Conductive Polymers Market Size, Share & Industry Analysis, By Type (Electrically Conductive and Thermally Conductive), By Application (ESD/EMI Shielding, Antistatic Packaging, Electrostatic Coating, Capacitor, and Others), and Regional Forecast, 2026-2034

Conductive Polymers Market Overview

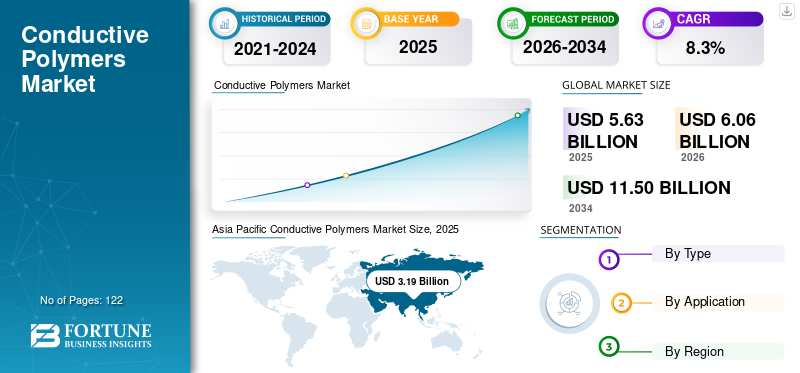

The global conductive polymers market size was valued at USD 5.63 billion in 2025. The market is projected to grow from USD 6.06 billion in 2026 to USD 11.50 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period. Asia Pacific dominated the conductive polymers market with a market share of 56.66% in 2025.

Conductive polymers are application-driven materials that sit at the intersection of electronics manufacturing, electrostatic protection, and thermal management. These polymers are used not simply as material upgrades, but as functional enablers in systems that require static charge control, shielding integrity, stable capacitor performance, or heat dissipation reliability. In modern electronics supply chains, conductive polymer demand is structural as ESD-safe handling and packaging are required for organizations that manufacture, assemble, test, transport, or otherwise handle electronic parts and assemblies.

Demand intensity increases with higher specification requirements: tighter EMI/ESD performance, longer-life polymer capacitors (low ESR, high ripple current), and thermally conductive polymer compounds used in compact high-power electronic devices and electrified systems. Global value growth is therefore influenced as much by specification intensity and material performance as by underlying unit volumes of electronics.

Key players operating in the market include Heraeus Group, Agfa-Gevaert NV, SABIC, Covestro, and BASF.

Download Free sample to learn more about this report.

Conductive Polymers Market Takeaways

- 2025 Market Size: USD 5.63 billion

- 2026 Market Size: USD 6.06 billion

- 2034 Forecast Market Size: USD 11.50 billion

- CAGR: 8.3% from 2026–2034

- Asia Pacific dominated the conductive polymers market with a 56.66% share in 2025.

- The Electrically Conductive segment held the largest market share in 2025.

- The ESD/EMI Shielding application segment dominated the market in 2025.

North America

North America is supported by investments in data centers, advanced computing, aerospace, defense, and medical electronics, boosting demand for high-performance conductive polymers.

Europe

Europe's market is driven by high-compliance automotive electronics, industrial manufacturing, and increasing demand for thermal management materials in electrified systems.

Asia Pacific

Asia Pacific led the market with USD 3.19 billion in 2025, driven by the strong presence of electronics and semiconductor manufacturing industries.

U.S.

The U.S. market reached USD 1.02 billion in 2025, accounting for approximately 18.1% of global sales, supported by robust demand from the electronics sector.

Japan

Japan's market is supported by its advanced electronics manufacturing industry and increasing adoption of conductive polymers in high-performance electronic components and automotive applications.

Read More

CONDUCTIVE POLYMERS MARKET TRENDS

Performance-Driven Electrification and High-Density Electronics are Key Market Trends

Conductive polymers are increasingly pulled by electronics architectures that demand lower losses, stable electrical behavior, and thermal control at higher power density. On the electrical side, conductive polymer capacitors are designed for low ESR and ripple performance, with manufacturers emphasizing longer life and durability, valued in high-load electronic environments.

In parallel, thermally conductive polymer compounds are expanding as engineered plastics replace metals or ceramic-heavy assemblies in heat spreading and enclosure components. Suppliers highlight suitability for LED fixtures, consumer electronics, aerospace and automotive cooling systems, and motor/battery housings, reflecting a broader trend toward integrated thermal management in compact systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

ESD/EMI Compliance Across Electronics Handling Drives Market Growth

ESD protective packaging is intended to protect ESDS items throughout production, rework/maintenance, transport, and storage, supporting structurally recurring demand for antistatic and shielding packaging formats. As electronics output expands (and as high-value components become more sensitive), the frequency and intensity of ESD packaging and shielding requirements rise, supporting consistent baseline consumption. This also reinforces the scale of the ESD/EMI shielding and antistatic packaging segments in the market. This is expected to boost the conductive polymers market growth in the coming years.

