Battery Materials Market Size, Share & Industry Analysis By Type (Lithium-Ion, Lead Acid, Nickel Metal Hydride Battery, Solid-State Battery, and Others), By Materials (Lithium-ion {Cathode [LCO, NMC, NCA, LMO, and, LFP], Anode [Artificial Graphite, Natural Graphite, and Others], Electrolyte, Separator, and Others} and Lead Acid {Cathode, Anode, Electrolyte, Separator and Others}), By Application (Lithium-Ion {Consumer Electronics, Automotive, Industrial, and Others} and Lead Acid {Automotive, Industrial, and Others}), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

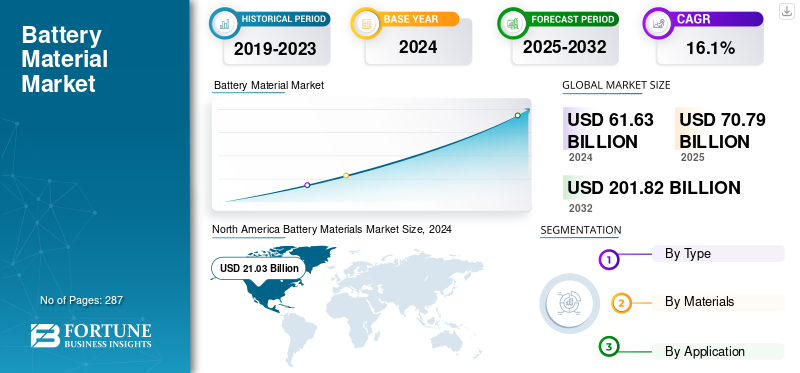

The global battery materials market size was valued at USD 61.63 billion in 2024. The market is projected to grow from USD 70.79 billion in 2025 to USD 201.82 billion by 2032 at a CAGR of 16.1% during the forecast period. North America dominated the global battery materials market with a market share of 34.12% in 2024.

A battery is a device that consists of one or more electrochemical cells with external connections that provide power to other electrical devices. Battery materials are the raw materials used to construct batteries. Battery materials include active cathode materials, anode materials, separator films, electrolytes, electrode tapes, electrodes, electrolyte solvents, and other materials.

About 60% of the battery is made up of a combination of materials such as manganese (cathode), potassium, and zinc (anode). Secondary batteries are rechargeable and are obtained from nickel-hydrogen, lithium-ion, and nickel-cadmium sources. Lithium-ion batteries are extensively adopted owing to their high energy density and are significantly used in automotive, industrial, and consumer electronics applications. Improved compatibility and reliability of Li-ion batteries have led to a surge in demand for cathode. The rising demand from the automotive industry for various battery types, such as lithium-ion and lead-acid batteries, the increasing adoption of electric vehicles, and the expansion of renewable energy infrastructure will drive the market size.

The primary materials utilized in battery manufacturing include lithium, which is essential for the production of lithium-ion batteries; lithium is a critical component in the energy storage sector. Cobalt is used in cathodes to enhance energy density and stability, and it is vital for high-performance batteries. Nickel contributes to higher energy density and is increasingly used in battery chemistries. Graphite serves as the anode material. It is crucial for battery performance. Manganese is utilized in specific battery chemistries to improve stability and safety.

Download Free sample to learn more about this report.

Battery Materials Market KEY TAKEAWAYS

- 2024 Market Size: USD 61.63 billion

- 2025 Market Size: USD 70.79 billion

- 2032 Forecast Market Size: USD 201.82 billion

- CAGR: 16.1% from 2025–2032

- North America dominated the battery materials market with a 34.12% share in 2024.

- The lithium-ion segment accounted for the largest market share in 2024.

- The cathode materials segment accounted for the largest market share in 2024.

North America

Held the largest market share in 2024, supported by rising EV demand, battery innovation, and domestic supply chain investments.

Europe

Expected to witness significant growth, driven by EV adoption targets, battery recycling, and critical mineral initiatives.

Asia Pacific

Expected to witness the fastest growth, driven by strong EV production, battery manufacturing, and renewable energy adoption.

U.S.

Expected to witness steady growth, supported by expanding EV production and government incentives for battery materials.

Japan

Expected to witness steady growth, driven by advanced battery manufacturing and strong presence of leading technology companies.

