Membrane Filtration Market Size, Share & Industry Analysis, By Type (Reverse Osmosis (RO), Ultrafiltration (UF), Microfiltration (MF), and Nanofiltration (NF)), By Membrane Material (Polymeric, Ceramic, and Others), By Application (Water & Wastewater, Food & Beverages, Industrial, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

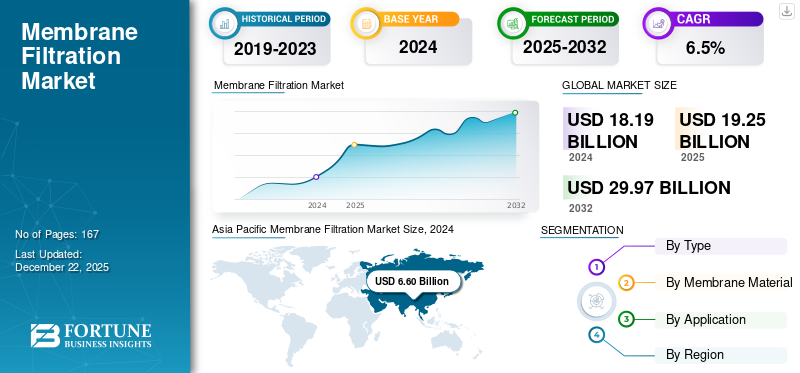

The global Membrane Filtration market size was valued at USD 19.25 billion in 2025. The market is projected to grow from USD 20.38 billion in 2026 to USD 34.08 billion by 2034, exhibiting a CAGR of 6.60% during the forecast period. Asia Pacific dominated the membrane filtration market with a market share of 37% in 2025.

Membrane filtration is a separation technique that uses semi-permeable membranes to selectively allow certain components (e.g., water, small molecules) to pass through while retaining others (e.g., suspended solids, microorganisms, macromolecules, salts). It is widely used in water purification treatment, food & beverage, biotechnology, and pharmaceutical industries.

As government rules tighten and water scarcity increases, the demand for water treatment systems surges. Membrane filtration systems offer excellent contaminant-removal performance, have compact, modular footprints, and are straightforward to scale up, making them the preferred technology for compliance, resilience, and cost control. These advantages are expected to drive market growth.

Furthermore, the market encompasses several major players with Alfa Laval, Mann+Hummel, DuPont, Pall Corporation, and 3M at the forefront. Broad portfolio with innovative product launch, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Membrane Filtration Market KEY TAKEAWAYS

- 2025 Market Size: USD 19.25 billion

- 2026 Market Size: USD 20.38 billion

- 2034 Forecast Market Size: USD 34.08 billion

- CAGR: 6.60% from 2026–2034

- Asia Pacific dominated the membrane filtration market with a 37.00% share in 2025.

- The Reverse Osmosis (RO) segment accounted for the largest market share of 61.73% in 2026.

- The polymeric segment held the largest global market share of 74.39% in 2026.

Asia Pacific

Asia Pacific held a 37.00% share of the global market in 2025, reaching USD 7.05 billion and projected to grow to USD 7.53 billion in 2026.

Europe

Europe accounted for 25.00% of global revenue in 2025, with the market valued at USD 4.89 billion and expected to reach USD 5.16 billion in 2026.

North America

North America represented 20.00% of the global market in 2025, valued at USD 3.88 billion and projected to reach USD 4.13 billion in 2026.

U.S.

U.S. The membrane filtration market is projected to reach USD 3.4 billion by 2026.

Japan

Japan The membrane filtration market is projected to reach USD 0.62 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increased Demand for Clean & Safe Water to Propel the Market Growth

The rising demand for clean and safe water is a major driver of membrane filtration market growth. Rapid growth in population, increasing urbanization, and industrial expansion are putting enormous pressure on limited freshwater resources. Similarly, contamination of surface and groundwater by industrial effluents, agricultural runoff, and municipal waste has made conventional treatment methods less effective in ensuring safe water quality. Governments and international organizations, including the WHO and EPA, have introduced stringent regulations for drinking water and wastewater discharge, convincing municipalities and industries to adopt advanced treatment technologies.

