Lung Cancer Surgery Market Size, Share & Industry Analysis, By Procedure Type (Lobectomy, Segmentectomy, Pneumonectomy, and Others), By Surgical Approach (Open Surgery, Video-Assisted Thoracoscopic Surgery (VATS), and Robotic-Assisted Thoracic Surgery (RATS)), By Cancer Type (Non-Small Cell Lung Cancer (NSCLC) and Small Cell Lung Cancer (SCLC)), By Provider (Hospitals, Cancer Care Centers, and Others), and Regional Forecast, 2026-2034

Lung Cancer Surgery Market Size and Future Outlook

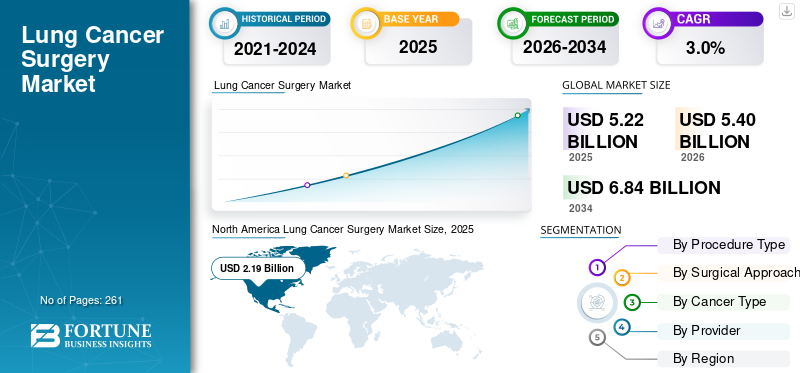

The global lung cancer surgery market size was valued at USD 5.22 billion in 2025 and is projected to grow from USD 5.40 billion in 2026 to USD 6.84 billion by 2034, exhibiting a CAGR of 3.0% during the forecast period. North America dominated the global lung cancer surgery market with a market share of 41.95% in 2025.

Lung cancer surgery refers to the procedures used to remove the tumor, ranging from a small piece to a whole base or even an entire lung. The increasing prevalence of lung cancer, the rising number of surgical procedures, and the expansion of lung screening programmes are resulting in a growing adoption rate of these procedures in the market. This, along with a growing preference for minimally invasive surgical procedures, is further driving patient demand for surgical procedures, thereby boosting the adoption rate of lung cancer surgeries in the market.

- For instance, according to the 2024 data published by the Lung Cancer Research Foundation (LCRF), about 0.7 million people have been diagnosed with lung cancer at some point in their lives in the U.S.

Furthermore, the rising focus toward improving their services among the major players, such as HCA Healthcare, Cleveland Clinic, among others, is further supporting the demand for these procedures in the market.

Download Free sample to learn more about this report.

Lung Cancer Surgery Market Trends

Preferential Shift Toward Minimally Invasive Surgeries to be a Significant Market Trend

There is a strong preferential shift toward minimally invasive and lung-sparing procedures to improve post-operative outcomes among the patient population. The procedures such as Robot-Assisted Thoracic Surgery (RATS) and Video-Assisted Thoracoscopic Surgery (VATS) are increasingly preferred owing to the benefits, including lower blood loss, shorter hospital stays, faster recovery, smaller incisions, and others.

Furthermore, technological advancements in minimally invasive surgeries, increasing adoption of sublobar resections, including wedge resection and segmentectomy for early-stage Non-Small Cell Lung Cancer (NSCLC) patients, primarily due to enhanced tumor localization, improve patient outcomes and reduce perioperative morbidity.

- According to 2020 data published by Science Direct, the use of robotic approaches for thoracic surgery has grown exponentially, with the percentage of cases performed estimated to be up to 20% of lobectomies in the U.S. per year.

Other Prominent Trends

- Increasing uptake of bronchoscopic/percutaneous diagnostic and localized therapy platforms, reducing the need for some surgical interventions.

- Integration of AI/augmented‑reality navigation and image‑guided surgery improves localisation of small pulmonary nodules.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Prevalence of Lung Cancer to Drive Market Growth

The increasing prevalence of chronic conditions, including lung cancer, is resulting in a growing number of surgeries among the patient population, subsequently boosting the demand for innovative products in the market.

- For instance, according to 2022 data published by the World Cancer Research Fund (WCRF), it was reported that about 2.5 million people were diagnosed with lung cancer globally.

