Polyvinylidene Fluoride (PVDF) Market Size, Share & Industry Analysis, By Type (Homopolymer PVDF, Copolymer PVDF, and Others), By Application (Battery, Coatings, Films & Sheets, Pipes & Fittings, Wire & Cable, Membranes, and Others), By End Use Industry (Automotive & Transportation, Chemical, Building & Construction, Electrical & Electronics, Energy, and Others), and Regional Forecast, 2025-2032

Polyvinylidene Fluoride (PVDF) Market Size and Future Outlook

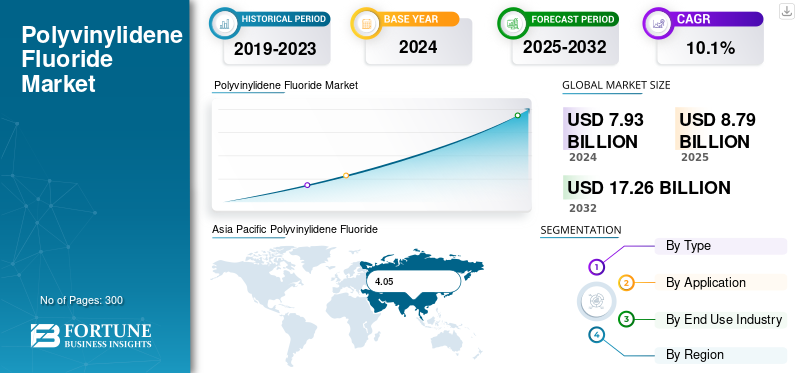

The global Polyvinylidene Fluoride (PVDF) market size was valued at USD 7.93 billion in 2024. The market is projected to grow from USD 8.79 billion in 2025 to USD 17.26 billion by 2032, exhibiting a CAGR of 10.1% during the forecast period. Asia Pacific dominated the global polyvinylidene fluoride (PVDF) market with a market share of 51.07% in 2024.

PVDF is a high-performance semi-crystalline fluoropolymer produced primarily by the polymerization of vinylidene fluoride (VDF) monomer. The material offers exceptional chemical resistance and mechanical strength, making it a preferred engineering polymer across demanding applications such as coatings, membranes, lithium ion batteries, wires and cables, and high-purity piping systems. Its versatility enables use in both homopolymer and copolymer forms, tailored for flexibility, purity, or mechanical strength depending on end-use specifications.

Product’s use in architectural coatings, chemical processing components, and photovoltaic backsheets continues to benefit from durability and corrosion resistance mandates. As global industries align with sustainability targets and material efficiency goals, PVDF’s lightweight profile, recyclability initiatives, and compatibility with next-generation electrolytes are supporting its penetration across energy storage and advanced manufacturing sectors.

The market is dominated by several major players, with Arkema S.A., Solvay S.A., Kureha Corporation, and 3M Company at the forefront. Their broad product portfolios, including Kynar, Solef, and Foraflon, as well as geographic expansion in Asia Pacific, and continued investment in battery-grade PVDF capacities, have reinforced their leading position globally.

Download Free sample to learn more about this report.

POLYVINYLIDENE FLUORIDE (PVDF) MARKET KEY TAKEAWAYS

- 2024 Market Size: USD 7.93 billion

- 2025 Market Size: USD 8.79 billion

- 2032 Forecast Market Size: USD 17.26 billion

- CAGR: 10.1% from 2025–2032

- Asia Pacific dominated the market with a 51.07% share in 2024.

- The Automotive & Transportation segment dominated the market in 2024.

- The Homopolymer PVDF segment held the largest market share in 2024.

North America

North America is expanding with investments in lithium-ion battery manufacturing and clean energy.

Europe

Europe is witnessing steady growth due to rising demand for EVs, renewable energy, and sustainable construction.

Asia Pacific

Asia Pacific led the market with USD 4.05 billion in 2024, driven by EV and battery production.

U.S.

Capacity expansion and EV gigafactories are strengthening demand for high-purity PVDF.

