Renewable Energy Market Size, Share & Industry Analysis, By Type (Wind, Solar, Bioenergy, Geothermal, Ocean Energy, and Hydropower), By End-User (Residential, Commercial, Industrial, and Utility), and Regional Forecast, 2026-2034

RENEWABLE ENERGY INDUSTRY OUTLOOK ANALYSIS 2026-2034

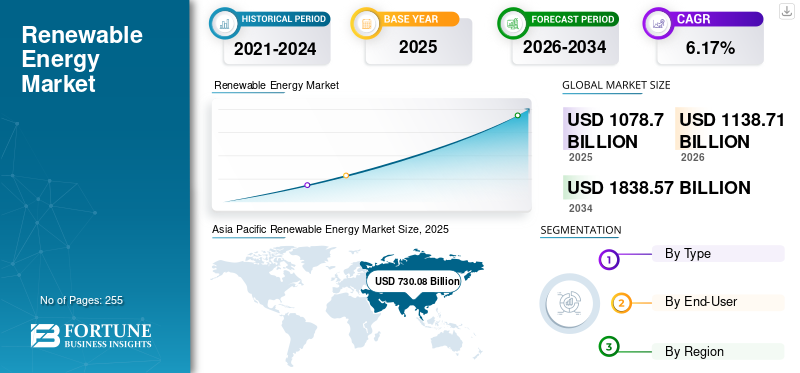

The global renewable energy market size was valued at USD 1,078.7 billion in 2025 and is projected to grow from USD 1,138.71 billion in 2026 to USD 1,838.57 billion by 2034, exhibiting a CAGR of 6.17% during the forecast period. Asia Pacific dominated the renewable energy market with a 71.72% market share in 2025. The industry growth is driven by accelerating clean energy investments, grid modernization, technological innovation, supportive policies, and expanding decarbonization commitments worldwide.

Renewable energy refers to the energy that comes from natural resources, also known as finite resources. These sources include the sun, wind, rain, tides, waves, and heat. Equated to fossil fuels, such as natural gas, coal, and oil, renewable power sources are sustainable and have the least impact on the environment. With growing concerns about climate change, energy security, and declining fossil fuel reserves, the use of renewable energy has accelerated globally.

The global renewable energy market is undergoing structural transformation as governments, utilities, corporations, and institutional investors accelerate capital allocation toward low-carbon power generation. Long-term growth is supported by energy security priorities, decarbonization commitments, declining technology costs, and sustained expansion of electricity demand. Consequently, renewable energy market growth is increasingly driven by structural policy and economic fundamentals rather than cyclical investment activity.

Technology diversification has strengthened the industry's resilience. Solar photovoltaic, onshore and offshore wind, hydropower, bioenergy, geothermal resources, and emerging ocean energy technologies collectively create a balanced generation portfolio capable of supporting evolving grid requirements. Investment decisions increasingly prioritize lifecycle economics, grid integration capability, capacity utilization, and long-term operational reliability over initial installation costs alone.

Electricity demand is evolving alongside industrial electrification, electric vehicle adoption, digital infrastructure expansion, and artificial intelligence-enabled data centers. These developments are reshaping procurement strategies across utilities and commercial enterprises while increasing demand for renewable generation assets capable of delivering stable, low-carbon electricity. Energy storage systems, advanced transmission infrastructure, and digital grid management platforms are becoming essential complements to renewable deployment, improving system flexibility and operational efficiency.

Competitive dynamics within the renewable energy industry increasingly reflect execution capability rather than technology access alone. Leading participants are expanding vertically across project development, equipment manufacturing, engineering services, financing, and long-term asset management. Strategic partnerships between utilities, technology suppliers, financial institutions, and infrastructure investors are accelerating project deployment while reducing development risk.

Despite permitting complexity, transmission bottlenecks, supply chain volatility, and financing constraints in selected regions, the renewable energy market remains positioned for sustained expansion. Continued technological innovation, supportive regulatory frameworks, and increasing corporate procurement of renewable electricity are expected to strengthen renewable energy market size, reinforce renewable energy market trends, and support long-term industry competitiveness through 2032.

Authorities, companies, and individuals invest in new energy technology to reduce greenhouse gas emissions, diversify energy sources, and promote sustainable development. In addition, technological advances and cost reductions have made renewable energy more competitive with conventional energy sources, rapidly expanding and integrating it into the energy mix. The market share of renewable energy is being fueled by a growing need for eco-friendly energy solutions, favorable government policies, and advancements in technology.

Download Free sample to learn more about this report.

Global Renewable Energy Market Overview

- 2025 Market Size: USD 1,078.7 Billion

- 2026 Market Size: USD 1,138.71 Billion

- 2034 Forecast Market Size: USD 1,838.57 Billion

- CAGR: 6.17% from 2026–2034

- Asia Pacific dominated the renewable energy market with a 71.72% share in 2025.

- The solar power segment is projected to account for 57.53% of the market in 2026.

- The utility segment held a 53.96% market share in 2024.

North American

North America is projected to reach USD 143.97 billion in 2026 with the second-fastest growth rate.

Europe

Europe is expected to reach USD 138.08 billion in 2026, supported by renewable energy policies.

Asia Pacific

Asia Pacific led the global market and is expected to reach USD 773.73 billion in 2026.

U.S.

The renewable energy market is projected to reach USD 132.03 billion in 2026.

Japan

The renewable energy market is projected to reach USD 23.58 billion in 2026.

Read More

Renewable Energy Industry Trends

Growing Technological Advances to Support the Market Development

As renewable energy grows more important to technology and energy systems, it plays an important role in maintaining energy supplies while ensuring energy security and stability. Since new energy sources, especially wind and solar, are vulnerable to environmental conditions, it is important to ensure optimal generation and distribution to provide a reliable supply of electricity. Renewable energy forecasting is fast becoming an important tool in the energy transition.