The surgical resection remains the primary treatment for early-stage non-small cell lung cancer, growing number of diagnosed patients, especially those identified at resectable stages, directly fuels demand for lung cancer surgeries. Therefore, the factors mentioned above, coupled with the increasing focus of key providers on improving surgical procedures, are anticipated to drive the adoption rate of these procedures, thereby supporting the global market size.

Market Restraints

High Cost of Surgical Procedures to Hamper Market Growth

There is an increasing demand for lung cancer surgical procedures among the patient population. However, the high cost associated hampers the adoption rate for these systems, especially in developing nations, such as Brazil, Mexico, and others.

Additionally, the adoption of robot-assisted thoracic surgery further increases the costs owing to increasing capital investment, costly consumables, and annual maintenance contracts. These financial barriers hamper the procedure accessibility in emerging countries, which limits the adoption in low-and middle-income countries and places pressure on hospital budgets where reimbursement levels do not cover total procedural costs among patients.

- For instance, according to statistics published by Practo, the average cost of lung transplant surgery in India ranges from USD 17,000 to USD 39,000.

Market Opportunities

Expansion of Healthcare Infrastructure to Create Lucrative Market Opportunities

There is an increasing focus on expanding healthcare systems in developing nations, such as India, Brazil, and others. The rising surgical procedural volumes, expansion of hospital infrastructure, and the rising number of healthcare settings such as hospitals, cancer care centers, and others are subsequently supporting the adoption of lung cancer surgical procedures in healthcare facilities.

Moreover, the expansion of tertiary and quaternary care hospitals, coupled with the growing availability of minimally invasive surgical procedures and robotic-assisted operating rooms, is increasing access to lung cancer surgeries and supporting higher procedural volumes.

- According to 2025 data published by the American Hospital Association (AHA), there are about 6,093 hospitals in the U.S.

Market Challenges

Healthcare Access Challenges in Emerging Countries to Hinder Market Growth

There is a growing demand for minimally invasive surgeries and robot-assisted surgeries among the patient population. However, a shortage of skilled surgeons, limited healthcare expenditure, and an insufficient reimbursement framework, particularly in price-sensitive healthcare systems, are limiting access to healthcare settings among the patient population.

Moreover, a limited number of healthcare facilities, including, among others, are some of the vital factors resulting in the delayed surgical procedures among the patient population, particularly in developing countries, including Mexico, Brazil, among others.

- For instance, according to data published by The World Bank Group (WBG), approximately 4.5 billion people lacked full access to essential health services globally in 2023.

Other Prominent Challenges

- Variable reimbursement policies across countries for robotic-assisted thoracic procedures.

- Clinical evidence and long‑term outcomes for certain RATS indications are still maturing compared with established VATS data.

- Access disparities, such as large procedure volumes concentrated in tertiary centres, limit geographic access.

SEGMENTATION ANALYSIS

By Procedure Type

Increasing Number of Lobectomy Procedures Led to Segment Dominance

Based on procedure type, the market is classified into lobectomy, segmentectomy, pneumonectomy, and others.

To know how our report can help streamline your business, Speak to Analyst

The lobectomy segment held the major revenue share in 2025. The growth is due to the rising incidence of lung cancer among patients, resulting in a growing number of surgical procedures, such as lobectomy procedures, globally. This, along with the rising focus of key providers on launching innovative services, is further anticipated to contribute to the global lung cancer surgery market growth.

- For instance, according to 2024 statistics published by JAMA Network, over 40,000 lung cancer lobectomies were performed in the U.S. in 2017.

The segmentectomy segment is expected to grow at a CAGR of 3.8% over the forecast period.

By Surgical Approach

Increasing Number of Open Surgeries Led to Dominance of Open Surgery Segment

Based on surgical approach, the market is segmented into open surgery, Video-Assisted Thoracoscopic Surgery (VATS), and Robotic-Assisted Thoracic Surgery (RATS).

The open surgery segment dominated in 2025 and accounted for 44.7% market share. The growth is due to the increasing incidence of lung cancer, resulting in a growing number of open surgeries.

- For instance, according to 2022 data published by Springer, it was reported that 40% of lobectomies performed are open lobectomy procedures in the U.S.

The segment of Video-Assisted Thoracoscopic Surgery (VATS) is set to flourish with a growth rate of 2.9% across the forecast period.

