Automotive Biofuels Market Size, Share & Industry Analysis, By Fuel Type (Bioethanol, Biodiesel (FAME), Renewable Diesel (HVO), Biogas / Biomethane, and Others), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Feedstock Type (Food Crops, Non-Food Crops, Waste & Residues, and Algae-based Feedstock), By Blend Type (Low-Level Blends, High-Level Blends, and Drop-in Fuels), and Regional Forecast, 2026-2034

Automotive Biofuels Market Size and Future Outlook

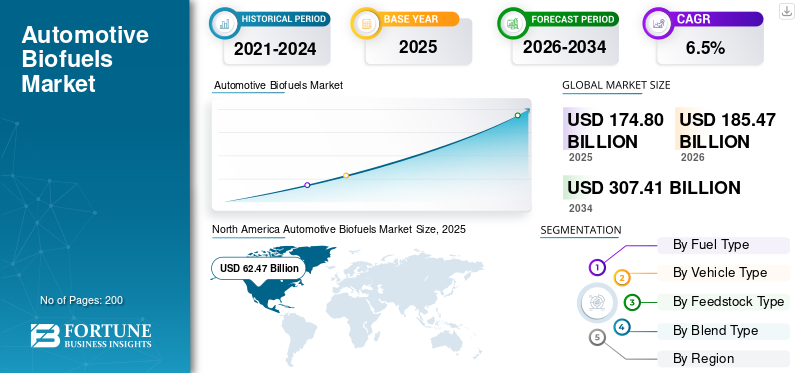

The global automotive biofuels market size was valued at USD 174.80 billion in 2025. The market is projected to grow from USD 185.47 billion in 2026 to USD 307.41 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. North America dominated the automotive biofuels market with a market share of 35.73% in 2025.

The global automotive biofuels market represents the production, distribution, and consumption of sustainable fuels derived from biological sources as alternatives to fossil fuels within the automotive sector. These fuels, including bioethanol, biodiesel, and biomethane, are increasingly being adopted as a sustainable alternative to conventional gasoline and diesel in fuel vehicles. As concerns over climate change intensify, governments and industries are shifting away from traditional fossil fuels toward renewable fuels that reduce greenhouse gas emissions.

The market is evolving due to a combination of regulatory mandates, technological progress, and increasing focus on energy security. Countries such as the U.S., Brazil, and India have introduced aggressive blending targets, which are significantly boosting biofuel production. At the same time, technological advancements in advanced biofuels are improving fuel efficiency and compatibility with existing engines, making them more viable alternatives.

The transition is also supported by growing investment in research and development, particularly in second-generation and waste-based biofuels. These innovations aim to overcome limitations associated with food-based feedstocks while enhancing sustainability. Additionally, biofuels are gaining importance as a renewable energy source that can be integrated into existing fuel infrastructure without requiring major modifications.

Applications of automotive biofuels span across passenger vehicles, light commercial vehicles, and heavy-duty transport, making them a versatile solution for decarbonization. While electric mobility is gaining traction, biofuels continue to play a crucial role in reducing emissions from existing internal combustion engine fleets.

Key players such as Shell and Chevron are focusing on expanding production capacity, forming strategic partnerships, and investing in next-generation biofuel technologies to strengthen their market position.

Download Free sample to learn more about this report.

AUTOMOTIVE BIOFUELS MARKET TRENDS

Shift toward Low-Carbon and Drop-in Renewable Fuels to be a Significant Market Trend

The market is witnessing a shift toward drop-in renewable fuels such as renewable diesel, which can directly replace traditional fossil fuels without engine modification. This trend is driven by the need for scalable and immediate emission reductions in fuel vehicles, supported by ongoing technological advancements.

- For instance, in April 2025, the U.S. EIA reported continued growth in renewable diesel consumption, driven by its compatibility with existing diesel engines in heavy-duty transport applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Government Blending Mandates Accelerate Biofuel Adoption

Government policies mandating blending of renewable fuels with fossil fuel are significantly driving automotive biofuels market growth. These regulations ensure consistent demand for biofuel production, encouraging investments and infrastructure development. Countries aiming to enhance energy security are increasingly adopting biofuels as viable alternatives to imported fuels, thereby accelerating their integration into the automotive sector.

