others), and Regional Forecast, 2026-2034

Lunar Surface Infrastructure Market Size and Future Outlook

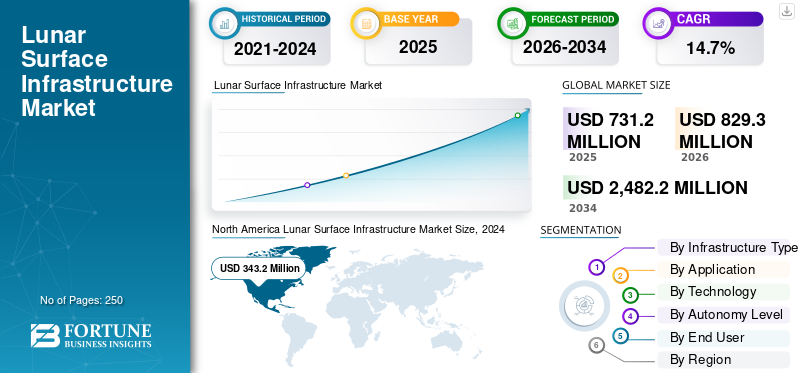

The global lunar surface infrastructure market size was valued at USD 731.2 million in 2025. The market is projected to grow from USD 829.3 million in 2026 to USD 2,482.2 million by 2034, exhibiting a CAGR of 14.7% during the forecast period. North America dominated the lunar surface infrastructure market with a market share of 46.94% in 2025.

Lunar surface infrastructure encompasses a growing ecosystem of landing pads, habitats, power systems, communications nodes, and logistics hubs designed to enable sustained human and robotic presence on the Moon. The global market is expanding rapidly, driven by national lunar‑base programs such as NASA’s Artemis‑aligned “Moon Base” architecture, rising investment in In‑Situ Resource Utilization (ISRU), and public‑private partnerships that are accelerating deployment of hardened landing sites, modular habitats, and surface‑based communications networks.

- For instance, in March 2026, NASA announced transformative initiatives at its "Ignition" event to align with President Trump's National Space Policy, aiming for a Moon return before his term ends, base construction, and enduring U.S. space leadership. Key shifts include phased Moon architecture, LEO commercial transitions, lunar science access, and nuclear propulsion via Space Reactor-1 Freedom, with investments in workforce and partnerships.

Leading industrial players include Lunar Outpost (U.S.), Venturi Astrolab (U.S.), Intuitive Machines and are prioritizing innovations such as modular, expandable habitats, autonomous surface construction systems, and integrated lunar‑data networks to support long‑term operations, resource‑extraction facilities, and secure communications.

Download Free sample to learn more about this report.

Lunar Surface Infrastructure Market Key Takeaways

- 2025 Market Size: USD 731.2 million

- 2026 Market Size: USD 829.3 million

- 2034 Forecast Market Size: USD 2,482.2 million

- CAGR: 14.7% from 2026–2034

- North America dominated the market with a 46.94% share in 2025.

- Landing & Mobility Infrastructure held the largest market share by infrastructure type in 2025.

- Commercial Support & Logistics Services accounted for the largest market share by application in 2025.

North America

The market reached USD 343.2 million in 2025, driven by strong government funding and commercial lunar programs.

Asia Pacific

The market reached USD 194.9 million in 2025, driven by rising investments in lunar missions and domestic space capabilities.

Europe

The market is projected to grow at a 14.7% CAGR during 2026–2034, supported by ESA-led lunar infrastructure initiatives.

U.S.

The market was valued at USD 322.2 million in 2025.

Japan

The market was valued at USD 36.6 million in 2025.

Read More

LUNAR SURFACE INFRASTRUCTURE MARKET TRENDS

Modular and Incremental Lunar‑Base Architectures to Emerge as a Defining Market Trend

The market is exhibiting a pronounced trend toward modular, incremental lunar‑base architectures, where core infrastructure elements such as landing pads, habitats, power systems, and communications nodes are deployed and expanded landing by landing across multiple missions rather than in a single, fully integrated build‑out. This evolution reflects programmatic and strategic imperatives for sustained, long‑term presence on the Moon, favoring phased construction that reduces reliance on any single high‑risk launch and enables continuous learning and adaptation between missions. Industry and agencies are increasingly adopting modular, plug‑and‑play infrastructure designs, often using standardized interfaces for power, data, and mechanical berthing, to allow new modules and systems to be added incrementally as funding, technology, and mission requirements rise.

