Marine Cranes Market Size, Share & Russia Ukraine War Impact & Industry Analysis, By Crane Type (Offshore Cranes, Ship Cranes, Port / Harbor Cranes, Floating Cranes, and Others), By Lifting Capacity (Upto 500 Tons, 500 – 3,000 Tons, and Above 3,000 Tons), By Design (Fixed Cranes, and Mobile Cranes), By Power Source (Diesel, Electric, and Hybrid), By Application (Port & Cargo Handling, Offshore Oil & Gas, Offshore Renewable Energy, Government & Defense, Shipbuilding & Repair, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

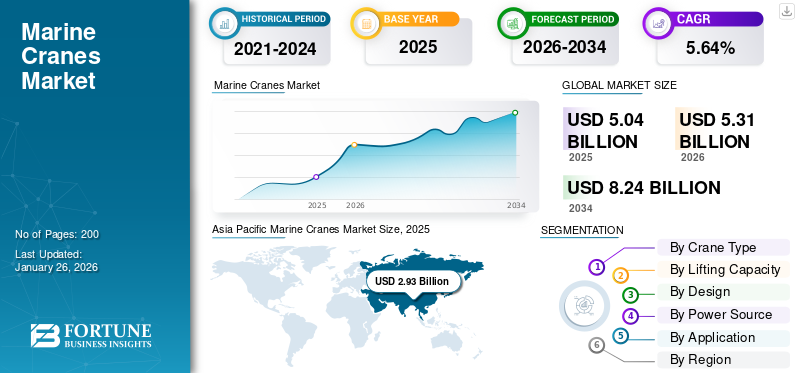

The global marine cranes market size was valued at USD 5.04 billion in 2025. The market is projected to grow from USD 5.31 billion in 2026 to USD 8.24 billion by 2034, exhibiting a CAGR of 5.64% during the forecast period. Asia Pacific dominated the marine cranes market, accounting for 58.14% of the market in 2025.

Marine crane is a lifting equipment which is designed for marine and offshore environments including ships, ports, offshore platforms and floating structures. They are widely used for cargo handling, shipbuilding, offshore oil & gas operations, and offshore wind farm installation. Ship-mounted cranes and offshore heavy-lift cranes are some types of marine cranes.

Key players in the market including Liebherr Group, Konecranes Plc, Cargotec, ZPMC (Shanghai Zhenhua Heavy Industries) are focused on building cranes to withstand harsh maritime conditions such as saltwater corrosion, high humidity, and offshore movement. These companies are increasingly designing space-efficient, high-performance cranes for different end user requirements. In addition, integration of smart technologies and digital tools is gaining traction which is expected to drive the growth of the marine cranes market. Various types of marine cranes including telescopic boom cranes are increasingly favored in the marine cranes market for their adjustable reach and space-saving design.

Download Free sample to learn more about this report.

Impact of Tariff on Global Marine Cranes Market

The marine port industry faces increasing uncertainty from tariffs on Chinese-built cranes introduced by the U.S. in 2025. For instance, in August 2025, The U.S. Commerce Department expanded steel and aluminum tariffs to 407 new product categories, including cranes at a 50% rate.

Moreover, ZPMC of Shanghai, a port crane manufacturer which holds a large share of the global ship-to-shore crane market, is the main supplier to major U.S. ports. The rise in tariffs has increased the procurement costs and is anticipated to surge project costs and potential funding. Smaller ports with limited budgets may delay modernization. Such slowing down of budget allocation is expected to widen efficiency gaps with larger hubs. The higher prices and budget overruns are anticipated to delay or scale back expansion projects of various ports. This, in turn, reduces product demand growth during the forecast period. Therefore, all such factors decline the overall market momentum in the short to medium term, as fewer cranes are ordered and installed in U.S. ports.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Expansion of Ports for Maritime Trade to Propel Market Growth

The marine cranes market growth is driven significantly by the expansion of offshore wind farms and related infrastructure. Countries in Europe, North America, and Asia Pacific region are investing heavily into offshore wind as part of decarburization strategies. For instance, the European Union aims for 60 GW of offshore wind capacity by 2030, while the U.S. targets 30 GW by 2030. Such projects require heavy-lift cranes capable of handling turbine blades, which is expected to drive the demand for marine cranes. Moreover, such activities demand highly specialized cranes with active heave compensation.

In addition, as the global trade volumes are increasing rapidly, the demand to handle containerized cargo has surged. The governments and private operators across the globe are investing heavily in port infrastructure to boost cargo handling capacity.

