Collision Avoidance System Market Size, Share & Industry Analysis, By End-use Industry (Automotive, Aviation, Industrial, Warehousing and Logistics, and Marine), By Sensor Type (Radar, Camera, LiDAR, Ultrasonic, GNSS / V2X modules, and Infrared / Thermal sensors), By Function (Collision Warning Systems, Automatic Emergency Braking (AEB), Blind-Spot &, Surround Monitoring, Obstacle Detection for Autonomous Navigation, and Proximity & Safe-Distance Monitoring), By Technology (Radar Systems, Camera-Based Vision Systems, LiDAR Systems, & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

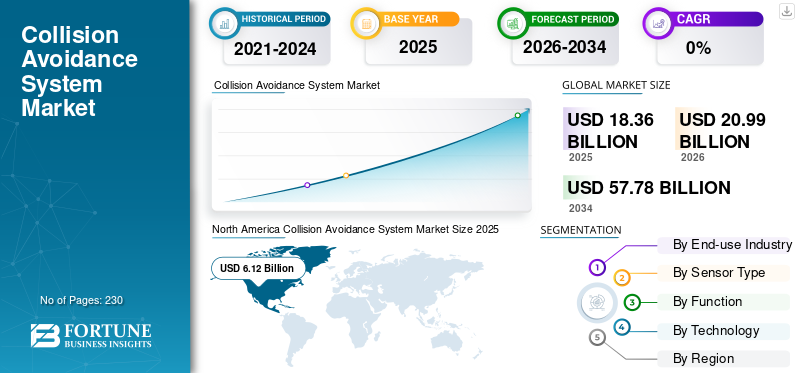

The global collision avoidance system market size was valued at USD 18.36 billion in 2025. The market is projected to grow from USD 20.99 billion in 2026 to USD 57.78 billion by 2034, exhibiting a CAGR of 13.49% during the forecast period. North America dominated the global collision avoidance system market with a market share of 33.33% in 2025.

The collision avoidance system includes the technologies that help vehicles, aircraft, industrial machines, and autonomous equipment detect obstacles and prevent accidents. These systems use radar, cameras, LiDAR, ultrasonic sensors, and software that interprets surroundings and supports quick decision-making.

The market is growing because governments are strengthening safety regulations, industries are increasing their use of automation, and companies want to reduce accidents, downtime, and insurance exposure. Automotive manufacturers are integrating these systems as standard features, and warehouses, mining operations, and logistics facilities are adopting advanced detection systems for autonomous robots and heavy equipment. Improvements in artificial intelligence, sensor accuracy, and processing capability are also making these systems more reliable and easier to deploy.

Leading companies include Bosch, Continental, ZF, Mobileye, Aptiv, Honeywell, Garmin, Collins Aerospace, Hexagon AB, and Trimble. As industries shift toward connected and automated operations, collision avoidance becomes a core safety feature and technology in productivity.

Download Free sample to learn more about this report.

COLLISION AVOIDANCE SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 18.36 billion

- 2026 Market Size: USD 20.99 billion

- 2034 Forecast Market Size: USD 57.78 billion

- CAGR: 13.49% from 2026–2034

- North America dominated the collision avoidance system market with a 33.33% share in 2025.

- Radar was the leading sensor type segment due to its reliable all-weather detection and widespread adoption.

- Collision warning systems accounted for the largest market share among application segments in 2025.

North America

North America led the market with USD 6.12 billion in 2025, supported by strong automotive and industrial demand.

Europe

Europe maintained a significant market share, driven by strict vehicle safety regulations and ADAS adoption.

Asia Pacific

Asia Pacific was the fastest-growing region due to expanding automotive production and industrial automation.

U.S.

The U.S. remained the largest regional contributor, benefiting from high adoption of AEB and autonomous vehicle technologies.