- For instance, in March 2026, Intuitive Machines secured a USD 180.4 million NASA CLPS contract, its fifth task order for the IM-5 mission, deploying a larger Nova-D lunar lander to deliver seven payloads to Mons Malapert near the Lunar South Pole, including rovers from Australia's Space Agency and Blue Origin's Honeybee Robotics. Payloads feature the modular Near InfraRed Volatiles Spectrometer System (NIRVSS) on Honeybee's next-gen rover for detecting volatiles and mapping regolith.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Investment in In‑Situ Resource Utilization to Drive Market Growth

The market is being strongly driven by increasing investment in In‑Situ Resource Utilization (ISRU), where water‑ice, oxygen, and construction materials extracted from the Moon are used to reduce dependence on Earth‑based logistics and lower the cost of sustained operations.

- For instance, in February 2026, Canadian Space Agency (CSA) launched Lunar Surface Exploration Initiative (LSEI) Architecture Studies to define Canada's "signature technologies" for NASA's Artemis program, targeting sustainable Moon presence via mining/ISRU for processing lunar water ice and regolith into fuel, plus power generation/distribution systems resilient to 14-day nights.

This shift reflects strategic imperatives for long‑term lunar presence, as agencies and commercial players seek to produce propellant, life‑support consumables, and building materials on‑site, which in turn creates robust demand for permanent surface infrastructure such as mining sites, processing plants, and storage depots. Governments and space agencies are prioritizing demonstration and scaling of ISRU technologies, funding pilot missions and infrastructure nodes that will evolve into full‑scale lunar resource‑processing hubs.

MARKET RESTRAINTS

High Capital Intensity and Technical Complexity to Limit Market Expansion

The market faces a restraint in the form of very high upfront capital intensity and extreme technical complexity, which limits participation to well‑funded national agencies and a small group of large prime contractors. Establishing hardened landing pads, radiation‑shielded habitats, dust‑resistant power systems, and reliable surface‑based communications requires advanced materials, stringent safety standards, and multi‑year development cycles, all of which drive up costs and lengthen timelines.

These financial and technical barriers make it difficult for smaller commercial players or emerging space nations to enter the market without significant government backing or international partnerships. Moreover, the need to design systems for extreme thermal swings, abrasive regolith, and long‑term autonomous operation increases engineering risk and hampers the lunar surface infrastructure market growth during the forecast period.

MARKET OPPORTUNITIES

Lunar Infrastructure‑as‑a‑Service and Multi‑User Nodes Presents Growth Opportunities for Market

The market presents a major market opportunity in the development of dedicated, multi‑user infrastructure nodes such as landing complexes, shared power grids, surface‑based communications networks, and logistics hubs that can be reused across multiple missions and customers. As lunar programs move from standalone landings toward sustained operations, demand is shifting toward flexible, service‑based infrastructure that can be leased or accessed on a mission‑by‑mission basis, rather than being built and discarded for each flight.

This transition opens strong scope for Infrastructure‑as‑a‑Service (IaaS)‑style business models, where operators monetize assets through landing‑zone access fees, power‑and‑data subscriptions, refueling services, and logistics support contracts. These service‑based models mirror terrestrial utility and logistics frameworks, where early infrastructure providers capture recurring revenue and become the de‑facto standard for later entrants.

MARKET CHALLENGES

Lack of Common Standards Act as a Key Market Challenge

A major challenge faced is the absence of widely accepted technical, safety, and regulatory standards, which complicates interoperability and raises costs for all participants. As national space agencies, commercial operators, and international partners pursue different architectures, interfaces, and operational rules, infrastructure elements such as landing pads, power connectors, and data protocols.

This fragmentation increases programmatic risk as operators must either design custom interfaces for each partner or carry multiple incompatible systems, driving up weight, complexity, and development time. In addition, there is no clear global framework for lunar‑safety, environmental protection, and traffic‑management rules, which creates legal and political uncertainty around who owns or governs common infrastructure which creates significant challenges for the market growth.

Segmentation Analysis

By Infrastructure Type

Reliable Landing Access and Surface Transport Demand to Propel Landing & Mobility Infrastructure Segment Leadership

Based on infrastructure type, the market is divided into habitation & crewed facilities, landing & mobility infrastructure, energy infrastructure, ISRU & extraction infrastructure, communications & data infrastructure, and logistics & storage infrastructure.

