Lupus Drugs Market Size, Share & Industry Analysis, By Drug Class (Antimalarials, Corticosteroids, Antimetabolites/Immunosuppressants, Calcineurin Inhibitors, and Others), By Disease Indication (Systemic Lupus Erythematosus (non-renal), Lupus Nephritis, Cutaneous Lupus Erythematosus, and Others), By Route of Administration (Oral, Intravenous, and Subcutaneous), By Age Group (Pediatric, Geriatric, and Adult), By Type (Branded and Generics), By Distribution Channel (Hospital Pharmacies, Retail/Drug Store Pharmacies, Specialty Pharmacies, and Others), and Regional Forecast, 2026-2034

Lupus Drugs Market Size and Future Outlook

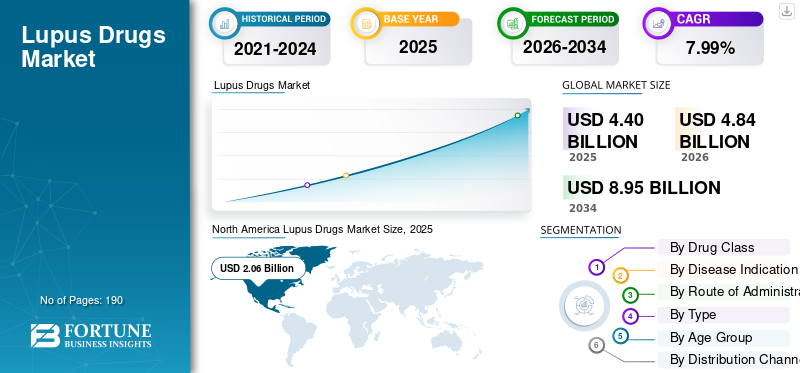

The global lupus drugs market size was valued at USD 4.40 billion in 2025. The market is projected to grow from USD 4.84 billion in 2026 to USD 8.95 billion by 2034, exhibiting a CAGR of 7.99% during the forecast period. North America dominated the lupus drugs market with a market share of 46.81% in 2025.

The global market includes medicines used to treat systemic lupus erythematosus (SLE) and related conditions such as lupus nephritis. The market is experiencing steady growth, driven by the rising prevalence of lupus and the high demand for therapeutics for long-term treatment to control flares, reduce inflammation, and prevent organ damage. Additionally, rising diagnosis rates, greater disease awareness, and the launch of newer targeted therapies are improving treatment access and expanding the use of advanced lupus drugs across broader patient groups.

Key companies are focusing on expanding their offerings and investing in pipeline expansion, followed by regulatory approval, to boost their respective positions.

- For instance, in December 2025, AstraZeneca received approval from the European Union for Saphnelo (anifrolumab) for subcutaneous self-administration via a prefilled pen in adults with systemic lupus erythematosus. These developments improve treatment convenience, support wider patient uptake outside infusion settings, boosting global market growth opportunities for targeted lupus therapies.

Major players, such as GSK plc, AstraZeneca plc, Aurinia Pharmaceuticals Inc, and F. Hoffmann-La Roche Ltd, are expanding their offerings to strengthen their market position.

Download Free sample to learn more about this report.

LUPUS DRUGS MARKET TRENDS

Shift Toward Targeted Biologics and Advanced Immunology Therapies is an Emerging Trend Observed

The global lupus drugs market is witnessing a clear shift toward targeted biologics and advanced immunology therapies. The shift is gaining momentum as conventional lupus treatments often help control symptoms but can still leave many patients with ongoing flares, steroid dependence, and an increased risk of long-term organ damage. As a result, drug developers and healthcare providers are placing greater emphasis on therapies that target specific immune pathways and provide more precise disease control. This shift is improving confidence in biologic-based treatment approaches and expanding the role of advanced therapies in the management of moderate-to-severe lupus.

In addition, continued clinical progress with newer formulations is making these therapies more practical for broader patient use, further strengthening this trend in the market.