Read More

BATTERY MATERIALS MARKET TRENDS

Rise in Automotive Sector and Sustainability Initiatives to Drive the Market Growth

The automotive sector is witnessing a significant increase in electric vehicle adoption. In 2022, the demand for lithium-ion batteries surged by 65%, reaching 550 GWh compared to 330 GWh in 2021. This growth highlights the critical role of battery materials in meeting EV production needs. Continuous R&D is enhancing battery performance and cost-efficiency. Innovations in chemistries such as lithium nickel manganese cobalt (NMC) and lithium iron phosphate (LFP) are improving energy density, making batteries more affordable and efficient for EV applications.

Moreover, global supply chains for critical minerals are increasingly affected by trade restrictions and resource nationalism. For example, China's ban on the export of gallium, germanium, and antimony has disrupted industries relying on these materials, emphasizing the need for diversified sourcing strategies. To mitigate environmental impact and reduce reliance on raw material extraction, recycling initiatives are gaining traction. Europe, for instance, has set ambitious goals to recycle enough battery material by 2030 to support the production of two million electric vehicles, aligning with global sustainability trends.

MARKET DYNAMICS

MARKET DRIVERS

Smart Device Evolution Intensifies the Demand For Advanced Battery Materials

The consumer electronics sector continues to be a significant driver of demand for battery materials, with the persistent growth of smartphones, laptops, and tablets forming the foundation of this demand. As these devices become more powerful and feature-rich, they require increasingly sophisticated battery solutions to maintain reasonable usage times while supporting enhanced capabilities and larger screens.

The emergence of wearable technology has added another layer of demand to the market. Smartwatches, fitness trackers, wireless earbuds, and other wearable devices each require compact, high-performance batteries. This market segment is experiencing rapid growth as consumers embrace these technologies for health monitoring, communication, and entertainment purposes.

Battery performance has become a critical differentiator in consumer electronics, with manufacturers competing to offer devices with longer battery life and faster charging capabilities. This has led to ongoing research and development in battery materials and technologies, pushing the boundaries of energy density and charging speeds. Companies are investing heavily in developing new battery solutions that can meet these demanding requirements while maintaining safety and reliability.

The Internet of Things (IoT) revolution has further expanded the need for battery materials, as billions of connected devices are being deployed in homes, offices, and industrial settings. These devices, ranging from smart home sensors to industrial monitoring equipment, require reliable power sources that can often operate for extended periods without replacement.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Supply Chain and Infrastructure Challenges Hampers the Market Expansion

Supply chain constraints and technical/infrastructure challenges are significantly hampering the growth of the market. The heavy concentration of critical raw materials in a few countries, particularly lithium in Chile and cobalt in Congo, creates supply vulnerabilities and geopolitical risks. This geographic consolidation, combined with international trade tensions, makes it difficult for manufacturers to ensure stable material supplies. The situation is further complicated by limited refining capacity globally, as processing these materials requires sophisticated facilities and expertise. Additionally, the technical challenges in processing battery-grade materials demand substantial capital investment, with new mining operations and refining facilities requiring significant upfront costs. The establishment of new mining projects faces lengthy lead times, often taking years from exploration to production. The infrastructure needed for efficient material processing and transportation is also lacking in many regions, creating blockage in the supply chain. These factors collectively create a complex web of challenges that slow down market expansion and make it difficult for new players to enter the market, ultimately restricting the overall growth of the sector.

MARKET OPPORTUNITIES

Exponential Growth In Energy Storage Systems to Drive Market Growth

The energy storage systems (ESS) sector is creating substantial opportunities in the market through its rapid expansion across utility, commercial, and residential applications. The growing deployment of renewable energy sources, particularly solar and wind power, has made energy storage essential for grid stability and reliability, driving demand for large-scale battery installations. Utility companies are increasingly investing in grid-scale battery storage systems to manage peak load demands and integrate intermittent renewable energy sources. This trend is creating significant opportunities for battery material suppliers, particularly in the lithium-ion segment, as these installations require massive amounts of raw materials. The commercial and industrial sectors are adopting energy storage solutions to reduce electricity costs, ensure power quality, and meet sustainability goals. This has opened new market opportunities for various battery chemistries and materials, including flow batteries and advanced lead-acid systems.