For example, solutions, such as IBM's Renewable Energy Forecasting Platform in IBM's Environmental Intelligence Suite, can provide wind and solar forecasts with 92% accuracy. Better storage helps make electronic systems more flexible.

Energy system transformation is redefining renewable energy market trends beyond simple capacity expansion. Investment priorities increasingly emphasize dispatchability, grid resilience, and lifecycle efficiency rather than standalone generation assets. As renewable penetration rises, utilities are integrating storage technologies, flexible transmission networks, and digital energy management platforms to maintain system reliability while accommodating variable power generation.

Corporate electricity procurement has evolved into a significant market catalyst. Multinational manufacturers, technology companies, and industrial operators are expanding long-term renewable power purchase agreements to stabilize energy costs and meet environmental commitments. This shift is broadening demand beyond regulated utilities and encouraging developers to diversify project portfolios.

Technology convergence is reshaping competitive dynamics. Renewable generation assets are increasingly deployed alongside battery energy storage systems, artificial intelligence-enabled forecasting tools, and advanced grid automation platforms. These integrated solutions improve energy balancing, optimize asset utilization, and reduce curtailment risks, strengthening the commercial viability of renewable infrastructure.

Solar, wind, and hydropower require energy storage systems (ESS) to provide a stable energy source. As grid-scale battery technology develops, utilities can store energy for longer periods to better handle loads with little or no downtime. For example, flow batteries are a low-cost, long-term hybrid type of grid-based energy storage that is being developed.

Download Free sample to learn more about this report.

Renewable Energy Market Growth Factors

Rising Efforts to Reduce the Effects of High Carbon Emissions to Lead Market Growth

Increasing environmental, social, and governance (ESG) criteria among investors has led to a major shift toward sustainable investments. Companies and financial organizations are increasingly focusing on renewable energy projects to align with their ESG goals and attract a broader base of savvy investors. This trend will increase demand for clean energy and increase innovation and competition in the sector.

According to the International Energy Agency, global energy-related CO2 emissions increased by 1.1% in 2023, increasing by 410 million tons (Mt) to a new record of 37.4 billion tons (Gt). This compares to an increase of 490 million tons in 2022 (1.3%). Greenhouse gas emissions account for more than 65% of the increase by 2023.

Technology cost improvements continue strengthening commercial competitiveness. Manufacturing scale, engineering optimization, and operational experience have reduced the levelized cost of electricity across multiple renewable technologies. These improvements enhance project viability even in markets where direct policy support is gradually declining.

Corporate sustainability strategies provide another important growth catalyst. Industrial companies, commercial enterprises, and global technology firms increasingly procure renewable electricity through direct investments and long-term contractual arrangements. Energy security considerations further reinforce this trend by reducing exposure to fossil fuel price volatility.

As more capital is poured into the clean energy industry, economies of scale will lower costs, and technological advances will further stimulate market growth and speed up the transition to a low-carbon economy. In addition, government policies and incentives play an important role in increasing the demand. All such factors are anticipated to drive market growth during the forecast period.

Growing Government Investments in Renewable Energy and Favorable Policies to Boost Market Expansion

Governments across the globe have enacted laws to endorse the development and utilization of renewable energy sources, including mandates, tax incentives, and subsidies. As of August 2023, the world's total installed solar energy capacity was 1,624 gigawatts (GW). This would result in 447 GW of new PV capacity installed in 2023 alone. Globally, 77.6 GW of new wind capacity was connected to the grid in 2022, reaching 1,906 GW, a 9% increase over 2021.

Government policy remains one of the strongest drivers supporting renewable energy market growth. Carbon reduction commitments, renewable portfolio standards, competitive auctions, tax incentives, and public infrastructure investments continue to improve project economics while reducing investment uncertainty. Stable policy environments encourage long-term capital deployment across utility-scale and distributed renewable energy projects.

Electricity demand is expanding as economies undergo widespread electrification. Electric vehicles, digital infrastructure, industrial automation, and heat electrification are increasing consumption while encouraging utilities to diversify generation portfolios. Renewable energy technologies increasingly represent the preferred option because of competitive operating costs and favorable environmental characteristics.

Further, in September 2021, the U.K. government allotted a USD 1.2 billion package for both public and private investments in India's green enterprises and renewable power. To mobilize private finance for green infrastructure in India, they launched the Climate Finance Management Initiative (CFLI) India. These investments aim to support India in achieving its 2030 aim of 450 GW of renewable energy, helping the industry to grow over the expected period and increase the compound annual growth rate (CAGR) of the market.

Restraining Factors

High Capital Investments to Establish Renewable Energy Plants Hinder Market Growth

High capital costs hinder the installation of renewable energy by small and medium-sized retailers. While the long-term savings from lower energy bills and the profits from selling excess electricity to the grid are significant, the initial costs of purchasing and installing energy systems are high. In addition, the cost of installing renewable energy infrastructure often requires advanced technology, specialized equipment, and extensive site preparation. The preliminary costs of installing solar panels are, for example, the panels and inverters themselves, installation systems, and labor. All these factors hinder the growth of the market.

Grid infrastructure limitations represent one of the most significant constraints affecting the renewable energy market. Generation capacity is expanding faster than transmission and distribution networks in many countries, creating congestion, project delays, and curtailment risks. Developers increasingly encounter challenges securing timely grid connections, particularly in regions experiencing rapid renewable deployment. These infrastructure bottlenecks can reduce project economics and postpone commercial operations.

Permitting complexity continues to influence investment timelines. Renewable energy projects frequently require multiple environmental assessments, land-use approvals, and stakeholder consultations before construction can begin. Regulatory fragmentation across jurisdictions further increases administrative costs and extends development schedules. Such delays affect capital efficiency and create uncertainty for investors managing large project pipelines.