Japan

Strong fluoropolymer manufacturing and battery supply chains continue to support market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rapid Expansion of Electric Vehicle (EV) Production and Energy Storage Systems to Drive Market Growth

The exponential rise of Electric Vehicles (EVs) and renewable energy storage has made PVDF a strategic material across the energy value chain. PVDF is widely used as a binder and separator coating polymer in lithium-ion batteries due to its superior adhesion, dielectric strength, and resistance to solvents and electrolytes. Its ability to maintain structural integrity and thermal stability at high voltages enhances battery efficiency, longevity, and safety, making it indispensable for NCM, NCA, and LFP chemistries. As global EV production surpasses 15 million units annually, with battery gigafactory expansions in China, Europe, and the U.S., the consumption of battery-grade PVDF has surged significantly. In parallel, the integration of renewable energy storage systems (ESS) and grid-scale batteries is broadening the material’s application footprint. Therefore, rapid expansion of EV production and growing demand for energy storage systems are set to drive the global polyvinylidene fluoride (PVDF) market growth during the forecast period.

MARKET RESTRAINTS:

Tightening Environmental regulations and Limited Production Capacity for Battery-Grade PVDF May Hamper Market Growth

The tightening of PFAS (per- and polyfluoroalkyl substances) regulations in Europe and North America poses one of the most significant challenges for the PVDF industry. Although PVDF itself is typically considered a stable, non-migratory polymer, its association with the broader PFAS family has led to regulatory scrutiny. Agencies such as the European Chemicals Agency (ECHA) and the U.S. Environmental Protection Agency (EPA) are implementing policies to restrict the production and emissions of fluorochemicals, compelling manufacturers to adopt closed-loop and low-emission production systems.

Furthermore, the market faces growing pressure from supply chain tightness and limited production capacity for battery-grade PVDF, a critical material used in lithium-ion battery binders. Rapid growth in EV manufacturing and energy storage systems has outpaced global PVDF capacity expansions, creating bottlenecks that ripple through downstream industries. Restricted availability of high-purity grades, long lead times, and dependence on a few specialized suppliers intensify pricing volatility and procurement risks. Until substantial capacity additions materialize, the supply of battery-grade PVDF will remain a key restraint.

MARKET OPPORTUNITIES:

Increasing use of PVDF Membranes in Water Treatment, Pharmaceuticals, and Chemical Separation Processes Generate Growth Prospects

The expanding use of PVDF membranes in water treatment, pharmaceuticals, and chemical separation processes presents a strong growth opportunity for the global market. PVDF’s superior chemical resistance, hydrophobicity, thermal stability, and mechanical strength make it an ideal material for ultrafiltration, microfiltration, and nanofiltration systems. The rising global focus on clean water access, stricter discharge regulations, and the modernization of industrial wastewater treatment plants are driving the widespread adoption of PVDF membrane technologies. Similarly, in the pharmaceutical industry, increasing biologics production, the need for sterile filtration, and purification processes further accelerate demand. In the chemical and petrochemical industries, PVDF membranes are relied upon for solvent recovery and high-purity separations, where durability and performance under harsh operating conditions are critical. As companies prioritize efficient, energy-saving, and long-life filtration solutions, PVDF membranes are positioned to capture significant value. Growing investments in desalination, water recycling, and advanced membrane systems will create lucrative opportunities.

POLYVINYLIDENE FLUORIDE (PVDF) MARKET TRENDS:

High-Purity PVDF for Battery Binders and Next-Generation PVDF Grades

High-purity PVDF and next-generation PVDF grades are rapidly emerging as the central focus of market growth, driven primarily by the accelerating shift toward electric mobility and advanced energy storage technologies. Battery manufacturers increasingly require ultra-high-purity PVDF binders to ensure superior adhesion, chemical stability, and cycle life in lithium-ion cells used for EVs and high-capacity energy storage systems. This demand is pushing producers to enhance purification technologies, develop cleaner production routes, and expand specialty-grade PVDF capacities.

Simultaneously, next-generation PVDF grades engineered for improved thermal resistance, higher molecular weight, and tailored rheological properties are gaining importance in high-performance membranes, separators, coatings, and cathode formulations. Innovations such as modified PVDF copolymers and gradient-distribution binder technologies are reshaping PVDF products development pipelines. As global EV battery manufacturing scales up and clean energy transitions accelerate, the focus on high-performance, application-specific PVDF grades will continue to intensify, making these advanced materials the epicenter of long-term market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Homopolymer PVDF Gains High Demand Due to its Durability and Cost Efficiency

On the basis of type, the market is classified into homopolymer PVDF, copolymer PVDF, and others.