MARKET CHALLENGES

Supply Chain Disruptions, Environmental and Ethical Concerns, and Price Volatility Hampers the Market Growth

Countries often impose trade restrictions or tariffs as part of more extensive geopolitical strategies, disrupting the global flow of critical materials. For example, the U.S. government has raised concerns about over-reliance on chinese lithium batteries due to national security risks and trade imbalances. Key components such as lithium, cobalt, and nickel are essential for battery production, but their supply chains are concentrated in a few regions. Supply chain disruptions can increase lead times, raise costs, and limit production, particularly in industries like electric vehicles (EVs).

The extraction of raw materials like lithium and cobalt often involves habitat destruction, water depletion, and soil degradation. Lithium mining, for instance, requires significant water resources, leading to challenges in arid regions like Chile's Atacama Desert. Cobalt mining in the DRC is linked to child labor and unsafe working conditions, raising significant human rights concerns.

Moreover, political instability in resource-rich countries or changes in export policies can impact availability and prices. Rising raw material costs can reduce profit margins for battery producers. Small and medium-sized manufacturers are particularly vulnerable to price fluctuations due to limited resources to absorb sudden cost increases. Companies like Tesla are securing their supply chains by investing directly in mining and refining operations.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

The global market is facing significant challenges due to the rise of trade protectionism and resource nationalism. Countries are increasingly implementing policies to secure access to critical minerals, leading to supply chain disruptions and increased costs for manufacturers. China, a dominant player in the market, has recently taken steps to tighten control over its resources:

In 2024, China implemented export restrictions on key minerals like gallium, germanium, and graphite, essential for semiconductor and battery production. These measures aim to protect domestic industries and maintain technological and economic dominance. These restrictions have led to significant supply chain disruptions, increased technology development costs, and potential shifts in global mineral and technology sourcing strategies.

Other nations are responding to these challenges by seeking to diversify their supply chains and reduce dependence on dominant suppliers. The U.S. has been lobbying for access to alternative sources of rare earths. For instance, U.S. and Danish officials have lobbied Tanbreez Mining, the developer of Greenland's largest rare earth deposit, not to sell its project to Chinese-linked firms, highlighting efforts to secure critical mineral supplies. Countries rich in critical minerals are increasingly asserting control over their resources. For example, Chile's government has moved to take greater control of its lithium resources, aiming to benefit more from the global demand for this essential battery material.

SEGMENTATION ANALYSIS

By Type

Lithium-Ion Remains the Leading Segment Due to Growing Electric Vehicle Demand.

Based on type, the market is segmented into lithium-ion, lead acid, nickel metal hydride battery, solid-state battery, and others.

The lithium-ion segment held the largest battery materials market share in 2024 and is anticipated to dominate the market during the forecast period. This is due to their high energy density, long lifespan, and broad applicability across industries such as electric vehicles (EVs), consumer electronics, and renewable energy storage. The significant growth driving the segment is the surging demand for EVs, fueled by global efforts to transition to clean energy and reduce greenhouse gas emissions. Governments globally are implementing stringent emissions regulations and offering subsidies to promote EV adoption, thereby driving the demand for lithium-ion batteries. Additionally, advancements in lithium-ion technology, such as the development of solid-state batteries and high-capacity cathodes, are enhancing performance and reducing costs, further accelerating market growth.

The lead-acid segment is expected to grow significantly during the forecast period due to its reliability, cost-effectiveness, and established applications. The automotive industry remains the largest end-user, with lead-acid batteries being widely used in starter, lighting, and ignition (SLI) applications in internal combustion engine vehicles. Additionally, the rising demand for hybrid vehicles, which also rely on lead-acid batteries for auxiliary power, contributes to the segment's growth.

The nickel metal hydride battery segment witnessed significant growth during the forecast period. The growth is driven by its unique balance of performance, cost-effectiveness, and environmental considerations. NiMH batteries offer high energy density and long cycle life, making them ideal for applications in hybrid electric vehicles (HEVs), consumer electronics, and industrial equipment. The growing adoption of HEVs, particularly as a transitional technology towards full electrification, has bolstered the demand for NiMH batteries. These batteries are preferred in HEVs for their ability to handle frequent charging and discharging cycles, reliability, and mature supply chain.

The solid-state battery segment is expected to grow considerably during the forecast period due to the growing demand for high-performance batteries in electric vehicles (EVs) and renewable energy storage systems. The automotive industry is witnessing solid-state batteries as game-changers, offering extended driving ranges, faster charging times, and reduced risks of thermal runaway.

