Port Equipment Market Size, Share & Russia Ukraine War Analysis, By Equipment Type (Cranes, Forklifts, Automated Guided Vehicles, Tugboats, Terminal Tractors/Yard Tractors, Straddle Carriers, and Others), By Fuel Type (Gasoline, Diesel, Electric-Powered, Hybrid, and Others), By Application (Container Handling, Bulk Handling, Ship Handling, and Others), By Mode of Operation (Manual and Automated), By Solutions (Port Software and Port Equipment), By Port Type (Brownfield and Greenfield), By End User (Port Authorities, Terminal Operators, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

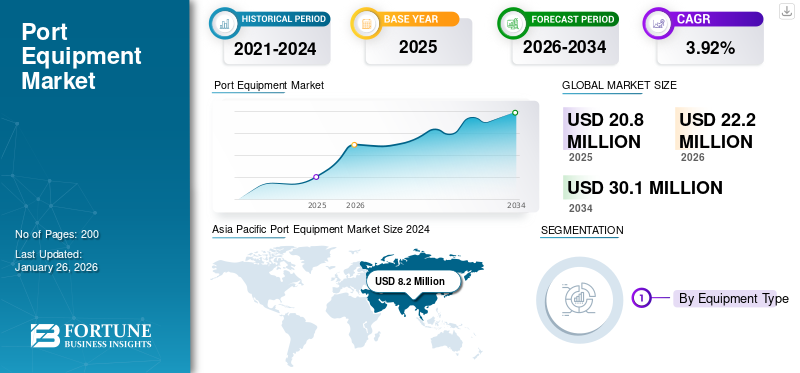

The global port equipment market size was valued at USD 20.8 million in 2025 and is projected to grow from USD 22.2 million in 2026 to USD 30.1

billion by 2034, exhibiting a CAGR of 3.92% during the forecast period. Asia Pacific dominated the port equipment market with a market share of 39.47%% in 2025.

Port equipment includes machinery and vehicles used to perform cargo handling and transport/ movement of goods at ports & terminals. The equipment used in maritime port operations comprises cranes, stackers, rubber tired gantry (RTG), rail mounted gantry (RMG), automated guided vehicles, terminal tractors, forklifts, loaders, conveyors, and hopper feeders, among others. Ports need a wide range of equipment for material handling and ensuring smooth operations of port facility. The equipment is powered by different types of fuel such as diesel and gasoline. Electric and hydrogen powered equipment are also used to reduce emissions and the contribution to climate change.

Download Free sample to learn more about this report.

Key players in the market are Liebherr, Kalmar Corporation, Konecranes, Shanghai Zhenhua Heavy Industries (ZPMC), and others. Major companies are focused on manufacturing efficient and reliable port machinery and vehicles according to the various cargo handling needs of port authorities. They are involved in the development of a wide range of products including mobile harbor cranes, ship-to-shore cranes, reachstackers, and other equipment for both seaports and inland harbors. Moreover, some companies such as Konecranes offer various port solutions to improve handling operations and their productivity and safety. Industry players are also focused on manufacturing advanced equipment integrated with automation and intelligent technologies. For instance, in 2023, ZPMC revealed 14 products in port machinery and offshore engineering including next-generation horizontal transport trolley, automated rail-mounted gantry crane, and eco-friendly and low-carbon lightweight quay crane, and other equipment.

Download Free sample to learn more about this report.

Impact of Russia Ukraine War on Port Equipment Market

Disruption of Trade Routes and Supply Chains amid the War May Affect Industry Expansion

The Russia Ukraine War has severely affected various industries in the world including the maritime sector. Commercial shipping is impacted by the war and it has resulted in the disruption of port operations and shipping. Terminals and port infrastructure are increasingly getting targeted and destroyed in this conflict. For instance, 321 Ukrainian port infrastructure facilities were damaged by the drones and missiles of Russia. The inaccessibility of such ports has caused a disruption in the trade of grain and other agricultural products across the globe. Such factors also encourage the use of alternative routers, mostly longer routes, which leads to an increase in fuel consumption and higher price shipments. Therefore, high shipping prices can negatively impact the market by potentially decreasing cargo volumes and reducing the need for new equipment.

