Luxury Coaches Market Size, Share & Industry Analysis, By Deck (Single Deck Luxury Coaches and Double Deck Luxury Coaches), By Propulsion Type (ICE and Electric), By Application (Tourism & Charter Services, Corporate Transport/Executive Shuttles, Airport & Hotel Transfers, and Others), By Seating Capacity (Up to 30 Seats, 31-45 Seats, 46-55 Seats, and Above 55 Seats), and Regional Forecast, 2026-2034

Luxury Coaches Market Size and Future Outlook

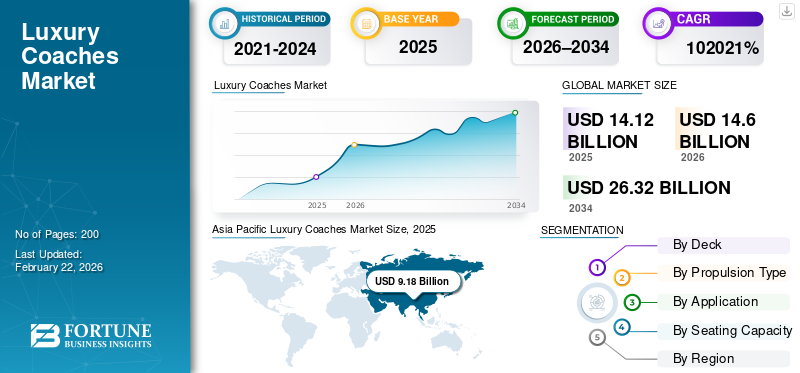

The global luxury coaches market size was valued at USD 14.12 billion in 2025. The market is projected to grow from USD 14.60 billion in 2026 to USD 26.32 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period. Asia Pacific dominated the global luxury coaches market with a market share of 65.01% in 2025.

The luxury coaches market comprises premium buses designed for high comfort, safety, and advanced amenities. These coaches are used for tourism, intercity travel, corporate transport, and charter services, offering features such as spacious seating, onboard entertainment systems, climate control, and modern powertrains to deliver an upscale passenger travel experience.

Key market drivers include rising tourism demand, growing preference for premium travel experiences, expansion of corporate mobility services, increasing disposable income, and advancements in comfort, safety, and electric coach technologies.

Key players in the market include Daimler Buses (Mercedes-Benz & Setra), Volvo Buses, Scania, Irizar Group, Yutong Bus, Van Hool, and Prevost, competing through premium interiors, advanced safety systems, electrification, connectivity, and customized coach solutions.

Download Free sample to learn more about this report.

Luxury Coaches Market Key Takeaways

- 2025 Market Size: USD 14.12 billion

- 2026 Market Size: USD 14.60 billion

- 2034 Forecast Market Size: USD 26.32 billion

- CAGR: 7.6% from 2026–2034

- Asia Pacific dominated the luxury coaches market with a 65.01% share in 2025.

- The double deck luxury coaches segment is projected to grow at a CAGR of 8.9% during the forecast period.

- The electric segment is expected to expand at a CAGR of 10.0% during the forecast period.

Asia Pacific

Asia Pacific remains the largest and fastest-growing regional market, with a CAGR of 8.1% during the forecast period.

Europe

Europe is projected to grow steadily at a CAGR of 7.5% through 2034.

North America

North America is expected to register a CAGR of 6.6% during the forecast period.

U.S.

The market was valued at approximately USD 0.48 billion in 2025.

Japan

Growing demand for premium and sustainable passenger transportation supports market expansion.

Read More

LUXURY COACHES MARKET TRENDS

Integration of Smart Technologies and Connectivity to Shape Market Trends

Luxury coach manufacturers are increasingly integrating smart technologies to enhance passenger experience and operational efficiency. Features such as onboard Wi-Fi, digital infotainment systems, real-time vehicle monitoring, advanced driver-assistance systems, and predictive maintenance solutions are becoming standard in premium coaches. Connectivity enables fleet operators to optimize routes, improve vehicle uptime, and deliver personalized passenger services. Additionally, digital ticketing and integrated mobility platforms are supporting seamless travel experiences. This trend reflects the broader shift toward intelligent transportation systems and positions luxury coaches as technologically advanced alternatives within the premium mobility ecofriendly system.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Premium Tourism and Intercity Travel to Drive Luxury Coach Demand

The steady growth of global tourism, coupled with increasing demand for comfortable intercity travel, is a key driver for the market. Travelers are increasingly prioritizing comfort, convenience, and service quality, encouraging operators to upgrade fleets with high-end coaches featuring ergonomic seating, infotainment systems, and enhanced ride quality. Additionally, the expansion of premium bus services on long-distance and cross-border routes is supporting new vehicle procurement. Corporate travel, luxury travel experiences, and charter services further strengthen demand, particularly in regions with improving road infrastructure and rising disposable incomes, making luxury coaches a preferred alternative to other modes of transport for medium-distance travel.