By Cancer Type

Growing Prevalence of Non–Small Cell Lung Cancer (NSCLC) Led to Dominance of Segment

Based on cancer type, the market is segmented into Non–Small Cell Lung Cancer (NSCLC) and Small Cell Lung Cancer (SCLC).

The Non–Small Cell Lung Cancer (NSCLC) segment dominated in 2025 and held majority of the market share. The segment’s growth is driven by growing prevalence of non–small cell lung cancer, resulting in a growing number of surgeries.

- For instance, according to the 2026 statistics published by the American Cancer Society, it was reported that about 229,410 new cases of lung cancer are projected to occur among the patient population, among which 77% of cases are NSCLC in the U.S.

The segment of Small Cell Lung Cancer (SCLC) is set to flourish with a growth rate of 1.5% across the forecast period.

By Provider

Rising Number of Hospitals Led to Segmental Dominance

In terms of provider, the market segments include hospitals, cancer care centers, and others.

The hospitals segment dominated the market in 2025. The growing number of open and minimally invasive surgeries in hospitals, the rising number of healthcare facilities such as hospitals, among others, are some of the vital factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold a 75.5% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are about 1,874 hospitals in Germany.

In addition, cancer care centers’ providers are projected to grow at a 3.7% CAGR during the forecast period.

Lung Cancer Surgery Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Lung Cancer Surgery Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 2.12 billion, and also took the leading share in 2025 with USD 2.19 billion. The leading adoption of robotic & minimally invasive surgical approaches, high procedure volumes, strong reimbursement, and hospital investments, among others, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2024 statistics published by the State of Lung Cancer 2025, about 20.7% of cases underwent surgery, ranging from best at 31.9% in Massachusetts to worst at 13.1% in New Mexico in the U.S.

U.S. Lung Cancer Surgery Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2.03 billion in 2026, accounting for roughly 37.5% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.70 billion in 2026 and secure the position of the second-largest region in the market. The rapid growth and large procedure volumes, expansion of minimally invasive and robotic thoracic programs in China, Japan, South Korea, and high-volume surgical centers are likely to support the growth of the market.

Japan Lung Cancer Surgery Market

The Japan market in 2026 is estimated at around USD 0.14 billion, accounting for roughly 5.6% of global revenues. Japan has historically reported a relatively increasing prevalence of lung cancer, with a large number of surgical volumes.

China Lung Cancer Surgery Market

China’s market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.83 billion, representing roughly 15.4% of global sales.

India Lung Cancer Surgery Market

The Indian market size in 2026 is estimated at around USD 0.14 billion, accounting for roughly 2.6% of global revenues.

Europe

Europe is projected to record a growth rate of 2.1% in the coming years, which is the third-highest among all regions, and reach a valuation of USD 1.09 billion by 2026. The significant adoption, strong VATS expertise, high surgical volumes in specialized centres, and growing RATS adoption in Western European countries are likely to support market growth.

U.K. Lung Cancer Surgery Market

The U.K. market in 2026 is estimated at around USD 0.18 billion, representing roughly 3.3% of global revenues.

Germany Lung Cancer Surgery Market

Germany’s market is projected to reach approximately USD 0.24 billion in 2026, equivalent to around 4.4% of global sales.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.25 billion in 2026. The growth is due to the variable uptake, project-based investments, and the investment in centers of excellence, among others, which are some of the factors supporting the growth of the market in these regions.

South Africa Lung Cancer Surgery Market

The GCC is set to reach USD 0.07 billion in 2026.

South Africa Lung Cancer Surgery Market

The South Africa lung cancer surgery market is projected to reach around USD 0.03 billion in 2026, representing roughly 0.5% of global revenues.

Competitive Landscape

Key Industry Players

Rising Adoption of Robotic Systems to Sustain Market Expansion

A prominent services portfolio, along with a rising focus on strategic initiatives globally, is one of the key factors contributing to the dominance of these companies in the market. HCA Healthcare and Chesapeake Regional Health are notable companies in the market in 2025. Moreover, the growing focus of key providers on the adoption of advanced robotic systems for lung cancer surgical procedures is likely to strengthen their brand presence and further support the global lung cancer surgery market share.

- For instance, in December 2025, Chesapeake Regional Health announced the adoption of Da Vinci Surgical Robots to perform lung cancer surgery.

Other notable players, including the Cleveland Clinic and others, are also growing in the market, primarily owing to their growing focus on acquisitions and partnerships among other players to fortify their presence in the market.