In addition, sanctions imposed on Russia, particularly those impacting maritime activities and trade, significantly affect the market. Restrictions on Russian vessels, prohibitions on port access, and limitations on the provision of maritime services disrupt established trade routes and supply chains, leading to a decreased demand for port equipment. However, although the war has severely impacted the port industry, there have been numerous efforts and rebuilding strategies made by countries involved in the war. For instance, in June 2025, Ukraine announced an urgent need for at least around USD 566 million to begin rebuilding vital port infrastructure along the Black Sea coast. Such initiatives are expected to help the port industry recover and fuel the growth of the market.

Market Dynamics

Port Equipment Market Trends

Equipment Electrification to Emerge as a Key Trend during the Forecast Period

The conventional port machinery is extensively used in by various ports. However, the electrical version of port equipment is gaining popularity due to environmental concerns and emission reduction. Battery-powered port machinery offers high efficiency and cost efficiency compared to traditional fuel powered equipment. The electrification of equipment required at ports reduces air and noise pollution, lowers operational costs through improved energy efficiency and reduced maintenance, and enhances compliance with environmental regulations.

Numerous port authorities are adopting electric powered port handling equipment for reducing carbon emissions. For instance, in March 2025, Saguenay Port Authority, Quebec placed an order to Konecranes for electric-driven Konecranes Gottwald ESP.6B Mobile Harbor Crane for cargo handling application. The order was made by the authority to reduce carbon footprint and improve port handling with increasing cargo traffic.

In addition, there is also an increasing trend of retrofitting existing traditional equipment to electric driven models. This transition is highly being promoted owing to the broader environmental initiatives and sustainability goals. Moreover, retrofitting can extend the life of existing equipment, delaying the need for costly replacements. For instance, in 2023, APM Terminals announced plans to invest USD 60 million port-equipment electrification trials. Under this initiative, the port operating company aims to purchase or retrofit more than 2,650 pieces of electric heavy port equipment. Such developments, focused on achieving 100% carbon neutrality by escalating the adoption of electric port machinery, is expected to propel the growth of the market significantly during the forecast period.

Market Drivers

Rise in Maritime Trade across the Globe to Propel Market Growth

There is an increase in maritime trade worldwide due to various factors such as the sourcing of raw materials from different countries, rise in e-commerce, and economic growth in developing countries. The maritime transport has significantly increased owing to a strong demand for bulk commodities such as iron ore, coal, and grains. According to the International Maritime Organization (IMO), maritime trade recorded a 5% increase in 2024 compared to the year 2023, driven by e-commerce and growth in manufacturing. Maritime trade volumes reached 12,292 million tons in 2023, an increase of 2.4%, after contracting in 2022.

Furthermore, the rise in international trade has resulted in need for more equipment to transport and handle the increased volume of goods. The port authorities require a wide variety of cargo handling equipment such as cranes, reach stackers, and automated guided vehicles. Various port companies and logistics providers are purchasing advanced equipment to efficiently handle large volumes of cargo. For instance, in April 2025, Salerno Container Terminal (SCT), Italy, placed an order for electric Konecranes Gottwald ESP.10 Mobile Harbor Crane for container handling of super post-Panamax vessels of up to 15,000 TEUs and 22 rows. Therefore, the surge in maritime trade has significantly increased the demand for advanced and efficient equipment for cargo handling and transportation at ports, further driving the port equipment market growth.

Market Restraints

High Capital Investment and Maintenance Costs May Hinder Market Growth

The procurement of some port machinery such as ship-to-shore cranes and rubber tyred gantry cranes (RTG) is expensive due to complex technology and high initial investment. The cost of building and installation of large cranes or specialized tailor made equipment for container handling requires high capital investment. Moreover, some advanced equipment often incorporates automated technologies and software integration which eventually increases the manufacturing and operational cost affecting the overall cost of the equipment. In addition, the large scale cranes are equipped with advanced safety features and operational capabilities which can significantly surge the cost. Sophisticated software systems and smart port equipment technologies that are essential for managing port operations are expensive to design, develop, and implement on ports. All such factors are expected to hamper the growth of the market during the forecast period.

Market Challenges

Raw Material Price Increase and Infrastructure Limitations Pose as a Significant Challenge for the Market

Port equipment such as cranes, straddle carriers, automated guided vehicles (AGVs), and reach stackers rely heavily on steel, copper, aluminum, lithium, and other materials. Increase in material costs has affected the price of the equipment which results in more expensive quay cranes, terminal tractors, and other machineries. In addition, port infrastructure requires maintenance and constant upgrades. However, port infrastructure is facing problems such as limited dock space, outdated equipment, insufficient storage facilities, and others. These critical issues are expected to result in further problems such as congestion, delays, and increased operational costs. Therefore, these factors are expected to act as challenges for market growth.