- In July 2025, MG Group unveiled its TIGRA super-premium luxury coach along with a refreshed corporate identity, marking a significant product development in the luxury coach segment. The TIGRA is positioned as a high-comfort intercity coach built at its Belagavi facility, targeting both domestic and international markets with enhanced safety and passenger amenities. This launch reflects OEM commitment to serving premium travel increased demand and supports market growth driven by rising preference for upscale road transport solutions.

MARKET RESTRAINTS

Limited Route Viability and Utilization Rates to Restrain Market Growth

The commercial success of luxury coaches depends heavily on achieving high utilization rates and operating on routes that can consistently support premium pricing. In many regions, passenger demand is seasonal or concentrated on specific corridors, limiting year-round deployment of luxury fleets. Low occupancy during off-peak periods reduces profitability and discourages operators from investing in high-end coaches. Additionally, competition from low-cost bus services, rail transport, and short-haul air travel restricts route viability for luxury offerings. These demand-side limitations can restrain market growth even as interest in premium travel experiences continues to rise.

MARKET OPPORTUNITIES

Electrification of Premium Coaches to Create Long-Term Growth Opportunities

The transition toward electric mobility presents a strong opportunity for the market. Electric luxury coaches align well with premium positioning by offering quieter operation, smoother rides, and reduced environmental impact. Government incentives, emission regulations, and focus on sustainability commitments from transport operators are accelerating interest in electric luxury fleets, particularly for airport transfers, urban premium routes, and tourist circuits. Advances in battery technology, charging infrastructure, and vehicle range are improving the commercial viability of electric coaches. Early adopters are expected to benefit from lower operating costs, brand differentiation, and compliance with future emission standards.

MARKET CHALLENGES

Infrastructure and Charging Limitations to Challenge Market Expansion

Despite growing demand, infrastructure limitations pose a key challenge for the luxury coaches market, particularly for electric variants. Inadequate charging networks, limited grid capacity, and lack of standardized charging solutions restrict large-scale deployment across long-distance routes. Even for ICE luxury coaches, road quality, parking facilities, and terminal infrastructure can impact vehicle utilization and passenger experience. Addressing these challenges requires coordinated investment from governments, transport authorities, and private stakeholders. Until infrastructure development aligns with vehicle advancements, operational constraints may slow adoption in certain regions and applications.

Segmentation Analysis

By Deck

High Operational Flexibility and Wider Route Compatibility to Propel Single Deck Luxury Coaches Segmental Dominance

Based on deck, the market is classified into single deck luxury coaches and double deck luxury coaches.

The single deck luxury coaches segment holds the major luxury coaches market share due to its broad applicability across tourism, corporate transport, airport transfers, and intercity routes. These coaches offer easier maneuverability, fewer height restrictions, and compatibility with diverse road and terminal infrastructure, enabling higher fleet utilization. Operators prefer single deck models for their lower acquisition costs, operational efficiency, and flexibility across short- and long-distance routes. Strong demand from charter services and premium tour operators sustains consistent replacement cycles and steady procurement across developed and emerging markets.

The double deck luxury coaches segment is expected to grow at a 8.9% CAGR over the forecast period. Growth is driven by increasing demand for high-capacity premium transport on busy tourism corridors and intercity routes, where operators seek higher revenue per trip while maintaining luxury standards.

By Propulsion Type

Established Infrastructure and Long-Haul Suitability to Sustain ICE Segmental Dominance

In terms of propulsion type, the market is categorized into ICE and electric.

The ICE segment holds the largest market share due to its proven reliability, long driving range, and widespread fueling infrastructure. These coaches are well-suited for long-distance tourism, intercity travel, and charter operations where route flexibility and quick refueling are critical. Fleet operators continue to prefer ICE models for their predictable performance, lower operational risk, and ease of maintenance, particularly in regions with limited charging infrastructure. Continuous upgrades in engine efficiency and emission compliance further support sustained demand.

The electric segment is expected to grow at a 10.0% CAGR over the forecast period. Growth is driven by tightening emission regulations, government incentives, and increasing deployment in premium urban transfers, airport routes, and environmentally focused tourism corridors.

