Mammography Systems Market Size, Share & Industry Analysis, By Type (Digital and Analog), By End-user (Hospitals, Specialty Clinics, Diagnostic Imaging Centers, and Others), and Regional Forecast, 2026-2034

Mammography Systems Market Size and Future Outlook

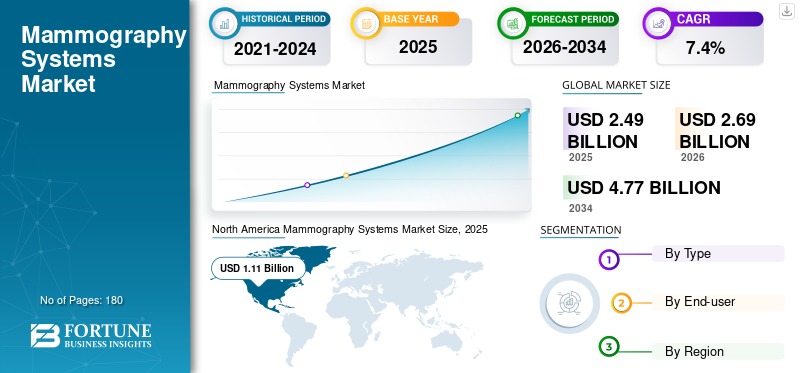

The global mammography systems market size was valued at USD 2.49 billion in 2025. The market is projected to grow from USD 2.69 billion in 2026 to USD 4.77 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period. North America dominated the mammography systems market with a market share of 44.58% in 2025.

Mammography systems are medical imaging platforms used to screen, detect, and evaluate breast abnormalities, especially breast cancer, through 2D digital mammography, 3D digital breast tomosynthesis (DBT), and contrast-enhanced mammography. Market growth is driven by the rising number of breast cancer cases and by key players actively launching AI-enabled reconstruction, workflow, and detection tools.

Furthermore, GE HealthCare, Hologic, Inc., and Siemens Healthineers AG held the highest market share in 2025 due to their broad portfolios and strong installed base worldwide.

Download Free sample to learn more about this report.

Mammography Systems Market KEY TAKEWAYS

- 2025 Market Size: USD 2.49 Billion

- 2026 Market Size: USD 2.69 Billion

- 2034 Forecast Market Size: USD 4.77 Billion

- CAGR: 7.4% from 2026–2034

- North America dominated the mammography systems market with a 44.58% share in 2025.

- The digital segment held the largest market share in 2025.

- The hospitals segment is projected to account for 45.8% of the market in 2026.

North America

North America reached USD 1.11 billion in 2025 and remains the leading regional market.

Europe

Europe is projected to reach USD 0.57 billion in 2026, supported by a strong network of diagnostic imaging centers.

Asia Pacific

Asia Pacific is expected to become the second-largest market, reaching USD 0.53 billion in 2026.

U.S.

The mammography systems market is projected to reach USD 1.15 billion by 2026.

Japan

The mammography systems market is projected to reach USD 0.10 billion by 2026.

Read More

MAMMOGRAPHY SYSTEMS MARKET TRENDS

Shift Toward 3D Mammography and AI-Assisted Workflow to Emerge as a Key Trend

Currently, there has been a significant shift from conventional digital mammography toward 3D mammography combined with AI-enabled workflow tools. Digital and DBT-led platforms improve tissue visualization, reduce overlap effects, and fit screening as well as diagnostic use cases. As a result, key players are packaging reconstruction software, density tools, risk assessment, reporting automation, and cloud integration.

- For instance, according to the article published by JEFFERSON RADIOLOGY in May 2024, the transition from 2D to 3D mammography represents a major technological advancement. Conventional 2D mammograms acquire four flat images of the breasts, where overlapping tissues can hide or obscure important details. In contrast, 3D mammography, or digital breast tomosynthesis, greatly improves breast cancer detection by acquiring around 200 images from multiple angles to build a detailed three‑dimensional view, boosting detection rates by up to 41.0% compared with conventional 2D mammograms.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Incidence of Breast Cancer Cases to Fuel the Market Expansion

Over the past few years, there have been an increasing number of cases of breast cancer worldwide, which is driving the clinical shift toward higher-performance imaging such as 2D and 3D mammography. In contrast, the healthcare providers are moving toward DBT, contrast-enhanced mammography, and AI-supported workflows because these tools improve lesion visibility, support radiologist efficiency, and strengthen confidence in dense-breast imaging. Such a scenario is anticipated to drive the global mammography systems market growth during the forecast period.

