Male Infertility Market Size, Share & Industry Analysis By Techniques (DNA Fragmentation Technique, Oxidative Stress Analysis, Microscopic Examination, Sperm Penetration Assay, Sperm Agglutination, Computer Assisted Semen Analysis, and Others), By Condition Type (Primary Male Infertility and Secondary Male Infertility), By End-user (Hospitals and Clinics, Diagnostic Laboratories, and Others), and Regional Forecast, 2026-2034

Male Infertility Market Size and Future Outlook

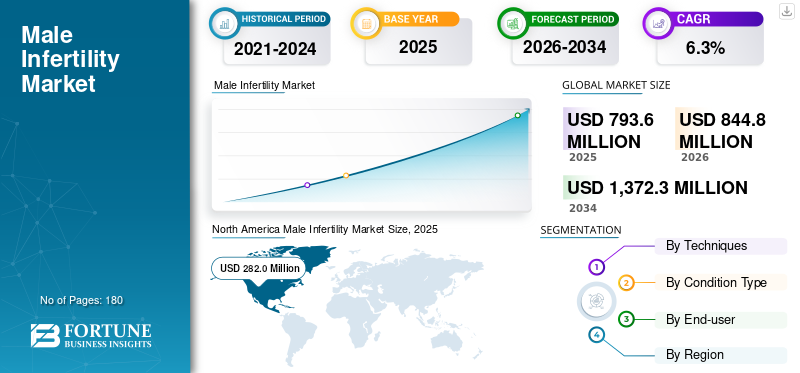

The global male infertility market size was valued at USD 793.6 million in 2025. The market is projected to grow from USD 844.8 million in 2026 to USD 1,372.3 million by 2034, exhibiting a CAGR of 6.3% during the forecast period. North America dominated the global market with a market share of 35.53% in 2025.

Male infertility refers to the inability of a male partner to contribute to conception due to problems such as low sperm count, poor motility, abnormal morphology, oxidative stress, DNA damage, obstruction, hormonal imbalance, or other reproductive disorders. The market includes diagnostic techniques, clinical evaluation, and care pathways used to identify and manage these conditions. The market growth is being supported by a steady rise in delayed parenthood, increasing awareness that infertility is not only a female health issue, and broader acceptance of fertility testing among couples. The market is also benefiting from the expansion of fertility clinics, improving access to semen analysis and advanced testing, and stronger clinical guidance around male-factor evaluation. In addition, more couples are entering assisted reproduction pathways, which often brings male partners into formal diagnostic workflows.

Furthermore, Hamilton Thorne, Inc., Medical Electronic Systems (MES), CooperSurgical, Inc., and Bonraybio Co., Ltd held the largest market share in 2025. This is driven by the limited market presence of other players and market consolidation.

Download Free sample to learn more about this report.

Male Infertility Market Key Takeaways

- 2025 Market Size: USD 793.6 million

- 2026 Market Size: USD 844.8 million

- 2034 Forecast Market Size: USD 1,372.3 million

- CAGR: 6.3% (2026–2034)

- North America dominated the market with a 35.53% share in 2025.

- The semen analysis segment is projected to lead the market with a 70.1% share in 2026.

- The computer-assisted semen analysis segment is projected to register a CAGR of 8.2% during the forecast period.

Asia Pacific

Asia Pacific market is projected to reach USD 209.2 million by 2026.

North America

North America generated USD 282.0 million in 2025 and is expected to maintain its leading market position.

Europe

Europe is projected to reach USD 269.2 million by 2026, registering a CAGR of 5.8% during the forecast period.

U.S.

U.S. market is projected to reach USD 271.4 million by 2026.

Japan

Japan market is projected to reach USD 37.3 million by 2026.

Read More

MALE INFERTILITY MARKET TRENDS

Fertility Care is Moving toward More Structured, Data-Backed, and Male-Factor Assessment

A notable market trend is the gradual transition from ad hoc male fertility evaluation to a more standardized, evidence-based model. Historically, male partners were often assessed late in the fertility journey, sometimes only after repeated failed attempts or after female-focused testing had already been exhausted. That pattern is changing. Clinical guidelines now frame male infertility as a defined medical condition that warrants a structured workup rather than a cursory semen check alone. This is encouraging more consistent use of diagnostic algorithms, repeat semen testing when needed, and the selective use of add-on assessments in more complex cases.