Supply chain volatility remains another structural concern. Availability of critical minerals, power electronics, transformers, and specialized manufacturing equipment can influence project costs and delivery schedules. Trade policies, geopolitical developments, and transportation disruptions periodically affect procurement strategies, encouraging developers to diversify supplier networks and regional sourcing arrangements.

Market Opportunities

Integration of Renewable Energy into Smart Grids Creates New Growth Opportunities for the Market

The integration of renewable energy into smart grids enhances energy efficiency and reduces system losses. Smart meters, sensors, and automation technologies allow for more precise monitoring and control of electricity consumption, enabling utilities to identify inefficiencies and implement demand-side management strategies. In addition, distributed renewable energy generation at the local level, such as rooftop solar panels or community wind turbines, reduces the need for long-distance transmission of electricity, minimizing energy losses during transmission and distribution.

Furthermore, smart grids facilitate the integration of electric vehicles (EVs) and other forms of distributed energy resources (DERs). As the adoption of EVs continues to rise, smart grids support vehicle-to-grid (V2G) technology, enabling EV batteries to store and discharge electricity back to the grid as needed. All these factors are expected to provide new growth opportunities for the global market during the forecast period.

In May 2024, Tata Power Delhi Distribution Limited (Tata Power-DDL) amalgamated with the India Smart Grid Forum (ISGF) to set up a Vehicle-to-Grid (V2G) technology demonstration project in North Delhi. The Memorandum of Understanding (MoU) was signed, marking an important step toward the introduction of electric vehicles (EVs) and electric power to increase the sustainability of inventory and electrical equipment.

Grid modernization presents one of the largest long-term opportunities within the renewable energy market. Expansion of high-voltage transmission networks, digital substations, and intelligent distribution systems will enable greater integration of renewable generation while improving operational reliability. Companies supplying grid technologies, engineering services, and digital infrastructure are positioned to benefit from sustained investment cycles.

Energy storage is becoming an increasingly attractive growth segment. Battery systems, pumped hydro storage, and emerging long-duration storage technologies improve renewable energy utilization by balancing supply variability and strengthening grid resilience. As storage economics continue improving, integrated renewable-plus-storage projects are expected to capture a growing share of infrastructure investment.

Market Challenges

Lack of Affordable Energy Storage is A Challenge for Renewable Energy

Renewable energy sources produce the most energy at certain times of the day. Its power output does not match peak demand hours. Solar radiation and wind cannot provide a sufficient source of energy for 24 hours per week. Solar and wind power are unpredictable. The output is different, and the loads are different. Energy generation is more efficient than fossil fuels.

On the other hand, regular power generation from renewable energy sources creates a need for an efficient battery storage system. A battery storage system helps store excess energy for later use. This can disrupt the network and cause power outages. Technological advances have improved battery life and storage system capacity. High cost prevents widespread adoption. The cost of batteries should be reduced to make solar energy storage more affordable.

Renewable Energy Market Segmentation Analysis

By Type

Solar Segment Leads the Market with Its Rapid Installation Across Developing Countries

Based on type, the market is segmented into wind, solar, bioenergy, geothermal, ocean energy, and hydropower.

Solar

Solar power leads the market in both revenue and volume terms. The segment is expected to capture 57.53% of the market share in 2026. Solar generation increased by 270 terawatt-hours (a 26% increase) to 1,300 terawatt-hours by 2022. Rapid cost reductions, supportive government policies, technological advancements, diverse applications, growing demand for clean energy, enhanced energy independence, rising electricity demand, increased public awareness, and expansion of utility-scale projects drive the market growth.

Solar photovoltaic technology has become a cornerstone of renewable electricity generation because of its scalability, declining installation costs, and broad geographic applicability. Utility-scale projects, commercial rooftops, and distributed residential systems collectively support diversified demand patterns across developed and emerging economies. The technology's modular architecture enables flexible deployment ranging from small installations to multi-gigawatt power plants.

Manufacturing innovation continues to improve conversion efficiency and reduce production costs. Advanced cell architectures, bifacial modules, and tracker systems are increasing electricity yields while enhancing project economics. These developments strengthen solar competitiveness across multiple climatic conditions and operating environments.

Corporate procurement strategies have become an important demand driver. Commercial enterprises increasingly deploy rooftop installations or secure long-term power purchase agreements to reduce electricity expenses and achieve sustainability objectives. Industrial facilities are also expanding captive solar generation to improve energy resilience.

Wind

Wind energy has grown rapidly since 2000, thanks to R&D, supportive policies, and cost reductions. The segment is likely to hold a strong CAGR of 7.51% during the forecast period. According to IRNA, the world's installed wind generation capacity - onshore and offshore - has increased 98 times in the last two years. From 7.5 GW in 1997 to 733 GW in 2018.

Wind energy remains one of the most mature and commercially competitive segments within the renewable energy market. Strong capacity factors, technological maturity, and declining operating costs continue to support large-scale deployment across onshore and offshore installations. Investment activity increasingly focuses on maximizing electricity generation through larger turbines, advanced blade designs, and improved predictive maintenance capabilities.

Offshore wind has emerged as a strategic growth area because stronger and more consistent wind resources improve long-term project economics. Governments are expanding offshore leasing programs to strengthen energy security while reducing dependence on fossil fuel imports. Floating wind technologies are also extending development opportunities into deeper coastal waters previously considered commercially inaccessible.

Digital technologies are transforming operational performance. Artificial intelligence-enabled forecasting, condition monitoring, and remote diagnostics improve turbine availability while reducing maintenance expenditures. These capabilities strengthen project profitability throughout the operational lifecycle.

