Smart Home Appliance Market Size, Share & Industry Analysis, By Type (Kitchen Appliances, Laundry Appliances, Climate Control Appliances, and Others), By Technology (Wi-Fi, ZigBee, Bluetooth, Cellular Technology, and Radio Frequency Identification), By Distribution Channel (OEM D2C Channels, Specialty Stores, Online/E-Commerce, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

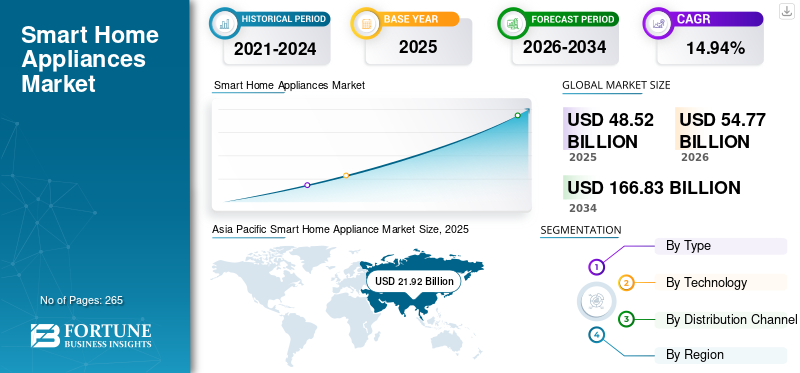

Smart Home Appliance Market Size and Future Outlook

The global smart home appliance market size reached USD 48.52 billion in 2025. It is projected to grow from USD 54.77 billion in 2026 to USD 166.83 billion by 2034, exhibiting a CAGR of 14.94% over the forecast period. Asia Pacific dominated the smart home appliance market with a market share of 45.18% in 2025.

Smart home appliances are everyday household devices that are integrated with the internet via Wi-Fi, Bluetooth, Zigbee, Thread, or cellular. These digital devices allow consumers to monitor, control, and automate them remotely through mobile apps or voice assistants such as Alexa, Google Home, and Apple HomeKit. These devices combine traditional mechanical functions with IoT capabilities, enabling remote operation and scheduling, energy and water usage optimization, predictive maintenance, and integration with smart home technology-based ecosystems. The expansion of 5G infrastructure and broadband connections has made IoT-enabled appliances accessible and popular worldwide, driving demand in smart homes. International Telecommunication Union (ITU) reports ~5.4 billion Internet users in 2024, covering over 66% of the world’s population. GSMA’s Mobile Connectivity Index (2024) exhibits global 4G/5G coverage exceeding 90%, enabling IoT adoption even in emerging markets. Moreover, government bodies and regulatory authorities, including the International Energy Agency (IEA) and U.S. DOE, promote smart, connected energy-efficient appliances to curb energy usage. This regulatory push has increased consumer adoption of smart home appliances.

Key players in the market include LG, Samsung, Haier, Whirlpool, and Bosch. Major strategies adopted by leading companies include integrating AI, IoT, and energy-efficient technologies into their appliance portfolios to enhance connectivity and user convenience. Moreover, these players strive for sustainability, regulatory compliance, and localized production, while emphasizing after-sales service and digital platforms to maintain competitiveness.

Download Free sample to learn more about this report.

SMART HOME APPLIANCE MARKET TRENDS

Integration of Artificial Intelligence (AI) and Voice Assistants in Smart Appliances

The integration of AI-driven features and voice assistant compatibility to enhance personalization and automation is a defining trend in the market. Modern smart connected appliances use machine learning algorithms to analyze user habits, recommend customized settings, and optimize energy usage. For instance, Samsung’s Bespoke AI refrigerators track food freshness and suggest recipes, while LG’s ThinQ AI washers automatically adjust detergent dosage and water levels based on load type.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Growing Smart Ecosystem Integration and Internet Connectivity to Fuel Market Growth

The swift growth of 5G infrastructure and broadband has significantly heightened the adoption of IoT-enabled appliances globally. Key players in the market, including Samsung and LG Electronics, are capitalizing on this opportunity by integrating AI capabilities and Wi-Fi across nearly all product categories through platforms such as SmartThings and ThinQ. These smart home ecosystems allow users to control and monitor appliances remotely and connect them via voice assistants such as Amazon Alexa and Google Assistant. This connectivity trend has made smart household appliances a mainstream category across both developed and developing markets.