At the same time, fertility care itself is becoming more data-rich. High ART volumes, formal surveillance systems, clinic benchmarking, and specialized andrology programs are helping providers more closely link diagnostic findings to personalized treatment plans. In the U.S., CDC’s ART surveillance highlights the scale and maturity of fertility care infrastructure, while ESHRE (European Society of Human Reproduction and Embryology) continues to support best-practice guidance across reproductive medicine.

Another visible trend is the commercial growth of specialized male fertility services within multidisciplinary reproductive centers. This is raising the profile of male infertility from a supporting topic to a distinct category with its own patient pathways, clinical tools, and service offerings.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Infertility Burden and Broader Male Evaluation to Expand Market Growth

One of the significant drivers for the global male infertility market growth is the increasing recognition that infertility is common, medically significant, and frequently linked to male factors. The World Health Organization estimates that roughly one in six people experience infertility in their lifetime, which underlines the scale of unmet need and the importance of timely diagnosis. At the same time, clinical practice has moved toward evaluating both partners early rather than focusing primarily on women. Current AUA/ASRM guidance recommends a structured male infertility workup that includes reproductive history, physical examination, and at least one semen analysis, with additional testing used when clinically indicated. This more systematic approach increases the number of men entering formal diagnostic pathways.

Another demand catalyst is the continued rise in assisted reproductive treatment activity, which creates a larger referral pool for male fertility testing. In the U.S. alone, the Centers for Disease Control and Prevention (CDC) reported 435,426 ART cycles in 2022, reflecting the size of the patient base flowing through fertility care. As infertility becomes more openly discussed and more clinically managed, male evaluation is no longer optional or secondary. It is becoming a routine part of the fertility journey, directly supporting market expansion.

MARKET RESTRAINTS

Uneven Access, Social Stigma, and Limited Reimbursement to Hamper Market Growth

Despite improving awareness, the market still faces restraints that limit broader and faster adoption. In many countries, fertility evaluation remains expensive, fragmented, or concentrated in urban private centers, resulting in uneven access. The WHO has highlighted the need for more affordable, high-quality fertility care, which reflects the reality that many patients either delay testing or never enter formal care at all.

Social stigma is another major barrier. Male infertility is still under-discussed in many societies and men often postpone evaluation due to embarrassment, denial, or the perception that fertility problems are primarily female-related. This delay reduces early diagnosis and weakens routine screening uptake. In addition, advanced tests are not always used consistently across clinics, partly as evidence standards, pricing, and reimbursement vary from one market to another. Even within developed healthcare systems, some specialized tests may be used selectively rather than universally, which limits volume growth.

Another restraint is the diagnostic complexity of male infertility itself. The European Society of Human Reproduction and Embryology (ESHRE) andrology initiative notes that current methods remain inadequate for identifying the cause in many men, leaving a significant share of cases in poorly defined or idiopathic categories. That uncertainty can reduce clinical confidence, complicate fertility treatment options, and temper spending on advanced diagnostics.

MARKET OPPORTUNITIES

Advanced Diagnostics and Earlier Workup Pathways to Create Significant Growth Opportunities

The market’s strongest opportunity lies in the shift from basic semen testing to more layered, clinically targeted diagnostic workups. Traditional semen analysis remains the entry point, but fertility specialists are increasingly looking beyond a single routine test when couples face recurrent pregnancy loss, unexplained infertility, repeated ART failure, or suspected male-factor abnormalities. American Urological Association (AUA)/ American Society for Reproductive Medicine (ASRM) guidance supports additional evaluation in selected clinical situations, including sperm DNA fragmentation and genetic workup in certain cases. This creates room for higher-value testing, repeat assessments, and more individualized diagnostic pathways. The opportunity is especially significant in private fertility networks and advanced hospital-based reproductive centers, where couples are willing to pay for deeper evaluation if it may improve outcomes or guide treatment decisions.

The expansion in digital imaging, computer-assisted semen analysis, standardized lab workflows, and specialized andrology services could also improve test consistency and commercial uptake. Beyond mature markets, there is a substantial whitespace in emerging economies, where demand exists, but diagnostic penetration remains relatively low. As awareness improves and fertility services spread beyond large cities, male infertility testing can move closer to routine practice. Over time, the market has room to expand by attracting more patients and better stratifying patients, expanding test options, and strengthening integration with the broader fertility ecosystem.