- For instance, in September 2025, AstraZeneca announced that its Phase III TULIP-SC trial met the primary endpoint for subcutaneous SAPHNELO (anifrolumab) in patients with systemic lupus erythematosus. The development shows continued advancement in targeted biologic therapy for lupus and supports the market’s shift toward more advanced immunology treatments with greater convenience and broader adoption potential.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Lupus and Lupus Nephritis to Drive Market Growth

The rising prevalence of lupus and lupus nephritis is driving demand in the global lupus drugs market. Lupus is a chronic autoimmune disease that requires continuous treatment, monitoring, and flare control over a long period. As the number of diagnosed patients increases, the need for corticosteroids, immunosuppressants, antimalarials, and targeted biologics also rises across hospital and specialty care settings. The impact is stronger in lupus nephritis cases, as kidney involvement increases disease severity and drives earlier and more intensive treatment.

- For instance, in May 2024, the CDC noted that 204,000 people in the U.S. have SLE, while published data show that lupus nephritis affects a substantial proportion of SLE patients, which keeps demand high for advanced and effective therapies. This reflects the growing burden of lupus nephritis, which is creating demand for newer drugs.

MARKET RESTRAINTS

High Cost of Biologics and Advanced Therapies to Limit Market Growth

The market faces a restraint due to the high cost of biologics and advanced therapies, which increases the overall treatment burden for patients. When therapy costs remain high, physicians and health systems may rely longer on older treatment approaches before moving patients to advanced drugs. These factors slow the adoption of newer lupus therapies. The impact is more pronounced in lupus nephritis, where treatment is intensive and prolonged, making cost a major barrier to broad and sustained use of premium therapies.

- For instance, in October 2023, a published review article titled ‘Management of Lupus Nephritis: New Treatments and Updated Guidelines’, highlighted that, alongside treatment advancements, significant challenges remain, including the cost of therapy and resistant disease. The findings indicated that even when innovative drugs become available, high pricing can still restrict wider uptake and limit market expansion across broader patient populations.

MARKET OPPORTUNITIES

Expansion of Targeted Biologics and Next-Generation Immunology Drugs Creating Growth Opportunities

The market is moving toward more advanced treatment approaches as lupus is a complex autoimmune disease in which many patients do not achieve stable disease control with conventional therapies alone. As a result, there is growing interest in therapies that target specific immune pathways and offer better long-term disease management. These factors create strong market growth opportunity, as targeted biologics and next-generation immunotherapies can address key gaps left by older treatments. When therapies are designed to act on defined immune mechanisms, they can improve disease control, reduce flare burden, and support lower dependence on broad immunosuppression or long-term steroid use.

At the same time, continued clinical progress and regulatory expansion are increasing confidence in advanced lupus therapies, which are opening more opportunities for premium products, lifecycle extensions, and future pipeline launches across the market.

- For instance, in June 2025, GSK plc received U.S. FDA approval for the BENLYSTA (belimumab) Autoinjector for children with active lupus nephritis. The development expanded the reach of targeted biologic therapy to an additional patient group and strengthened commercial opportunities by enabling at-home administration in serious disease settings.

MARKET CHALLENGES

Disease Heterogeneity and Clinical Trial Complexity to Hinder Market Development

High disease heterogeneity makes clinical trial design, patient selection, endpoint measurement, and treatment positioning more complex. When patient populations are highly variable, trial outcomes become less predictable, and even promising drugs candidates may show mixed results across subgroups. This variability slows regulatory progress, increases development risk, and forces companies to be more selective in lupus-related investments and commercial planning. As a result, the market can face delays in bringing newer therapies to patients, even when clinical unmet need remains high. This can result in more complex scrutiny, which can hamper timelines and hinders overall lupus drugs market growth.

- For instance, in February 2026, AstraZeneca received a Complete Response Letter from the U.S. FDA for subcutaneous Saphnelo. Such regulatory setbacks can delay the availability of more convenient administration options that could support wider uptake, highlighting how clinical and regulatory complexities can impact the market availability timeline.

Segmentation Analysis

By Drug Class

BLyS/BAFF Inhibitors Segment Led due to Its Ability to Offer a More Disease-focused Biologic Option for Both SLE and Lupus Nephritis

Based on drug class, the market is categorized into antimalarials, corticosteroids, antimetabolites/immunosuppressants, calcineurin inhibitors, BLyS/BAFF inhibitors, Type I interferon receptor inhibitors, and others.