Onshore wind capacity has increased from 178 GW in 2010 to 699 GW in 2020, as wind growth has increased on land, but from a low base, from 3.1 GW in 2010 to 34.4 GW in 2020. Wind power generation has increased by 5.2% between 2009 and 2019 to reach 1412 terawatt hours.

Hydropower, also known as hydroelectricity, provides benefits to local communities and plays an important role in helping to combat climate change by providing storage, energy, and livelihood services.

Bioenergy

Feedstock diversity distinguishes bioenergy from other renewable technologies. Agricultural residues, forestry by-products, municipal waste, and dedicated energy crops provide multiple resource pathways capable of supporting electricity generation, heating applications, and renewable fuel production. This flexibility enables bioenergy to complement intermittent renewable resources within integrated energy systems.

Dispatchable generation represents a significant competitive advantage. Unlike weather-dependent technologies, bioenergy facilities can produce electricity according to demand, improving grid stability and supporting system balancing requirements. These operational characteristics enhance their strategic importance in regions pursuing higher renewable penetration.

Circular economy principles further strengthen investment interest. Converting organic waste streams into energy supports resource efficiency while reducing landfill dependence and methane emissions. Governments increasingly recognize these environmental benefits within broader waste management and climate strategies.

Commercial viability depends on sustainable feedstock availability, logistics efficiency, and regulatory support. Operators capable of securing reliable biomass supply chains while optimizing conversion technologies are positioned to strengthen renewable energy market share across selected regional markets.

Geothermal

Geothermal energy occupies a distinctive position within the renewable energy market because it provides continuous baseload electricity independent of weather conditions. Stable output and high availability make geothermal resources particularly valuable for power systems requiring reliable generation alongside intermittent renewable technologies.

Resource availability remains geographically concentrated. Countries possessing significant geothermal reservoirs continue to expand investment to strengthen domestic energy security and reduce imported fuel dependence. Technological advances in drilling techniques and reservoir management are gradually improving project feasibility across additional regions.

Operational longevity contributes to favorable lifecycle economics. Once commissioned, geothermal facilities generally deliver predictable electricity production with comparatively low operating costs. These characteristics attract infrastructure investors seeking stable long-term returns.

Emerging enhanced geothermal technologies may broaden future deployment opportunities by improving access to previously uneconomic resources. Continued research and engineering innovation are expected to strengthen geothermal's contribution to renewable energy market trends.

Ocean Energy

Ocean energy remains an emerging segment characterized by significant long-term potential rather than widespread commercial deployment. Wave, tidal, and ocean current technologies offer predictable renewable generation profiles capable of complementing existing energy portfolios. Coastal nations are increasingly evaluating these resources as part of diversified decarbonization strategies.

Technology development remains the principal investment focus. Engineering improvements targeting durability, corrosion resistance, and energy conversion efficiency are essential for reducing lifecycle costs. Pilot projects continue generating operational experience necessary for commercial scaling.

Government funding and research collaborations play an important role because early-stage technologies require sustained innovation before achieving broad market competitiveness. Partnerships involving technology developers, universities, and public agencies are accelerating demonstration activities.

Although current market penetration remains limited, ocean energy represents an important long-term opportunity within the renewable energy industry because of its resource abundance and predictable generation characteristics.

Hydropower

Hydropower continues to provide the largest share of renewable electricity generation globally because of its established infrastructure, operational flexibility, and long asset lifecycles. Large reservoirs and run-of-river facilities support both baseload generation and grid balancing, making hydropower a cornerstone of many national electricity systems.

Grid stability represents one of hydropower's primary strengths. Rapid response capability enables operators to balance fluctuations associated with variable wind and solar generation. Pumped storage hydropower also contributes significantly to energy storage and system reliability.

Modernization initiatives are increasingly important as mature facilities undergo refurbishment to improve efficiency, environmental performance, and operational flexibility. Digital monitoring systems and turbine upgrades extend asset lifecycles while enhancing electricity output.

Environmental considerations remain influential during project planning. Water resource management, ecosystem protection, and community engagement are becoming increasingly integrated into development strategies. These priorities continue to shape hydropower investment within the broader renewable energy market.

By End-User

Increased Demand for Renewable Energy in the Utility Sector Boosts Segment Growth

By end-user, the market is divided into residential, commercial, industrial, and utility.

Utility

The utility segment dominates the renewable energy industry. The segment dominated the market share by 53.96% in 2024. The utility sector uses electricity to run industrial machines, lighting, computers, and office equipment, as well as equipment for cooling and heating spaces. In the industrial sector, manufacturing accounts for the largest share of annual industrial energy consumption, followed by mining, construction, and agriculture. Solar panel installation on the spot, wind energy, and hydropower on a large scale in industrial installations increased the demand in the industrial sector.

Utility operators remain the largest end-user segment within the renewable energy market because they are responsible for supplying electricity across national and regional power systems. Utility-scale renewable projects benefit from economies of scale, long-term financing structures, and integration with transmission infrastructure, enabling efficient deployment of large generation capacities.

Capacity planning increasingly reflects changing electricity demand and national decarbonization objectives. Utilities are replacing aging fossil fuel assets with diversified renewable portfolios that combine solar, wind, hydropower, and energy storage technologies. These investments improve system flexibility while reducing long-term operating emissions.

There is a huge demand for thermal energy for heating applications in the residential sector of the world. In 2026, the residential segment is projected to lead the market with a 14.88% share. Rapid urbanization and the rising need for electricity are boosting the demand for thermal energy in the residential sector. Increasing consumer awareness in developed and developing economies is expected to support the adoption of sources in the future.

Commercial solar PV panels have a lifecycle of 15-20 years and can be used to power industrial buildings outdoors or in remote areas, and water heating in office companies. The rapid use of PV modules in corporate offices, hotels, and hospitals is necessary. Driving product demand across industries and increasing power needs in information base stations and data centers.