By Material

Cathode Segment is the Largest and Fastest Growing Segment Owing to Growing Adoption in Applications

Based on material, the lithium-ion is segmented into cathode, anode, electrolyte, separator, and others. The cathode segment is further bifurcated into lithium cobalt oxide, lithium iron phosphate, lithium manganese oxide, lithium nickel cobalt aluminium oxide, and lithium nickel manganese oxide. the anode material is further segmented into artificial graphite, natural graphite, and others.

The cathode materials segment held the largest market share in 2024 and is anticipated to dominate the market during the forecast period due to the increasing demand for high-performance batteries across a range of applications. The primary active components of cathode materials are cobalt, manganese, and nickel. Today, cobalt is substituted partially by nickel, mostly Lithium Nickel, Manganese Oxide (NMC), and Nickel Cobalt Aluminium Oxide (NCA). Cathode materials require an extremely high purity level and must be free from unwanted metal impurities, mainly sulfur, vanadium, and iron. The growing shift towards sustainability, lower costs, and energy efficiency is driving investments in cathode material innovations, along with significant research and development efforts to increase the efficiency, stability, and performance of these cathode materials.

As global demand for EVs, portable electronics, and energy storage systems increases, the demand for advanced electrolyte materials is growing significantly. The conventional liquid electrolyte, composed of lithium salts in an organic solvent, remains the most widely used type in commercial lithium-ion batteries due to its high ionic conductivity and efficiency. Additionally, innovations in ionic conductivity and electrolyte stability are critical for improving battery performance. As electric vehicles and renewable energy storage systems become more widespread, the need for electrolytes that can withstand extreme temperature variations, charge/discharge cycles, and maintain performance over time will increase. The development of new electrolyte formulations, including those with improved conductivity and compatibility with new cathode and anode materials, will be key to driving growth in this segment. Moreover, regulatory standards for battery safety and sustainability are pushing manufacturers to invest in next-generation electrolyte materials that meet these stricter requirements.

Based on material, lead-acid is segmented into cathode, anode, electrolyte, separator, and others.

In the global lead-acid segment, the growth of cathode materials is primarily driven by advancements in battery performance and recycling technologies. Traditionally, lead is the primary material used in the cathode of lead-acid batteries, and its reliability in providing high surge currents and tolerance to extreme conditions has been a key factor in its continued use. Despite the rise of alternatives like lithium-ion, lead-acid batteries remain widely adopted in applications such as automotive, uninterruptible power supplies (UPS), and backup systems due to their cost-effectiveness and long-established infrastructure. Furthermore, improvements in the efficiency of lead-acid battery recycling have bolstered the demand for lead, as the majority of lead in these batteries can be recovered and reused. This closed-loop recycling process, which is particularly prominent in regions like Europe and North America, reduces the need for raw material mining and addresses environmental concerns, driving sustained growth in the cathode materials segment.

The growth of anode materials is driven by innovations aimed at improving battery performance in automotive applications. In lead-acid batteries, the anode is typically made of a grid structure that contains lead, contributing to the battery's ability to provide reliable power. The growing demand for lead-acid batteries in hybrid vehicles and micro-hybrid systems, which use start-stop technology, has increased the demand for high-performance anode materials that can withstand frequent charging and discharging cycles. In addition, the automotive sector's transition toward more energy-efficient and low-emission vehicles further supports growth, as lead-acid batteries remain an affordable option for smaller vehicles and specific applications.

By Application

To know how our report can help streamline your business, Speak to Analyst

Consumer Electronics Segment Held Largest Share Owing to High Product Demand

Based on its application, lithium-ion is segmented into consumer electronics, automotive, industrial, and other industries.

The consumer electronics segment accounted for the leading market share in 2024, drives the growth of lithium-ion batteries, fueled by the increasing demand for portable devices such as smartphones, laptops, tablets, wearables, and gaming consoles. Li-ion batteries are favored in this segment due to their high energy density, lightweight properties, and ability to provide long-lasting power in compact devices. As consumers increasingly rely on mobile and connected devices for work, entertainment, and communication, the demand for efficient, reliable, and rechargeable batteries continues to rise. Moreover, continuous advancements in battery technology, such as the development of fast-charging solutions and improved safety features, further bolster the adoption of Li-ion batteries in consumer electronics. Additionally, with global trends leaning toward sustainability, manufacturers are increasingly focusing on developing eco-friendly batteries, thereby further boosting the growth of lithium-ion batteries in the market.