The BLyS/BAFF inhibitors segment captured the dominant lupus drugs market share, as it includes BENLYSTA (belimumab), which remains one of the most established lupus-specific targeted therapies. This segment has gained strong commercial importance as it has shifted lupus treatment beyond broad symptom control to a more disease-focused biologic approach for both SLE and lupus nephritis. As physicians increasingly prefer targeted therapies for patients experiencing ongoing flares and organ-related risk, the uptake of this class has improved in higher-value treatment settings. This trend has helped the segment lead the market on a value basis, even though older therapies continue to be used more widely in volume terms.

- For instance, in June 2025, GSK announced that the FDA approved BENLYSTA (belimumab) Autoinjector for children with active lupus nephritis. The development strengthened the BLyS/BAFF inhibitor segment by expanding the use of a leading lupus biologic to an additional patient group and supporting broader, long-term adoption of targeted lupus therapy.

The Type I interferon receptor inhibitors segment is expected to grow at a CAGR of 19.25% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Availability of Targeted Therapies Boosted Systemic Lupus Erythematosus Segment Growth

Based on disease indication, the market is segmented into systemic lupus erythematosus (non-renal), lupus nephritis, cutaneous lupus erythematosus, musculoskeletal lupus manifestations, neuropsychiatric lupus, hematologic lupus manifestations, and others.

In 2025, the systemic lupus erythematosus (non-renal) segment dominated the market, as it represented the largest diagnosed patient pool in lupus treatment. The segment remains broad as many patients require long-term therapy to control flares, manage inflammation, and prevent disease progression, even before severe organ involvement develops. As a result, more patients are treated under the non-renal SLE category than in narrower, high-severity manifestations, which supports its leading market share. The wider treatment base across chronic outpatient care also helps this segment maintain strong overall demand. Key companies are actively focusing on regulatory approval for the disease indication.

- For instance, in December 2025, AstraZeneca announced that Saphnelo was approved in the EU for subcutaneous self-administration in adults with systemic lupus erythematosus. This development supports the broader non-renal SLE treatment segment and improves access to targeted therapy for the broader adult SLE population.

The lupus nephritis segment is projected to grow at a CAGR of 9.29% during the forecast period.

By Route of Administration

High Adoption of Oral Therapies Dominated the Segment Growth

Based on route of administration, the market is segmented into oral, intravenous, and subcutaneous.

In 2025, the oral segment accounted for the largest share of the market. Many commonly used lupus therapies, including antimalarials, corticosteroids, antimetabolites, and calcineurin inhibitors, are administered orally. This route remains dominant as lupus is a chronic disease that often needs long-duration treatment, and oral drugs are easier to prescribe, refill, and continue in outpatient settings. As a result, oral therapies support better routine access and are used across a broader range of disease severities than hospital-based injectable options. This wide and sustained use has helped oral administration maintain a leading position over intravenous and subcutaneous routes in overall market share.

- For instance, in June 2025, Merck presented Phase 2 data showing that enpatoran, an investigational oral TLR7/8 inhibitor, improved efficacy signals in patients with systemic lupus erythematosus and cutaneous lupus erythematosus. This development supports the strength of the oral segment, as companies continue to invest in oral lupus therapies that align with long-term outpatient treatment patterns.

The subcutaneous segment is projected to grow at a CAGR of 16.12% during the forecast period.

By Age Group

Adult Segment Led due to Increasing Regulatory Approvals

Based on age group, the market is segmented into pediatric, geriatric, and adult.

In 2025, the adult segment dominated the market as lupus is most commonly diagnosed and treated in adults, especially women of childbearing age. This makes the adult population the largest group receiving both chronic maintenance therapy and advanced treatment for serious complications such as lupus nephritis. As adult patients remain on treatment for longer periods and are more frequently included in commercial launches and label expansions, this age group contributes the highest revenue opportunity in the market. These factors have supported the adult segment’s leading market position.

- For instance, in October 2025, F. Hoffmann-La Roche Ltd received U.S. FDA approval for Gazyva/Gazyvaro for use in adult patients with active lupus nephritis receiving standard therapy. This development reinforced the dominance of the adult segment by introducing a new, high-value treatment option targeted toward the main patient population in lupus care.

The pediatric segment is projected to grow at a CAGR of 9.16% during the forecast period.

By Type

Widespread Use of Cost-effective First-line Therapies Boosted Generics Segment Expansion

Based on type, the market is segmented into branded and generics.