MARKET RESTRAINTS

Cost, Formulation Sensitivity, and Qualification Burden Limit Substitution in Cost-Driven Builds

Conductive polymers are functional materials; many end-uses require qualification, process stability, and consistent electrical/thermal behavior. That raises switching costs and slows rapid penetration into highly cost-optimized products. In practice, performance tuning often depends on formulation, dispersion quality, coating/printing compatibility, and long-term stability under humidity/temperature conditions, which can increase development cycles and supplier dependency.

For thermally conductive polymer compounds, value growth can be constrained by the need to meet performance targets while maintaining moldability, mechanical integrity, and safety compliance (e.g., flame-retardant requirements). RTP’s portfolio shows multiple resin systems and performance classes, highlighting how application-specific and qualification-heavy these compounds can be.

MARKET OPPORTUNITIES

Printed/Flexible Electronics and Functional Coatings Create a Higher-Value Path Beyond Bulk ESD Materials

Conductive polymers enable coating- and printing-based electronics and functional layers, an opportunity that extends beyond conventional packaging and shielding. Heraeus (Clevios PEDOT/PSS) explicitly points to printed electronics, conductive protective/shielding layers, flexible displays, and electrolytic capacitors as application areas, reflecting a portfolio direction toward higher value-added functional layers rather than commodity conductive fillers alone.

MARKET CHALLENGES

Meeting Tight ESD/EMI and Thermal Performance Windows Raises Execution and Reliability Risk

As ESD/EMI performance and thermal management requirements become more stringent, conductive polymers must deliver consistent resistivity/conductivity and stable behavior over time. The challenge material design, manufacturing repeatability, film thickness, dispersion uniformity, coating defects, and environmental aging can cause drift in electrical performance.

This challenge is amplified for multi-functional parts (e.g., enclosures or housings that must provide thermal management plus ESD behavior).

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions are raising costs and disrupting supply chains in the market, primarily through tariffs on raw materials and chemicals. These factors have trimmed growth forecasts and prompted supply chain diversification, though the Asia Pacific region remains dominant due to electronics production.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Supplier-facing application literature on PEDOT/PSS emphasizes broad functionality across capacitors, shielding/protective layers, and printed electronics, which aligns with industry R&D moving toward multi-property conductive layers and scalable manufacturing methods (coating/printing).

On the thermal side, commercially available compound families span resin types and performance classes, indicating ongoing development around formulation pathways tailored to electronics, lighting, automotive, and battery systems.

SEGMENTATION ANALYSIS

By Type

Electrically Conductive Segment Dominates Due to ESD/EMI Compliance and Capacitor Pull

Based on type, the global market is segmented into electrically conductive and thermally conductive.

The electrically conductive segment holds the dominant conductive polymers market share. The growth is primarily due to ESD/EMI shielding, antistatic packaging, and polymer capacitor materials, which are directly tied to electronics handling standards and high-reliability component demand. IEC standards reinforce the breadth of ESD-relevant activities (from manufacture through transport), structurally supporting demand for electrically conductive materials.

The thermally conductive segment is expected to rise at a 6.2% CAGR during the forecast period. Thermally conductive polymer compounds are growing in response to thermal management needs in LED lighting, consumer electronics, aerospace/automotive cooling, and motor/battery housings, where polymer solutions can reduce weight and enable integrated part designs.

By Application

To know how our report can help streamline your business, Speak to Analyst

ESD/EMI Shielding Dominates Due to Mandatory Control Environments and Shielding Layer Adoption

Based on application, the market is segmented into ESD/EMI shielding, antistatic packaging, electrostatic coating, capacitor, and others.

ESD/EMI shielding represents the dominant application segment. The growth is due to the embedding of shielding materials and conductive protective layers in electronics manufacturing environments and product designs. PEDOT/PSS suppliers explicitly cite conductive protective and shielding layers as key use-cases.

The antistatic packaging segment is predicted to grow at a 8.1% CAGR during the forecast period. Antistatic packaging is a large, recurring demand stream across electronics logistics. Packaging intended for ESDS protection is governed by defined property requirements across production, transport, and storage, supporting a large recurring demand base for antistatic and shielding packaging materials.

Polymer capacitors rely on conductive polymer technology to deliver performance attributes such as low ESR and ripple capability, supporting sustained demand in performance electronics. The segment is anticipated to experience notable growth during the forecast period.