- For instance, according to the data from the National Cancer Institute, there were 316,950 new cases of breast cancer in 2025.

MARKET RESTRAINTS

High Capital and Operating Cost Burden to Restrict Market Growth

Despite significant adoption of mammography, advanced mammography systems require substantial upfront investment, modifications to rooms, service contracts, quality-control compliance, and software upgrades. In such cases, smaller diagnostic centers and facilities, especially in emerging countries, often delay replacement cycles due to higher overall costs. This is expected to hinder the market growth over the forecast period.

- For instance, as of April 2026, LabX Media Group stated that new system prices typically range from USD 50,000 to USD 300,000, varying by brand, features, and digital capabilities.

MARKET OPPORTUNITIES

AI, Dense-Breast Imaging, and Emerging Markets to Create Significant Growth Opportunities

In recent years, there has been increasing adoption of AI-enabled mammography, dense-breast workflows, and expansion into underserved regions. As a result, there has been an increase in partnerships to expand the product and maintain higher availability of advanced systems worldwide. Moreover, the expansion of healthcare infrastructure in emerging countries is presenting a lucrative opportunity for the installation of mammography systems.

- For instance, in April 2025, iCAD partnered with Microsoft to make its AI‑powered mammography solutions in the ProFound Breast Health Suite available through Microsoft’s Precision Imaging Network (PIN).

MARKET CHALLENGES

Shortage of Professionals and Accessibility Gaps to Challenge Market Expansion

Despite the significant demand for mammography systems, several regions continue to struggle with limited screening infrastructure, a shortage of radiologists, and delayed follow-up pathways.

Even where demand is strong, integrating AI, PACS, reporting, biopsy, density notification, and contrast-enhanced workflows is complicating operations. This is expected to limit the adoption of mammography systems, challenging the market expansion.

- For instance, according to the Association of American Medical Colleges, the U.S. is projected to face a shortage of 17,000 to 42,000 radiologists by 2033.

Segmentation Analysis

By Type

Increasing Advanced Product Launches to Drive the Digital Segment’s Growth

Based on type, the market is bifurcated into digital and analog.

To know how our report can help streamline your business, Speak to Analyst

The digital segment accounted for the largest global mammography systems market share in 2025. In recent years, digital mammography systems have become the practical standard for modern breast screening and diagnostics. As a result, key players are launching advanced products to increase product availability, contributing to the segment’s growth.

- For instance, in November 2023, Hologic, Inc. showcased next-generation AI solutions at RSNA 2023, including Genius AI Detection 2.0 for mammography.

Additionally, the analog segment is projected to grow at a 3.8% CAGR during the forecast period.

By End-user

Higher Patient Volumes in Hospitals to Propel the Segment’s Growth

On the basis of end user, the market is segmented into hospitals, specialty clinics, diagnostic imaging centers, and others.

In 2025, hospitals dominated the market by end-users. The growth is attributed to the high patient volume in these settings, which is favoring the adoption of advanced mammography systems. Furthermore, the segment is set to hold 45.8% share in 2026.

In addition, the diagnostic imaging centers segment is projected to grow at a 8.3% CAGR over the forecast period.

Mammography Systems Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Mammography Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 1.01 billion, and held the market value of USD 1.11 billion in 2025. The growth is attributed to high breast-screening awareness, broad adoption of digital mammography and tomosynthesis, favorable reimbursement in the U.S., and faster uptake of AI-enabled breast imaging tools.

U.S. Mammography Systems Market

In 2026, the U.S. is anticipated to reach USD 1.15 billion, accounting for approximately 42.8% of the global market.

Europe

Europe is projected to record a 6.1% growth rate during the forecast period, the third-highest globally and is anticipated to reach USD 0.57 billion in 2026. The growth is driven by a large network of diagnostic imaging centers and radiologists, prompting major players to expand their product portfolios in the region.

- For instance, the Royal College of Radiologists (RCR) 2024 census reported that 4,699 whole‑time equivalent (WTE) consultant clinical radiologists were practicing in the U.K.

U.K Mammography Systems Market

The U.K. market is projected to reach USD 0.07 billion by 2026, representing approximately 2.8% of global revenues.