Market Opportunities

Rise in Port Expansion and Modernization Projects to Drive Market Growth Opportunities

The global trade is witnessing significant rising which has increased the demand for more efficient port facilities to handle large capacity of cargo. This expansion includes both Greenfield and Brownfield projects to accommodate rising trade volumes. For instance, in May 2025, DP World announced its investment plans of USD 2.5 million in port infrastructure development for the expansion of its logistics network. Through this plan, the company aims to launch major port infrastructure projects across India, Africa, South America, and Europe. Such expansion plans to meet the large volumes of cargo are expected to increase the demand for a wide range of equipment for port handling.

Moreover, the governments of various countries aid the port expansion plans to increase its productivity and to reduce logistics challenges. For instance, in June 2025, the U.K. government announced plans to support the port expansion project to drive economic growth. Moreover, the Southampton Port announced plans to invest USD 41.1 million in equipment such as four cranes for ship container handling.

In addition, the ongoing terminal expansion plans are also promoting strategic collaborations and contracts between port authorities and equipment manufacturers. In May 2024, APM Terminals announced major terminal expansion projects such as Suez Canal Container Terminal, APM Terminals Maasvlakte II, Côte d’Ivoire Terminal, APM Terminals MedPort Tangier, APM Terminals Lazaro Cardenas, and the upcoming terminal in Suape, Brazil. Therefore, the company invested in 240 pieces of container handling equipment ranging from ship-to-shore cranes to electric terminal tractors and rubber tyred gantry cranes. Furthermore, the development of green ports and rise in sustainability focus is also increasing the emphasis on the adoption of eco-friendly port machinery. All such developments promoting the increasing rate of port infrastructure and terminal expansion are expected to present significant opportunities for the growth of the market.

Segmentation Analysis

By Equipment Type

Cranes Segment Held the Largest Market Share Due to Increase in the Demand for Robust & Efficient Cranes for Cargo Handling

On the basis of equipment type, the market is classified into cranes, forklifts, automated guided vehicles (AGVs), tugboats, terminal tractors/yard tractors, straddle carriers, reach stackers, mooring system, conveyors & belt systems, and others. The terminal tractors/yard tractors segment is projected to account for 14.78% of the market.

The cranes segment held the largest share in the port equipment industry. The segment includes ship to shore (STS) cranes, rubber tired gantry (RTG) cranes, rail mounted gantry (RMG) cranes, mobile harbor cranes, container gantry cranes, and others. The dominance of the segment is due to an increase in the demand for robust and reliable cranes for loading and unloading cargo at ports. Numerous ports are investing in a range of port machinery especially ship to shore cranes to meet the growing number of vessels and perform efficient cargo handling. For instance, in January 2025, the Port of Savannah received four electric ship-to-shore cranes for accommodating large vessels in the U.S. East Coast.

The automated guided vehicles segment is expected to grow at the fastest rate during the forecast period. The segment is expected to grow in future due to an increase in the need for automation to enhance efficiency and safety in port operations. Automated systems are being preferred more as they are capable of optimizing and regulating traffic flow and avoid congestion. For instance, in August 2023, Westports Malaysia announced plans to integrate electric automated guided vehicles into its port equipment fleet. The port also aims to establish automated charging solutions and required infrastructure for AGVs.

By Application

Container Handling Segment Held the Largest Market Share Due to a Surge in Maritime Trade

On the basis of application, the market is classified into container handling, bulk handling, ship handling, and others.

The container handling segment dominated the global market with a market share of 56.69% in 2026. The dominance of the segment is owing to a rise in maritime trade across the globe and huge investments in the expansion of port infrastructure and terminal construction to meet increased trade demand. Port operators have launched significant port infrastructure expansion projects. For instance, in June 2025, DP World unveiled plans for an expansion project for port infrastructure worth USD 2.5 billion. Newer infrastructure allows for the integration of advanced technologies such as automated cranes, smart logistics systems, and digital solutions. In addition, improved infrastructure is able to handle larger ships and more cargo, requiring more efficient and powerful equipment which drives the segment growth.

To know how our report can help streamline your business, Speak to Analyst

By Fuel Type

Diesel Segment to Hold the Largest Share Due to High Power Output & Low Initial Investment

On the basis of fuel type, the market is classified into gasoline, diesel, electric-powered, hybrid, LPG/LNG powered, and hydrogen fuel cell.