Landing & mobility infrastructure segment leads the lunar surface infrastructure market share due to an increase in demand for reliable landing access and surface transport. Demand is driven by the need to improve mission continuity, reduce operational delays, and enhance the usability of surface assets over longer mission durations. As lunar programs move from demonstration missions to sustained presence models, infrastructure that supports landing, unloading, transfer, and mobility becomes increasingly critical.

- For instance, in September 2023, Astrobotic started working on two NASA SBIR contracts focused on plume-surface interaction, a key technical area for protecting landing systems, payloads, landing sites, and nearby surface infrastructure from lunar dust and engine effects.

ISRU & extraction infrastructure segment is anticipated to rise with a steady long term growth with a CAGR of 16.5% over the forecast period.

By Application

Scientific Objectives and Resource Mapping Boosted Scientific Research & Exploration Segment Growth

By application, the market is segmented into scientific research & exploration, crewed surface operations & habitation, resource utilization & industrial operations, and commercial support & logistics services.

The commercial support & logistics services holds largest share as lunar missions need continuous supply chains for cargo transfer, storage, mobility, and waste handling as activity shifts from one-off landings to sustained operations on the Moon. In addition, the buildout of lunar bases and infrastructure requires reliable support services for habitation, resupply, and surface operations, which makes logistics a foundational enabler of the broader lunar economy.

- For instance, in December 2024, ispace and Magna Petra signed an agreement establishing a framework for transporting prospecting and collection equipment to the lunar surface, aimed at advancing future resource-exploration infrastructure and the wider cislunar economy.

The scientific research & exploration segment is projected to be fastest growing segment and grows with a CAGR of 12.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Precision Resilience in Harsh Environments Supported Autonomous/Robotic Systems Segment Dominance

By technology, the market is segmented into in-situ resource-based systems, modular / prefabricated systems, and autonomous / robotic systems.

The autonomous / robotic systems segment led the market in 2025. The segment is dominating due to the increasing demand for high levels of precision, consistency, and resilience in harsh and communication-constrained environments. Autonomous and robotic systems improve productivity by reducing dependence on continuous human intervention and allowing critical tasks to be performed with greater efficiency. Growth is supported by the increasing need for systems that can conduct inspection, transport, handling, monitoring, maintenance, and surface preparation functions with limited operational overhead.

- For instance, in March 2026, Intuitive Machines announced that NASA awarded it a USD 180.4 million contract to deliver seven science and technology payloads, including an Australian lunar rover and Honeybee Robotics technologies, to the Moon’s South Polar region.

The in-situ resource-based systems segment is projected to be grow with fastest growth rate (CAGR) of 16.7% over the forecast period. The segment is the fastest growing segment owing to its critical role in enabling sustainable, cost-effective lunar bases. By extracting water ice, oxygen, and regolith-derived materials such as propellants and construction feedstock directly from the Moon ISRU drastically reduces reliance on expensive Earth-launched supplies.

- For instance, in September 2024, Sierra Space announced successful thermal-vacuum testing of its Carbothermal Oxygen Production Reactor at NASA’s Johnson Space Center, demonstrating automated extraction of oxygen from simulated lunar regolith in lunar-like conditions. The system is intended to produce oxygen in bulk for life support and propellant, supporting long-duration lunar operations through in-situ resource utilization.

By Autonomy Level

Balanced Remote Control and Adaptability Accelerated Teleoperated Segment Growth

Based on autonomy level, the market is segmented into crew-dependent, crew-assisted, teleoperated, and highly autonomous.

Teleoperated segment dominated the market in 2025 as lunar surface tasks require a balance between remote human control and system-assisted execution. This model is particularly valuable where precision, adaptability, and direct supervisory decision-making are important for mission success. The growth of the industry is accelerated by the need to maintain operational control over high-value assets while still reducing the burden of full on-site human presence. Teleoperation also supports gradual technology transition by allowing operators to manage critical functions before full autonomy is widely adopted.

Highly autonomous segment is expected to grow with a fastest growth rate of CAGR of 16.0% over the forecast period.

By End User

Civil Agency Funding and Program Direction to Propel Segment Growth

On basis of end user, the market is segmented into civil space agencies, commercial lunar operators, national security / defense agencies, and research institutions & academia.

Civil space agencies segment is expected to acquire majority share in market. As civil space agencies remain the primary source of funding, procurement activity, and long-term program direction in lunar development. Their role is critical in shaping early demand, defining mission requirements, and providing financial support for infrastructure that may not yet be commercially self-sustaining. Growth is supported by their ability to initiate multi-phase programs, create structured development pathways, and encourage broader industrial participation. These organizations also play an essential role in technology validation, system qualification, and operational standard-setting, which strengthens the segment growth.

