Dermatology Devices Market Size, Share & Industry Analysis, By Product Type (Diagnostic Devices [Dermatoscopes, Skin Imaging Devices, and Others], Treatment & Surgical Devices [Laser-based Devices, Light-based Devices, Energy-based Devices, Electrosurgical Devices, and Others]), By Portability (Fixed and Handheld), By Application (Medical Dermatology, Skin Cancer Management, and Aesthetic Dermatology), By End User (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Dermatology Devices Market Size and Future Outlook

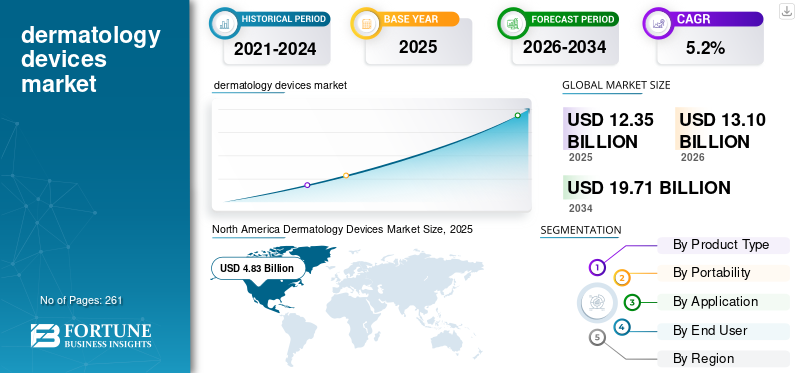

The global dermatology devices market size was valued at USD 12.35 billion in 2025 and is projected to grow from USD 13.10 billion in 2026 to USD 19.71 billion by 2034, exhibiting a CAGR of 5.2% during the forecast period. North America dominated the dermatology devices market with a market share of 39.11% in 2025.

Dermatology devices are specialized medical devices used to diagnose, monitor, and treat conditions affecting the skin, nails, and hair in the patient population. The growing prevalence of chronic conditions, such as skin cancer, and other conditions, rising dermatology surgical procedure volumes, and increasing healthcare spending are driving the adoption of these devices in the market. The ongoing technological advancements in dermatology devices are further boosting their adoption in the market.

- For instance, according to the data published by the World Health Organization (WHO), more than 1.5 million new cases of skin cancer were registered worldwide in 2022.

Furthermore, rising research and development activities by major players, such as Alma Lasers and Cutera, Inc., are contributing to the demand for these devices in the market.

Download Free sample to learn more about this report.

DERMATOLOGY DEVICES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 12.35 Billion

- 2026 Market Size: USD 13.10 Billion

- 2034 Forecast Market Size: USD 19.71 Billion

- CAGR: 5.2% from 2026–2034

- North America dominated the dermatology devices market with a 39.11% share in 2025.

- The treatment & surgical devices segment held the largest revenue share in 2025.

- The fixed segment accounted for 65.5% of the global market share in 2025.

North America

The North America market held the dominant share in 2024, valued at USD 4.55 billion, and also took the leading share in 2025 with USD 4.83 billion.

Europe

Europe is projected to record a growth rate of 4.4% in the coming years, which is the second highest among all regions, and reach a valuation of USD 3.60 billion by 2026.

Asia Pacific

Asia Pacific region is estimated to reach USD 3.26 billion in 2026 and secure the position of the third-largest region in the market.

U.S.

The market is projected to reach USD 4.53 billion in 2026, accounting for approximately 34.6% of global sales, supported by strong demand for dermatology treatments and aesthetic procedures.

Japan

The market is estimated at USD 0.67 billion in 2026, representing around 5.1% of global revenues, driven by a high prevalence of skin diseases and substantial procedure volumes.

Read More

Dermatology Devices Market Trends

Rising Technological Advancements in Diagnostic and Therapeutic Categories to Fuel the Demand

There are growing technological advancements across both diagnostic and therapeutic categories. The companies are emphasizing the development of portable, point-of-care tools, including advanced dermoscopy/optical assessment devices and artificial intelligence-assisted decision-support software that enable faster diagnosis of suspicious lesions, enhancing workflow efficiency and potentially accelerating referrals among patients.