List of Key Lung Cancer Surgery Companies Profiled in Report

- HCA Healthcare (U.S.)

- Cleveland Clinic (U.S.)

- Chesapeake Regional Health (U.S.)

- Mayo Clinic (U.S.)

- MD Anderson Cancer Center (U.S.)

- Ramsay Health Care (Australia)

- Spire Healthcare Group plc (U.K.)

- Fortis Healthcare (India)

- National Cancer Center Japan (Japan)

- Tata Memorial Centre (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: UT Health Rio Grande Valley opened new Valley’s cancer center with an aim to strengthen its brand presence.

- June 2025: Cleveland Clinic to expand Avon Hospital and Richard E. Jacobs Family Health Center with an aim to strengthen its cancer care capabilities.

- April 2025: Cleveland Clinic Fairview Hospital cancer center modernization advancements, with its plan to expand and modernize its Fairview Hospital cancer center, which includes demolition of aging structures and wider expansion of cancer care capabilities, are expected to increase its surgical treatment capacity.

- February 2025: HCA Healthcare launched lung cancer surgery with two cutting-edge robots at HCA Florida Brandon Hospital, with an aim to strengthen its presence.

- January 2025: Mayo Clinic expanded its cancer center at the New Prague campus. Mayo Clinic began construction on a USD 9.0 million oncology center expansion at its New Prague campus, adding surgical and full oncology services to the facility.

- October 2022: Livac USA, Inc. has been awarded a national group purchasing agreement under Premier, Inc.'s New Technology Breakthrough program for the LiVac Retractor System.

- August 2022: HCA Healthcare, one of the leading healthcare providers, announced that it will collaborate with Johnson & Johnson Services, Inc., to address key healthcare industry issues.

REPORT COVERAGE

The report provides a detailed global lung cancer surgery market analysis and focuses on key aspects such as leading companies and market segmentation, including procedure type, surgical approach, cancer type, and provider. Besides this, the report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Procedure Type, Surgical Approach, Cancer Type, Provider, and Region |

|

By Procedure Type |

· Lobectomy · Segmentectomy · Pneumonectomy · Others |

|

By Surgical Approach |

· Open Surgery · Video-Assisted Thoracoscopic Surgery (VATS) · Robotic-Assisted Thoracic Surgery (RATS) |

|

By Cancer Type |

· Non–Small Cell Lung Cancer (NSCLC) · Small Cell Lung Cancer (SCLC) |

|

By Provider |

· Hospitals · Cancer Care Centers · Others |

|

By Region |

· North America (By Procedure Type, By Surgical Approach, By Cancer Type, By Provider, and by Country) o U.S. (By Cancer Type) o Canada (By Cancer Type) · Europe (By Procedure Type, By Surgical Approach, By Cancer Type, By Provider, and by Country/Sub-region) o U.K. (By Cancer Type) o Germany (By Cancer Type) o France (By Cancer Type) o Italy (By Cancer Type) o Spain (By Cancer Type) o Scandinavia (By Cancer Type) o Rest of Europe (By Cancer Type) · Asia Pacific (By Procedure Type, By Surgical Approach, By Cancer Type, By Provider, and by Country/Sub-region) o China (By Cancer Type) o Japan (By Cancer Type) o India (By Cancer Type) o Australia (By Cancer Type) o Southeast Asia (By Cancer Type) o Rest of Asia Pacific (By Cancer Type) · Latin America (By Procedure Type, By Surgical Approach, By Cancer Type, By Provider, and by Country/Sub-region) o Brazil (By Cancer Type) o Mexico (By Cancer Type) o Rest of Latin America (By Cancer Type) · Middle East & Africa (By Procedure Type, By Surgical Approach, By Cancer Type, By Provider, and by Country/Sub-region) o GCC (By Cancer Type) o South Africa (By Cancer Type) o Rest of the Middle East & Africa (By Cancer Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.22 billion in 2025 and is projected to reach USD 6.84 billion by 2034.

In 2025, North Americas market value stood at USD 2.19 billion.

Growing at a CAGR of 3.0%, the market will exhibit steady growth over the forecast period (2026-2034).

By procedure type, the lobectomy segment is the leading segment in this market.

The introduction of novel lung cancer surgery services is one of the major factors driving the markets growth.

HCA Healthcare and the Cleveland Clinic are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of lung cancer, the increasing number of surgeries, among others, are some of the prominent factors anticipated to drive the adoption of these procedures globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us