The automotive industry is a significant growth driver for lithium-ion batteries due to the accelerating adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs). Governments worldwide are setting ambitious targets to phase out internal combustion engine (ICE) vehicles, with the European Union, China, and several other regions leading the way in implementing stricter emissions standards and offering incentives for EV adoption. Li-ion batteries, known for their high energy density and longer lifespan, are the preferred choice for powering electric vehicles due to their ability to store large amounts of energy in relatively small, lightweight packages. Furthermore, innovations in solid-state and high-capacity Li-ion batteries, along with the development of faster-charging infrastructure, are expected to further propel the demand for lithium-ion batteries in the automotive segment.

Based on the application, lead-acid is segmented into automotive, industrial, and others.

The automotive segment in lead-acid batteries is witnessing significant growth driven by the critical role they play in traditional internal combustion engine vehicles and hybrid vehicles. Lead-acid batteries are primarily used for starting, lighting, and ignition functions, where their ability to provide high surge currents makes them an ideal choice. Despite the growing adoption of electric vehicles (EVs), lead-acid batteries continue to be a cost-effective and reliable power source for conventional vehicles, particularly in emerging markets where affordability remains a key concern. Moreover, the proliferation of micro-hybrid vehicles, which incorporate start-stop technology to enhance fuel efficiency, further drives demand for advanced lead-acid batteries such as enhanced flooded batteries and absorbent glass mat batteries. These batteries offer superior performance, durability, and energy efficiency, making them ideal for modern automotive applications. In addition, the expansion of the global automotive market, particularly in developing economies, is fueling the demand for lead-acid batteries as the backbone of traditional vehicle power systems. The recycling infrastructure for lead-acid batteries, which is well-established globally, ensures a sustainable supply chain, offering long-term viability and environmental benefits, thus supporting continued growth in the automotive segment.

The industrial segment drives the growth of lead-acid batteries in backup power and energy storage applications. Lead-acid batteries are widely used in uninterruptible power supplies (UPS), where they provide reliable, cost-effective backup power to critical infrastructure such as data centers, telecommunications systems, and healthcare facilities. As businesses increasingly rely on digital platforms and cloud computing, the demand for uninterrupted power supply systems continues to grow, ensuring consistent demand for lead-acid batteries in this segment.

BATTERY MATERIALS MARKET REGIONAL OUTLOOK

Based on region, the market is studied across North America, Europe, Asia Pacific, South America, and Middle East & Africa.

North America

North America Battery Materials Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America accounted for the leading market share in 2024 and was valued at USD 21.03 billion. The growth is mainly driven by the strong demand for electric vehicles (EVs) and the increasing adoption of renewable energy sources. The U.S., in particular, is home to leading electric vehicle manufacturers like Tesla, and significant investment is being directed towards battery technology. This has led to a surge in demand for materials such as lithium, cobalt, nickel, and graphite. Additionally, the U.S. government has implemented policies and incentives to boost domestic production of battery materials, ensuring a stable supply chain. Canada, with its rich deposits of lithium, nickel, and other critical minerals, plays a crucial role in supplying raw materials for the North American market. This region's advancements in battery recycling and innovation in solid-state battery technology further cement its position as a key player in the industry.

Asia Pacific

The Asia Pacific region is set to emerge as the fastest-growing market over the forecast period. China is a global leader in the production of both electric vehicles and batteries. China's dominance in battery manufacturing has significantly influenced the demand for battery materials. The country has invested heavily in securing the supply of key raw materials such as lithium, cobalt, and nickel through mining operations and international partnerships. South Korea and Japan are also major players, with companies like Hitachi, Ltd., LG Chem, Samsung SDI, and Panasonic being key contributors to the global battery supply chain. The rapid expansion of EV sales and renewable energy adoption in this region continues to fuel demand for battery materials. Furthermore, the push for energy storage solutions to support renewable energy integration is likely to drive long-term growth in the market.