Residential

Consumer purchasing behavior is increasingly shaped by long-term electricity cost management, energy independence, and sustainability objectives. Residential customers are investing in rooftop solar systems, battery storage, and smart energy management platforms to reduce reliance on conventional electricity networks. Declining equipment costs and supportive financing mechanisms continue improving affordability, encouraging broader adoption across both developed and emerging housing markets.

Policy support remains an important catalyst for residential deployment. Net metering programs, tax incentives, feed-in tariffs, and low-interest financing schemes improve project economics while shortening investment payback periods. These mechanisms have encouraged homeowners to view renewable energy installations as long-term infrastructure investments rather than discretionary purchases.

Technology integration is becoming more sophisticated. Residential renewable systems increasingly operate alongside electric vehicle charging infrastructure, home energy storage, and intelligent demand management platforms. Such integration improves energy utilization while increasing self-consumption of locally generated electricity.

Commercial

Commercial organizations increasingly regard renewable electricity as a strategic operating asset rather than solely an environmental initiative. Office complexes, retail facilities, educational institutions, healthcare providers, and hospitality businesses are adopting renewable energy systems to improve cost predictability while advancing corporate sustainability commitments. Stable operating expenses and stronger environmental credentials enhance the financial attractiveness of renewable investments.

Energy procurement strategies are becoming increasingly diversified. Commercial customers frequently combine onsite generation with long-term power purchase agreements and renewable energy certificates to optimize energy portfolios. These approaches improve resilience while reducing exposure to electricity price volatility.

Building modernization programs further support adoption. Smart building technologies, advanced energy management systems, and digital monitoring platforms enable businesses to maximize renewable energy utilization while improving operational efficiency. Integration with battery storage enhances reliability and peak demand management.

Growing investor attention toward environmental, social, and governance performance also strengthens commercial demand. Organizations demonstrating measurable decarbonization progress often improve stakeholder confidence and strengthen long-term competitive positioning within their respective industries.

Industrial

Industrial users represent one of the fastest-evolving customer groups within the renewable energy market because electricity constitutes a significant operating expense across manufacturing, mining, chemicals, metals, and processing industries. Renewable energy procurement increasingly supports both cost optimization and corporate decarbonization strategies, particularly for businesses operating energy-intensive production facilities.

Long-term contractual arrangements are becoming increasingly common. Industrial organizations frequently secure renewable electricity through dedicated generation assets, direct power purchase agreements, or hybrid procurement models designed to ensure supply stability. These strategies improve budgeting certainty while reducing exposure to fossil fuel market volatility.

Electrification of industrial processes is expanding renewable energy demand. Hydrogen production, advanced manufacturing technologies, and digital production facilities require reliable low-carbon electricity to support operational efficiency and sustainability objectives. Consequently, renewable infrastructure is becoming increasingly integrated into industrial investment planning.

To know how our report can help streamline your business, Speak to Analyst

Regional Analysis of Renewable Energy Industry

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia-Pacific Renewable Energy Market Analysis

Asia Pacific Renewable Energy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Economic Growth of Asian Countries is Promoting the Expansion of the Renewable Energy Sector

As the world's fastest-growing region, the Asia Pacific needs to increase energy resources to accelerate its economic growth. The Asia Pacific renewable energy market accounted for USD 730.08 billion in 2025, representing 67.68% of the global industry, and is expected to reach USD 773.73 billion in 2026.

Rapid industrialization, rising electricity consumption, and supportive government policies position Asia-Pacific as the fastest-expanding renewable energy market. Large-scale solar and wind investments are transforming regional generation portfolios. Manufacturing leadership and competitive equipment supply chains improve project economics. Expanding transmission infrastructure and increasing institutional investment continue to support renewable energy market growth across major economies.

The geographical size of the Asia Pacific region, its diversity, and its diverse regulatory capacity provide a large market. Renewable energy is another opportunity for the region to achieve a major global position in the market and to be a leader in the transition to clean energy. Many Asian countries have abundant geothermal resources. Countries such as Indonesia and the Philippines use geothermal energy to generate electricity, but the widespread use of geothermal heat is popular in other countries.

At the end of 2017, the total thermal energy capacity of the 18 countries was 22.4 GWh. Biomass, especially traditional biomass as a fuel, is used for heating in remote areas, although there is little data on this use.

Nine countries in the region produce biofuel for transportation, with the largest share coming from the People's Republic of China, India, Thailand, and Indonesia, which are also among the world's leading biofuel producers. The total production in this area was 12 million tons in 2018, an increase of 2.5 million tons compared to the previous year. About 45% of this fuel production, and the remaining 55% is biodiesel Fatty Acid Methyl Esters (FAME).

Renewable capacity has increased to 988.9 gigawatts (GW) in 2018, due to the acceleration of wind and solar technologies. While hydropower had the largest share at 46%, the share of solar cells and wind energy reached 28% and 23%, respectively. Bioenergy is about 3%, and geothermal (in China, Indonesia, Japan, and the Philippines) is 0.45%. The Republic of Korea and China have 255 megawatts (MW) and 4.3 MW, respectively. India is likely to reach USD 30.9 billion, and Japan is projected to hit USD 23.58 billion in 2026.

Japan Renewable Energy Market

Japan continues to strengthen its renewable energy market through solar deployment, offshore wind development, and grid modernization initiatives. Energy security priorities and carbon neutrality objectives encourage investment in diversified renewable technologies. Corporate electricity procurement and advanced energy management systems support market expansion. Technological innovation and supportive regulatory reforms reinforce Japan's long-term renewable energy industry outlook.

China Renewable Energy Market

Rapid Expansion of Solar and Wind Power in China is Advancing Market Growth

China is the world leader in renewable energy consumption, with an annual installation of 312 GW of renewable energy in 2023. In 2023, China's solar power generation reached 584 TWh. In 2022, China installed roughly as much solar capacity as the rest of the world combined and doubled new solar installations in 2023.