Japan

Japan remained a key market in Asia Pacific, supported by advanced driver-assistance systems and smart mobility investments.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Regulatory Push Toward Zero-Accident Mobility and Autonomous Safety to Drive Market Growth

The key driver for the collision avoidance system industry is the strong global regulatory shift toward reducing road, air, and industrial accidents. Governments are mandating higher safety standards, such as automatic emergency brakes, intelligent mobility guidelines, UAV detect-and-avoid requirements, and safety protocols in mining and warehouse automation. This regulatory pressure is forcing OEMs, fleet operators, and industrial facilities to integrate collision-avoidance layers into both new platforms and retrofit programs. Automotive manufacturers are standardizing radar and camera fusion across vehicle segments, while drones, robots, and heavy equipment rely on multi-sensor systems for uninterrupted operations. Insurance incentives, electrification, urban mobility growth, and corporate safety KPIs further accelerate adoption. As industries embrace automation and connected operations, CAS becomes a foundational safety infrastructure, creating sustained long-term demand.

- In October 2024, the U.S. NHTSA finalized new rules requiring automatic emergency braking on all new passenger vehicles, confirming a major regulatory shift toward mandatory active safety systems.

MARKET RESTRAINTS

High System Costs, Integration Complexity, and Calibration Challenges to Act as a Restraint on Market Growth

A major restraint for the collision avoidance system market growth is the overall cost and engineering complexity of integrating multiple sensors, processing units, and software layers into a single reliable safety system. Radar, LiDAR, thermal cameras, and sensor-fusion processors require precise calibration, environmental robustness, and high-quality components that increase development and manufacturing costs. For industrial and off-highway vehicles, vibrations, dust, lighting variation, and harsh operating conditions complicate sensor performance, forcing companies to invest in ruggedized hardware and complex integration frameworks. Smaller manufacturers face additional challenges in meeting functional safety certifications, cybersecurity requirements, and interoperability standards. In emerging markets, cost sensitivity further slows adoption, especially for non-mandatory safety features. As a result, system affordability and integration time remain key barriers despite strong regulatory support.

- In Jun 2024, an Asian automotive OEM delayed the rollout of its mid-range LiDAR CAS module due to calibration issues and higher-than-expected production costs.

MARKET OPPORTUNITIES

Rapid Growth in Autonomous Systems, Robotics, and Industrial Automation Posing as a Major Market Opportunity

A significant opportunity for the market comes from rapid advancements in autonomous mobility, robotics, and industrial automation. Warehouses, mines, ports, and manufacturing plants are adopting autonomous mobile robots, driverless forklifts, drones, and automated haul-truck fleets that require high-precision, multi-sensor collision-avoidance systems for safe operation. As industries digitize their workflows and focus on reducing downtime and operational risks, demand for 360-degree perception, real-time monitoring, and predictive safety capabilities continues to rise. The shift toward safety-as-a-service, cloud-connected operations, and OTA upgrades also creates new recurring revenue streams for CAS suppliers. Governments and enterprises are investing in autonomous logistics, smart infrastructure, and drone corridors, further accelerating demand for scalable detection and avoidance systems across sectors.

- In February 2025, Volvo Autonomous Solutions deployed CAS-enabled autonomous haul trucks with Boliden, targeting improved safety and reduced collision-related downtime in mining operations.

MARKET CHALLENGES

Reliability in Harsh Environments and Extended Certification Cycles Present Threats for Market Growth

A persistent challenge for the market is ensuring reliable performance across real-world operating environments such as poor weather, dust, cluttered industrial layouts, and complex traffic patterns. Sensors must maintain accuracy despite rain, glare, fog, extreme temperatures, and electromagnetic interference, which require sophisticated filtering, redundancy, and ruggedization. For aviation, drones, and autonomous vehicles, achieving certification from regulators involves extensive testing, validation, and safety case documentation, often extending launch timelines and increasing development costs. Cross-border regulatory inconsistencies further complicate deployment for global OEMs. Industrial operators also struggle with maintaining calibration, cleaning sensors, and preventing downtime caused by environmental degradation. These issues limit adoption for some high-risk or outdoor applications.