- For instance, in March 2025, India’s Ministry of Petroleum confirmed expansion of E20 fuel availability across retail fuel stations, accelerating ethanol adoption in road transport and reducing dependence on fossil fuels.

MARKET RESTRAINTS

Volatility in Feedstock Supply and Pricing Constrains Biofuel Scalability

Fluctuations in feedstock availability and pricing, particularly for crops such as corn, sugarcane, and vegetable oils, create uncertainty in biofuel production costs. This directly impacts the economic viability of biofuel production compared to fossil fuel, limiting large-scale adoption. Additionally, competing demand from food and industrial sectors restricts consistent supply, slowing the transition toward sustainable fuels in the automotive sector.

- For instance, in May 2025, the IEA highlighted that increased demand for crop-based biofuels could strain agricultural supply chains, raising concerns over food security and feedstock availability for ethanol and biodiesel production.

MARKET OPPORTUNITIES

Advancement in Waste-Based Biofuels Unlocks New Growth Opportunities

The market is witnessing a shift toward drop-in renewable fuels such as renewable diesel, which can directly replace traditional fossil fuels without engine modification. This trend is driven by the need for scalable and immediate emission reductions in fuel vehicles, supported by ongoing technological advancements.

- For instance, in June 2025, Neste and Chevron Lummus Global completed initial piloting of technology converting lignocellulosic waste and residues into renewable diesel and sustainable fuels.

MARKET CHALLENGES

High Production Costs of Advanced Biofuels Hinder Adoption

Despite their benefits, advanced biofuels face challenges due to high production costs and complex processing technologies. These factors limit their competitiveness against fossil fuel, slowing their adoption as viable alternatives in price-sensitive markets.

- For instance, in June 2025, the IEA noted that advanced biofuels remain significantly more expensive than conventional fuels, limiting their scalability despite strong policy support for transport decarbonization.

Segmentation Analysis

By Fuel Type

Bioethanol Dominates Due to Large-Scale Blending Mandates and Established Production Ecosystem

On the basis of fuel type, the market is segmented into bioethanol, biodiesel (FAME), renewable diesel (HVO), biogas / biomethane, and others.

Bioethanol dominates the global automotive biofuels market share due to its extensive use as a blending component in gasoline and its compatibility with existing engines. Strong government mandates, particularly in the U.S., Brazil, and India, have driven large-scale biofuel production, making ethanol a leading renewable fuel. Its cost-effectiveness and scalability further position it as a sustainable alternative to conventional fuels within the automotive sector, supporting widespread adoption across passenger vehicles.

- For instance, in November 2023, India’s Ministry of Petroleum and Natural Gas reported that ethanol blending in petrol reached over 12% nationally, with a target of 20% (E20) by 2025–26, significantly increasing ethanol demand in the transportation fuel mix.

Renewable Diesel (HVO) segment is expected to grow at a CAGR of 10.1% over the forecast period.

By Vehicle Type

Passenger Vehicles Segment Dominate Due to Extensive Fuel Consumption Base and Ethanol Blending Penetration

On the basis of vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, and heavy commercial vehicles.

Passenger vehicles segment dominate the global market due to their massive global fleet size and high reliance on gasoline, which is widely blended with sustainable fuels such as ethanol. The widespread adoption of E10 and E20 fuels across major economies has significantly increased biofuel usage in this segment. Additionally, the existing infrastructure for fuel vehicles supports seamless integration of renewable fuels, making them a viable alternative to traditional fossil fuels without requiring major vehicle modifications.

- For instance, in February 2024, the U.S. Energy Information Administration reported that nearly all gasoline sold in the country contains about 10% ethanol, primarily used in passenger vehicles, reinforcing their dominance in biofuel consumption.

Heavy commercial vehicles segment is expected to grow at a CAGR of 8.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Feedstock Type

Food Crops Segment Dominate Due to Established Agricultural Infrastructure and High Yield Efficiency

On the basis of feedstock type, the market is segmented into food crops, non-food crops, waste & residues, and algae-based feedstock.

Food crops segment dominate the global market as they provide a reliable and scalable source for biofuel production. Crops such as corn, sugarcane, and soybean are widely cultivated and supported by established supply chains, ensured consistent feedstock availability. This enables efficient production of renewable fuels at scale, making them a key component in replacing fossil fuel consumption. Despite the emergence of advanced biofuels, food-based feedstocks continue to lead due to their economic viability.