The diesel segment is expected to contribute 59.11% of the market as it is so far the most commonly used type of fuel for port machinery, especially in cargo and bulk handling. The segment acquires the largest share in the market as this fuel type is mostly preferred for large and heavy duty equipment such as container handlers, reach stackers, and others. Moreover, major ports across the globe already possess required infrastructure for the installation and implementation of diesel powered equipment. This factor is driving partnerships of port authorities with equipment manufacturers for diesel powered machinery. For instance, in January 2025, Kalmar inked an agreement with MPDC (Maputo Port Development Company) to supply one Kalmar medium forklift truck, four Kalmar heavy forklift trucks, and five diesel powered Kalmar T2i terminal tractors. In addition, lower initial investment costs compared to electric alternatives is also driving the growth of the segment.

The electric segment is estimated to grow at the fastest CAGR over the forecast period. The segment is expanding rapidly due to various factors such as focus on sustainability, stringent emission norms, and maritime decarbonization goals. The government bodies and port associations establish regulatory norms to cut greenhouse gas emissions and meet sustainability goals. These efforts are expected to encourage ports to switch to electric equipment for cargo handling and other port operations. Thus, there is an increase in the replacement of conventional fuel powered equipment with electric models to reduce carbon emissions. For instance, in June 2026, APM Terminals signed an agreement with SANY Marine to replace 500 diesel powered vehicles with the supply of battery electric terminal tractors by 2030.

By Mode of Operation

Manual Segment Holds the Largest Market Share Due to its Cost Effectiveness and Ease of Use

On the basis of mode of operation, the market is classified into manual and automated.

The manual segment dominated the global market with a market share of 13.5% in 2026.

due to the increasing adoption of manual equipment is as it is significantly cheaper as compared to equipment with automated technology. Moreover, in regions with emerging economies, manual equipment is preferred as there is ready availability of manual labor. In addition, manual port machinery is easy to use and is cost effective, making it a suitable option for a large number of small & medium sized ports.

The automated segment is estimated to be the fastest-growing segment owing to an increase in the demand for high operational efficiency and increase the speed of port operations. For instance, in March 2023, Ouster and LASE GmbH announced an agreement for automating and retrofitting crane systems and container terminals at ports with 3D digital LiDAR sensors. Automated equipment provides end users with reduce turnaround times and least human error. Such advantages are expected to boost the growth of the segment.

By Solutions

Port Equipment Segment Holds the Largest Market Share Rise in Maritime Trade & Need for Replacement of Aging Equipment

On the basis of solutions, the market is classified into port software and port equipment.

The port equipment segment captures the largest share in the market due to an increase in the procurement contracts of port machinery to perform cargo handling of increased volumes of cargo. Moreover, there is a rise in need for the replacement of aging and outdated equipment with modern, fuel efficient, and automated equipment. In addition, the need to handle diverse cargo types is increasing the need for procuring specialized equipment. Therefore, all such factors are expected to propel the growth of the segment during the forecast period.

The port software segment is estimated to be the fastest-growing segment. The software includes systems that are installed in the equipment to optimize and streamline operations. These are integrated into port equipment to handle port activity, manage port resources, and regulate cargo handling. The segment is growing as there is an increase in the demand for software solutions to streamline port operations. For instance, in January 2024, Verbrugge International BV, a Dutch Logistics Service Provider purchased software solutions from Konecranes to simplify port and inland terminal operations. Some key players in the market also provide port software along with equipment for the efficient transport and storage of containers on the ports. For instance, companies such as Konecranes offer software for automated container handling which can also be integrated with existing systems.

By Port Type

Brownfield Segment Holds the Largest Market Share Due to Rise in Port Terminal Expansion and Upgrade

On the basis of port type, the market is classified into brownfield and greenfield.

The brownfield segment dominates the market and is estimated to be the fastest-growing segment. The segment is growing due to rise in the upgradation and expansion of existing terminals to handle more cargo using modern equipment. Numerous ports across the globe are upgrading outdated infrastructure and equipment for existing terminals to enhance productivity, safety, and compliance with the environmental standards. For instance, in August 2024, St. Vincent and the Grenadines Port Authority (SVGPA) signed a contract with Konecranes Gottwald ESP.7 Mobile Harbor Crane to support the container and cargo handling capacity in its new terminal opening in 2025.