By Application

Rising Leisure Travel and Group Mobility Demand to Drive Tourism & Charter Services Segmental Dominance

Based on application, the market is segmented into tourism & charter services, corporate transport/executive shuttles, airport & hotel transfers, and others.

The tourism & charter services segment dominates the market share due to its high volume of group travel, sightseeing tours, and long-distance leisure transportation. Luxury coaches are widely used by tour operators for domestic and international travel, offering superior comfort, onboard amenities, and luggage capacity. Seasonal tourism peaks, expansion of premium tour packages, and growing preference for road-based leisure travel sustain high fleet utilization and recurring vehicle replacement, reinforcing the segment’s leading position.

The corporate transport/executive shuttles segment is expected to grow at a 9.4% CAGR during the forecast period. Growth is driven by increasing corporate mobility needs, demand for premium employee transport, and rising use of luxury coaches for executive travel and business events.

To know how our report can help streamline your business, Speak to Analyst

By Seating Capacity

Balanced Capacity and Comfort to Strengthen 31–45 Seats Segmental Dominance

Based on seating capacity, the market is segmented into up to 30 seats, 31–45 seats, 46–55 seats, and above 55 seats.

The 31–45 seats segment dominates the luxury coaches market as it offers an optimal balance between passenger capacity, comfort, and operational efficiency. These coaches are widely preferred for tourism, charter services, and corporate travel, where operators seek high occupancy without compromising luxury amenities. Their suitability for both short- and long-distance routes, combined with manageable vehicle dimensions and strong route compatibility, supports higher utilization rates and sustained procurement across global markets.

The above 55 seats segment is expected to grow at a 8.8% CAGR over the forecast period. Growth is driven by rising demand for high-capacity luxury transport on busy tourism corridors and intercity routes, where operators aim to maximize revenue per trip while maintaining premium service standards.

Luxury Coaches Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Luxury Coaches Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and remains the fastest-growing luxury coaches market, driven by rapid growth in tourism, rising disposable incomes, and expanding intercity transport networks. China, India, and Southeast Asian nations are witnessing increased adoption of premium coaches for tourism and charter services. Ongoing fleet modernization, improving road infrastructure, and rising preference for comfortable long-distance travel further support demand. The region is expected to grow at a CAGR of 8.1% over the forecast period, reflecting strong volume expansion and increasing premiumization.

China Luxury Coaches Market

The China market in 2025 was valued at around USD 4.98 billion, accounting for a significant share of global revenues, driven by large tourism fleets, intercity travel demand, and strong domestic coach manufacturing capabilities.

India Luxury Coaches Market

The Indian market in 2025 was valued at around USD 2.33 billion, supported by rising tourism, highway expansion, premium intercity services, and increasing adoption of luxury coaches by private and state transport operators.

Europe

Europe holds the second-largest market share due to its well-established intercity coach networks, strong tourism industry, and high penetration of luxury and double-deck coaches. Operators focus on fleet upgrades emphasizing safety, comfort, and sustainability. Increasing adoption of electric luxury coaches, supported by stringent emission regulations and government incentives, continue to drive luxury coaches market growth. The European market is projected to expand at a CAGR of 7.5% during the forecast period.

Germany Luxury Coaches Market

The Germany market in 2025 was valued at around USD 0.53 billion, driven by a mature intercity coach network, strong tourism activity, fleet replacement demand, and increasing adoption of high-spec and electric luxury coaches.

U.K. Luxury Coaches Market

The U.K. market in 2025 was valued at around USD 0.35 billion, supported by tourism recovery, charter services, corporate mobility demand, and gradual electrification of premium coach fleets across key transport corridors.

North America

North America represents the third-largest market, supported by demand from charter services, corporate transport, and long-distance tourism. The region favors high-spec ICE luxury coaches designed for extended routes and passenger comfort. Replacement demand from established fleets and rising preference for premium group travel sustain market growth. Gradual electrification in airport and urban transfer applications is also emerging. The North American market is expected to grow at a CAGR of 6.6% over the forecast period.

U.S. Luxury Coaches Market

The U.S. market in 2025 was valued at around USD 0.48 billion, driven by charter services, corporate and entertainment transport, long-distance tourism, and steady replacement demand for high-comfort touring coaches.