Sustainability Initiatives and Energy Efficiency Regulations to Increase Product Adoption

Environmental mandates and government-led energy-efficiency programmes are pushing market players to enhance their products with smart, energy saving features. The IEA cited that connected household appliances can reduce residential energy consumption by 15-20% through real-time monitoring and intelligent scheduling. For instance, Bosch and Whirlpool launched washers and dishwashers that automatically shift operation to off-peak hours to balance energy load, while Midea and Haier promote inverter-driven smart ACs to optimize power use. Such sustainability trends and regulatory measures reduce environmental impact and enhance the appeal of smart appliances, positioning increasing awareness of energy efficiency as a major smart home appliance market growth.

Market Restraints

Limited Affordability and High Product Cost to Restrain Market Growth

The high initial cost of connected household appliances limits their adoption, particularly in price-sensitive regions such as South Africa, Africa, and parts of South America. These connected smart home devices are pricier than their conventional counterparts by 20-40% more, owing to their integration of sensors, connectivity modules, and AI software. For instance, a standard washing machine may cost around USD 350-400 at retail, while a Wi-Fi-enabled version from Samsung SmartThings or LG ThinQ can cost USD 600-700 or more. According to the World Bank, more than 3 billion people still live on less than USD 6.85 per day, creating an affordability barrier. Moreover, the lack of a stable broadband network and after-sales support in developing regions further underscores the need for mass adoption.

Market Opportunities

Expansion of Smart Home Appliances in Emerging Economies to Offer Lucrative Growth Opportunities

Rising urbanization and digital infrastructure development across emerging economies, particularly in the Asia Pacific, South America, and the Middle East, offer numerous growth opportunities for manufacturers. According to the World Bank (2024), urban populations in emerging nations are growing by more than 2% per year, driving demand for energy-efficient and modern household solutions. At the same time, the GSMA Mobile Connectivity Index (2024) reports that 4G and 5G coverage has now reached more than 90% of people in East and Southeast Asia, enabling large-scale IoT adoption. Key players such as LG, Haier, and Midea are capitalizing on this trend by establishing localized production and R&D facilities in Indonesia, India, and Vietnam to offer more affordable smart models. For instance, LG’s regional ThinQ and Haier’s “Made in India” smart washing machines cater specifically to middle-class households.

Market Challenges

Cybersecurity and Data Privacy Concerns Pose a Challenge

The growing risk of data breaches and cybersecurity vulnerabilities in connected smart devices poses a major challenge to market growth. As smart, connected appliances gather data such as schedules, voice controlled commands, and energy usage patterns, they have become easy targets for cyberattacks. According to the International Telecommunication Union (ITU, 2024), more than 30% of global IoT devices remain vulnerable to unauthorized access due to outdated firmware or weak encryption. These privacy challenges and security concerns continue to hamper mass adoption.

SEGMENTATION ANALYSIS

By Type

Widespread Adoption of Air Conditioning and Energy-Efficiency Demand Drives Climate Control Appliances Segment Growth

Based on type, the market is segmented into kitchen appliances, laundry appliances, climate control appliances, and others.The climate control appliances segment held the largest market share in 2025. Air conditioning (AC) and HVAC systems account for the highest share of household energy use globally, making them the primary emphasis for energy-efficient and smart upgrades. According to the IEA, residential space cooling demand has tripled since 1990. It continues to rise sharply, especially in Asia Pacific, which alone accounts for over 60% of global air conditioner stock growth.

The laundry appliances segment is expected to grow at the fastest CAGR during the forecast period. The segment’s growth is driven by the increasing adoption of IoT and AI capabilities in washing machines and dryers, enabling energy optimization, real-time monitoring, and remote operation. Moreover, shorter replacement cycles and government-backed energy-efficiency incentives are accelerating consumer adoption of smart, grid-responsive laundry systems.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Broad Consumer Router Adoption and High Data Capacity to Spur Wi-Fi Segment Growth

Based on technology, the market is segmented into Wi-Fi, ZigBee, Bluetooth, cellular technology, and radio frequency identification.

The Wi-Fi segment accounted for the majority of the smart home appliance market share. This dominance is driven by stable home internet penetration, high bandwidth, and compatibility with major ecosystems such as Google Home, Alexa, and Samsung SmartThings. According to the Wi-Fi Alliance, in 2024, over 200 billion Wi-Fi devices were in active use globally, indicating their widespread use in residential spaces. Moreover, Wi-Fi’s cloud integration and superior range make it a strong pillar of smart home connectivity, which explains its continued dominance in market share.