- For instance, in February 2025, Port of Salalah, Oman completed a USD 300 million expansion boosting capacity from 4.5 million to 6.5 million TEU. This expansion added 10 new STS cranes, 12 hybrid RTGs, and supporting yard/electrical upgrades to handle ultra-large vessels efficiently.

Such expansion and modernization of existing ports is expected to boost automation and electrification which increases the demand for advanced STS (Ship-to-Shore) and RTG (Rubber-Tyred Gantry) cranes.

MARKET RESTRAINTS

High Capital and Maintenance Costs to Restrict Market Expansion

A major restraint affecting the market negatively is high capital expenditure (capex) and maintenance cost associated with cranes used in marine industry. Port cranes, offshore heavy-lift systems, and shipboard cranes require companies to make huge investment around USD 2 million–USD 10 million per unit). Smaller shipping operators and mid-sized ports often struggle to justify such expenses. Furthermore, due to constant exposure of marine equipment to saltwater corrosion, humidity, and heavy loads, the maintenance costs and part replacements are frequent which also results in high maintenance cost. Heave compensation and automation are complex advanced systems that may add to the overall high cost, which in turn hampers the growth of the market.

MARKET OPPORTUNITIES

Increase in Adoption of Electrification and Green Technologies to Create Lucrative Growth Opportunities

The significant opportunity for the market is shifting toward integration of green technology and adoption of electric cranes. As the IMO regulations make it strict carbon-neutral shipping and encourage ports to reduce emissions, crane manufacturers are increasingly focusing on advanced product portfolios that include electric, hybrid, and energy-efficient systems. Moreover, electric cranes are getting popular as they help to reduce fuel costs, lower emissions, and require less maintenance.

- For instance, in May 2025, MacGregor received a contract to supply fully electric cargo cranes for four Vertom vessels being built at Chowgule Shipyard in India, marking its first electric crane project with vessels constructed in the country.

In addition, ports such as Rotterdam and Singapore are moving toward zero-emission cargo handling equipment, creating an increased demand for electric STS and RTG cranes. Such factors result in increased demand for electric-powered cranes to minimize environmental risks presenting lucrative opportunities for the growth of the market.

MARINE CRANES MARKET TRENDS

Emergence of Digitalization, Automation, and Remote Operations is a Significant Market Trend

A significant trend in the cranes industry for marine and offshore applications is the integration of digital technologies, automation, and remote operations. There is an increase in demand for controlling cranes and other marine equipment from safe, centralized offices. Therefore, ports are investing in adoption of smart port cranes which are semi or fully autonomous. Moreover, numerous ports are moving toward remote-controlled STS and RTG cranes to improve operator safety.

- For instance, in June 2025, The Port of Neom received its first shipment of remote-controlled container handling cranes, including Ship-to-Shore and Electric Rubber-Tyred Gantry units, as part of preparations for the 2026 launch of Terminal 1. The cranes are intended to enable high-efficiency operations and accommodate large container vessels.

In addition, incorporation of smart remote maintenance systems that use IoT sensors for predictive analytics, minimizing downtime has increased, which is anticipated to fuel the market growth during the forecast period.

MARKET CHALLENGES

Supply Chain Disruptions to Hamper Market Growth

A critical challenge to the market is global supply chain disruption. The important maritime chokepoints such as the Panama Canal, Suez Canal, and Red Sea are under pressure due to climate impacts, geopolitical crises, and drought. Therefore, this is causing significant route diversions and shipment delays resulting in long vessel wait times. Such delays increase costs and fuel expenses and extend lead times for marine crane shipments. This leads to delaying of port modernization and expansion projects, which is expected to present challenges for the manufacturing and contracts of cranes for marine industry.

Download Free sample to learn more about this report.

Segmentation Analysis

By Crane Type

Rise in Global Trade and Increase in Demand for High Capacity Cranes Contributed to Segmental Growth

On the basis of the segmentation of crane type, the market is classified into offshore cranes ship cranes, port / harbor cranes, floating cranes, and others. Port or harbor cranes comprises of ship-to-shore (STS) cranes, mobile harbor cranes, gantry cranes (RTG, RMG). The cranes in others sub-segment include deck cranes, specialized cranes, and others.

The port/harbor cranes segment accounted for the largest marine cranes market share 51.11% in 2026. The segment growth is attributed to a surge in global container trade and increase in demand for cranes to handle large and high capacity vessels smoothly and efficiently. Moreover, ports are investing in port harbor cranes to handle large volumes of containers and bulk cargo.

- For instance, in January 2025, Pilbara Ports ordered two 200-ton Konecranes Gottwald ESP.9 Mobile Harbor Cranes for Port Hedland to increase capacity at the world’s largest bulk export port.