- For instance, in June 2024, MDA Space received a USD 0.72 billion contract from the Canadian Space Agency for the next phases of Canadarm3, the robotic system for Gateway in lunar orbiters, strengthening MDA’s robotics portfolio for lunar-orbital and future surface applications.

The commercial lunar operators segment is projected to emerge as the fastest-growing at a CAGR of 16.4% over the forecast period.

Lunar Surface Infrastructure Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and rest of the world.

North America

North America Lunar Surface Infrastructure Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the lunar surface infrastructure market in 2025 with a valuation of USD 343.2 million, growing to USD 1,059.2 million in 2026, driven by strong institutional demand, advanced prime-contractor capability, and a well-developed private space ecosystem. The market growth also propels in the region owing to long-duration lunar planning, structured public procurement, and the presence of companies capable of delivering end-to-end lunar systems, from landers and mobility platforms to robotics and surface services. Moreover, the region also benefits from deep engineering depth, established test infrastructure, and strong integration between government programs and commercial execution.

- For instance, in April 2024, NASA awarded the Lunar Terrain Vehicle Services contract to the Lunar Dawn team led by Lunar Outpost, alongside partners including Lockheed Martin, GM, Goodyear, and MDA Space. The contract advances a human-rated rover platform designed for Artemis astronauts and future commercial mobility services on the Moon.

U.S. Lunar Surface Infrastructure Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 322.2 million in 2025. The market is expected to grow significantly in U.S. due to the push to establish repeat lunar access, expand surface mobility, and build an operationally sustainable lunar architecture over time. The country also has the most mature ecosystem of private companies working across lunar delivery, robotics, communications, mobility, and supporting infrastructure technologies.

- For instance, in February 2025, Venturi Astrolab and Astrobotic announced that Astrobotic’s Griffin-1 lander will deliver Astrolab’s FLIP rover to the Moon’s South Polar region. The mission gives Astrolab a near-term lunar technology-demonstration platform and expands Griffin-1’s role as a commercial infrastructure carrier for rovers and surface systems.

Europe

Europe is projected to record a growth rate of 14.7% during 2026 to 2034. Europe is expected to witness steady growth shaped by coordinated institutional planning, multinational industrial participation, and a strong focus on strategic autonomy in space access and enabling systems. The region emphasizes on building capabilities in cargo delivery, navigation, communications, robotics, and mission-support infrastructure which supports market expansion. Moreover, Europe is strengthening its role in the market through infrastructure segments that support future lunar operations rather than isolated demonstration missions.

- For instance, in January 2025, Thales Alenia Space signed a contract with ESA worth USD 1,010.1 million to design, develop, and deliver the Lunar Descent Element for ESA’s Argonaut mission. The cargo lander is intended to carry infrastructure, rovers, scientific equipment, and logistics payloads to the Moon, making it one of Europe’s most important lunar infrastructure programs.

U.K. Lunar Surface Infrastructure Market

The U.K. market was valued at around USD 40.9 million in 2025, representing roughly 5.6% of global revenues.

Germany Lunar Surface Infrastructure Market

Germany’s market reached approximately USD 30.1 million in 2025, equivalent to around 4.1% of global sales.

Asia Pacifia

Asia Pacific’s market reached USD 194.9 million in 2025. Asia Pacific is expected to emerge as a high-growth region as multiple countries are building lunar capability through a mix of national missions, technology development, and international partnerships. Growth is supported by rising public-sector investment in lunar landing, roving, in-situ science, and robotic surface systems, which is gradually expanding the region’s technical and industrial base. The region also benefits from a growing focus on indigenous capability development, giving national programs stronger incentives to build domestic supply chains and mission-critical technologies.

- For instance, in October 2025, Japan's ispace and India's OrbitAID signed an MoU at IAC 2025 in Sydney to develop sustainable lunar infrastructure through seamless docking and refueling. OrbitAID's SIDRP payload will integrate with ispace's landers for propellant demos, enabling mission extensions and optimizing refueling, recharging, and data in cislunar space.

Japan Lunar Surface Infrastructure Market

The Japanese market was valued at around USD 36.6 million in 2025, accounting for roughly 5.0% of global revenues.