In 2025, the generic segment accounted for the largest share of the market. Many first-line and long-standing lupus treatments, such as hydroxychloroquine, corticosteroids, mycophenolate mofetil, azathioprine, and cyclophosphamide, are available as lower-cost generic medicines. This supports higher prescription volume as lupus is a chronic disease that typically requires long-term treatment, and cost plays an important role in maintaining therapy access over time. As a result, physicians and healthcare systems continue to rely heavily on generics for routine disease control and maintenance treatment. Their broad availability across hospital and retail settings has likely helped the generic segment account for the larger share in volume terms.

- For instance, in June 2025, Camber Pharmaceuticals launched Mycophenolate Mofetil Tablets, USP, the generic version of CellCept. Mycophenolate mofetil is widely used in immunosuppressive treatment pathways, including the management of lupus nephritis, and increased generic availability helps improve affordability and supports wider treatment access. These developments highlight the continued importance of generics in the market.

The branded segment is projected to grow at a CAGR of 10.47% during the forecast period.

By Distribution Channel

Increasing Trend of Digital Order Placement to Support the Dominance of Online Pharmacies

Based on distribution channel, the market is segmented into hospital pharmacies, retail/drugstore pharmacies, specialty pharmacies, online pharmacies, and other institutional channels.

The retail/drugstore pharmacies segment dominated the market, as many lupus patients rely on long-term maintenance medications that are commonly dispensed through retail channels. This factor supports higher prescription volume as lupus is a chronic disease that needs regular refills, ongoing adherence, and easier access outside hospital settings. As a result, retail pharmacies remain an important point of care for routine disease management, especially for patients receiving oral and repeat-use therapies over a long treatment period.

- For instance, in June 2025, GSK plc announced that theS. FDA approved the BENLYSTA (belimumab) Autoinjector for children aged 5 years and older with active lupus nephritis who are receiving standard therapy. The development gave pediatric patients a first-of-its-kind at-home administration option. The availability of at-home, self-administered lupus treatment supports prescription fulfillment beyond hospital-based infusion settings and strengthens the role of retail pharmacies in ensuring continuous therapy access.

The online pharmacies segment is projected to grow at a CAGR of 13.80% over the study period.

Lupus Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Lupus Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 1.79 billion and maintained its leading position in 2025 at USD 2.06 billion. The market is growing as the region has high lupus diagnosis rates, strong access to specialists, and early adoption of biologics and advanced immunotherapy. The presence of leading drug manufacturers and the favorable use of branded therapies also support higher treatment uptake.

U.S. Lupus Drugs Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to reach around USD 2.08 billion by 2026, accounting for roughly 42.95% of the global sales.

Europe

Europe is projected to grow at a CAGR of 7.58% over the coming years, representing the second-highest among all regions. The market is expected to reach a valuation of USD 1.09 billion by 2026. Growth in the region is supported by well-established clinical pathways for the management of autoimmune diseases and broad access to hospital and specialty care services.

U.K. Lupus Drugs Market

The U.K. market is estimated to reach around USD 0.23 billion by 2026, representing roughly 4.74% of the global sales.

Germany Lupus Drugs Market

Germany's market is projected to reach approximately USD 0.26 billion by 2026, equivalent to around 5.43% of the global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.04 billion by 2026, secure the position of the third-largest region in the market. Growth in the region is supported by a large patient pool, improving diagnosis rates, and expanding healthcare systems that are increasing access to autoimmune disease management.

Japan Lupus Drugs Market

The Japanese market is estimated to reach around USD 0.28 billion by 2026, accounting for approximately 5.78% of the global sales.

China Lupus Drugs Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimates at around USD 0.28 billion, representing approximately 5.74% of global sales.

India Lupus Drugs Market

The Indian market is estimated to touch around USD 0.14 billion by 2026, accounting for roughly 2.90% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.29 billion. Latin America is growing as awareness of autoimmune diseases improves and more patients enter formal treatment pathways. In the Middle East & Africa, the GCC is set to reach USD 0.07 billion by 2026.