The homopolymer PVDF segment accounted for the largest global polyvinylidene fluoride market share in 2024. Homopolymer PVDF is the most widely used form of polyvinylidene fluoride, produced by the direct polymerization of vinylidene fluoride monomers. It offers high crystallinity, superior chemical resistance, and excellent mechanical and thermal stability. These properties make it ideal for coatings, pipes and fittings, wires and cables, as well as chemical processing equipment. Due to its outstanding purity, durability, and cost efficiency, it represents the dominant share of total PVDF consumption globally across industrial and high-performance engineering applications.

Copolymer PVDF is synthesized by polymerizing vinylidene fluoride with comonomers such as hexafluoropropylene (HFP) or trifluoroethylene (TrFE). This modification imparts greater flexibility, lower melting point, and enhanced processability compared to the homopolymer. Copolymer PVDF exhibits improved film-forming ability, making it suitable for lithium-ion battery binders, coatings, and membranes requiring higher elongation and adhesion. The increasing demand for battery-grade copolymers, combined with the product’s superior dispersion stability, is driving the segment’s rapid growth, particularly in the energy storage and advanced electronics sectors.

The others segment in PVDF types encompasses modified PVDF blends, terpolymers, and tailored product solutions designed to meet specialized performance requirements. These variants are often reinforced with glass fibers, carbon, or nano-fillers to improve thermal conductivity, mechanical strength, or dielectric response. Emerging formulations include cross-linked and functionalized PVDF materials, which are used in biomedical devices, membranes, and next-generation capacitors. Although smaller in volume, these niche PVDF variants represent high-value opportunities driven by customization, sustainability goals, and the development of advanced functional materials.

By Application

Battery Application Leads as PVDF is Extensively used in lithium-ion Batteries

On the basis of application, the market is classified into battery, coatings, films & sheets, pipes & fittings, wire & cable, membranes, and others.

The battery segment holds the leading position in the market. PVDF is extensively used as a binder and separator coating in lithium-ion batteries due to its superior chemical resistance, adhesion, and electrochemical stability. It ensures uniform dispersion of active materials, enhancing energy density and cycling performance. Battery-grade PVDF, especially high-purity homopolymers and copolymers, has become indispensable in cathode formulations for NCM, NCA, and LFP chemistries. With the rapid expansion of electric vehicles, renewable energy storage, and grid applications, battery use represents the fastest-growing PVDF segment.

PVDF coatings are valued for their exceptional UV resistance, weatherability, and chemical inertness, making them ideal for architectural, industrial, and chemical applications. Widely used on metal panels, claddings, and façades, these coatings provide long-term color stability and corrosion protection in harsh environments. Additionally, PVDF-based coatings are used in offshore infrastructure, aerospace components, and photovoltaic back sheets. With increasing sustainability standards and demand for low-maintenance structures, PVDF coatings are gaining adoption as a high-performance solution for durable and aesthetically pleasing surface protection.

PVDF pipes and fittings are used in the chemical processing, water treatment, and semiconductor industries, where resistance to acids, oxidants, and solvents is crucial. Their high mechanical strength, high temperature tolerance up to 150°C, and low permeability make them ideal for corrosive fluid transport systems. PVDF’s smooth internal surface minimizes pressure drop and contamination, ensuring consistent performance in ultrapure water and chemical handling systems. Growth in pharmaceuticals, electronics, and environmental infrastructure continues to drive this segment’s industrial relevance.

The others segment encompasses specialized and emerging PVDF applications, including sensors, 3D printing filaments, coatings for medical devices, and piezoelectric films. PVDF’s unique electroactive properties enable its use in actuators, transducers, and smart material systems. In medical and analytical fields, it serves as a durable, biocompatible polymer for microfluidic and diagnostic components. While smaller in volume, these niche applications represent significant technological innovation and value creation opportunities, driven by PVDF’s versatility across advanced engineering and functional materials markets.