Rest of the World

The rest of the world, including the Middle East & Africa and Latin America, is witnessing gradual growth driven by tourism development, infrastructure investments, and expanding hospitality sectors. Luxury coaches are increasingly used for airport transfers, intercity travel, and premium tourism in key hubs. While adoption remains limited by cost and infrastructure constraints, rising investments in transport modernization and tourism recovery are creating new opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players

Global OEMs and Premium Coach Manufacturers Strengthening Competitiveness in Market

The luxury coaches market is led by established global OEMs and premium bus manufacturers such as Daimler Buses (Mercedes-Benz & Setra), Volvo Buses, Scania, Irizar Group, Yutong Bus, Van Hool, Prevost, and King Long. These players leverage strong engineering capabilities, global manufacturing footprints, and extensive service networks to cater to tourism, intercity, and corporate transport operators. Their portfolios span single- and double-deck coaches with advanced safety systems, high-end interiors, and multiple propulsion options.

Key participants are increasingly focusing on differentiation through passenger comfort enhancements, digital connectivity, and electrified powertrains. Strategic partnerships with component suppliers, investments in electric coach platforms, regional capacity expansions, and customized offerings for fleet operators further strengthen competitive positioning amid rising demand for premium and sustainable road travel.

LIST OF KEY LUXURY COACHES COMPANIES PROFILED IN REPORT

- Daimler Buses (Mercedes-Benz & Setra) (Germany)

- Volvo Buses (Sweden)

- Scania AB (Sweden)

- Irizar Group (Spain)

- Yutong Bus Co., Ltd. (China)

- Van Hool NV (Belgium)

- Prevost (Volvo Group Canada) (Canada)

- King Long United Automotive Industry Co., Ltd. (China)

- Higer Bus Company Limited (China)

- MAN Truck & Bus (Germany)

- MCI (U.S.)

- Alexander Dennis Limited (U.K.)

- Solaris Bus & Coach (Poland)

- TEMSA(Turkey)

- Marathon Coach (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Volvo Buses advanced commercialization of its Volvo BZR Electric Coach platform, targeting long-distance premium applications with higher battery capacity and improved range, strengthening its position in zero-emission luxury and intercity coach segments across Europe and Asia.

- November 2025: Daimler Buses expanded production capacity for Mercedes-Benz and Setra luxury coaches in Europe, focusing on premium interiors, advanced driver assistance systems, and fleet customization to address rising demand from tourism and corporate transport operators.

- September 2025: Irizar Group increased deployment of its i6S Efficient and electric coach platforms, supporting sustainable premium mobility initiatives and strengthening its footprint in European intercity and long-distance luxury coach markets.

- September 2025: Volvo Buses launched the BZR Electric coach chassis, featuring up to 720 kWh battery capacity and a 700 km range, expanding long distance electric coach viability for tour, charter, and intercity use.

- September 2025: Daimler Buses began public road testing of its Setra H₂ Coach hydrogen fuel-cell touring coach, marking progress toward zero-emission long-distance coach technology.

- July 2025: India-based MG Group launched the TIGRA super-premium luxury coach, targeting high-end intercity and charter applications, marking a strategic expansion into global luxury coach markets with enhanced comfort and safety specifications.

- June 2025: Yutong Bus introduced upgraded luxury coach models with intelligent cockpit systems and advanced passenger comfort features, reinforcing its competitive positioning in Asia Pacific and export markets focused on premium tourism transportation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Deck, By Propulsion Type, By Application, By Seating Capacity, and By Region |

|

By Deck |

· Single Deck Luxury Coaches · Double Deck Luxury Coaches |

|

By Propulsion Type |

· ICE · Electric |

|

By Application |

· Tourism & Charter Services · Corporate Transport / Executive Shuttles · Airport & Hotel Transfers · Others |

|

By Seating Capacity |

· Up to 30 Seats · 31–45 Seats · 46–55 Seats · Above 55 Seats |

|

By Region |

· North America (By Deck, By Propulsion Type, By Application, By Seating Capacity, and By Country) o U.S. (By Propulsion Type) o Canada (By Propulsion Type) o Mexico (By Propulsion Type) · Europe (By Deck, By Propulsion Type, By Application, By Seating Capacity, and By Country) o Germany (By Propulsion Type) o U.K. (By Propulsion Type) o France (By Propulsion Type) o Rest of Europe (By Propulsion Type) · Asia Pacific (By Deck, By Propulsion Type, By Application, By Seating Capacity, and By Country) o China (By Propulsion Type) o Japan (By Propulsion Type) o India (By Propulsion Type) o Rest of Asia Pacific (By Propulsion Type) · Rest of the World (By Deck, By Propulsion Type, By Application, By Seating Capacity, and By Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 14.12 billion in 2025 and is projected to reach USD 26.32 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 9.18 billion.

The market is expected to exhibit a CAGR of 7.6% during the forecast period of 2026-2034.

The ICE segment led the market by propulsion type.

Rising premium tourism and intercity travel to drive luxury coach demand.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us