The market in China is expected to hit USD 679.18 billion in 2026. Chinese energy investments remained extremely strong, accounting for one-third of clean energy investments globally and an important share of China’s overall GDP growth. China has announced dual carbon goals to peak carbon emissions before 2030 and achieve carbon neutrality before 2060 – and has shown remarkable progress in adding renewable capacity.

In 2023, China commissioned as much solar PV as the entire world did in 2022, while its wind additions also grew by 66% year-on-year. Over the past five years, China also added 11 GW of nuclear power, by far the largest of any country in the world. The Chinese renewable energy market is projected to reach USD 679.18 billion by 2026.

North America

Technological Advancements to Boost Market Growth

North America is anticipated to account for the second-highest market size of USD 143.97 billion in 2026, exhibiting the second-fastest CAGR of 3.32% during the forecast period. The region maintained a strong presence in the global market, reaching USD 139.00 billion in 2025 and accounting for a 12.89% market share.

Investment certainty, grid modernization, and supportive policy frameworks underpin North America's leadership within the renewable energy market. Utilities and corporate buyers continue expanding renewable generation portfolios to strengthen energy security and decarbonization efforts. Battery storage integration and transmission upgrades remain strategic priorities. Strong institutional investment and technological innovation continue to support renewable energy market growth across the regional power sector.

North America is a growing market with advancements in technology and the adoption of new policies to increase penetration in the region. In Canada, water, gas, and wind energy technologies play an important role in future energy self-sufficiency. Increased energy trade between countries could bring USD 10-30 billion in net value to the system. Expanding inter-border transit could bring net benefits of USD 180 billion. Although these amounts are a small percentage (less than 4%) of the total system cost of USD 5-8 trillion (including all capital and operating costs of the generation and transmission system), they have a great opportunity to reduce costs.

United States Renewable Energy Market

Rapid Growth of Solar Energy to Boost Renewable Energy Penetration in the U.S.

In the U.S., between 1,200 and 2,000 GW of renewable energy could be used to generate 70 to 80% of U.S. electricity by 2050 while meeting projected storage needs. The country depends on renewable energy for significant power generation, particularly in the form of hydropower. In Canada, hydropower accounts for 63% of electricity generation, and some of the dams are over 100 years old.

The United States represents a major contributor to the renewable energy market size through large-scale solar, wind, and energy storage deployment. Corporate power purchase agreements and utility investments continue accelerating renewable capacity additions. Manufacturing incentives and domestic supply chain expansion strengthen industry competitiveness. Grid modernization initiatives and increasing electricity demand reinforce long-term renewable energy market growth across diverse end-use sectors.

The U.S., home to famous hydroelectric projects, such as the Hoover Dam, which dams the Colorado River, pioneered solar power and remains a powerhouse of energy technology. The solar industry employs more than 260,000 people in this country, creating jobs 17 times faster than the average. The U.S. renewable energy market size is estimated to be USD 132.03 billion in 2026.

Europe Renewable Energy Market Analysis

Government Initiatives in Europe are Helping in the Regional Growth

In 2025, Europe generated USD 130.06 billion, contributing 12.06% to global market revenue, and is projected to grow to USD 138.08 billion in 2026. In the last two years, the production and consumption of renewable energy have increased rapidly across Europe in response to dedicated policies and measures due to the rapid development of technology and the use of renewable electricity.

Climate policy leadership and ambitious decarbonization targets continue shaping Europe's renewable energy market. Offshore wind, solar expansion, and cross-border electricity interconnections remain central investment priorities. Energy security considerations are accelerating renewable deployment and grid modernization programs. Mature regulatory frameworks, technological innovation, and institutional financing collectively strengthen renewable energy market share throughout the region.

As a result, greenhouse gas emissions in the EU energy system have been steadily decreasing since 1990, and the EU reached its 2020 target of 20%. EU aims to raise the share of renewables in final energy consumption to 42.5% by 2030. Solar panels on rooftops, electric cars, and wind turbines on the horizon are becoming increasingly visible across Europe. However, fossil fuels are still the chief source of energy. The market value in the U.K. is expected to be USD 10.57 billion in 2026.

The share of energy consumed in Europe in 2022 that came from renewable sources was 23%. This increase, from a level of 21.9% in 2021, is due to the strong growth of solar energy. This sector was also strengthened by the reduction of non-renewable energy consumption in 2022, linked to high energy prices, but renewable energy in Europe will continue to grow. Achieving the new target of 42.5% by 2030 would more than double the deployment of renewable energy seen in the past decade and profoundly transform the European energy system.

Germany Renewable Energy Market

Germany is projected to hit USD 47.55 billion in 2026, and France is likely to hold USD 11.44 billion in 2025. Germany maintains a leading position within the renewable energy market through sustained investment in wind, solar, and grid infrastructure. Industrial decarbonization strategies and expanding renewable electricity demand continue to support project development. Modernization of transmission networks and energy storage deployment enhances system flexibility. Engineering expertise and supportive regulatory frameworks reinforce Germany's contribution to renewable energy market growth.

United Kingdom Renewable Energy Market

Offshore wind development and net-zero commitments define the United Kingdom renewable energy market. Long-term policy support encourages investment across renewable generation, electricity storage, and transmission infrastructure. Corporate renewable procurement and power market reforms further stimulate capacity expansion. Advanced project financing capabilities and engineering expertise continue to strengthen the country's renewable energy market position and long-term competitiveness.