Membrane filtration, particularly ultrafiltration (UF), nanofiltration (NF), and reverse osmosis (RO), and has emerged as a preferred solution as it can effectively remove microorganisms, suspended solids, organic matter, and even dissolved salts. Unlike chemical-based methods, membranes provide a physical barrier to contaminants, ensuring consistently high-quality water without introducing harmful by-products. This technology is also vital to desalination projects in water-scarce regions such as the Middle East and parts of Asia, where access to potable water is a major challenge.

As climate change further stresses freshwater availability and demand for water reuse grows, membrane filtration will continue to expand as a reliable, scalable, and sustainable solution to global water challenges.

MARKET RESTRAINTS

Energy-Intensive Processes to Restrict Market Expansion

One of the key restraints in the market is high energy consumption, particularly in reverse osmosis (RO) desalination and nanofiltration processes. These technologies rely on high-pressure pumps to drive water through semi-permeable membranes, which can be energy-intensive compared to conventional treatment methods.

- For instance, according to the International Desalination Association, energy use in RO desalination typically accounts for 40–55% of total operating costs, making it the single largest expense in many large-scale facilities.

MARKET OPPORTUNITIES

Rising Wastewater Reuse and ZLD Adoption to Create Lucrative Growth Opportunities

A major opportunity for the market lies in wastewater reuse and zero liquid discharge (ZLD) systems. With growing industrialization and increasing water scarcity, governments worldwide are tightening regulations on wastewater discharge, forcing industries to adopt advanced treatment solutions. Membrane technologies such as ultrafiltration (UF), nanofiltration (NF), and reverse osmosis (RO) are at the core of ZLD systems, enabling the recovery of high-quality water while minimizing waste.

- According to the World Bank, global water demand is expected to exceed supply by 40% by 2030, underscoring the urgency of large-scale water reuse.

MARKET CHALLENGES

Fouling and Scaling of Membranes to Hamper Market Growth

A major challenge in the market is issue of fouling and scaling, which significantly impacts system efficiency and operational costs. Fouling occurs when suspended solids, organic matter, or microbial growth accumulate on membrane surfaces, while scaling results from the precipitation of salts such as calcium carbonate or silica. These problems reduce water flux, increase energy consumption, and shorten membrane lifespan, requiring frequent chemical cleaning or costly replacement.

- For example, according to the International Desalination Association, fouling accounts for 30–45% of unplanned downtime in reverse osmosis desalination plants, making it one of the most critical operational challenges. In addition, cleaning chemicals can damage sensitive polymeric membranes, further reducing their durability. This not only raises costs but also disrupts reliability in essential applications such as municipal water supply and pharmaceutical production.

MEMBRANE FILTRATION MARKET TRENDS

Shift toward Digitalization and Smart Monitoring is a Significant Market Trend

One of the most notable trends in the market is the integration of digitalization and smart monitoring systems. Traditional membrane operations often face challenges such as fouling, scaling, and energy inefficiency, which can lead to high maintenance costs and downtime. To address this, companies are increasingly adopting IoT-enabled sensors, artificial intelligence (AI), and predictive analytics to monitor water quality, pressure drops, and membrane performance in real time. These technologies allow operators to predict fouling events, optimize cleaning schedules, and reduce unplanned shutdowns, ultimately extending membrane life.

- For instance, a study by the International Water Association highlighted that predictive maintenance using digital tools can reduce membrane fouling-related downtime by up to 30%. This shift toward smart water management is particularly valuable in industries such as municipal water treatment and pharmaceuticals, where reliability and compliance are critical. As the costs of digital solutions decline, the process adoption is expected to accelerate globally.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

High Efficiency of RO Contributed to Segmental Growth

On the basis of type, the market is classified into Reverse Osmosis (RO), Ultrafiltration (UF), Microfiltration (MF), and Nanofiltration (NF).

The Reverse Osmosis (RO) segment accounted for the largest membrane filtration market share of 61.73% in 2026. The segment has seen steady growth due to its broad applicability and high efficiency in separating dissolved solids, salts, and contaminants from water. RO membranes can remove up to 99% of total dissolved solids (TDS), making them essential for producing safe drinking water, ultrapure water for pharmaceuticals, and high-quality process water for industries.

- According to the International Desalination Association, over 70% of global desalination capacity is based on RO technology, reflecting its dominance.