MARKET CHALLENGES

Clinical Variability and Unclear Root Causes to Complicate Market Growth

A major challenge in the male infertility market is that diagnosis is rarely simple, linear, or uniform across patients. Many men present with overlapping causes, fluctuating semen parameters, or findings that do not fully explain infertility outcomes. Even after testing, a considerable number of cases remain unexplained. This creates a practical challenge for clinicians and a commercial challenge for the market as the value of advanced testing depends heavily on how reliably results influence treatment decisions.

Another challenge is standardization across laboratories. Male fertility diagnostics depend on sample quality, lab processes, interpretation, and repeatability, all of which can affect confidence in results. In addition, patient behavior remains unpredictable. Some men resist evaluation, some couples drop out before completing workups, and others move directly into treatment decisions without pursuing a full diagnostic pathway. When clinical ambiguity, lab variability, and patient hesitation occur together, market development becomes less linear. These factors do not eliminate demand, but they make growth more uneven and more dependent on provider quality, protocol consistency, and education.

Segmentation Analysis

By Techniques

High First-Line Use to Push the Dominance of the Microscopic Examination Segment

Based on techniques, the market is segmented into DNA fragmentation technique, oxidative stress analysis, microscopic examination, sperm penetration assay, sperm agglutination, computer assisted semen analysis, and others.

To know how our report can help streamline your business, Speak to Analyst

The microscopic examination segment holds the highest market share as it is the most established and widely used first-line method in male infertility evaluation. In routine clinical practice, semen analysis remains the starting point for assessing sperm count, motility, volume, and morphology, making microscopic examination the foundation of male fertility testing. Its dominance is supported by relatively broad availability across hospitals, clinics, and diagnostic laboratories, as well as lower cost compared to advanced assays such as DNA fragmentation or oxidative stress analysis.

Additionally, the computer assisted semen analysis segment is projected to grow at a CAGR of 8.2% during the forecast period.

By Condition Type

High Evaluation Rate for First-Time Conception Supports the Leading Share of the Primary Segment

By condition type, the market is classified into primary male infertility and secondary male infertility.

The primary male infertility segment accounts for the largest share as a significant proportion of men enter fertility evaluation while attempting conception for the first time. In real-world practice, couples who fail to achieve an initial pregnancy are more likely to seek structured assessment earlier, which pushes primary infertility into the larger diagnostic pool. This segment is projected to hold a 70.1% share in 2026.

Additionally, the secondary male infertility segment is estimated to grow at a CAGR of 7.0% during the forecast period.

By End-user

Integrated Fertility Care Delivery to Foster the Dominance of the Hospitals and Clinics Segment

On the basis of end-user, the market is classified into hospitals and clinics, diagnostic laboratories, and others.

The hospitals and clinics segment holds the highest male infertility market share as they serve as the primary access points for fertility consultations, semen testing, referral decisions, and integrated reproductive care. Patients usually begin their journey in a clinical setting, where history-taking, physical examination, initial semen analysis, and follow-up planning can be coordinated in one place. Furthermore, the segment is set to hold a 58.2% share in 2026.

The diagnostic laboratories segment is projected to grow at a CAGR of 7.4% during the forecast period.

Male Infertility Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Male Infertility Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, with a value of USD 266.0 million, and dominated the market in 2025 with a valuation of USD 282.0 million. The market growth in North America is being driven by the high awareness of infertility, strong use of specialist fertility services, and the region’s ability to monetize advanced diagnostics better than most other markets. The U.S. remains the key engine of regional demand due to its large fertility clinic base and high treatment throughput. The region also benefits from earlier male-factor evaluation, wider use of advanced laboratory workups, and greater acceptance of private-pay for add-on tests beyond routine semen analysis.

U.S. Male Infertility Market

In 2026, the U.S. market is estimated to represent USD 271.4 million, capturing 32.1% of the global revenue.

Europe

Europe is expected to achieve a CAGR of 5.8% over the forecast period, the second-highest globally, and is anticipated to reach USD 269.2 million by 2026. The Europe market is growing on the back of a broad, well-established fertility care network spanning multiple sizeable markets, including the U.K., Germany, France, Spain, and Italy. The regional market growth is supported by the presence of national registries, structured reproductive medicine frameworks, and relatively strong clinician awareness of infertility workups.

- For instance, ESHRE’s European IVF Monitoring Programme was created to collect and publish regional data on service structure, treatment activity, and outcomes, reflecting the maturity of fertility care infrastructure across Europe.

U.K. Male Infertility Market

The U.K. market is projected to reach USD 37.6 million by 2026, accounting for 4.4% of the global market revenue.

Germany Male Infertility Market

The Germany market is projected to reach about USD 45.7 million by 2026, representing roughly 5.4% of the global revenue.