Latin America Renewable Energy Market Analysis

Accelerating Growth of Biofuels to Fuel Market Growth

Latin America is vast and diverse in terms of economic development and natural resources. Latin America contributed 4.67% to the global market in 2025, with a valuation of USD 50.35 billion, and is projected to reach USD 52.59 billion in 2026. The country is rich in fossil fuels and precious minerals. While biofuels are used in Brazil, hydroelectric power is used in Brazil, Venezuela, Mexico, Colombia, Argentina, and Paraguay, and solar and wind resources are used in Brazil, Mexico, Chile, and Argentina.

Abundant natural resources and improving investment environments support renewable energy development across Latin America. Hydropower, wind, and solar projects continue diversifying regional electricity generation portfolios. Government auctions and private infrastructure investment encourage capacity expansion. Rising electricity demand, transmission improvements, and favorable resource availability strengthen renewable energy market growth across key regional economies.

The production of copper or lithium in Chile, Peru, and Argentina, the most important minerals for clean energy technology, or using large oil and natural gas resources in Venezuela, Brazil, Colombia, Argentina, Mexico or Guyana, Latin America and the Caribbean are well positioned to promote the transition to clean energy and have opportunities to global energy security and climate goals.

According to the World Economic Forum, Brazil has increased its renewable energy and share of clean energy due to long-term investment in hydropower and biomass while using solar and wind energy. Brazil's focus on planning and policy tools guarantees that businesses have created the necessary ecosystem for the energy transition movement. Brazil, the largest country in South America and the fifth in the world, has for many years demonstrated its commitment to transitioning to renewable energy. It currently uses almost half of its energy (49%) from renewable sources.

Middle East & Africa Renewable Energy Market Analysis

Government Initiatives are Creating Opportunities for the Regional Market

In 2025, the Middle East & Africa represented USD 29.21 billion, accounting for 2.71% of the worldwide market, and is projected to grow to USD 30.34 billion in 2026. Economic diversification and growing electricity demand are accelerating renewable energy investments across the Middle East and Africa. Utility-scale solar, wind, and emerging green hydrogen projects are reshaping regional energy strategies. Infrastructure modernization and international investment continue to support project development. Resource availability and long-term policy commitments strengthen renewable energy market growth.

According to the IRNA World Energy Transition Outlook (WETO) analysis, the Middle East & Africa can obtain approximately 26% of the total primary energy from renewables by 2050, which is the share of renewable energy reaching 53% in the electricity sector. This will decrease greenhouse gas emissions by 1.1 Gt CO2 per year. The number of professions in the sector in the region under the energy transition scenario will reach 2 million, from 542,000 in 2017.

Accordingly, the green hydrogen market in the Middle East is moving from what seems to be the future to reality, with many initiatives at the national level to meet demand from export and import markets. The GCC market size is expected to be USD 23.41 billion in 2025.

Competitive Landscape

Key Industry Players

GE Vernova Leads with Its Innovative Energy Solutions

The global market is mostly fragmented, with key players operating in the industry. Globally, GE Renewable Energy (Vernova), Tata Power Solar, and Renewable Energy Group are dominating the market. GE Renewable Energy (Vernova) was a manufacturing and services division of the American company General Electric. It is an American multinational conglomerate that was established in 1892, incorporated in New York State, and headquartered in Boston. GE Vernova brings to market innovative solutions that deliver essential energy, renewable energy, and transportation infrastructure. The company also works with the utmost integrity, amenability culture, and admiration for human rights while also reducing the impact of its environmental and technology footprint.

Competitive intensity within the renewable energy market is determined by project execution capability, technology innovation, capital access, and long-term asset management expertise rather than equipment manufacturing scale alone. Market participants compete across project development, engineering, procurement, financing, operations, and digital energy management. As renewable deployment accelerates globally, companies capable of integrating generation assets with storage, transmission, and intelligent grid solutions are strengthening their competitive positions.

Leading global participants include NextEra Energy, Iberdrola, Enel Green Power, Ørsted, Brookfield Renewable Partners, EDF Renewables, RWE, TotalEnergies, ACCIONA Energía, and ENGIE. These organizations maintain substantial renewable energy market share through diversified technology portfolios, geographically balanced asset bases, and disciplined capital allocation strategies. Vertical integration across development, construction, operations, and asset optimization enables them to improve project economics while reducing execution risk.

Technology providers continue differentiating through innovation in photovoltaic modules, wind turbine platforms, battery energy storage systems, power electronics, and digital monitoring solutions. Strategic investments in artificial intelligence-enabled forecasting, predictive maintenance, and grid optimization technologies are improving asset availability and lifecycle performance. Such capabilities have become increasingly important as utilities seek greater operational flexibility and higher renewable penetration.

Strategic partnerships are reshaping competitive dynamics across the renewable energy industry. Developers increasingly collaborate with utilities, financial institutions, equipment manufacturers, transmission operators, and technology companies to accelerate project deployment and optimize financing structures. Joint ventures are particularly common in offshore wind, utility-scale solar, battery storage, and green hydrogen projects where technical complexity and capital requirements remain substantial.

Top Renewable Energy Companies Analyzed

- Enel Green Power (Italy)

- Canadian Solar Inc. (Canada)

- First Solar Inc. (U.S.)

- Jinko Solar Holding (China)

- Tata Power Solar (India)

- Engie (France)

- Vestas Wind System (Denmark)

- Siemens Gamesa Renewable Energy (Germany)

- GE Renewable Energy (Vernova) (U.S.)

- Goldwind (China)

- Envision Energy (China)

- Renewable Energy Group (U.S.)

- POET (U.S.)

- Drax Group (U.K.)

- Cosan (Brazil)

- ADM (U.S.)

- Toshiba (Japan)

- Centrais Elétricas Brasileiras (Brazil)

- RusHydro (Russia)

- Statkraft (Norway)

- ANDRITZ AG (Austria)

- Nova Innovation (Scotland)

- SIMEC Atlantis Energy (U.K.)

- Orbital Marine Power (U.K.)