By Membrane Material

Polymeric Membranes Segment To Lead The Market Due to Strong Adoption Across Key Industries

In terms of membrane materials, the market is categorized into polymeric, ceramic, and others.

The polymeric segment accounted for the largest market share contributing 74.39% globally in 2026 due to its cost-effectiveness, versatility, and wide commercial availability. Polymeric membranes, typically made from materials such as polyethersulfone (PES), polyvinylidene fluoride (PVDF), and polysulfone (PS), dominate as they are significantly cheaper to produce compared to ceramic alternatives, making them attractive for large-scale applications such as in municipal water treatment, food and beverage processing, and pharmaceuticals.

- According to the International Desalination Association and various industry reports, polymeric membranes account for more than 85–90% of the global membrane market by volume, owing to their lower cost and versatility compared to ceramic alternatives.

The ceramic membrane segment is experiencing steady market growth, driven by its durability, chemical resistance, and suitability for harsh operating environments.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rising Water Scarcity and Stricter Discharge Regulations to Propel Water & Wastewater Segment Growth

In terms of application, the market is categorized into water & wastewater, food & beverages, industrial, and others.

The water & wastewater segment captured the largest share of the market of 46.61% in 2026. In 2025, the segment is anticipated to dominate with a share of 46.4%. The segment’s growth is driven by rising water scarcity and stricter discharge regulations. For instance, according to the UN, 80% of global wastewater is still untreated, highlighting vast growth potential.

- According to the European Environment Agency, in the European Union, over 90% of urban wastewater is collected, and around 86% is treated as per EU standards.

Food & beverages segment is expected to grow at a CAGR of 6.4% over the forecast period. The segment is driven by rising demand for high-quality, safe, and nutrient-preserving processing methods. Membrane filtration systems are increasingly adopted for milk protein concentration, whey recovery, juice clarification, and microbial stabilization in brewing, supporting cleaner-label and functional food trends.

Membrane Filtration Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Membrane Filtration Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 37.00% of the global market, reaching a valuation of USD 7.05 billion, and is projected to grow to USD 7.53 billion in 2026. The demand is driven by rapid urbanization, industrial growth, and rising water scarcity. Governments in China, India, and Southeast Asia are investing heavily in wastewater treatment, desalination, and food processing industries to meet regulatory standards and growing population needs. Additionally, expanding dairy, beverage, and pharmaceutical sectors further boosts the adoption of membrane technologies, reinforcing the region’s leadership. In 2025, China market is estimated to reach USD 2.82 billion. The Japan market is valued at USD 0..62 billion by 2026, the China market is valued at USD 3.25 billion by 2026, and the India market is valued at USD 1.34 billion by 2026.

- For instance, according to the China Ministry of Ecology and Environment, the country treats more than 90 million cubic meters of wastewater daily, making it the world’s largest wastewater treatment market. This scale of investment in water infrastructure strongly drives the region’s adoption of membrane filtration technologies.

To know how our report can help streamline your business, Speak to Analyst

Europe

The Europe market was valued at USD 4.89 billion in 2025, capturing 25.00% of global revenue, and is estimated to reach USD 5.16 billion in 2026. Europe is anticipated to witness a notable growth in membrane filtration in the coming years. The EU Urban Waste Water Treatment Directive requires member states to collect and treat wastewater before discharge, pushing municipalities and industries to adopt advanced filtration technologies. Additionally, Europe has a strong food & beverage sector, particularly in dairy, brewing, and juice processing, which relies heavily on ultrafiltration and microfiltration for product quality and safety. The market in Europe is estimated to reach USD 4.89 billion in 2025 and secure the position of the second-largest region in the market. Across this region, Germany is estimated to reach USD 0.98 billion in 2025. The UK market is valued at USD 0.72 billion by 2026, and the Germany market is valued at USD 1.04 billion by 2026.

North America

North America accounted for USD 3.88 billion in 2025, representing 20.00% of the global market share, and is projected to reach USD 4.13 billion in 2026. A major growth driver for the market in North America is increasing demand for safe drinking water and advanced wastewater treatment. The U.S. and Canada face aging water infrastructure, pushing municipalities toward modern membrane filtration technologies such as RO and UF. Backed by these factors, countries including the U.S. are expected to record USD 3.2 billion, and Canada to record USD 0.68 billion in 2025. The U.S. market is valued at USD 3.4 billion by 2026.

