Mobile Commerce Market Size, Share & Industry Analysis, By Transaction Type (Mobile Retailing, Mobile Ticketing/Booking, and Mobile Billing), By Payment Mode (Near-field Communication (NFC), Wireless Application Protocol (WAP), Premium SMS, and Direct Carrier Billing), By End User (Individual Customers, Business Customers, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

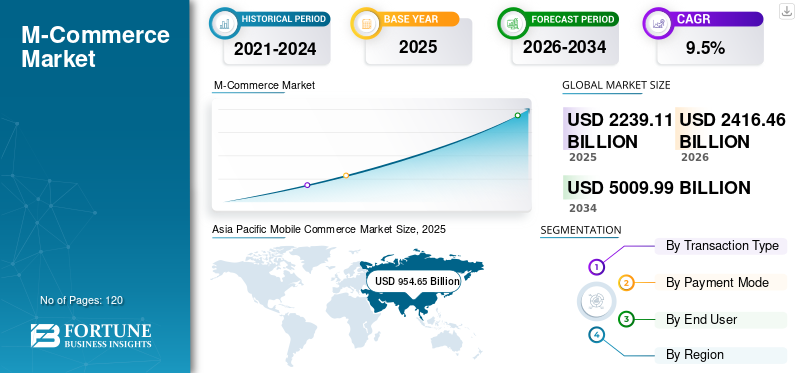

The global mobile commerce market size was valued at USD 2,239.11 billion in 2025. The market is projected to grow from USD 2,416.46 billion in 2026 to USD 5,009.99 billion by 2034, exhibiting a CAGR of 9.5% during the forecast period. Asia-specific dominated the global market with a share of 42.66% in 2025.

Mobile commerce (m-commerce) refers to the buying and selling of goods and services through mobile devices such as smartphones and tablets, typically via mobile apps or web browsers. It encompasses a wide range of transactions, including retail shopping, mobile payments, ticketing, and financial services, all of which are conducted through mobile platforms.

Innovations in mobile payment solutions such as digital wallets (e.g., Apple Pay, Google Pay), near-field communication (NFC), and secure payment gateways have made transactions quicker, safer, and more convenient, thereby boosting m-commerce adoption. This factor is driving global market growth.

The market is dominated by established key players, such as Thales Group, Telefonaktiebolaget LM Ericsson, IBM Corporation, Mastercard Inc., and Mopay AG. These players are continually focused on enhancing the user experience through personalized, seamless, and secure mobile shopping interfaces, while expanding payment options such as digital wallets and mobile payment solutions to improve convenience and conversion rates.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Growing Influence of Generative AI on M-Commerce Strategies Boosts Market Growth

Generative AI is transforming the market by enabling hyper-personalized shopping experiences through AI-driven product recommendations, conversational commerce, and virtual shopping assistants. It helps businesses create dynamic marketing content, personalized ads, and chatbots that improve customer engagement and conversion rates. Generative AI also enhances visual search and product visualization, allowing users to “try before they buy” through image and video generation. Furthermore, it optimizes backend operations by automating inventory descriptions, customer service scripts, and pricing strategies. Overall, it drives efficiency, personalization, and customer loyalty, positioning AI as a core enabler of next-generation mobile commerce. For instance,

- In March 2025, Shopify acquired the generative AI search startup Vantage Discovery to enhance retailer search and product discovery on its commerce platform.

MARKET DYNAMICS

Market Drivers

Growing Adoption of Mobile Payment Solutions Driving M-Commerce Demand

The growing adoption of mobile payment solutions is a key driver of the m-commerce market, as it enables fast, secure, and convenient transactions directly through smartphones. Digital wallets such as Apple Pay, Google Pay, Paytm, Alipay, and Samsung Pay have made one-tap payments mainstream, reducing friction in the checkout process and enhancing user trust. The increasing integration of contactless technologies, including NFC and real-time payment systems (e.g., UPI in India, Pix in Brazil), further accelerates mobile transaction volumes. These solutions not only improve convenience for consumers but also empower merchants with faster settlements and lower processing costs. As a result, mobile payments are becoming the preferred mode of digital transactions, driving the continued global expansion of mobile commerce. For instance,

- October 2025, PayPay Corp. acquired approximately 40% stake in Binance Japan K.K. to expand its mobile payment and crypto services for mobile commerce transactions in Japan.

