Infrared Sensors Market Size, Share & Industry Analysis By Wavelength (Near Infrared (NIR), Mid Infrared (MIR), and Far Infrared (FIR)), By Sensor Type (Active and Passive (Thermal IR Sensors and Quantum IR Sensors)), By Application (Motion Sensing, Temperature Measurement, Security and Surveillance, Gas and Fire Detection, Spectroscopy, and Others), By End-Use (Consumer Electronics, Aerospace and Defense, Industrial, Healthcare, Automotive, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

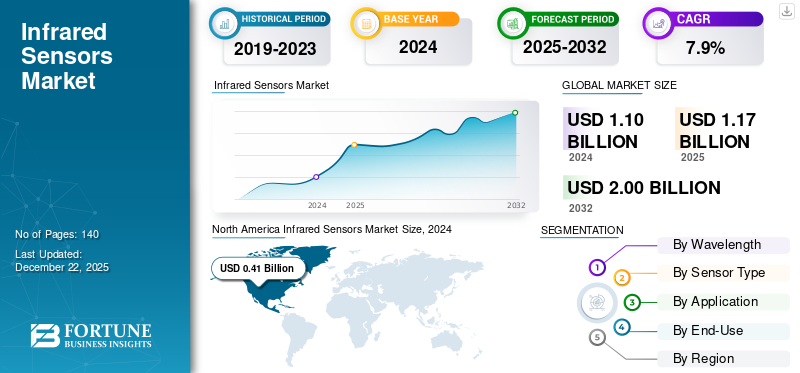

The global infrared sensors market size was valued at USD 1,173.70 million in 2025. The market is projected to grow from USD 1,256.30 million in 2026 to USD 2,294.20 million by 2034, exhibiting a CAGR of 7.8% during the forecast period.

An IR sensor is an electronic device that emits light to detect objects in its surroundings. The major players included in this market are Panasonic Corporation, Hamamatsu Photonics K.K., Murata Manufacturing Co., Ltd., Texas Instruments Incorporated, Raytheon Technologies Corporation, Honeywell International Inc., NXP Semiconductors N.V., Teledyne Technologies Incorporated, Excelitas Technologies Corp., and Lynred.

Many factors, including the growth of smart consumer products and non-contact temperature measurement, drive market growth. Industry analysts stated that global smart home device shipments stagnated in 2024 at 892.3 million devices. The increased interest in battery-powered applications such as wearables and IoT devices is pushing the demand for low-power designs in the IR sensors sector. Moreover, these sensors can enable energy-saving devices that modulate power usage based on user proximity and surroundings.

The COVID-19 pandemic created a heightened demand for infrared sensors in public settings, particularly for non-contact temperature checks, fever detection, and crowd management. Healthcare, transportation, retail, and industrial sectors accounted for many of the sensors used in the non-invasive screening of interactions for promoting public health.

Download Free sample to learn more about this report.

Infrared Sensors Market KEY TAKEAWAYS

- 2025 Market Size: USD 1,173.70 million

- 2026 Market Size: USD 1,256.30 million

- 2034 Forecast Market Size: USD 2,294.20 million

- CAGR: 7.8% from 2026–2034

- North America dominated the infrared sensors market with a 37.00% share in 2025.

- The near infrared (NIR) segment accounted for the largest market share of 44.86% in 2026.

- The active sensor type segment held the largest market share of 59.29% in 2026.

Asia Pacific

Asia Pacific reached USD 408.0 million in 2025, driven by strong demand from consumer electronics and automotive industries.

North America

North America reached USD 434.4 million in 2025, supported by technological advancements and widespread adoption across key industries.

Europe

Europe reached USD 203.1 million in 2025, driven by increasing use of infrared sensors in energy-efficient and smart building applications.

U.S.

The U.S. market is projected to reach USD 349.7 million by 2026, fueled by strong R&D and innovation.

Japan

Japan is projected to reach USD 98.7 million by 2026, supported by growing demand from consumer electronics and automotive sectors.

Read More

IMPACT OF GENERATIVE AI

Advantage of Enhanced Sensor Data Analysis via Generative AI to Impel Industry Expansion

Generative AI provides improved sensor data analysis, including noise reduction, synthetic IR images for training, and multimodal data building. AI models will increase the clarity of the image, facilitate better detection of anomalies, and allow for better real-time understanding of sensor output.