Additionally, the adoption of teledermatology ecosystems, standardized imaging technology, connected software, and store-and-forward workflows is further driving market adoption of these products.

- In April 2025, Skinwood Luxury Aesthetic Centre launched SkinPen Precision, a U.S. FDA-approved microneedling device, with the aim of advancing aesthetic dermatology.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Rising Prevalence of Chronic Skin Disorders to Fuel the Market Growth

The growing prevalence of chronic skin conditions, such as skin cancer and psoriasis, is driving an increase in diagnostic and treatment procedures among the patient population, thereby boosting the global dermatology devices market growth.

- For instance, according to 2021 data published by the National Eczema Association (NEA), about 31.6 million people have some form of eczema.

This, along with chronic and recurrent skin diseases, which are further increasing the need for routine evaluation, is augmenting the adoption rate of these devices in the market. Therefore, the factors above, coupled with the growing emphasis by key players on introducing research and development activities to launch novel products, are anticipated to drive adoption rates for these products, thereby supporting the global dermatology devices market size.

Market Restraints

High Cost Associated with Advanced Devices to Hamper the Market Growth

There is an increasing demand for clinical and aesthetic procedures among the patient population. The high upfront cost of advanced diagnostic and energy-based treatment devices makes it challenging for small and independent clinics to adopt them. Additionally, recurring costs for preventive maintenance, repairs, software upgrades, calibration, and replacement of wear parts/handpieces further increase the financial burden.

Furthermore, certain procedure types require ongoing consumables, including single-use tips/cartridges, disposables, and other accessories, which raise total ownership costs and can reduce margins for key players and distributors.

- For instance, according to the 2024 statistics published by DermLite, the cost of the DermLite DL4 dermatoscope is around USD 1,695.0.

Market Opportunities

Expansion of Private Dermatology Clinics to Create a Rise in Dermatology Procedures

The expansion of private dermatology clinics, corporate clinic networks, and med-spa chains is driving a rise in dermatology procedures in these settings. The growing disposable incomes, medical tourism, and increasing penetration of minimally invasive aesthetic treatments are driving key providers in these nations to focus on mid-priced energy-based platforms, portable diagnostic devices, and advanced software to improve patient throughput.

- According to Bookimed's 2025 data, over 3.5 million medical tourists visit Thailand annually.

Market Challenges

Limited Healthcare Access in Developing Countries to Hamper the Market Growth

There is a growing demand for dermatology procedures among the patient population. However, the lack of developed infrastructure, limited adoption of technologically advanced devices, and inadequate reimbursement frameworks, especially in developing countries, are resulting in limited access to diagnostic and treatment facilities among the patient population.

Furthermore, limited healthcare settings and specialized dermatologists, among other factors, are crucial factors that delay diagnostic and treatment procedures among the patient population, particularly in developing countries such as India and China.

- For instance, according to a 2026 survey published by medRxiv, the mean dermatogist density is about 0.37 per 100,000 in low-income (LICs) countries.

Other Prominent Challenges

- Regulatory compliance requirements for energy-based devices.

- Risk of procedural complications in untrained settings.

SEGMENTATION ANALYSIS

By Product Type

Increasing Number of Surgical Procedures Led to the Treatment & Surgical Devices Segment Dominance

Based on the product type, the market is classified into diagnostic devices and treatment & surgical devices. The diagnostic devices are further classified into dermatoscopes, skin imaging devices, and others. The treatment & surgical devices are also divided into laser-based devices, light-based devices, energy-based devices, electrosurgical devices, and others.

To know how our report can help streamline your business, Speak to Analyst

The treatment & surgical devices segment held the largest revenue share in 2025. The growth is driven by the increasing prevalence of skin disorders among patients, leading to a rising number of surgical procedures globally. This, along with the growing focus of key companies on launching novel dermatology devices, is expected to further support the global dermatology devices market's growth.