By End User

Port Authorities Segment Holds the Largest Market Share Due to Favorable Government Initiatives and Modern Equipment Investment

On the basis of end user, the market is classified into port authorities, terminal operators, and logistic providers.

The port authorities segment dominates the market as there is an increase in government initiatives and investment in modern port equipment. The port authorities are supported by government through various efforts. The ports are increasingly investing in modern equipment such as automated cranes, electric RTGs, and advanced terminal tractors. Moreover, with a rise in global trade volumes, port authorities and terminal operators are witnessing pressure to modernize the equipment fleet to reduce congestion and conduct port operations efficiently. For instance, in February 2024, South Carolina Inland Port Greer upgraded its equipment fleet with two hybrid Konecranes hybrid rubber-tired gantry cranes (RTGs) for port operation.

The logistics providers segment is growing at the fastest CAGR over the forecast period due to private investment in terminal operations and a rise in need for electrification of conventional equipment. Logistics companies are investing in port handling equipment with advanced features and automated technology to boost competitiveness. Moreover, logistic firms are focused on replacing aging equipment or traditional fuel powered machinery with new advanced electric versions to reduce carbon footprint. For instance, in May 2024, Luka Koper, logistics firm ordered four Konecranes electric Rubber-Tired Gantry (RTG) cranes to replace old RTGs in its container yard.

Port Equipment Market Regional Outlook

On the basis of region, the market has been studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

Asia Pacific

Asia Pacific Port Equipment Market Size 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific currently holds the largest market share. Asia Pacific is a leading region in the market primarily due to the high trade volume and increased container traffic. The region is home to some of the busiest ports namely Shanghai, Singapore, Busan, and others. These ports handle large volumes of containers and cargo, creating strong and sustained demand. Increase in trade volumes in port equipment is expected to drive the growth of the Asia Pacific market. Moreover, manufacturers in the region are collaborating with international and domestic customers for the supply of advanced equipment to increase their market presence. For instance, in March 2024, Huadong Heavy Machinery signed a contract worth USD 194 million for intelligent port equipment from domestic and overseas clients. In addition, the governments of various countries in the region are supporting expansion programs with the help of initiatives such as China’s Belt & Road Initiative, the Sagarmala Project of India, and others. The India market is projected to reach USD 1.7 million by 2026. The Asia Pacific region captured 39.47% of the global market in 2025, generating USD 8.2 million in revenue, and is projected to reach USD 8.8 million in 2026.

North America

The market in North America is growing with a moderate rate due to replacement of old and outdated equipment and infrastructure upgrades. Moreover, leading ports are integrating new advanced technologies such as automation and smart port technologies which is expected to boost the product demand. In addition, the region experiences strict environmental regulations in coastal areas and ports, which is stimulating the need for zero emission equipment and electric equipment infrastructure. For instance, in April 2025, the Port of Long Beach, California announced a huge investment of USD 3.2 million over the next 10 years to upgrade its infrastructure and focus on sustainability. This effort includes funding for zero-emission (ZE) trucks and other initiatives aimed at improving cargo handling efficiency and environmental impact. The U.S. market is projected to reach USD 4.8 million by 2026. North America contributed approximately USD 5.3 million to the global market in 2025, accounting for 25.66% share, and is expected to reach USD 5.7 million in 2026.

Latin America

Latin America recorded a market size of USD 1 million in 2025, capturing 4.67% of the global market share, and is projected to reach USD 1 million in 2026.

Middle East & Africa

In the Middle East, countries such as UAE, Saudi Arabia, and Qatar are investing in world class port infrastructure. Major projects in the region such as King Abdulaziz Port, Hamad Port, Jebel Ali Port Expansion, and others are anticipated to bring opportunities for equipment manufacturers. In addition, the privatization of ports in the Middle East countries is expected to push investment in modern equipment to achieve operational efficiency and to speed up the port operations. For instance, in June 2025, Saudi Ports (Mawani) signed critical contracts for privatizing multipurpose cargo terminals at eight ports. In Africa, the upgrading of ports to handle large vessels and investment in port equipment to improve efficiency drives the market growth. For instance, in January 2025, Maputo Port Development Company (MPDC), Mozambique, Africa contracted with Kalmar for the supply of five Kalmar T2i terminal tractors to conduce maritime operations. In 2025, Middle East & Africa generated USD 1.9 million, contributing 9.26% to global market revenue, and is projected to grow to USD 2 million in 2026.