Market Restraints

Rising Security and Privacy Concerns May Hinder the Market Growth

Security and privacy concerns remain a major restraint in the market, as users are increasingly cautious about sharing personal and financial data on social media platforms. The increasing number of cyberattacks, data breaches, phishing, scams, and identity theft undermines consumer trust in mobile payment systems and e-commerce apps. Many smartphone users hesitate to store payment details or use mobile wallets due to fears of unauthorized access or fraud. Additionally, weak encryption practices and inconsistent data protection regulations across regions exacerbate the risk. As a result, ensuring robust security frameworks, end-to-end encryption, and compliance with privacy laws is crucial for maintaining user confidence and mobile commerce market growth.

Market Opportunities

Rising Emergence of Quick-Commerce and On-Demand Apps Creating Market Opportunities

The emergence of quick-commerce and on-demand apps presents a major opportunity in the market by catering to consumers’ growing demand for speed, convenience, and instant gratification. Platforms such as Blinkit, DoorDash, Getir, and GoPuff leverage mobile-first technology and hyperlocal delivery networks to fulfill orders within minutes, transforming traditional e-commerce into real-time commerce. This model is particularly attractive for categories such as groceries, pharmaceuticals, and daily essentials, where immediacy is valued. The integration of AI-driven inventory management and geolocation-based logistics further enhances delivery efficiency and customer satisfaction. As consumer expectations for faster fulfillment continue to rise, quick-commerce is expected to become a key growth pillar for m-commerce globally. For instance,

- In May 2025, Uber announced the acquisition of an 85% stake in Turkey’s Trendyol GO for USD 700 million, strengthening its position in the global quick-commerce and food delivery segment. The deal allows Uber to expand its mobile commerce footprint in Europe and the Middle East by leveraging Trendyol GO’s vast local network of restaurants and couriers.

Mobile Commerce Market Trends

Growing Advancements in AI and Personalization are Creating New Market Trends

Advancements in AI and personalization are significantly transforming the m-commerce landscape by enabling tailored and data-driven shopping experiences. Artificial intelligence analyzes consumer behavior, preferences, and purchase history to deliver personalized product recommendations, dynamic pricing, and predictive search results, enhancing customer satisfaction and conversion rates. AI-powered chatbots and virtual assistants also provide real-time support and interactive shopping experiences, improving engagement and retention. Moreover, generative AI is now being used to create customized marketing content, visuals, and product descriptions, making interactions more relevant and appealing. Overall, these advancements are helping businesses build stronger customer relationships and drive higher sales efficiency in m-commerce. For instance,

- December 2024, The Australian department store announced a new mobile shopping app as part of a USD 40 million investment in its digital transformation, aimed at enhancing the omnichannel mobile experience.

SEGMENTATION ANALYSIS

By Transaction Type

Rising Mobile Shopping Convenience Drives the Dominance of the Mobile Retailing Segment

Based on transaction type, the market is divided into mobile retailing, mobile ticketing/booking, and mobile billing.

Mobile retailing captured the largest market share of USD 1,616.27 billion in 2025. This is due to consumers increasingly preferring to shop through mobile websites and apps, driven by convenience, personalized recommendations, and seamless checkout experiences. Additionally, the widespread adoption of digital wallets, social commerce integrations, and one-click payment options has made mobile devices the dominant channel for retail transactions, boosting their share within the overall transaction type segment.

Mobile retailing is anticipated to grow at the highest CAGR of 10.4% during the forecast period, as consumers increasingly favor mobile-first, personalized, and seamless shopping experiences, supported by enhanced app functionality and secure, fast mobile payment options.

By Payment Mode

Integration of NFC-Enabled Devices Leads to Surge in Mobile Payment Adoption

Based on payment mode, the market is classified into near-field communication (NFC), wireless application protocol (WAP), premium SMS, and direct carrier billing.

Near-field communication (NFC) captured the largest market share in 2025 with a value of USD 1,238.38 billion. This is owing to consumers increasingly embracing contactless payments for their speed, security, and convenience in both online and in-store transactions. The growing integration of NFC-enabled smartphones, wearables, and POS terminals across retail environments further accelerated adoption, making NFC the dominant mode of mobile payment globally.

Near-field communication (NFC) is expected to grow at the highest CAGR of 10.4% during the forecast period. This is due to the widespread adoption of digital wallets, tap-to-pay features, and NFC-enabled smartphones, which enhance user convenience and transaction efficiency.

By End User

To know how our report can help streamline your business, Speak to Analyst

Rising Smartphone Adoption Drives Individual Customer Dominance in the Market

Based on end-user, the market is categorized into individual customers, business customers, and others (government agencies, NPOs).