The ZigBee segment is projected to grow at the fastest CAGR over the forecast period. Its low power usage, integration with Matter, and strong mesh networking make it the fastest-expanding protocol in multi-device ecosystems. Supported by SmartThings, Bosch Home Connect, and Haier hOn, ZigBee enables reliable inter-appliance communication without relying solely on Wi Fi bandwidth.

By Distribution Channel

Hands-on Demos, Expert Guidance, and Installation Support Drive Specialty Stores Segment Growth

Based on distribution channel, the market is segmented into OEM D2C channels, specialty stores, online/e-commerce, and others.

The specialty stores segment accounted for the largest market share in 2025. These stores remain the primary retail channel for large, installation-dependent appliances, including washing machines, refrigerators, and air conditioners. Specialty stores such as Croma, MediaMarkt, Best Buy, and LG brand shops offer hands-on demonstrations, in-person guidance, financing options, and installation services. These are key parameters in consumer purchasing decisions when making high-value purchases.

The online/e-commerce segment is anticipated to expand at the highest CAGR over the forecast period. Growing consumer trust in online shopping and accelerated post-COVID digital adoption have accelerated the growth of e-commerce platforms such as BestBuy.com, Flipkart, Amazon, and JD.com, which now account for about one-third of global appliance sales. Moreover, the expansion of direct brand-owned webstores and online-to-offline fulfillment models is driving the segment's growth.

Smart Home Appliance Market Regional Outlook

Regionally, the market is divided into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

Asia Pacific

Asia Pacific Smart Home Appliance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market held the dominant share in 2025, valued at USD 21.92 billion, and is expected to maintain its leading position in 2026, with a value of USD 25.03 billion. The region's growth is attributed to rapid urbanization, rising disposable incomes, and expanding digital infrastructure. The area benefits from the presence of prominent manufacturers, including Haier, LG, and Midea, which also have localized production and R&D facilities in countries with low labor costs, such as India and Vietnam. Furthermore, government initiatives, including India’s Digital India Program and China’s “Smart Home 2025” policy, further trigger consumer awareness and adoption rates.

Japan Smart Home Appliance Market

The Japanese market in 2025 was valued at USD 1.81 billion, accounting for roughly 3.73% of global product revenues. Expansion of OTT and streaming platforms support the demand for smart homes products.

China Smart Home Appliance Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 7.19 billion, representing roughly 14.81% of global product sales.

India Smart Home Appliance Market

The Indian market in 2025 was valued at USD 6.80 billion, accounting for roughly 14.02% of the global market revenues.

North Americ

The North America region reached a valuation of USD 12.90 billion in 2025. The region’s growth is fueled by high consumer adoption of advanced and smart technologies, strong broadband infrastructure, and increasing demand for energy-saving, connected household solutions.

U.S. Smart Home Appliance Market

The U.S. market size reached USD 11.27 billion in 2025. The U.S. market accounted for around 23.22% of the global market sales.

Europe

The European market reached USD 9.84 billion in 2025, securing its position as the third-largest region. European market growth is attributed to widespread broadband connectivity and strong government mandates for energy efficiency. In addition, a highly eco-conscious consumer base and sustainability-centric consumer behavior supplement demand for energy-optimized and connected products.

U.K. Smart Home Appliance Market

The U.K. market in 2025 was valued at USD 1.16 billion, representing approximately 2.39% of global product revenues.

Germany Smart Home Appliance Market

Germany’s market is reached approximately USD 1.74 billion in 2025, equivalent to around 3.58% of global product sales.

South America and the Middle East & Africa

Over the forecast period, the South America, Middle East & Africa regions would witness significant growth, following the Asia Pacific. The South America market in 2025 reached the valuation of USD 2.00 billion. The increasing adoption of smart city initiatives, growing urbanization, and the rising need for energy-efficient cooling and connected living solutions are likely to drive South America’s market growth. The Middle East & Africa are experiencing steady growth, driven by increasing urbanization and expanding internet penetration, especially in Saudi Arabia and the UAE.

UAE Smart Home Appliance Market

The UAE market reached approximately USD 0.49 billion in 2025, accounting for roughly 1.01% of the global market revenues.

Competitive Landscape

Key Industry Players

Innovative Features and Aesthetic Design Drive Demand, Compelling Brands to Evolve Market Strategies

The market landscape is highly dynamic, with players competing on product innovation, ecosystem integration, energy-saving features, and consumer experience. Companies are also investing heavily in cloud-based platforms, AI, and IoT to improve product interoperability and intelligence. Many key players, such as Samsung, LG, and Bosch, are strengthening their smart ecosystems through SmartThings, ThinQ, and Home Connect, respectively, to enable multi-device connectivity. Furthermore, expanding D2C channels, localizing production hubs to curb manufacturing costs, and emphasizing sustainability through eco-friendly, energy-efficient designs in compliance with global standards.