- For instance, according to statistics published by the International Society of Aesthetic Plastic Surgery (ISAPS), more than 17.4 million surgical procedures were performed globally in 2024.

The diagnostic devices segment is expected to grow at a CAGR of 5.1% over the forecast period.

By Portability

Growing Number of Product Launches Led to the Dominance of the Fixed Portability Segment

Based on portability, the market is segmented into fixed and handheld.

The fixed segment dominated the global market in 2025 held the share of 65.5%. The growth is driven by the rising prevalence of skin disorders, which is prompting key players to invest in research and development to launch fixed products, thereby supporting the adoption of these devices in the market.

- For instance, in October 2025, Acclaro Medical launched the UltraClear 2910 nm cold-ablative fiber laser with the aim of providing advanced devices for beauty and aesthetics.

The segment of handheld is set to flourish with a growth rate of 5.6% across the forecast period.

By Application

Growing Number of Aesthetic Procedures Led to the Dominance of the Aesthetic Dermatology Segment

Based on application, the market is segmented into medical dermatology, skin cancer management, and aesthetic dermatology.

The aesthetic dermatology segment dominated the global market share of 56.4% in 2025. The growth is driven by the rising number of aesthetic procedures, such as rhinoplasty and the removal of vascular and pigmented lesions, resulting in an increase in surgical and non-surgical procedures globally and thereby contributing to the adoption rate of these devices in the market.

- For instance, according to the 2024 statistics published by the International Society of Aesthetic Plastic Surgery (ISAPS), approximately 1.08 million rhinoplasty procedures were performed globally in 2024.

The segment of medical dermatology is set to flourish with a growth rate of 4.8% across the forecast period.

By End-user

Increasing Number of Dermatology Clinics Led to the Specialty Clinics Segmental Dominance

Based on end user, the market is categorized into hospitals & ASCs, specialty clinics, and others.

The specialty clinics segment dominated the dermatology devices market share in 2025. The growing prevalence of skin cancer, the rising number of dermatology procedures in specialty clinics, and the growing number of dermatology clinics, among others, are some of the crucial factors contributing to the segment's growth in the market. Furthermore, the segment is set to hold a 54.5% share in 2026.

- For instance, according to 2025 statistics published by Rentech Digital, it was reported that 20,420 skin care clinics in India.

In addition, hospitals & ASCs’ end users are projected to grow at a 4.8% CAGR during the forecast period.

Dermatology Devices Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Dermatology Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 4.55 billion, and also took the leading share in 2025 with USD 4.83 billion. The rising prevalence of skin conditions, the growing number of clinical and aesthetic procedures such as body contouring and fat removal, advanced healthcare infrastructure, among others, are some of the factors contributing to the growth of the segment in the market.

- For instance, according to 2024 statistics published by the International Society of Aesthetic Plastic Surgery (ISAPS), about 4.2 million non-surgical aesthetic procedures were performed in the U.S.

U.S. Dermatology Devices Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is set to reach USD 4.53 billion in 2026, accounting for roughly 34.6% of global sales.

Europe

Europe is projected to record a growth rate of 4.4% in the coming years, which is the second highest among all regions, and reach a valuation of USD 3.60 billion by 2026. The growing number of clinical and aesthetic procedures and technological advancements in these devices are likely to support the market growth.

U.K Dermatology Devices Market

The U.K. market in 2026 is estimated at around USD 0.55 billion, representing roughly 4.2% of global revenues.

Germany Dermatology Devices Market

Germany’s market is projected to reach approximately USD 0.69 billion in 2026, equivalent to around 5.2% of global sales.

Asia Pacific

Asia Pacific region is estimated to reach USD 3.26 billion in 2026 and secure the position of the third-largest region in the market. The growing volume of surgical procedures, expanding hospital capacity, and increasing healthcare spending are expected to contribute to the growth of the market. In the region, India and China are both estimated to reach USD 0.50 billion and USD 0.90 billion, respectively, in 2026.