Individual customers accounted for the largest market share of USD 1,496.15 billion in 2025, primarily due to the widespread adoption of smartphones, digital wallets, and mobile shopping apps, which made mobile commerce highly accessible for personal use. The growing preference for convenient, personalized, and on-the-go shopping experiences further solidified this segment’s dominance over business and institutional users.

Business customers are projected to grow at the highest CAGR of 13.8% during the forecast period. Enterprises are increasingly adopting mobile platforms for B2B transactions, procurement, and payment processing, driven by the need for efficiency, real-time operations, and digital transformation in commerce.

MOBILE COMMERCE MARKET REGIONAL OUTLOOK

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Mobile Commerce Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest mobile commerce market share in 2024, valued at USD 871.66 billion, and also maintained the leading share in 2025, with USD 954.65 billion. It is expected to grow at the highest CAGR of 11.4% during the forecast period. The factors behind the regional growth include the region’s massive smartphone user base, rapid internet penetration, and widespread adoption of digital payment systems such as UPI, Alipay, and WeChat Pay. Additionally, the dominance of mobile-first economies such as China, India, and Southeast Asia, coupled with the growth of e-commerce giants and super apps, has positioned the Asia Pacific as the global leader in mobile commerce transactions. In the region, India and China are both estimated to reach USD 0.23 billion and USD 0.36 billion, respectively, in 2026. For instance,

- In August 2025, Nykaa launched its “Nykaa Now” quick-commerce service to seven additional Indian cities, including major metros such as Mumbai, Delhi, and Bengaluru, offering 10-minute delivery of beauty and personal care items directly via its mobile app.

Download Free sample to learn more about this report.

In 2026, the Chinese market is estimated to reach USD 221.86 billion. The robust ecosystem of super apps such as WeChat, Alipay, and Taobao seamlessly integrates social media, payments, and shopping into a single mobile experience. Additionally, high smartphone penetration, widespread use of QR-based payments, and advanced logistics networks have made mobile commerce seamless and dominant across both urban and rural areas.

To know how our report can help streamline your business, Speak to Analyst

North America

The market in North America is estimated to reach USD 592.63 billion in 2026, and it is expected to grow at a moderate CAGR of 6.8% during the forecast period. The high adoption of smartphones, digital wallets, and contactless payment technologies, including Apple Pay and Google Pay, drives regional growth. Additionally, the presence of well-established e-commerce players, a strong logistics infrastructure, and a rising demand for personalized shopping experiences continue to drive mobile transaction volumes across the region. In the region, the U.S. is estimated to reach USD 410.37 billion in 2026.

Europe

Europe is expected to experience significant growth in the upcoming years. During the forecast period, the European region is expected to record a growth rate of 7.9%, which is the fourth-highest among all regions, and reach a valuation of USD 471.22 billion by 2026. The primary reason is the increasing use of smartphones and the widespread adoption of secure digital payment methods, including NFC and digital wallets. Furthermore, strong regulatory frameworks for data protection (for instance, GDPR) and the growing shift toward omnichannel retail and cross-border mobile shopping are enhancing consumer trust and fueling market growth across the region. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 92.43 billion, Germany to stand at USD 87.66 billion, and France to hold USD 74.49 billion in 2026.

South America

South America is expected to witness significant growth in this market. The South American market is projected to reach USD 140.24 billion by 2026, driven by the expansion of digital payment platforms, rising smartphone penetration, and increasing consumer trust in online shopping, particularly in emerging markets, such as Brazil, Argentina, and Chile.

Middle East & Africa

The Middle East & Africa are estimated to reach USD 160.51 billion in 2026 and are expected to grow at a significant rate in the coming years, owing to the rising smartphone penetration, expanding internet connectivity, and increasing adoption of mobile payment solutions such as M-Pesa and STC Pay. Additionally, government initiatives promoting digital transformation and financial inclusion, along with the surge of youth-driven online shopping behavior, are propelling the region’s m-commerce expansion. In the region, the GCC is expected to reach a value of USD 51.14 billion by 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Market Players Are Focusing on Mobile-First Expansion and Customer Experience Enhancement to Expand Their Customer Base

Leading companies are expanding their global presence by offering industry-specific and mobile-first solutions. They are focusing on creating fast, seamless shopping experiences through one-tap payments, AI-based personalization, and easy-to-use mobile apps. Alongside this, they are integrating online and offline channels with features such as store pickup, scan-and-go checkout, and faster delivery. Many are also forming partnerships and making acquisitions in payments, logistics, and AI to strengthen their reach and profitability. These strategies enable top players to stay competitive and meet the growing demand for convenient mobile commerce experiences.