LIST OF KEY SMART HOME APPLIANCE COMPANIES PROFILED

- LG Electronics Inc. (South Korea)

- Samsung Electronics Co., Ltd. (South Korea)

- Haier Smart Home Co., Ltd. (China)

- Midea Group Co., Ltd (China)

- Whirlpool Corporation (U.S.)

- Daikin Industries, Ltd. (Japan)

- GE Appliances (U.S.)

- BSH Hausgeräte GmbH (Germany)

- Electrolux AB (Sweden)

- Panasonic Holdings Corporation (Japan)

Key Industry Developments

- September 2025: LG Electronics introduced an upgraded ThinQ AI Platform designed to extend the functionality, longevity, and user convenience of its smart home appliances. The platform enables users to upgrade appliance features, perform predictive maintenance, and receive tailored energy-saving recommendations through the LG ThinQ app.

- June 2025: Xiaomi introduced the Mijia Air Conditioner Pro Eco Inverter, expanding its lineup of intelligent climate control appliances within the Mi Home ecosystem. The new model features a high-efficiency inverter compressor, smart temperature regulation, and AI-driven energy optimization, allowing users to monitor and control cooling performance remotely via the Mi Home app.

- June 2025: BSH Hausgeräte GmbH inaugurated a new manufacturing facility in Egypt, marking a significant milestone in the company’s strategic expansion across Africa and the Middle East. The plant will focus on producing high-quality, energy-efficient home appliances to meet rising regional demand and strengthen BSH’s local market presence. This investment aligns with the company’s long-term vision to establish Egypt as a central production and export hub for Africa, supporting both domestic consumption and international distribution.

- March 2025: Samsung Electronics introduced its new Bespoke AI appliance series, featuring seamless integration with the company’s SmartThings ecosystem to deliver a more intelligent and energy-efficient home experience. The product lineup includes AI powered refrigerators, washing machines, ovens, and air conditioners equipped with advanced sensors and AI and machine learning capabilities for personalized operation.

- January 2025: Bosch announced the expansion of its Home Connect ecosystem, emphasizing enhanced interoperability, energy-efficient appliance solutions, and integration with artificial intelligence. The initiative includes new dishwashers, smart ovens, and laundry systems designed to work seamlessly with Home Connect Plus and third-party platforms, including the Matter and Amazon Alexa connectivity standards.

- September 2024: Midea Group offers a wide range of smart products. The company accelerated its global expansion strategy by enhancing its international manufacturing and R&D network to better serve diverse consumer needs. Midea Group is actively investing in AIoT-driven product innovation and establishing new research and development centers across Asia, Europe, and the Middle East to advance its smart home ecosystem. This initiative supports Midea’s long-term vision to become a leading global provider of intelligent, energy-efficient home solutions, delivering technologically advanced, sustainable appliances to consumers worldwide.

- April 2022: Xiaomi announced the launch of its Redmi Smart TV A58 (2022), strengthening its position in the connected home entertainment segment. The new 58-inch model features a 4K ultra-high-definition display, narrow-bezel design, and integration with Xiaomi’s PatchWall interface and Mi Home ecosystem, enabling seamless connectivity with other smart devices.

REPORT COVERAGE

The smart home appliance market report provides a detailed analysis of the market and focuses on key aspects, including the competitive landscape, services, leading product types, and other key market segments. It also offers global market trends and insights, highlighting key industry developments. In addition to the aforementioned factors, the report on the market outlook includes several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.94% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Technology

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the market size was USD 48.52 billion in 2025 and is anticipated to reach USD 166.83 billion by 2034.

In 2025, the global market stood at USD 48.52 billion.

The market will grow at a CAGR of 14.94% and exhibit a significant growth rate during the forecast period.

By type, the climate control appliance segment dominated the market in 2025.

Growing smart ecosystem integration and internet connectivity along with rising internet penetration and expanding digital infrastructure are the key factors driving the market.

LG, Samsung, Haier, Whirlpool, and Bosch are among the few significant players in the global market.

Asia Pacific held the highest market share in 2025.

Sustainability initiatives and energy efficiency regulations compelled by government authoritative bodies to likely drive the product adoption amongst consumers.

- 2021-2034

- 2025

- 2021-2024

- 265

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us