Japan Dermatology Devices Market

The Japanese market in 2026 is estimated at around USD 0.67 billion, accounting for roughly 5.1% of global revenues. Japan has historically reported a relatively high prevalence of skin diseases, with a large number of dermatology procedures.

China Dermatology Devices Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.90 billion, representing roughly 6.9% of global sales.

India Dermatology Devices Market

The India dermatology devices market size in 2026 is estimated at around USD 0.50 billion, accounting for roughly 3.8% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.62 billion in 2026. The growth is due to the improving healthcare access and rising adoption of these products in these regions. In the Middle East & Africa, the GCC is set to reach a value of USD 0.24 billion in 2026.

South Africa Dermatology Devices Market

The South Africa market is projected to reach around USD 0.09 billion in 2026, representing roughly 0.7% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches by Major Industry Players to Support Their Market Position

A significant device portfolio, along with a significant emphasis on strategic initiatives globally, is one of the prominent factors contributing to the dominance of these companies in the market. Alma Lasers and Cutera, Inc., are major companies in the market in 2025. Furthermore, the growing focus of key players on research and development activities to launch innovative devices is expected to strengthen their presence, further contributing to the global dermatology devices market expansion.

- For instance, in September 2023, Cutera, Inc., launched Secret DUO, an innovative skin resurfacing and revitalization platform that utilizes dual non-ablative fractional technologies.

Other key players, including Cynosure Lutronic, and others, are also growing in the market, primarily due to their increasing focus on expansion of their geographical presence among other companies to strengthen their presence in the market.

List of Key Dermatology Devices Companies Profiled

- Alma Lasers (Israel)

- Cutera, Inc. (U.S.)

- Cynosure Lutronic (U.S.)

- Candela Corporation (U.S.)

- Bausch Health Companies Inc. (Canada)

- Canfield Scientific, Inc. (U.S.)

- HEINE Optotechnik GmbH & Co. KG (Germany)

- STRATA Skin Sciences (U.S.)

- Aerolase (U.S.)

- Veriosys Technologies, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Candela Corporation, launched the Glacē System, a facial treatment platform with an aim to provide innovative solutions for aesthetic medicine.

- December 2025: Cutera, Inc., received U.S. FDA approval for expanded indications for its truFlex muscle stimulation technology. This expanded clearance added rehabilitative and therapeutic applications and opened new treatment areas.

- October 2025: Cynosure Lutronic launched eCO2 3D, a fractional CO2 laser in aesthetics, with an aim to strengthen its product channel.

- September 2025: Sciton, Inc., a player in medical aesthetic laser and light-based technology, launched HALO TRIBRID, a 3-in-1 customizable resurfacing laser, with an aim to strengthen its devices channel.

- August 2025: STRATA Skin Sciences announced it is working with the Centers for Medicare & Medicaid Services (CMS) to obtain temporary codes that would increase access to expanded reimbursement for its XTRAC excimer laser treatment. This helped the company in strengthening its presence.

- July 2024: InMode Ltd., a global provider of innovative medical technologies, received U.S. FDA 510(k) clearance for the Morpheus8 technology, a fractional radiofrequency (FRF) microneedling technology for contraction of soft tissue with an aim to widen its device channel.

- April 2024: Cutera, Inc., launched xeo+, a laser and light-based multi-application platform with an aim to strengthen its product channel.

REPORT COVERAGE

The report provides a detailed global dermatology devices market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, portability, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Portability, Application, End User, and Region |

| By Product Type |

|

| By Portability |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 12.35 billion in 2025 and is projected to reach USD 19.71 billion by 2034.

In 2025, North Americas market value stood at USD 4.83 billion.

Growing at a CAGR of 5.2%, the market will exhibit steady growth over the forecast period (2026-2034).

By product type, the treatment & surgical devices segment is the leading segment in this market.

The introduction of novel dermatology devices is one of the major factors driving the market's growth.

The introduction of novel dermatology devices is one of the major factors driving the market's growth.

North America dominated the market share in 2025.

The growing prevalence of skin disorders, the increasing number of diagnostic and treatment procedures, among others, are some of the crucial factors expected to boost the adoption of these devices globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us