China Lunar Surface Infrastructure Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 86.1 million, representing roughly 11.8% of global sales.

India Lunar Surface Infrastructure Market

The Indian market was valued at around USD 30.2 million in 2025, accounting for roughly 4.1% of global revenues.

Rest of the World

This region is expected to grow from a smaller base, with demand developing more selectively through targeted national programs, international cooperation, and niche technology participation. The growth in this region is driven by specialized contributions in research, subsystem development, remote operations, and collaboration-led market entry.

The Middle East currently shows stronger visibility within this grouping since some countries are using lunar missions to accelerate domestic space-sector capability and international positioning. Latin America, by contrast, is more likely to participate through institutional partnerships, scientific collaboration, and gradual industrial capability.

Latin America Lunar Surface Infrastructure Market

The Latin America market was valued at around USD 11.5 million in 2025, accounting for roughly 1.6% of global revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strategic Partnerships, Modular Designs, and Phased Fielding Drive Market Leadership

The global lunar surface infrastructure market is defined by a mix of national space agencies, defense‑oriented primes, and emerging commercial space firms delivering hardened landing pads, habitats, power systems, communications nodes, and logistics hubs to enable sustained human and robotic presence on the Moon. Leading players such as NASA, Lockheed Martin, Northrop Grumman, Intuitive Machines, and specialized habitat and construction‑technology firms are prioritizing modular, incrementally fielded architectures that can evolve from single‑mission landing zones into multi‑user lunar‑base complexes.

- For instance, in March 2026, Lockheed Martin advocates nuclear Fission Surface Power (FSP) reactors as the key to powering lunar settlements through 14-day nights and shadowed craters, where solar fails and ice resources abound. A White House executive order mandates Moon reactors by 2030; Lockheed's scalable 5-50 kW modular designs draw on submarine nuclear expertise, bolstered by NASA/DOE Phase 1 (2022) and 2025 testbed contracts.

LIST OF KEY LUNAR SURFACE INFRASTRUCTURE COMPANIES PROFILED IN REPORT

- Intuitive Machines (U.S.)

- Lunar Outpost (U.S.)

- Venturi Astrolab (U.S.)

- Firefly Aerospace (U.S.)

- Astrobotic (U.S.)

- Thales Alenia Space (Italy)

- Telespazio (Italy)

- ispace (Japan)

- MDA Space (Canada)

- Canadensys Aerospace (Canada)

KEY INDUSTRY DEVELOPMENTS

- March 2026: ispace signed a payload service agreement with Korea’s Unmanned Exploration Laboratory to transport a two-wheeled Korean rover to the lunar surface aboard ispace’s new ULTRA lander on Mission 3.

- March 2026: Astrobotic announced it had been awarded a contract by Thales Alenia Space to develop a lunar wheel assembly solution for the Italian Space Agency’s Multi-Purpose Habitation Mobility System. The program supports long-term human surface operations and gives Astrobotic a direct role in mobility hardware for future lunar habitation infrastructure.

- December 2025: Firefly Aerospace signed a commercial payload agreement with Volta Space Technologies to fly a wireless power receiver on Blue Ghost Mission 2 to the Moon’s far side. The payload is intended to demonstrate technology relevant to surviving the lunar night and supporting future lunar power-grid

- July 2025: Canadensys Aerospace was awarded a USD 3.39 million (CAD 4.725 million) contract by the Government of Canada to carry out preparatory studies and develop technology options for a 1-tonne-class Canadian Lunar Utility Rover.

- October 2024: Telespazio signed a USD 144.1 million (EUR 123 million) contract with ESA for the first phase of the Moonlight program. The deal positions Telespazio at the center of Europe’s effort to build a lunar communications and navigation constellation, a foundational element of future lunar infrastructure.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.7% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Infrastructure Type, By Application, By Technology, By Autonomy Level, By End User, and By Region |

| By Infrastructure Type |

|

| By Application |

|

| By Technology |

|

| By Autonomy Level |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 731.2 million in 2025 and is projected to reach USD 2,482.2 million by 2034.

In 2025, the North America’s market value stood at USD 343.2 million.

The market is expected to exhibit a CAGR of 14.7% during the forecast period of 2026-2034.

By application, the commercial support & logistics services segment is expected to lead the market.

Rising investment in‑situ resource utilization is driving market expansion.

Intuitive Machines (U.S.), Lunar Outpost (U.S.), Venturi Astrolab (U.S.), and Firefly Aerospace (U.S.) are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us