Germany Mammography Systems Market

Germany's market is expected to reach USD 0.14 billion by 2026, accounting for approximately 5.2% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is projected to reach approximately USD 0.53 billion, making it the second-largest market worldwide. The growth is attributed to improved diagnostic infrastructure, rising breast cancer awareness, and increasing investments in women’s health across China, India, Japan, Australia, and Southeast Asia.

Japan Mammography Systems Market

Japan is projected to generate approximately USD 0.10 billion in revenue by 2026, representing nearly 3.8% of the global market.

China Mammography Systems Market

China’s market is anticipated to reach around USD 0.26 billion by 2026, accounting for nearly 9.6% of global revenues.

India Mammography Systems Market

India’s market is expected to reach approximately USD 0.03 billion by 2026, accounting for around 1.3% of global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate growth, with the Latin America market estimated to reach approximately USD 0.24 billion by 2026. The growth is driven by the gradual expansion of screening programs, increasing urban hospital capacity, and rising government initiatives and private-sector focus on early cancer detection.

GCC Mammography Systems Market

By 2026, the GCC market is estimated to reach approximately USD 0.06 billion, representing around 2.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Portfolios and Strong Installed Base to Strengthen the Market Presence of Major Players

In 2025, GE HealthCare, Hologic, Inc., and Siemens Healthineers AG held the largest global share. The dominance of these companies is mainly due to their strong focus on technological innovation, broad product portfolios, and a wide global installed base.

Moreover, other prominent players are strengthening their presence through cost-competitive systems and expansion in emerging markets. Also, these companies are focusing on upgrading existing installed bases, further intensifying competition.

LIST OF KEY MAMMOGRAPHY SYSTEMS COMPANIES PROFILED

- Hologic, Inc. (U.S.)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- Fujifilm Holdings Corporation (Japan)

- Planmed Oy (Finland)

- Metaltronica S.p.A. (Italy)

- Trivitron Healthcare (India)

- Shanghai United Imaging Healthcare Co., LTD (China)

- Genoray (South Korea)

- SternMed GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Vega Imaging Informatics curated the world’s largest digital breast tomosynthesis (DBT) dataset, comprising over 1 million studies paired with biopsy outcomes for more than 22,000 patients, including over 7,000 cancer cases.

- October 2025: RAYUS Radiology launched Transpara Breast AI services at its clinics in Washington State, adding FDA‑cleared AI‑assisted mammography as an optional second‑reader tool to help radiologists detect breast cancer earlier.

- June 2025: Dharamshila Narayana Superspeciality Hospital in Delhi launched an advanced 3D mammography system to mark Cancer Survivor Month, offering more accurate breast cancer screening with lower radiation exposure.

- January 2025: Siemens Healthineers AG installed the first Mammomat B.brilliant mammography system in the United States at GRACE Breast Imaging & Medical Spa in Iowa.

- December 2024: GE HealthCare introduced the Pristina Via mammography system, designed to improve the screening experience for both patients and technologists by streamlining workflow and lifting diagnostic accuracy.

- October 2024: Siemens Healthineers AG obtained FDA premarket approval for the 3D tomosynthesis portion of its Mammomat B.brilliant mammography system, marking its first fully redesigned platform in over a decade.

- February 2024: Fujifilm Holdings Corporation unveiled AMULET SOPHINITY, a new digital mammography technology, at the European Congress of Radiology (ECR) 2024, emphasizing improved diagnostic accuracy, patient comfort, and workflow efficiency.

REPORT COVERAGE

The report provides an in-depth assessment of all market segments, outlining key growth drivers, emerging trends, opportunities, major restraints, and challenges influencing the industry. It further analyzes technological advancements, radiologist workforce trends, installed base dynamics, and notable industry developments. Additionally, it includes detailed market share analysis, recent product launches, and comprehensive profiles of leading market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, End-user, and Region |

| By Type |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.49 billion in 2025 and is projected to reach USD 4.77 billion by 2034.

In 2025, the market value stood at USD 1.11 billion.

The market is expected to exhibit a CAGR of 7.4% during the forecast period.

The digital segment led the market by type.

The key factor driving the market is the rising incidence of breast cancer.

GE HealthCare, Hologic, Inc., and Siemens Healthineers AG are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us