South Africa Lupus Drugs Market

The South African market is projected to reach approximately USD 0.04 billion by 2026, accounting for roughly 0.89% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on New Product Launches to Reinforce their Market Position

The global lupus drugs market is highly consolidated, with companies such as GSK plc, AstraZeneca plc, Aurinia Pharmaceuticals Inc., F. Hoffmann-La Roche Ltd., and Pfizer Inc. holding significant market share. Strategic partnerships, new product launches, and regulatory approvals continue to drive market share gains among these companies.

- For instance, in October 2024, GSK plc acquired CMG1A46, a clinical-stage dual CD19 and CD20-targeted T cell-engager (TCE), from Chimagen Biosciences (Chimagen), a privately held biotechnology company. The development aimed to develop and commercialize CMG1A46 with a focus on B-cell-driven autoimmune diseases, such as systemic lupus erythematosus (SLE) and lupus nephritis (LN), with potential expansion into related autoimmune diseases indications.

Other notable players in the global market include Sanofi, Pfizer Inc., Viatris Inc., Amneal Pharmaceuticals, Inc., and AbbVie Inc. These companies are expected to prioritize strategic collaborations and new producit launches to strengthen their positions during the forecast period.

LIST OF KEY LUPUS DRUGS COMPANIES PROFILED

- GSK plc (U.K.)

- AstraZeneca (U.K.)

- Aurinia Pharmaceuticals Inc. (Canada)

- Hoffmann-La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Viatris Inc. (U.S.)

- Amneal Pharmaceuticals, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- UCB S.A. (Belgium)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Johnson & Johnson received Fast Track designation from the U.S. FDA for nipocalimaba as a potential treatment for adults with systemic lupus erythematosus (SLE).

- October 2025: Hoffmann-La Roche Ltd received approval from the U.S. FDA for Gazyva/Gazyvaro (obinutuzumab) for the treatment of adult patients with active lupus nephritis (LN) who are receiving standard therapy. The approval also includes a shorter 90-minute infusion time after the first infusion for eligible patients.

- May 2025: Aurinia Pharmaceuticals Inc. reported that a post-hoc analysis of the 52-week, Phase 3 AURORA 1 study showed that lupus nephritis (LN) patients who received triple immunosuppressive therapy with LUPKYNIS (voclosporin), mycophenolate mofetil (MMF) achieved lower proteinuria targets at substantially higher rates. These outcomes were compared to patients in the control group who received mycophenolate mofetil (MMF) and low-dose glucocorticoids alone.

- October 2024: GSK plc acquired CMG1A46, a clinical-stage dual CD19 and CD20-targeted T cell-engager (TCE), from Chimagen Biosciences (Chimagen), a privately held biotechnology company. The development aims to develop and commercialize CMG1A46 with a focus on B-cell-driven autoimmune diseases, such as systemic lupus erythematosus (SLE) and lupus nephritis (LN), with potential to expand into related autoimmune diseases.

- September 2024: UCB, in collaboration with Biogen Inc., announced positive topline results from the Phase 3 PHOENYCS study evaluating dapirolizumab pegol, a drug candidate, in people living with moderate-to-severe systemic lupus erythematosus (SLE). Clinical improvements were observed among key secondary endpoints measuring disease activity and flares.

REPORT COVERAGE

The report provides a detailed global lupus drugs market analysis, focusing on the major clinical and commercial factors shaping market growth. It covers market size and forecast assessment, key growth drivers, restraints, challenges, and emerging opportunities influencing the competitive landscape. The study also examines how rising lupus prevalence, increasing diagnosis of lupus nephritis, growing adoption of targeted biologics, and continued need for long-term disease control are supporting market expansion. In addition, it reviews recent developments, including product approvals, label expansions, clinical progress, collaborations, partnerships, and acquisitions, that are influencing competition and future growth across the industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.99% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Route of Administration, Type, Age Group, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Route of Administration |

|

| By Type |

|

| By Age Group |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.40 billion in 2025 and is projected to reach USD 8.95 billion by 2034.

In 2025, the market value stood at USD 2.06 billion.

The market is expected to grow at a CAGR of 7.99% over the forecast period.

By drug class, the BLyS/BAFF inhibitors segment led the market.

The rising prevalence of lupus and lupus nephritis are the key factors driving market growth.

GSK plc, AstraZeneca plc, Aurinia Pharmaceuticals Inc, Inc, F. Hoffmann-La Roche Ltd, and Pfizer Inc. are the major market players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us