Long List of Mobile Commerce Companies Studied

- Thales Group (France)

- Telefonaktiebolaget LM Ericsson (Sweden)

- IBM Corporation (U.S.)

- Mastercard Inc. (U.S.)

- Mopay AG (Germany)

- Oxygen8 (Canada)

- PayPal Holdings Inc. (U.S.)

- Visa Inc. (U.S.)

- SAP SE (Germany)

- Gemalto (Netherlands)

- Ant Group Co., Ltd. (Alipay) (China)

- Boku Inc. (U.S.)

- Google Inc. (U.S.)

- Rakuten Group, Inc. (Japan)

- Adyen N.V. (Netherlands)

- Razorpay Software Private Limited (India)

- Kakao Corp. (South Korea)

- MercadoLibre, Inc. (Argentina)

- Grab Holdings Inc. (Singapore)

- Tencent Holdings Ltd. (China)

….and more

KEY INDUSTRY DEVELOPMENTS

- November 2025: SAP launched advanced AI capabilities (Joule Agents, data ecosystem) at SAP TechEd, aimed at enabling developers to build AI-driven commerce and enterprise solutions.

- October 2025: Ericsson announced a major USD 3 billion partnership agreement in Canada to advance next-generation connectivity and enable smarter commerce channels (5G/edge) supporting mobile commerce experiences.

- July 2025: Curve and Thales announced an expanded collaboration that supports the launch of Curve Pay on iOS and enables NFC contactless payments via the Curve app for both iOS and Android devices.

- April 2025: Visa announced a new “Era of Commerce” featuring AI-enabled payments and strategic partnerships with major tech firms (Anthropic, Microsoft, OpenAI) to enable consumers to browse and buy via AI agents.

- February 2025: IBM completed the acquisition of HashiCorp to bolster its infrastructure automation and hybrid-cloud/AI capabilities, supporting mobile and digital commerce back-end systems.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and the primary applications of the product. Additionally, the report offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the growth of the mobile commerce market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.5% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Transaction Type · Mobile Retailing · Mobile Ticketing/Booking · Mobile Billing By Payment Mode · Near-field Communication (NFC) · Premium SMS · Wireless Application Protocol (WAP) · Direct Carrier Billing By End User · Individual Customers · Business Customers · Others (Government Agencies, NPOs) By Region · North America (By Transaction Type, By Payment Mode, By End User, and By Country) o U.S. (By End User) o Canada (By End User) o Mexico (By End User) · South America (By Transaction Type, By Payment Mode, By End User, and By Country) o Brazil (By End User) o Argentina (By End User) o Rest of South America · Europe (By Transaction Type, By Payment Mode, By End User, and By Country) o U.K. (By End User) o Germany (By End User) o France (By End User) o Italy (By End User) o Spain (By End User) o Russia (By End User) o Benelux (By End User) o Nordics (By End User) o Rest of Europe · Middle East & Africa (By Transaction Type, By Payment Mode, By End User, and By Country) o Turkey (By End User) o Israel (By End User) o GCC (By End User) o North Africa (By End User) o South Africa (By End User) o Rest of Middle East & Africa · Asia Pacific (By Transaction Type, By Payment Mode, By End User, and By Country) o China (By End User) o India (By End User) o Japan (By End User) o South Korea (By End User) o ASEAN (By End User) o Oceania (By End User) o Rest of Asia Pacific |

|

Companies Profiled in the Report |

· Thales Group (France) · Telefonaktiebolaget LM Ericsson (Sweden) · IBM Corporation (U.S.) · Mastercard Inc. (U.S.) · Mopay AG (Germany) · Oxygen8 (Canada) · PayPal Holdings Inc. (U.S.) · Visa Inc. (U.S.) · SAP SE (Germany) · Gemalto (Netherlands) |

Frequently Asked Questions

The market is expected to reach USD 5,009.99 billion by 2034.

In 2025, the market was valued at USD 2,239.11 billion.

The market is expected to grow at a CAGR of 9.5% during the forecast period.

By end user, individual customers led the market.

The growing adoption of mobile payment solutions is driving demand for mobile commerce.

Thales Group, Telefonaktiebolaget LM Ericsson, IBM Corporation, Mastercard Inc., Mopay AG, Oxygen8, PayPal Holdings Inc., Visa Inc., SAP SE, and Gemalto are the top players in the market.

North America held the highest market share.

By end user, the business customers are expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us