CONDUCTIVE POLYMERS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Conductive Polymers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading market share in 2025. The demand stems from the concentration of electronics and semiconductor manufacturing, which scales and therefore has the highest pull for ESD/EMI shielding materials, antistatic packaging, and capacitor supply chains.

China Conductive Polymers Market

China’s market is one of the largest globally, with 2025 revenue at USD 1.40 Billion, representing roughly 24.8% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America demand is supported by data-center and advanced computing investments, plus high-specification intensity in aerospace/defense, medical electronics, and high-reliability industrial systems, which drive higher-value conductive polymer usage per unit output.

U.S. Conductive Polymers Market

In 2025, the U.S. represented a USD 1.02 Billion market in North America, driven primarily by strong conductive polymer demand from the electronics sector. The U.S. accounted for roughly 18.1% of global sales.

Europe

Europe’s demand is value-weighted toward high-compliance industrial electronics, automotive electronics, and advanced manufacturing, where materials qualification and performance stability matter. Thermal management compounds also see pull in electrified systems and engineered components.

Germany Conductive Polymers Market

The Germany market in 2025 was at USD 0.25 billion, representing roughly 4.4% of global revenues.

U.K. Conductive Polymers Market

The U.K. market in 2025 was at around USD 0.22 billion, representing roughly 3.9% of global revenues.

Latin America

Latin America remains a smaller share but grows with electronics assembly footprints, infrastructure electronics, and rising packaged electronics consumption. Demand is skewed toward packaging and ESD handling materials as supply chains formalize compliance practices.

Brazil Conductive Polymers Market

The Brazil market in 2025 was at around USD 0.11 billion, representing roughly 2.0% of global revenues.

Middle East & Africa

The Middle East & Africa has a lower base demand but is supported by industrial buildout, energy infrastructure, and localized manufacturing/assembly. Thermal management polymers can appear in specific industrial and infrastructure projects.

GCC Conductive Polymers Market

The GCC market in 2025 was at around USD 0.06 billion, representing roughly 1.0% of global revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Materials Platforms, Compounders, and Capacitor OEMs Shape Competition Through Qualification, Performance Specs, and Application Engineering

The conductive polymers market is led by ICP technology suppliers, specialty compounders, and capacitor OEM ecosystems, where competition is driven more by qualification and performance specs than price. Leaders differentiate through material innovation, application engineering, and long-term OEM partnerships that lock in multi-year programs. Investment is increasingly focused on purity/consistency, conductivity stability, and scalable processing (coating/printing or compounding) to meet demanding ESD/EMI, capacitor, and thermal management requirements. Leading producers, such as Heraeus Group, Agfa-Gevaert NV, SABIC, Covestro, and BASF are directing capital toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices.

LIST OF KEY CONDUCTIVE POLYMER COMPANIES PROFILED

- Heraeus Group (Germany)

- Agfa-Gevaert NV (Belgium)

- SABIC (Saudi Arabia)

- Covestro (Germany)

- BASF (Germany)

- DuPont (U.S.)

- Celanese (U.S.)

- RTP Company (U.S.)

- Avient (U.S.)

- Panasonic Holdings (Japan)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Nichicon developed the PCY series chip-type conductive polymer aluminum solid electrolytic capacitors, rated for 12,000 hours at 125°C. Mass production starts in July 2025, with an exhibition at Electronica China, targeting high-reliability applications in electronics such as automotive and industrial gear. These advanced polymer capacitor trends are for extreme endurance and compact power handling.

- January 2025: Covestro launched a digital simulation suite and an AI Heatsink Screener to optimize heat management using patent-pending Makrolon TC thermally conductive polycarbonates. These tools predict thermal performance in complex designs, outperforming die-cast aluminum in weight and cost for EVs and electronics. They reduce prototyping while enhancing the adoption of conductive polymers in high-heat applications.

- January 2025: Panasonic expanded its OS-CON SVPG conductive polymer capacitors, adding 20-25V ratings with enhanced polymer technology for 1.37x higher ripple current and superior reliability. Aimed at servers, base stations, and AI accelerators, they offer low ESR, 105°C endurance, and compact power smoothing.

REPORT COVERAGE

The report provides a detailed analysis of the conductive polymers market. It focuses on key aspects, such as leading companies, type, and application. Additionally, it provides valuable insights into the market and current industry trends, and highlights key developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 8.3% from 2026 to 2034 |

| Segmentation | By Type, By Application, By Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 5.63 billion in 2025 and is projected to reach USD 11.50 billion by 2034.

Recording a CAGR of 8.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By application, the ESD/EMI Shielding segment leads the market.

Asia Pacific held the highest market share in 2025.

ESD/EMI compliance across electronics handling drives market growth.

- 2021-2034

- 2025

- 2021-2024

- 122

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us