COLLISION AVOIDANCE SYSTEM MARKET TRENDS

AI-Driven Sensor Fusion and Predictive Perception Systems Pose as a Technological Trend

The technological landscape of collision avoidance systems is transitioning from basic sensor-based alerts to advanced AI-driven perception platforms capable of understanding complex environments. Next-generation systems integrate radar, LiDAR, cameras, GNSS, and V2X inputs into unified sensor-fusion engines supported by machine-learning models that classify objects, predict movement trajectories, and make real-time decisions. Enhanced safety edge-processing power and automotive-grade neural processors enable faster and more accurate hazard detection. In industrial and robotics environments, 3D LiDAR technology mapping, SLAM algorithms, and autonomous navigation systems are accelerating adoption. Meanwhile, connected CAS platforms allow remote diagnostics, continuous learning, and OTA improvements. These advancements collectively improve accuracy, reliability, and performance across automotive, industrial, UAV, and marine applications.

- In September 2024, Mobileye announced an upgraded perception stack powered by its EyeQ6 platform, enhancing Radar-LiDAR fusion accuracy and predictive collision-avoidance capabilities.

Download Free sample to learn more about this report.

Segmentation Analysis

By Sensor Type

Radar Segment is Holds the Largest Share Due to Its Reliability and Cost Efficiency

Based on sensor type, the market is classified into radar, camera, LiDAR, ultrasonic, GNSS / V2X modules, and infrared / thermal sensors.

Radar remains the largest sensor type because it offers reliable object detection in all weather conditions at a competitive cost. Automotive manufacturers deploy radar across majority of vehicle classes as part of ADAS suites, and industrial fleets also use ruggedized radar for operations in dust, rain, and low visibility. Radar’s performance in long-range detection, mature supply chain, and strong regulatory push for AEB systems strengthens its leading position. Radar’s scalability also supports large-volume automotive platforms, giving it higher penetration than LiDAR or camera-only systems.

The GNSS / V2X modules segment is expected to grow at a higher CAGR of 13.45% in the forthcoming years.

By Function

Collision Warning Systems Segment to Take the Primary Position Due To their Widespread Adoption

In terms of function, the market is categorized into collision warning systems, Automatic Emergency Braking (AEB), blind-spot & surround monitoring, obstacle detection for autonomous navigation, and proximity & safe-distance monitoring.

Collision warning systems account for the largest segment because they form the foundational layer of active safety across automotive, industrial, and UAV platforms. Most regulatory frameworks require baseline forward-collision alert and warning features even before advanced automatic braking and autonomy functions. Their relatively lower integration cost and compatibility with radar-camera architectures enable deployment on mass-market vehicles and commercial equipment. Industrial and warehouse operators also rely heavily on warning systems to reduce incident rates and protect workers around mobile machinery.

The obstacle detection for the autonomous navigation segment accounted for a significant market share in the global market and is expected to grow at the highest CAGR of 14.68% from 2026-2034.

To know how our report can help streamline your business, Speak to Analyst

By End-use Industry

Automotive Segment Takes the Leading Position due to Mandatory Safety Integration

Based on end-use industry, the market is segmented into automotive, aviation, industrial, warehousing and logistics, and marine.

Automotive is the largest end-use segment due to global mandates for active safety systems and OEM standardization of ADAS components. Mass production volumes, platform-wide adoption, and government rules requiring AEB and collision-warning capabilities accelerate radar and camera integration across vehicle classes. The rise of electrification and connected vehicles further increases CAS demand as automakers shift toward centralized safety architectures. High penetration in developed markets and increasing adoption in emerging economies give automotive the strongest overall volume and revenue contribution.

The warehousing and logistics segment accounted for a significant market share in the global market and is expected to grow at the highest CAGR of 14.6% from 2026-2034.

By Technology

OEMs Rely on Radar Systems as They Provide Better Features, Boosting the Demand for Radar Systems

Based on technology, the market is segmented into radar systems, camera-based vision systems, LiDAR systems, ultrasonic sensors, AI perception and sensor fusion software, and V2X / connectivity modules.