Offshore cranes segment is the fastest growing segment in the market during the forecast period due to adoption of new generation offshore support vessels which requires automated cranes. In addition, an increase in projects for oil exploration is expected to drive demand for the segment.

By Lifting Capacity

Rise in Port Projects and Offshore Construction Fueled Growth of upto 500 tons Segment

In terms of lifting capacity, the market is categorized into upto 500 tons, 500 – 3,000 tons, and above 3,000 tons.

The upto 500 tons segment captured the largest share 59.84% of the market in 2026. Cranes with lifting capacities up to 500 tons are significantly in demand to handle heavier cargo and oversized shipments efficiently at modern ports and shipyards. In addition, increase in port infrastructure projects and offshore construction is driving growth of the segment.

- For instance, HD Hyundai Heavy Industries announced installation of two Liebherr BOS 4200 offshore cranes on a Floating Production Unit (FPU). And the cranes designed are capable of lifting up to 44 tons.

The 500 – 300 tons segment is growing moderately due to rising upgrading of cranes for increasing lifting capacity and operational flexibility.

- For instance, in November 2023, Huisman, heavy lifting equipment manufacturer contracted to upgrade the second crane on Heerema’s Aegir heavy lift vessel from 2,000 to 3,200 tons, enhancing its capacity for large offshore installations.

The above 3,000 tons is expected to be the fastest growing segment due to rising upgrading of cranes for increasing lifting capacity and operational flexibility. There is a rise in demand for single-lift installation to cut project time and risk, which then requires cranes with higher lifting capacity.

By Design

Ability to Handle Large Quantity of Cargo at Ports & Offshore Sites Supported Fixed Cranes Segment Growth

Based on design, the market is segmented into fixed cranes and mobile cranes.

The fixed cranes segment held the dominating position with a share of 54.91% in 2026, as they are installed at ports and offshore sites for continuous, high-capacity operations, handling large volumes of cargo and heavy loads efficiently. Their stability and durability make them the preferred choice for long-term infrastructure projects.

The mobile segment is anticipated to be the fastest growing segment during the forecast period. The segment is growing as there is increase in deployment of mobile cranes for on-site flexibility and component handling in constrained marine environments.

By Power Source

Surge in Need for Heavy Duty Marine Cranes for Continuous Operation Propelled Segment Growth

Based on power source, the market is segmented into diesel, electric, and hybrid

The diesel cranes accounted for the largest share in the market as they are widely deployed across a large number of ports and offshore sites across the globe. Diesel systems are increasingly preferred for supporting heavy lifting in continuous operations.with a share of 49.96% in 2026

In 2026, the electric segment held the second largest share in the market, due to increasing demand for sustainable and energy efficient solutions. Introduction of stricter emission regulations and green initiatives in port shipping is driving the adoption of electric cranes.

- For instance, in July 2025, Port Nelson commissioned New Zealand’s first electric dual-drive mobile harbor crane, the Liebherr LHM600E, as part of its strategy to reduce emissions and modernize port infrastructure.

To know how our report can help streamline your business, Speak to Analyst

By Application

Increase in Need for Cranes for Handling Port Cargo for Space Monitoring Propelled Segment Growth

Based on application, the market is segmented into port & cargo handling, offshore oil & gas, offshore renewable energy, government & defense, shipbuilding & repair, and others.

In 2024, the port & cargo handling segment maintained the largest share in the market owing to the large number of marine crane deployments at ports to handle huge volumes of cargo. Moreover, the continuous global trade growth and port expansions drive steady demand for STS, RTG, and mobile harbor cranes.

- For instance, in January 2025, DP World announced a USD 1 billion investment to expand port infrastructure in Peru. The port expansion is expected to drive demand for new marine cranes to handle increased cargo volumes efficiently.

Offshore renewable energy is the fastest-growing segment during the forecast period. The rise in size of turbines, deeper water installations, and global decarburization targets are driving demand for specialized heavy-lift offshore cranes.

Marine Cranes Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

ASIA PACIFIC

Asia Pacific Marine Cranes Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The market in Asia Pacific reached USD 2.93 billion in 2025, representing 58.14% of total market revenue, and is projected to reach USD 3.11 billion in 2026. The Asia Pacific region held the dominant share and is expanding rapidly. The market in Asia Pacific is witnessing significant growth due to dominance in global shipping and trade volumes. Rapid expansion of ports in countries such as China, India, and Southeast Asia experience increased demand for cargo handling cranes. China’s Belt and Road Initiative is also fostering large-scale infrastructure and port development. The region leads global shipbuilding activity, particularly in South Korea, China, and Japan, which drives crane installations in shipyards and offshore projects.The Japan market is projected to reach USD 0.39 billion by 2026, the China market is projected to reach USD 1.55 billion by 2026, and the India market is projected to reach USD 0.29 billion by 2026.