- Sustainable Marine Energy Ltd. (Scotland)

- Calpine (U.S.)

- Ormat Technologies, Inc. (U.S.)

- Chevron (U.S.)

- Mitsubishi Power (Japan)

- Fuji Electric (Japan)

- Veolia (France)

Recent Renewable Energy Industry Key Developments

- February 2025: Enel presented its 2026–2028 Strategic Plan, allocating approximately €20 billion toward renewable energy expansion with a target to add around 15 GW of new renewable capacity by 2028. The strategic purpose was to accelerate clean electricity generation, strengthen capital discipline, and expand its integrated renewable portfolio. Technologies and capabilities involved included onshore wind, solar photovoltaic generation, battery energy storage systems, and hybrid renewable energy projects.

- May 2025: TotalEnergies commissioned its largest solar project in Europe, comprising five photovoltaic plants with a combined installed capacity of 263 MW in Seville, Spain. The strategic purpose was to expand renewable electricity generation, strengthen the company's integrated power portfolio, and support Spain's decarbonization objectives. Technologies and capabilities involved included utility-scale solar photovoltaic systems, advanced asset management platforms, and long-term renewable electricity integration.

- September 2025: TotalEnergies unveiled its updated 2025 Strategy and Outlook, reaffirming plans to increase annual electricity production to 100–120 TWh by 2030, with approximately 70% derived from renewable sources. The strategic purpose was to accelerate profitable growth in integrated power while strengthening long-term energy transition resilience. Technologies and capabilities involved included utility-scale solar, onshore and offshore wind, battery energy storage, and integrated electricity generation and trading capabilities.

- September 2025: Iberdrola updated its long-term strategic investment program, increasing planned investment through 2028 while prioritizing electricity networks, renewable generation, and energy storage across major international markets. The strategic purpose was to reinforce regulated asset growth, improve grid resilience, and expand renewable electricity capacity. Technologies and capabilities involved included offshore wind, solar photovoltaic projects, battery energy storage systems, and smart electricity grid infrastructure.

- December 2025: NextEra Energy expanded its strategic collaboration with Google Cloud to develop approximately 15 GW of new power generation capacity supporting future hyperscale data center campuses in the United States. The strategic purpose was to address rapidly growing electricity demand from artificial intelligence infrastructure while accelerating deployment of low-carbon generation assets. Technologies and capabilities involved included utility-scale renewable energy generation, digital energy management, cloud-enabled infrastructure planning, and grid-scale power development

INVESTMENT ANALYSIS AND OPPORTUNITIES

In 2023, private equity and venture capital transactions in the renewable energy sector reached nearly USD 15 billion, the highest total in the last five years. Private equity firms are drawn to renewable energy due to its economic benefits, such as low-cost power, reduced reliance on imported fuel, and a more reliable energy supply. There are opportunities for higher cash flows and capital value improvement in adjacent technologies, such as green hydrogen, battery energy storage systems, and the electrification of heat, cooling, and transport.

GE Renewable Energy is a USD 16 billion business that combines one of the broadest portfolios in the renewable energy industry to provide end-to-end solutions for customers demanding reliable and affordable green power. GE Renewable Energy has installed more than 400+ gigawatts of clean, renewable energy and equipped more than 90% of utilities worldwide with its grid solutions.

Further, GE is strengthening its financial services in India's market through its partnership with Continuum, an India-focused renewable energy group, with 4 GW of which 855.4 MW of operating capacity, 444.4 MW is under construction, supported by strong government support, and a renewable energy target of 500 GW by 2030. By 2021, more than 1.2 GW of orders will be received from GE Renewable Energy in India, as it is the largest producer of wind power equipment.

Capital allocation across the renewable energy market continues to accelerate as institutional investors increasingly prioritize infrastructure assets offering predictable long-term cash flows and inflation-linked revenue profiles. Utility-scale solar, onshore and offshore wind, battery energy storage systems, and transmission infrastructure remain the primary destinations for investment because they benefit from improving project economics, supportive policy frameworks, and rising electricity demand. Infrastructure funds, pension investors, sovereign wealth funds, and strategic energy companies are expanding renewable portfolios to strengthen long-term returns while supporting energy transition objectives.

Investment activity is also broadening beyond conventional generation assets. Technologies such as green hydrogen, long-duration energy storage, grid digitalization, and renewable-powered industrial decarbonization are attracting higher levels of private capital despite relatively early commercialization stages. These adjacent markets offer opportunities for stronger value creation as industrial electrification, low-carbon manufacturing, and clean fuel production become increasingly important across global energy systems.

Emerging economies present particularly attractive investment prospects because expanding electricity demand, favorable renewable resource availability, and supportive government policies continue to improve project pipelines. Countries investing in transmission infrastructure, domestic equipment manufacturing, and streamlined permitting processes are expected to attract greater international capital over the medium term. Public-private partnerships and blended finance structures are further reducing investment risks for large-scale renewable projects.

Report Coverage

The global renewable energy market report delivers a detailed insight into the market. It focuses on key aspects such as leading companies and their operations in drilling and producing renewable energy. Besides, the report offers insights into the market trends & technology and highlights key industry developments. In addition to the factors above, the report encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.17% from 2026 to 2034 |

|

Unit |

Value (USD Billion) and Volume (MW) |

|

Segmentation |

By Type

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 1078.7 billion in 2025.

The market is likely to grow at a CAGR of 6.17% over the forecast period.

The utility segment leads the market.

The market size of Asia Pacific stood at USD 730.08 billion in 2025.

Rising efforts to reduce the effects of high carbon emissions are the key factors driving the market growth.

Some of the top players in the market are GE Renewable Energy, Tata Power Solar, Renewable Energy Group, and others.

The global market size is expected to reach USD 1838.57 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 255

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us