Radar systems forms the largest technology category because they balance cost, performance, and environmental robustness better than other sensing technologies. Automotive OEMs rely on radar for highway, urban, and parking assistance safety functions, while industrial operators depend on radar for operations in dust, fog, and low-light environments. Radar’s long-range capability and stable signal performance make it a default component in both basic and advanced CAS architectures. Its maturity and ease of integration ensure continued dominance despite the rapid growth of LiDAR and AI perception software.

The AI perception and sensor fusion software segment accounted for a significant market share in the global market and is expected to grow at the highest CAGR of 14.55% from 2026-2034.

Collision Avoidance System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America held the dominant collision avoidance system market share in 2024, valued at USD 5.30 billion, and also took the leading share in 2025 with USD 6.12 billion. North America leads the CAS market due to strong regulatory momentum, large automotive production volumes, and high adoption of industrial automation. The U.S. benefits from early integration of AEB, advanced perception systems, and commercial fleet safety technologies. Industrial sectors such as mining, warehousing, and logistics also drive significant demand for collision avoidance retrofits and autonomous equipment. The region’s technology ecosystem and investment in autonomous testing accelerate CAS innovation and deployment across industries.

- In January 2025, Garmin released upgraded collision-avoidance features for general aviation aircraft in North America to improve operational safety.

North America Collision Avoidance System Market Size 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

Europe maintains a strong market share is driven by some of the world’s most stringent safety standards, including GSR-II and Euro NCAP 2030 protocols. These standards accelerate CAS integration across vehicles and support adoption in industrial and UAV applications. European OEMs and Tier-1 suppliers also lead in radar, camera, and software innovation, further reinforcing market maturity. Broad adoption across automotive, aviation, and manufacturing makes Europe highly stable with consistent year-on-year growth.

Asia Pacific

Asia Pacific is the fastest-growing region due to the rapid expansion of automotive manufacturing, warehouse automation, robotics, and UAV operations. China, Japan, and South Korea lead in advanced driver-assistance technology, while India increases safety mandates for new vehicles. The region’s industrial sectors adopt CAS-enabled robots, forklifts, and mining equipment to improve safety and operational efficiency. Strong government focus on smart mobility and intelligent manufacturing reinforces this growth trend.

Rest of the World

The Rest of the World region grows steadily due to rising adoption in mining, oil and gas, security fleets, and commercial vehicle applications across Latin America, Africa, and the Middle East. Latin America, the Middle East, and Africa collectively represent the smallest regional block by value, yet remain significant in the market. Limited passenger vehicle regulation slows large-scale CAS penetration, but industrial sectors adopt CAS aggressively to reduce collisions in high-risk environments. Port operations, heavy mining fleets, and security vehicles represent core demand areas, supported by modernization investments.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings and Strong Distribution Network of Key Companies, Supported their Leading Positions

A mix of automotive Tier-1 suppliers, aviation safety specialists, and industrial automation companies shapes the market. In automotive, Bosch, Continental, ZF, Mobileye, and Aptiv lead the market with strong radar, camera, and sensor-fusion portfolios that are integrated across global vehicle platforms. Aviation and UAV safety is driven by companies such as Honeywell, Garmin, and Collins Aerospace, which supply certified detect-and-avoid solutions for aircraft and advanced drones. Industrial and mining applications rely heavily on Hexagon AB and Trimble for high-precision perception systems used in construction, logistics, and heavy-equipment fleets. Competition is steadily shifting from hardware to software, with AI perception, autonomous navigation support, and connected safety analytics becoming key differentiators. Companies that offer scalable sensor fusion and safety-certified software gain an advantage as industries move toward higher automation.

LIST OF KEY COLLISION AVOIDANCE SYSTEM COMPANIES PROFILED:

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Mobileye Global Inc. (Israel)

- Aptiv PLC (Ireland)

- Honeywell International Inc. (U.S.)

- Garmin Ltd. (U.S.)

- Collins Aerospace (Raytheon Technologies) (U.S.)