- For instance, in June 2025, Huisman announced that it will supply two knuckle boom cranes to Olympic Subsea’s new sustainable energy vessels, built by CMHI in Shenzhen for offshore and subsea construction projects.

EUROPE

In 2025, Europe held 16.17% of the global market, reaching a valuation of USD 0.82 billion, and is projected to grow to USD 0.85 billion in 2026. Europe is anticipated to witness a notable growth during the forecast period. Countries across the region such as Germany, the U.K., and the Netherlands are witnessing establishment of wind farms which is expected to boost the demand for heavy-lift offshore cranes. The region has a large number of shipbuilding hubs in countries such as Italy and Spain and is expected to contribute to crane demand for vessel construction and maintenance. In addition, players in the region are launching new and advanced cranes for various purposesThe UK market is projected to reach USD 0.17 billion by 2026, while the Germany market is projected to reach USD 0.21 billion by 2026.

- For instance, in September 2024, PALFINGER MARINE launched the PFM 2100, a heavy-duty foldable knuckle boom crane with its patented P-Profile, offering superior lifting capacity, 29m outreach, and lightweight design.

NORTH AMERICA

The North America market was valued at USD 0.74 billion in 2025, capturing 14.64% of global revenue, and is estimated to reach USD 0.77 billion in 2026. The North America region is witnessing steady growth in the market. The market is due to expansion of trade volumes and is fueling the demand for ship-to-shore (STS) and rubber-tired gantry (RTG) cranes. Moreover, the offshore oil and gas exploration activities being carried out by the Gulf of Mexico push the need for heavy-lift and offshore. The expanding offshore wind energy sector is also stimulating demand for specialized cranes in the region.The U.S. market is projected to reach USD 0.64 billion by 2026.

- For instance, in August 2025, the American Association of Port Authorities (AAPA) backed Washington’s move to revive U.S. ship-to-shore crane manufacturing, reducing dependency on Chinese imports. This supports the market by enhancing competition, diversifying suppliers, and accelerating innovation in the market.

LATIN AMERICA & MIDDLE EAST & AFRICA

Latin America maintained a strong presence in the global market, reaching USD 0.2 billion in 2025, accounting for 3.92% share, and is expected to reach USD 0.2 billion in 2026.During the forecast period, Latin America and Middle East & Africa regions would witness a moderate growth in this market space. There is an increase in export of commodities such as minerals, oils, agricultural products which push the cargo handling. Moreover, the offshore and gas industry in deep-water exploration is driving the demand for offshore cranes. In addition, the huge investments by container terminals for procurement of cranes are creating opportunities for STS and RTG crane installations.

- For instance, in April 2024, Konecranes secured an order from Brazil Portonave, a first private container terminal in Brazil for 14 fully electric RTGs, set for delivery in 2026.

In 2025, the Middle East & Africa market stood at USD 0.36 billion, representing 7.13% of global demand, and is projected to grow to USD 0.38 billion in 2026. For the Middle East region, offshore projects in the Persian Gulf and Red Sea are driving the adoption of heavy-duty offshore cranes. In addition, the rise in crane procurement due to port infrastructure development in Gulf Cooperation Council (GCC) countries, such as the UAE and Saudi Arabia is stimulating further growth of the market in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Port Expansion, Offshore Energy Projects, and Strategic Collaborations with Maritime Technology Providers Supports Market Expansion of Key Players

The global marine cranes market is influenced by increasing seaborne trade, large-scale port modernization programs, and rising investments in offshore oil & gas projects and rising demand for renewable energy. Key players in this market include Shanghai Zhenhua Heavy Industries (ZPMC), Liebherr Maritime Cranes, Konecranes, Cargotec Corporation (MacGregor), and Sany Heavy Industry, among others, each contributing in the market through innovative lifting solutions for ports, shipyards, and offshore platforms.

Companies offer a wide portfolio of products such as ship-to-shore cranes, rubber-tired gantry cranes, mobile harbor cranes, and offshore heavy-lift cranes tailored for cargo handling, shipbuilding, and energy operations. Moreover, for market expansion, the key players are increasingly investing in automation technologies, electrification of cranes, and digital solutions for predictive maintenance. In addition, port authorities and offshore developers are partnering with crane manufacturers to expand global footprints and improve service networks.