Asia Pacific

In 2026, Asia Pacific market is predicted to be valued at USD 209.2 million, ranking as the third-largest globally. The regional market is expanding due to its very large patient pool, improving fertility awareness, and the continued development of organized fertility services in countries such as Japan, China, South Korea, and Australia. Even though average realized pricing is lower than in North America, the region benefits from rising consultation volumes, delayed parenthood in urban populations, and the gradual uptake of advanced infertility workups for men in higher-tier centers.

Japan Male Infertility Market

The Japan market is projected to generate approximately USD 37.3 million in revenue by 2026, contributing nearly 4.4% to the global market.

China Male Infertility Market

The China market is estimated to reach approximately USD 58.9 million by 2026, contributing about 7.0% to global revenues.

India Male Infertility Market

The India market is anticipated to contribute approximately USD 34.0 million to the global market by 2026, corresponding to about 4.0% of the global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa markets are anticipated to witness moderate market growth, with Latin America expected to reach around USD 37.4 million by 2026. Growth in Latin America is being supported by improving fertility awareness, the gradual expansion of specialist reproductive centers, and the existence of an established regional assisted reproduction network. The Middle East and Africa region is growing from a smaller base, with demand supported by rising awareness, gradual expansion of fertility care in Gulf countries, and improving clinical infrastructure in select markets such as South Africa.

GCC Male Infertility Market

By 2026, the GCC market is expected to generate approximately USD 10.6 million in the market, accounting for nearly 1.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The global male infertility market is moderately fragmented, with competition spread across routine semen analysis, CASA systems, sperm DNA fragmentation testing, oxidative stress testing, and related andrology workflows. While no single company dominates the market, a handful of established players hold stronger positions in high-volume segments such as semen analysis and automated systems. At the same time, several specialist companies compete in advanced and niche testing areas. Key companies such as Hamilton Thorne, Inc., Medical Electronic Systems (MES), CooperSurgical, Inc., and Bonraybio Co., Ltd. lead the global market share.

Moreover, other key players, such as Halotech DNA, S.L., PROiSER R+D, S.L., Sperm Processor Pvt. Ltd., and Nidacon International AB, compete based on the product development in clinical trials and ongoing advancements in technology.

LIST OF KEY MALE INFERTILITY COMPANIES PROFILED

- Hamilton Thorne, Inc. (U.S.)

- Medical Electronic Systems (MES) (U.S.)

- CooperSurgical, Inc. (U.S.)

- Bonraybio Co., Ltd. (Taiwan)

- Halotech DNA, S.L. (Spain)

- PROiSER R+D, S.L. (Spain)

- Sperm Processor Pvt. Ltd. (India)

- Nidacon International AB (Sweden)

- FertiPro N.V. (Belgium)

- MiOXSYS (Lithuania)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Fellow Health closed a USD 24 million Series B financing round to expand male reproductive test offerings, signaling continued investment in patient-centric male testing platforms.

- July 2025: Medical Electronic Systems (MES) launched MaleMan, an all-in-one semen-analysis reference lab service and at-home test kit.

- May 2025: ReproUnion announced a collaboration between RUBIC, Rigshospitalet, and Caerus Biotech to use MiOXSYS on 1,000 semen samples, a significant validation-and-adoption step for oxidative-stress testing.

- March 2025: PS Fertility announced the commercial availability of PS Detect, a new male fertility test positioned as a complement to standard semen analysis.

- November 2024: Hamilton Thorne announced a partnership with MIM Fertility, bringing MIM’s AI-powered embryo assessment onto Hamilton Thorne systems.

REPORT COVERAGE

The report provides a detailed global male infertility market analysis and focuses on key aspects such as leading companies and market segmentation, including techniques, condition type, and end-user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years. It also provides insights into technological advancements, company market share analysis, and the profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.3% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Techniques, Condition Type, End-user, and Region |

| By Techniques |

|

| By Condition Type |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 793.6 million in 2025 and is projected to reach USD 1,372.3 million by 2034.

In 2025, North Americas market value stood at USD 282.0 million.

The market is expected to exhibit a CAGR of 6.3% during the forecast period of 2026-2034.

The microscopic examination segment leads the market by techniques.

The key factors driving the market are the rising infertility burden and broader male evaluation.

Hamilton Thorne, Inc., Medical Electronic Systems (MES), CooperSurgical, Inc., and Bonraybio Co., Ltd are the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us