IMPACT OF RECIPROCAL TARIFFS

In 2025, U.S. reciprocal tariffs will radically alter the IR sensor industry, causing rising costs, modifying global supply chains, and re-establishing domestic advancement. This will ultimately encourage domestic production and integration. Companies are likely to diversify manufacturing locations or transfer supply chains to overcome tariff challenges.

MARKET DYNAMICS

Market Drivers

Rising Adoption of Smart Devices in Consumer Electronics to Aid Market Growth

As technological advancements and smart devices have become more prevalent, infrared sensors have many applications in consumer electronics. Smart devices such as smartphones, tablets, and smart home devices utilize infrared level (or proximity) sensors for gesture recognition, proximity detection, and day and night ambient light detection. The increased use of AR and VR-enabled devices employing IR sensors enhances user interaction with the product in a more immersive experience. Demand Sage states that over 171 million people worldwide use VR technology.

Market Restraints

Technical Specification Complexities to Hinder Market Expansion

The constraints of infrared sensors create notable obstacles in the expansion of the market. For instance, infrared frequencies can be influenced by physical barriers such as walls and doors, along with dust, fog, and sunlight. Furthermore, in screen and control applications, these sensors are limited to managing one device at a time, making it difficult to oversee items that are not directly visible. These complexities are hampering the growth of the infrared sensors market.

Market Opportunities

Increase in Security and Surveillance Systems to Create Lucrative Market Opportunities

The rising demand for security and surveillance systems provides opportunities for IR sensors; thus, heightened security concerns characterize the need for such systems. Governments, corporations, and private citizens constantly invest in advanced surveillance technologies to protect their assets, infrastructure, and people. IR sensors play a crucial role in these systems since they can detect heat signatures and motion under any light conditions and weather situation, accounting for enhanced surveillance efficiency. In addition, increased criminal activities, terrorist threats, and geopolitical tensions across the globe have created a strong demand for security solutions.

Infrared Sensors Market Trends

Substantial Need for Energy-Efficient Devices to Emerge as a Key Market Trend

Infrared sensors are driving energy-efficient designs since they allow power consumption concerning the users and environmental conditions can be regulated. The consumer tilt toward connected and intelligent devices pushes the adoption of infrared sensors across various product categories. The escalated adoption underpins their role in making technology more functional and sustainable.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Wavelength

Demand for Adaptability and Affordability in Various Industries Boosted the Expansion of NIR Wavelengths

Based on wavelength, the market is segmented into near infrared (NIR), mid infrared (MIR), and far infrared (FIR).

By a share of 44.86%, the near infrared (NIR) segment is likely to secure the market in 2026 as it is broadly used in major industries such as healthcare, automotive, and environmental monitoring. The NIR wavelength offers choices and low costs, making it the preferred selection for many commercial and industrial applications, driving the leading market share of the segment.

The far infrared (FIR) segment is set to show the highest compound annual growth rate (CAGR) over the forecast period. This results from the sensors’ excellent thermal imaging and temperature measurement capabilities that are critical in numerous applications.

By Sensor Type

Active Sensors Dominated the Market with Their Enhanced Features in Precise Detection and Measurement

Based on sensor type, the market is categorized into active and passive.

In 2026, the active sensor type segment led the global market share of 59.29%, as these sensors can deliver more reliable and precise measurements than passive systems. They produce IR light and track the reflections to detect accurately, and measurements can be achieved even under low-light conditions. The growing demand for automation and advanced security systems has increased the adoption of active IR sensors, strengthening their market dominance.

The passive sensor type segment is expected to witness the highest CAGR during the forecast period. Its cost-effectiveness and energy efficiency make it an attractive option for many applications. Unlike their counterparts, PIR (passive infrared) sensors detect IR radiation from objects that emit light. Therefore, they can be used for motion detection in lighting management, security systems, and home automation.

By Application

Motion Sensing Dominated the Market with Its Widespread Usage in Various Industries

By application, the market is categorized into motion sensing, temperature measurement, security and surveillance, gas and fire detection, spectroscopy, and others.

In 2026, the motion sensing segment is expected to capture the largest market share of 32.88%, primarily owing to widespread application in consumer electronics, home automation, and security systems. Motion sensors detect movement in and around the home, triggering responses such as lights, alerts, and automation controls, making them vital to commercial and home safety. Additionally, the industry rules their market with motion sensors embedded into various devices, from smartphones to gaming consoles.