- For instance, in July 2023, the U.S. Department of Agriculture confirmed that corn remains the primary feedstock for ethanol production, supporting large-scale biofuel output in North America.

Algae-based feedstock segment is expected to grow at a CAGR of 11.2% over the forecast period.

By Blend Type

Low-Level Blends Segment Dominates Due to Universal Compatibility with Existing Vehicle Fleet

On the basis of blend type, the market is segmented into low-level blends, high-level blends, and drop-in fuels.

Low-level blends segment dominates the market as they can be used across existing fuel vehicles without requiring engine modifications or infrastructure changes. Blends such as E10 and B7 are widely adopted across regions, enabling easy integration of sustainable fuels into the automotive sector. Their compatibility and regulatory support make them the most practical and scalable solution for reducing dependence on traditional fossil fuels while maintaining fuel efficiency and affordability.

- For instance, in June 2023, the European Commission confirmed that E10 petrol is now widely available across European Union member states, supporting the transition toward renewable energy in road transport.

Drop-in fuels segment is expected to grow at a CAGR of 9.6% over the forecast period.

Automotive Biofuels Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Automotive Biofuels Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valuing at USD 62.47 billion, and also maintained the leading share in 2024, with USD 59.76 billion. The growth is driven due to its well-established regulatory framework and large-scale biofuel production capacity. The region benefits from strong mandates promoting renewable fuels as alternatives to fossil fuels, supported by extensive infrastructure for fuel vehicles. The U.S. plays a central role, with high ethanol blending and increasing adoption of advanced biofuels such as renewable diesel. Continuous investment in research and development further strengthens the region’s leadership in sustainable fuels.

- For instance, in February 2024, the U.S. Energy Information Administration reported that nearly all gasoline sold in the country contains ethanol blends, reinforcing sustained biofuel demand in road transport.

U.S. Automotive Biofuels Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was approximated at around USD 53.60 billion in 2025, representing roughly 35.7% of market.

Asia Pacific

Asia Pacific is estimated to reach USD 46.62 billion in 2026 and secure the position of the second-largest region in the market. Asia Pacific is witnessing rapid growth due to aggressive government initiatives promoting sustainable fuels and reducing dependence on traditional fossil fuels. India, Indonesia, and Thailand are expanding biofuel production through ethanol and biodiesel blending programs. Rising energy demand and focus on energy security are further driving the adoption of renewable fuels across the automotive sector.

China Automotive Biofuels Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 7.98 billion, representing roughly 4.5% of market.

India Automotive Biofuels Market

The Indian market was valued at around USD 8.82 billion in 2025, accounting for roughly 5.0% of global revenues.

Europe

Europe is projected to record a growth rate of 6.1% in the coming years, and reach a valuation of USD 39.51 billion by 2026. Europe is experiencing steady growth driven by stringent emission regulations and increasing focus on renewable energy. The region is emphasizing advanced biofuels and waste-based feedstocks to reduce reliance on fossil fuel. Regulatory frameworks continue to support the transition toward sustainable alternative to conventional fuels.

Germany Automotive Biofuels Market

The German market was valued at around USD 9.21 billion in 2025, accounting for roughly 5.3% of global revenues.

U.K. Automotive Biofuels Market

The U.K. market was valued at around USD 6.49 billion in 2025, accounting for roughly 3.7% of global revenues.

Latin America

Latin America is projected to record a growth rate of 6.7% in the coming years, and reach a valuation of USD 28.95 billion by 2026. Latin America shows strong growth due to abundant feedstock availability, particularly sugarcane, supporting large-scale biofuel production. Brazil lead in ethanol adoption, using renewable fuels as viable alternatives to traditional fossil fuels. Established infrastructure supports widespread use in the automotive sector.

Brazil Automotive Biofuels Market

The Brazil market was valued at around USD 24.00 billion in 2025, accounting for roughly 13.7% of global revenues.

Middle East & Africa

Middle East & Africa is projected to record a growth rate of 7.3% in the coming years, and reach a valuation of USD 4.58 billion by 2026. The Middle East & Africa region is gradually expanding as countries diversify energy sources beyond fossil fuel dependence. Increasing focus on renewable energy and sustainable fuels is encouraging early-stage biofuel production. Government initiatives aimed at improving energy security are expected to support long-term market development.