By End Use Industry

Automotive & Transportation to Maintain Dominance Due to Surging Demand for EVs

Based on end use industry, the market is segmented into automotive & transportation, chemical, building & construction, electrical & electronics, energy, and others.

To know how our report can help streamline your business, Speak to Analyst

The automotive and transportation industry segment dominated the market share in 2024. PVDF is increasingly used in the automotive and transportation industry for fuel system components, wire insulation, battery binders, and coatings due to its excellent chemical resistance, thermal stability, and lightweight profile. The surge in EV production has driven the adoption of PVDF as a key material for lithium-ion battery cathode binders and separator coatings. Additionally, PVDF-coated films and tubing are employed in fuel lines, brake cables, and emission control systems, ensuring durability and corrosion resistance. Its combination of high performance, weight reduction, and chemical inertness will continue to strengthen PVDF’s role in modern mobility and electrification systems.

In the chemical processing industry, PVDF is valued for its exceptional resistance to acids, bases, and oxidizing agents, making it ideal for piping, valves, tanks, and linings exposed to aggressive environments. PVDF components are widely used in chlor-alkali, petrochemical, and semiconductor industries for chemical delivery systems. Its purity and low permeability prevent contamination, meeting stringent industrial and environmental standards. As global chemical and pharmaceutical industries expand, PVDF’s role as a reliable corrosion-resistant material continues to gain prominence.

The others category encompasses specialized PVDF applications in the medical, pharmaceutical, and industrial sectors. PVDF membranes are utilized in sterile filtration, bioprocessing, and analytical equipment due to their purity and biocompatibility. In the aerospace industry, PVDF coatings and films offer lightweight, corrosion-resistant surfaces for structural components. Although smaller in market volume, these high-value applications highlight PVDF’s adaptability across precision and performance-driven sectors, reflecting its continued evolution as an advanced material in modern engineering and scientific innovation.

Polyvinylidene Fluoride (PVDF) Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Polyvinylidene Fluoride (PVDF) Market Size, 2024(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valued at USD 4.05 billion, and is expected to lead in 2025. The region dominates the global polyvinylidene fluoride (PVDF) market share, accounting for the majority of production and consumption. The region’s growth is underpinned by rapid industrialization, the adoption of electric vehicles, and the expansion of solar energy. PVDF demand is concentrated in lithium-ion battery binders, chemical processing components, and high-performance coatings. Leading producers in China, Japan, and South Korea have established vertically integrated value chains for fluoropolymers, supported by robust raw material availability and cost-efficient manufacturing. In 2025, the market in China is estimated to reach USD 2.84 billion.

- China is the world's largest producer of lithium-ion batteries, which makes it the largest consumer of PVDF globally. The country also hosts extensive VDF and PVDF production capacity, supported by major players such as Dongyue, Zhejiang Fluorine, and Sinochem. China’s leadership in battery manufacturing and photovoltaic installations has positioned it as the global epicenter of PVDF demand, driving rapid innovation in high-purity and copolymer grades for advanced applications.

To know how our report can help streamline your business, Speak to Analyst

Europe

The European PVDF market benefits from strong regulatory support for electric vehicles, renewable energy, and sustainable construction. Demand is concentrated in France, Germany, and the U.K., where stringent emission standards and industrial electrification are accelerating the use of battery-grade and coating-grade PVDF. European producers, such as Solvay and Arkema, are advancing low-carbon and PFAS-compliant manufacturing technologies to align with REACH and the Green Deal objectives. Ongoing initiatives to localize battery material supply chains are expected to sustain moderate yet consistent growth in PVDF consumption across the continent.

North America

The North American PVDF market is driven by the expansion of the electric mobility, renewable energy, and chemical processing industries. Growing investment in lithium-ion battery manufacturing, supported by the Inflation Reduction Act (IRA) and clean energy policies, has positioned the region as a key growth hub for battery-grade PVDF. In the U.S., significant capacity expansions by Arkema and Solvay, coupled with the establishment of EV gigafactories, are reinforcing the country’s leadership in high-purity PVDF for energy storage and advanced industrial applications.

Rest of The World

Over the forecast period, the Latin America and Middle East & Africa regions would witness a moderate growth in this market. The Latin America PVDF market remains relatively small but is gradually expanding, supported by growth in infrastructure development, coatings, and industrial applications. Brazil and Mexico lead regional consumption, driven by construction, automotive components, and chemical processing projects.