The gas and fire detection segment is expected to record the highest CAGR during the forecast period, owing to its critical role in ensuring industrial safety and meeting compliance requirements. These sensors offer reliable services for detecting fires and gas leaks in various sectors, such as oil and gas, manufacturing, and residential safety systems. An expanding domain of the sector for motion sensors is in consumer electronics, with enhanced safety regulations and increasing awareness of accident prevention.

By End-Use

To know how our report can help streamline your business, Speak to Analyst

Consumer Electronics Dominated Market for Increasing Need of Smart Devices and Safety for Customers

The market is categorized by end-use into consumer electronics, aerospace and defense, industrial, healthcare, automotive, and others.

The consumer electronics segment was the primary segment in 2024 due to the growing need for smart home devices, functionality in greater security, and effective IoT Technology applications. End-users can expect IR sensors to provide capabilities such as night vision, proximity sensing, and remote control functions for consumer offerings to use daily. This ultimately enhances the user experience and operation.

The healthcare segment is likely to surge at the highest CAGR during the forecast period. IR sensors are heavily implemented in medical diagnostics products and imaging devices for non-invasive visual observations. They are reliable tools for measuring temperature, monitoring vitals, and diagnosing abnormalities that lead to early-detection disease identification. While healthcare continues to improve through technology, infrared sensor implementation is expected to increase as the demand for fast, reliable, and non-invasive diagnostic tools rises.

INFRARED SENSORS MARKET REGIONAL OUTLOOK

By region, the market is divided into North America, Europe, South America, the Middle East & Africa, and Asia Pacific.

North America

North America Infrared Sensors Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 37.00% to the global market in 2025, with a valuation of USD 434.4 million, and is projected to reach USD 460.7 million in 2026, due to technological advancements that led to higher adoption rates in numerous industries. The region has strong capabilities in aerospace and defense industries, large investments in research and development, and a strong industrial foundation. Additionally, various regulatory requirements and the increasing number of applications in automotive safety, smart technologies, and healthcare strengthen dominance of the region in the market.

The U.S.’s market leadership is bolstered by its strong R&D framework, which promotes ongoing technological and innovation progress in IR sensor technologies. The U.S. market is projected to reach USD 349.7 million by 2026.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe accounted for USD 203.1 million in 2025, representing 17.30% of the global market share, and is projected to reach USD 216.4 million in 2026. The European market is expected to experience the second-largest growth throughout the predicted timeframe. Europe's focus on environmental regulations and energy efficiency requirements promotes the use of infrared sensors in building automation and climate monitoring applications, enhancing the region's market leadership. The UK market is projected to reach USD 45.8 million by 2026, while the Germany market is projected to reach USD 42.2 million by 2026.

South America

While there is an increasing need for automation in South America, businesses are limited in their awareness and spending capacity for infrared sensor systems. In 2025, the Latin America market stood at USD 43.8 million, representing 3.70% of global demand, and is projected to grow to USD 45.7 million in 2026.

Middle East & Africa

The market in Middle East & Africa reached USD 84.4 million in 2025, representing 7.20% of total market revenue, and is projected to reach USD 88.4 million in 2026. The region faces challenges, such as political instability, varying regulatory environments, and inadequate digital infrastructure in some areas, contributing to slower market development. On the other hand, growth is influenced by several elements, such as the rising demand for automation and advanced building technologies, along with government initiatives to develop smart cities and infrastructure.

Asia Pacific

The Asia Pacific market was valued at USD 408 million in 2025, capturing 34.80% of global revenue, and is estimated to reach USD 445 million in 2026. The region is home to some of the largest global consumer electronics manufacturing companies, whose parent companies are from Japan, South Korea, China, and Taiwan. Their IR sensors are on the rise due to a growing demand for applications in smartphones, tablets, and other smart devices for facial recognition, proximity reading, and remote sensing tasks. As the largest automotive producer, China's immense scale of vehicle production means that IR sensor adoption will increase. The requirement to integrate advanced sensing technologies into millions of vehicles generates a significant market for IR sensors. According to the Development Plan for the New Energy Automobile Industry in China (2021-2035), electric vehicles will attain a 25% market share by 2025. The Japan market is projected to reach USD 98.7 million by 2026, the China market is projected to reach USD 161.8 million by 2026, and the India market is projected to reach USD 61.1 million by 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Notable Players to Implement Strategic Strategies to Expand Business Reach

Mergers and acquisitions, partnerships, and investments will surge demand for this technology. Key players in this market offer infrared sensors to provide users with non-contact measurement, high accuracy, rapid response, versatility, energy efficiency, and others. They concentrate on striking contracts with small and local businesses to grow their business.