- Hexagon AB (Sweden)

- Trimble Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2025- Volvo Autonomous Solutions partnered with Boliden on a USD 65 million project to deploy autonomous haul trucks equipped with 360-degree collision-avoidance systems in mining operations. The deployment aims to reduce incidents and improve productivity in demanding industrial environments.

- January 2025 – Garmin released an enhanced GTS traffic-collision avoidance update with more accurate ADS-B-assisted detection. The upgrade improves pilot situational awareness and strengthens Garmin’s position in general aviation safety systems. No contract value has been reported.

- September 2024 – Mobileye launched the EyeQ6 platform, featuring improved Radar-LiDAR fusion and trajectory prediction for advanced assisted-driving systems. The upgrade supports OEM compliance with next-generation safety standards and strengthens Mobileye’s position in premium ADAS deployments. No contract value disclosed.

- November 2024 – Continental signed a USD 210 million contract with a leading Asian EV producer to deliver radar and camera-based collision-avoidance systems for 2025–2028 models. The contract expands Continental’s presence in the fast-growing APAC EV market.

- June 2024 – Hexagon AB acquired an AI-driven industrial safety software provider to enhance its collision-avoidance offerings for mining and construction fleets. The USD 95 million acquisition will integrate predictive analytics with Hexagon’s sensor ecosystem, expanding its heavy-equipment safety footprint.

- March 2024 – Bosch partnered with a major European automaker to supply long-range radar modules for new ADAS platforms. The USD 180 million deal aims to enhance AEB performance and improve highway safety functions. The partnership accelerates radar adoption across mid-segment vehicle lines.

- January 2024 – Honeywell launched a next-generation UAV collision-avoidance suite integrating radar and vision fusion to support safer BVLOS operations. The upgrade aims to help drone operators meet tightening aviation safety requirements. The launch strengthens Honeywell’s position in advanced UAV safety systems. No contract value disclosed.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.49% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By End-use Industry, Sensor Type, Function, Technology, and Region |

|

By End Use Industry |

· Automotive · Aviation · Industrial · Warehousing and Logistics · Marine |

|

By Sensor Type |

· Radar · Camera · LiDAR · Ultrasonic · GNSS / V2X modules · Infrared / Thermal sensors |

|

By Function |

· Collision Warning Systems · Automatic Emergency Braking (AEB) · Blind-Spot & Surround Monitoring · Obstacle Detection for Autonomous Navigation · Proximity & Safe-Distance Monitoring |

|

By Technology |

· Radar Systems · Camera-Based Vision Systems · LiDAR Systems · Ultrasonic Sensors · AI Perception and Sensor Fusion Software · V2X / Connectivity Modules |

|

By Geography |

· North America (By End-use Industry, Sensor Type, Function, Technology, and Country) o U.S. (By End-use Industry) o Canada (By End-use Industry) · Europe (By End-use Industry, Sensor Type, Function, Technology, and Country) o U.K. (By End-use Industry) o Germany (By End-use Industry) o France (By End-use Industry) o Russia (By End-use Industry) o Rest of Europe (By End-use Industry) · Asia Pacific (By End-use Industry, Sensor Type, Function, Technology, and Country) o China (By End-use Industry) o India (By End-use Industry) o Japan (By End-use Industry) o Australia (By End-use Industry) o Rest of Asia Pacific (By End-use Industry) · Rest of the World (By End-use Industry, Sensor Type, Function, Technology, and Country) o Latin America (By End-use Industry) o Middle East & Africa (By End-use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 18.36 billion in 2025 and is projected to reach USD 57.78 billion by 2034.

In 2025, the market value stood at USD 6.12 billion.

The market is expected to exhibit a CAGR of 13.49% during the forecast period.

The automotive segment led the market in terms of end-use industry.

Regulatory push toward zero-accident mobility and autonomous safety to drive market growth.

Robert Bosch GmbH (Germany), Continental AG (Germany), and ZF Friedrichshafen AG (Germany) are prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us