Latin America and Middle East & Africa

Middle East & Africa contributed approximately USD 2.05 billion to the global market in 2025, accounting for 11.00% share, and is expected to reach USD 2.12 billion in 2026. The Latin America region captured 7.00% of the global market in 2025, generating USD 1.38 billion in revenue, and is projected to reach USD 1.44 billion in 2026. The region’s market is driven primarily by growing investments in water and wastewater treatment infrastructure. Rising urbanization and industrialization in countries such as Brazil, Mexico, and Chile are increasing demand for advanced filtration systems to address water scarcity and pollution. In the Middle East & Africa, Saudi Arabia is set to attain the value of USD 2.05 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Offerings and Global Reach Support Competitive Advantage for Key Players

The market is moderately fragmented, with few major companies dominating global production and trade. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Alfa Laval, Mann+Hummel, DuPont, Pall Corporation, and 3M are some of the dominating players in the market. A comprehensive range of products, global presence through a strong distribution network, and collaborations with end-use industries are few characteristics of these players that support their dominance.

Apart from this, other prominent players in the market include Veolia, KOCH, Toray Industries, and others. These companies are undertaking various strategic initiatives, such as investments in R&D and partnerships with other companies to enhance their market presence.

LIST OF KEY MEMBRANE FILTRATION COMPANIES PROFILED

- Mann +Hummel (Germany)

- DuPont (U.S.)

- Pall Corporation (U.S.)

- 3M (U.S.)

- Toray Industries (Japan)

- Veolia (France)

- Pentair (U.K.)

- KOCH Separation Solutions (U.S.)

- Synder Filtration (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Alfa Laval secured one of its largest-ever membrane filtration orders, an approximately USD 9.38 million contract to build an advanced nano- and ultrafiltration plant for a fermentation facility in Asia. The system will be delivered in autumn 2025, highlighting Alfa Laval’s capacity to engineer highly customized, large-scale membrane solutions.

- March 2025: DuPont Water Solutions has introduced WAVE PRO, an advanced online modeling tool designed to support ultrafiltration (UF) applications across drinking water, industrial utility water, wastewater treatment, and seawater desalination.

- February 2025: Pall Corporation and MTR Carbon Capture have partnered to deliver modular, scalable, and cost-effective carbon capture solutions. The collaboration combines MTR’s Polaris membrane system with Pall’s advanced filtration and pre-treatment technologies, ensuring efficient flue gas processing and protection of critical assets across decarbonization industries.

- January 2025: Toray Industries has developed a high-efficiency separation membrane module for biopharmaceutical The new module offers over twice the filtration performance of conventional systems, reduces clogging, and is expected to boost yields above 90% while improving purification.

- July 2023: DuPont has launched its first nanofiltration products dedicated to lithium brine purification — the DuPont FilmTec LiNE-XD and LiNE-XD HP membranes. These new elements are designed to deliver high lithium recovery from chloride-rich brine streams while providing strong selectivity against divalent metals such as magnesium.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.60% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Reverse Osmosis (RO) · Ultrafiltration (UF) · Microfiltration (MF) · Nanofiltration (NF) |

|

By Membrane Material · Polymeric · Ceramic · Others |

|

|

By Application · Water & wastewater · Food & beverages · Industrial · Other |

|

|

By Geography · North America (By Type, Membrane Material, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Type, Membrane Material, Application, and Country/Sub-region) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Spain (By Application) o Russia (By Application) o Rest of Europe (By Application) · Asia Pacific (By Type, Membrane Material, Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Type, Membrane Material, Application, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America(By Application) · Middle East & Africa (By Type, Membrane Material, Application, and Country/Sub-region) o GCC (By Application) o South Africa (By Application) · Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 19.25 billion in 2025 and is projected to reach USD 34.08 billion by 2034.

In 2025, the market value stood at USD 7.05 billion.

The market is expected to exhibit a CAGR of 6.60% during the forecast period of 2026-2034.

The Reverse Osmosis (RO) segment led the market by type.

The key factor driving the market is the increasing demand for clean and safe water.

Alfa Laval, Mann+Hummel, DuPont, Pall Corporation, and 3M are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Increasingly strict food safety, pharmaceutical purity, and water treatment regulations are expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us