The Middle East & Africa (MEA) PVDF market is characterized by moderate but steady growth, driven by industrial expansion, desalination, and infrastructure development. In the MEA PVDF market, the Gulf Cooperation Council (GCC) countries are key consumers, utilizing PVDF in piping, membranes, and protective coatings for oil, gas, and water treatment facilities. Although the region currently relies on imports, government diversification strategies and local manufacturing initiatives are expected to gradually strengthen its position in the global PVDF value chain.

COMPETITIVE LANDSCAPE

Key Industry Players:

Rapidly Scaling Battery Grade Production is Identified as a Key Growth Strategy by Key Players

The global polyvinylidene fluoride market is characterized by a few key players investing in capacity expansion, sustainability, and the development of new applications. Key companies include Arkema S.A., Solvay S.A., Kureha Corporation, Dongyue Group, and 3M Company. These firms collectively account for a majority of global capacity, supported by vertically integrated operations and established brands such as Kynar, Solef, and Foraflon. Competitive strategies focus on expanding battery-grade PVDF production, regional localization, and innovation in PFAS-free processes to meet evolving environmental standards. Collaboration with battery and cathode material producers will allow companies to strengthen their positioning and sustain long-term growth.

LIST OF KEY POLYVINYLIDENE FLUORIDE (PVDF) COMPANIES PROFILED:

- 3M Company (U.S.)

- Arkema (France)

- Daikin Industries, Ltd. (Japan)

- Dongyue Group Limited (China)

- Flurine (China)

- Gujarat Fluorochemicals (India)

- Kureha Corporation (Japan)

- Shandong Hengyi New Material Technology Co., Ltd (China)

- Shinkwang Acrylic (SKPC) (South Korea)

- Syensqo (Belgium)

KEY INDUSTRY DEVELOPMENTS:

- August 2023: Solvay and Agru, a leader in engineered polymer applications, entered into a long-term supply agreement under which Solvay will provide Solef PVDF to Agru for the production of ultra-pure water piping systems used in the rapidly growing semiconductor industry.

- August 2023: Kureha Corporation announced the plan to increase production capacity for PVDF at its Iwaki Factory in Fukushima, Japan. The strategic expansion plan will address the growing customer demand and will further expand the PVDF business, which is the most promising business division for the company.

- June 2023: Solvay and Zotefoams formed a partnership under which Solvay will provide Solef PVDF to Zotefoams to produce Zotefoams' ZOTEK F, a high-performance, closed-cell, cross-linked aerospace foam range. The collaboration targets a wide range of interior applications in the aerospace industry, including ducting, carpet underlay, environmental control systems, and insulation.

- October 2022: The U.S. Department of Energy's Office of Manufacturing and Energy Supply Chains announced funding worth USD 178 million to Solvay. The funding will support Solvay’s construction of a facility at its Augusta, Georgia, site to produce battery-grade PVDF.

- February 2022: Solvay is expanding the production capacity of its high-performance polymer, PVDF, known as “Solef,” at its site in Tavaux, France. The expansion initiative is part of the company's existing leadership position in the global lithium-ion battery market, positioning it to capitalize on the growing demand for electric and hybrid vehicles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 10.1% from 2025-2032 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Type, Application, End Use Industry, and Region |

| By Type |

|

| By Application |

|

| By End Use Industry |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.93 billion in 2024 and is projected to reach USD 17.26 billion by 2032.

In 2024, the market value stood at USD 4.05 billion.

The market is expected to exhibit a CAGR of 10.1% during the forecast period of 2025-2032.

The homopolymer PVDF segment led the market by type.

The key factors driving the market are the rising demand for PVDF as a battery binder and coating agent in lithium-ion batteries.

Arkema S.A., Solvay S.A., Kureha Corporation, 3M Company, and Dongyue Group Limited are some of the prominent players in the market.

Asia Pacific dominated the market in 2024 by holding the largest share.

An increased focus on high-purity and battery-grade polyvinylidene fluoride will favor product adoption.

- 2019-2032

- 2024

- 2019-2023

- 300

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us