List of Key Infrared Sensors Companies Studied

- Panasonic Corporation (Japan)

- Hamamatsu Photonics K.K. (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- Texas Instruments Incorporated (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- Teledyne Technologies Incorporated (U.S.)

- Excelitas Technologies Corp. (U.S.)

- Lynred (France)

- Omron Corporation (Japan)

- L3Harris Technologies, Inc. (U.S.)

- Fluke Corporation (U.S.)

- Wuhan Guide Infrared Co., Ltd (China)

- Kado Intelligent Sensor Type (China)

- SENBA Sensing Sensor Type Co., Ltd (China)

- Amphenol Corporation (U.S.)

- InfraTec GmbH (Germany)

- KEMET (Yageo Group) (U.S.)

- Melexis NV (Belgium)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Hamamatsu Photonics introduced a mid-infrared detector module that complies with RoHS standards and includes an integrated preamplifier. This small and easy-to-use module is intended for operation at room temperature, delivering improved performance suitable for various applications.

- January 2025: Lynred introduced the Eyesential SW, a cost-effective shortwave infrared (SWIR) sensor for machine vision. This sensor delivers high resolution and rapid frame rates to improve industrial automation.

- April 2024: InfrecTec GmbH announced the completion of a newly built project extension. The new building is operational and the company is now focused on modernizing the existing site. Modernization has a large functional area for producing and developing innovative thermography cameras and infrared sensors.

- October 2023: Omron Automation introduced its SWIR camera series, which uses the latest Short-Wave IR technology to solve the most common problems in production.

- July 2023: STMicroelectronics, a global company that produces semiconductors for a variety of electronic applications, created a sensor for human motion to upgrade security systems, home automation devices, and IoT devices that are generally powered by PIR sensing.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Ongoing consolidations (e.g., FLIR acquisition by Teledyne) and partnerships (Himax with Obsidian Sensors for AI-integrated thermal vision) reflect the market's focus on technology integration and expanding capabilities, especially in AI/edge computing. Investors seeking exposure should consider established leaders for stable growth and smaller innovative firms/partnerships for higher risk-reward in emerging application verticals. Additionally, investors are supporting companies in seeking out more opportunities. For instance,

- In March 2025, a British startup, Phlux Technology, which focuses on infrared sensor technology, announced a Series A round of funding worth around 10 million dollars. This investment will boost Phlux’s growth into optical communications and sensing by utilizing its pioneering antimonide-based semiconductor technology to provide quicker and more energy-efficient sensor and connectivity solutions.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, product/types, and the leading end-use of the product. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.8% from 2026 to 2034 |

|

Unit |

Value (USD million) |

|

Segmentation |

By Wavelength

By Sensor Type

By Application

By End-Use

By Region

|

|

Companies Profiled in the Report |

Panasonic Corporation (Japan) Hamamatsu Photonics K.K. (Japan) Murata Manufacturing Co., Ltd. (Japan) Texas Instruments Incorporated (U.S.) Raytheon Technologies Corporation (U.S.) Honeywell International Inc. (U.S.) NXP Semiconductors N.V. (Netherlands) Teledyne Technologies Incorporated (U.S.) Excelitas Technologies Corp. (U.S.) Lynred (France) |

Frequently Asked Questions

According to Fortune Business Insights, the market is projected to reach a valuation of USD 2,294.20 million by 2034.

In 2025, the market was valued at USD 1,173.70 million.

The market is projected to record a CAGR of 7.8% during the forecast period.

By wavelength, the NIR segment led the market in 2025.

The rising adoption of smart devices in consumer electronics is a key factor aiding market growth.

Panasonic Corporation, Hamamatsu Photonics K.K., Murata Manufacturing Co., Ltd., Texas Instruments Incorporated, Raytheon Technologies Corporation, Honeywell International Inc., NXP Semiconductors N.V., Teledyne Technologies Incorporated, Excelitas Technologies Corp., and Lynred are the top players in the market.

North America held the highest market share in 2025.

By end-use, the healthcare segment is expected to record the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us