UAE Automotive Biofuels Market

The UAE market was valued at around USD 0.85 billion in 2025, accounting for roughly 0.5% of revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Expansion and Innovation by Key Players to Boost Market Expansion

The competitive landscape of the global automotive biofuels market is characterized by the presence of large energy companies, agricultural processors, and specialized biofuel producers. Companies are increasingly focusing on investment in research and development to enhance the efficiency of biofuel production and develop advanced biofuels that can serve as viable alternatives to traditional fossil fuels. Strategic collaborations, mergers, and capacity expansions are common approaches adopted to gain a competitive edge.

Major players are prioritizing diversification of feedstock sources to reduce dependency on food crops and improve sustainability. Additionally, companies are investing in refining technologies that enable the production of high-quality renewable fuels compatible with existing fuel vehicles. Geographic expansion into emerging markets is also a key strategy, as countries in Asia-Pacific and Latin America offer strong growth potential due to favorable government policies.

Another critical strategy is vertical integration, where companies control multiple stages of the value chain, from feedstock sourcing to distribution. This helps in optimizing costs and ensuring supply chain stability. Furthermore, partnerships with automotive manufacturers and fuel distributors are strengthening market penetration.

- For instance, in March 2024, Neste announced expansion of its renewable diesel production capacity in Singapore, strengthening supply of sustainable fuels for global transportation markets.

LIST OF KEY AUTOMOTIVE BIOFUELS COMPANIES PROFILED IN REPORT

- Neste (Finland)

- Archer Daniels Midland (U.S.)

- Valero Energy (U.S.)

- BP Bioenergy (U.K.)

- Shell (U.K.)

- TotalEnergies (France)

- Chevron (U.S.)

- Raízen (Brazil)

- POET LLC (U.S.)

- Petrobras (Brazil)

- Wilmar International (Singapore)

- ENI (Italy)

- Gevo Inc. (U.S.)

- Cargill (U.S.)

- Indian Oil Corporation (India)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Optimus Technologies and Sunoil Biodiesel entered a commercial partnership to accelerate adoption of 100% biodiesel (B100) among heavy-duty fleets in the Netherlands, directly supporting diesel fleet decarbonization.

- March 2026: Eni announced that all 100 Itabus vehicles now run on Enilive’s HVOlution diesel, made from 100% renewable raw materials. In 2025, Itabus used more than 3 million liters of HVO across 20 million kilometers.

- February 2026: NASCAR announced POET as its Official Bioethanol Partner, marking a major step in integrating renewable fuels into high-performance motorsports. The collaboration enables the use of zero-carbon bioethanol in racing fuel, demonstrating ethanol’s viability as a sustainable alternative in demanding automotive applications.

- January 2026: Corteva and bp launched Etlas, a joint venture focused on developing scalable biofuel feedstocks such as canola, mustard, and sunflower. The initiative aims to strengthen supply chains for renewable diesel and other low-carbon fuels, supporting long-term growth in sustainable transportation energy.

- December 2025: ADM and Tallgrass marked the opening of a large bioethanol carbon capture facility, strengthening low-carbon ethanol production and supporting lower-emission fuel pathways linked to road-fuel blending.

- September 2025: POET signed an agreement to acquire Green Plains Obion, a Tennessee bioethanol facility, adding 120 million gallons of annual production capacity and expanding access to southeastern U.S. markets.

- August 2025: Conestoga Energy acquired SAFFiRE Renewables from Southwest Airlines Renewable Ventures, gaining technology for ultra-low-carbon ethanol and intermediates from agricultural residues.

REPORT COVERAGE

The global automotive biofuels market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Fuel Type, Vehicle Type, Feedstock Type, Blend Type, and Region |

| By Fuel Type |

|

| By Vehicle Type |

|

| By Feedstock Type |

|

| By Blend Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 174.80 billion in 2025 and is projected to reach USD 307.41 billion by 2034.

In 2025, the North America’s market value stood at USD 62.47 billion.

The market is expected to exhibit a CAGR of 6.5% during the forecast period of 2026-2034.

Passenger vehicles segment led the market by vehicle type.

Government blending mandates is driving the global market.

Neste, Valero Energy, Shell, and Chevron are the top players in the market.

North America held the largest share market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us