Europe

The UK market is projected to reach USD 0.5 million by 2026, while the Germany market is projected to reach USD 1.2 million by 2026. In 2025, the Europe market stood at USD 4.4 million, representing 20.93% of global demand, and is projected to grow to USD 4.7 million in 2026.

Latin America

Countries in the Latin America region are witnessing higher demand for container & bulk material handling, which further accelerates the need for necessary equipment at ports. Countries such as Mexico & Brazil are experiencing increased e-commerce and manufacturing exports. This drives the demand for efficient equipment at ports and terminal operation software to effectively handle large volumes of cargo.

Competitive Landscape

Key Market Players

Key Players Focus on Investment in Research & Development and Strategic Partnerships to Enhance Their Market Presence

The market is highly competitive, driven by a rise in maritime trade and port expansion and upgrading programs. The industry is influenced by various trends such as automation, electrification, and digitization. Companies adopt numerous strategies such as contracts, product launch, agreements, expansion, and acquisition to increase their port equipment market share. Industry participants such as Konecranes, Liebherr, Kalmar, and others focus on the development of high quality, durable, and energy efficient port machinery to handle a variety of cargo. Kalmar and Konecranes aim to manufacture electrified and automated equipment including hybrid carriers and electric terminal tractors due to their strong focus on sustainability. Overall, companies focus on aspects such as innovation, integration, and long term cost efficiency for equipment manufacturing.

LIST OF KEY PORT EQUIPMENT COMPANIES PROFILED

- Konecranes (Finland)

- Kalmar (Finland)

- Shanghai Zhenhua Heavy Industries Company Limited (ZPMC) (China)

- Liebherr Group (Switzerland)

- Hyster-Yale Group (U.S.)

- SANY Heavy Industry Co., Ltd. (China)

- Toyota Material Handling Equipment, Inc (Japan)

- J.C. Bamford Excavators Limited (U.K.)

- Elecon Engineering Company Limited (India)

- Banner Engineering (U.S.)

- H&K Equipment (U.S.)

- Taylor Machine Works (U.S.)

- Anhui Heli Co. Ltd (China)

- CVS Ferrari (Italy)

- TIL Limited (India)

- Doosan Industrial Vehicle Co., Ltd. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, Kalmar collaborated with Mutiara Perlis Sdn Bhd (MPSB) and Mach 1 Group to equip Perlis Inland Port in Malaysia by supplying fleet of container handling equipment. The fleet includes six Kalmar reachstackers, three empty container handlers, and six terminal tractors.

- In April 2025, Adanaport, a division of SANKO Holding, commenced the expansion of its port by the procurement of LHM 550 mobile harbor crane. Adana Port agreed on the acquisition of a new Liebherr LHM 550 with a maximum capacity of 154 tonnes and equipped with two ropes, ready for container operation

- In March 2025, Konecranes received a contract from Saguenay Port Authority in Quebec, Canada, to supply Konecranes Gottwald ESP.6B Mobile Harbor Crane for a new cargo handling system that the port is developing.

- In December 2024, ZPMC received a contract worth USD 205 million to supply cargo handling gear and equipment to the Port of Safi in Morocco.

- In January 2023, Konecranes signed an agreement with Larsen & Toubro to expand its port crane business in India. Under this agreement, the company would deliver two shipyard jib cranes to the Cochin Shipyard in Cochin, Kerala.

REPORT COVERAGE

The report provides a detailed analysis of the industry and focuses on important aspects such as key players, technology, product application, and market scenario across various regions. Moreover, the research report offers deep insights, Porters’ five forces analysis into the market trends, competitive landscape, market competition, and market status and highlights key industry developments. Additionally, it encompasses several direct and indirect factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

|

|

Segmentation

|

By Equipment Type

|

|

By Fuel Type

|

|

|

By Application

|

|

|

By Mode of Operation:

|

|

|

By Solutions

|

|

|

By Port Type

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 20.8 million in 2025 and is projected to reach USD 30.1 million by 2034

Registering a CAGR of 3.92%, the market will exhibit significant growth during the forecast period.

By application, the container handling segment leads the market and held a dominant share in 2025.

Konecranes (Finland), Liebherr Group (Switzerland), Kalmar (Finland), and Shanghai Zhenhua Heavy Industries (ZPMC) (China) are some of the leading players in the market.

Asia Pacific dominate the market in terms of share.

In 2025, the Asia Pacific market value stood at USD 8.2 mllion.

The key factors driving the market comprise a rise in increase in maritime trade and surge in port expansion and modernization projects.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us