LIST OF KEY MARINE CRANES COMPANIES PROFILED

- Shanghai Zhenhua Heavy Industries Co., Ltd. (ZPMC) (China)

- Liebherr Group (Switzerland)

- Konecranes Plc (Finland)

- Cargotec Corporation (MacGregor & Kalmar) (Finland)

- Sany Heavy Industry Co., Ltd. (China)

- TTS Group ASA (part of MacGregor) (Norway)

- Manitowoc Cranes (U.S.)

- DMW Marine Group (U.S.)

- Heila Cranes (Italy)

- PALFINGER Marine (Austria)

- KenzFigee (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Liebherr will deliver eight LS 250 heavy-lift ship cranes to ship Carriers’ four newbuild vessels by 2026, enhancing fleet cargo handling capacity.

- March 2025: Techano Oceanlift, a subsidiary of Nekkar ASA, will deliver a 150-ton knuckle boom crane with active heave compensation to a new construction support vessel being built at Turkey’s Sefine Shipyard for Agalas, Eidesvik, and Reach Subsea.

- January 2025: The Port of Tilbury added a third Liebherr LHM 550 mobile harbour crane to boost cargo handling capacity and support new industrial operations.

- December 2024: SCCT received four Super Post-Panamax quay cranes and six electric RTG cranes as part of its terminal expansion, boosting capacity for heavy lifts and twin-container handling.

- August 2024: Palfinger Marine will deliver 108 fixed boom service cranes, including 107 fully electric PF120 units, for the Baltica 2 offshore wind farm in Poland. Deliveries are scheduled from September 2025 to March 2026, supporting turbine installation and training operations.

- October 2024: Huisman will deliver a 100-ton pedestal mounted crane to Eastern Navigation’s Asia Pacific offshore support fleet, marking their fifth crane for the company.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.64% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Crane Type · Offshore Cranes · Ship Cranes · Port / Harbor Cranes o Ship-to-Shore (STS) cranes o Mobile Harbor Cranes o Gantry Cranes (RTG, RMG) · Floating Cranes · Others |

|

By Lifting Capacity · Upto 500 Tons · 500 – 3,000 Tons · Above 3,000 Tons |

|

|

By Design · Fixed Cranes · Mobile Cranes |

|

|

By Power Source · Diesel · Electric · Hybrid |

|

|

By Application · Port & Cargo Handling · Offshore Oil & Gas · Offshore Renewable Energy · Government & Defense · Shipbuilding & Repair · Others |

|

|

By Region · North America (By Crane Type, By Lifting Capacity, By Design, By Power Source, By Application, and Country) o U.S. (By Crane Type) o Canada (By Crane Type) · Europe (By Crane Type, By Lifting Capacity, By Design, By Power Source, By Application, and Country) o U.K. (By Crane Type) o Germany (By Crane Type) o Netherlands (By Crane Type) o Italy (By Crane Type) o Spain (By Crane Type) o Rest of Europe (By Crane Type) · Asia Pacific (By Crane Type, By Lifting Capacity, By Design, By Power Source, By Application, and Country) o China (By Crane Type) o India (By Crane Type) o Japan (By Crane Type) o Australia (By Crane Type) o South Korea (By Crane Type) o Singapore (BY Crane Type) o Rest of Asia Pacific (By Crane Type) · Latin America (By Crane Type, By Lifting Capacity, By Design, By Power Source, By Application, and Country) o Brazil (By Crane Type) o Chile (By Crane Type) o Colombia (By Crane Type) o Rest of Latin America (By Crane Type) · Middle East & Africa (By Crane Type, By Lifting Capacity, By Design, By Power Source, By Application, and Country) o UAE (By Crane Type) o Saudi Arabia (BY Crane Type) o Egypt (By Crane Type) o South Africa (By Crane Type) · Rest of Middle East & Africa ( By Crane Type) |

Frequently Asked Questions

The global marine cranes market size was valued at USD 5.04 billion in 2025. The market is projected to grow from USD 5.31 billion in 2026 to USD 8.24 billion by 2034.

In 2025, the market value stood at USD 0.74 billion.

The market is expected to exhibit a CAGR of 5.64% during the forecast period of 2026-2034.

The space based segment led the market by port cranes.

The key factors driving the market are growth of offshore wind & renewable projects and rise in expansion of ports.

Shanghai Zhenhua Heavy Industries (ZPMC), Liebherr Maritime Cranes, Konecranes, Cargotec Corporation (MacGregor), and Sany Heavy Industry and others are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us