Europe

The European region is expected to grow and will showcase substantial battery materials market growth during the forecast period. The European Union (EU) has set ambitious targets for EV adoption, including a ban on the sale of new internal combustion engine vehicles by 2035. This shift is driving an increased demand for lithium-ion batteries, which require key materials such as lithium, cobalt, and nickel. European countries like Germany and France are at the forefront, with major automotive companies such as Volkswagen and Renault scaling up their electric vehicle production. The EU has also focused on securing a steady supply of battery materials by establishing partnerships with mining companies and focusing on recycling efforts. The region's commitment to reducing dependence on non-EU sources for critical minerals is expected to drive growth in the market in the coming years.

Latin America

Latin America is expected to have steady market growth due to its vast mineral resources. Countries like Chile, Argentina, and Bolivia make up the "Lithium Triangle," which holds more than half of the world's lithium reserves. This region is central to the supply chain of lithium, a critical material for battery production, especially in electric vehicles. The global shift towards cleaner energy and the rising demand for electric vehicles present significant opportunities for Latin American countries to expand their role in the global market. Increasing investment in sustainable mining practices and refining technologies is expected to enhance the region's position in the global market.

Middle East & Africa

The Middle East and Africa market is growing steadily. The region's involvement is primarily related to the mining and extraction of critical minerals such as cobalt, lithium, and nickel. Countries like Morocco and South Africa are witnessing growing interest from international investors in their mining industries. Additionally, there is an increasing focus on diversifying the economies in this region, which may lead to further development of battery material extraction capabilities.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Increasing Investment for Facility Expansion by Major Companies to Boost Market Share

NICHIA CORPORATION, NEI Corporation, Tokyo Chemical Industry Co. Ltd, Mitsubishi Chemical Corporation, and Hitachi Energy Ltd. are the most prominent players in the market. The key strategies major companies adopt include new product launches to increase their regional presence and improve their portfolio. Most manufacturing companies, battery makers, and various research institutions are investing heavily in the technological advancements of these batteries, which will create batteries with a long life cycle, high power density, environment-friendly performance, and low cost.

LIST OF KEY BATTERY MATERIALS PLAYERS PROFILED IN THE REPORT

- NICHIA CORPORATION (Japan)

- NEI Corporation (K.)

- Tokyo Chemical Industry Co Ltd (Japan)

- Mitsubishi Chemical Corporation (Japan)

- Hitachi Energy Ltd. (Switzerland)

- TORAY INDUSTRIES, INC. (Japan)

- Shanghai Shanshan Technology Co., Ltd. (China)

- Kureha Corporation (Japan)

- BASF SE (Germany)

- Asahi Kasei Corporation (Japan)

- Umicore Cobalt & Specialty Materials (CSM) (Belgium)

KEY INDUSTRY DEVELOPMENTS

- December 2024- China's Contemporary Amperex Technology Co. Limited (CATL), the world's largest battery maker, is offering financial support to its suppliers to accelerate technology innovation in battery materials and equipment. This initiative aims to alleviate stress on its supply chain amid a severe EV price war.

- June 2024—Asahi Kasei has achieved proof of concept (POC) of lithium-ion batteries (LIBs) with the use of its proprietary high-ionic conductive electrolyte. This technology will help the company improve durability at high temperatures and increase power output even at low temperatures, both pressing issues of current LIBs. Furthermore, this technology can contribute to lower cost and smaller size of battery packs, further raising the energy density.

- April 2024- BASF started operating its prototype metal refinery for battery recycling in Schwarzheide, Germany. This facility will help in the development optimization of innovative battery recycling technology, operational procedures, and processing of end-of-life lithium-ion batteries and battery production scrap.

- January 2024- Umicore and Microsoft agreed to utilize artificial intelligence (AI) as a means to accelerate and facilitate its research in battery material technologies for electric vehicles. With this development, the company would create a tailored AI environment that would synthesize, analyze, and bring together decades of complex and vast data from Umicore's proprietary battery materials research and development.

- December 2023- Europe is focusing on enhancing its battery recycling capabilities to reduce dependence on imported materials and promote sustainability. The EU Battery Regulation mandates that by 2031, industrial batteries must incorporate minimum recycled shares of lithium, nickel, and cobalt.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, types, materials, and product applications. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Unit |

Value (USD Billion) and Volume (Kiloton) |

|

Growth Rate |

CAGR of 16.1% from 2025 to 2032 |

|

Segmentation |

By Type, By Materials, By Application, By Region |

|

By Type |

· Lithium-Ion · Lead Acid · Nickel Metal Hydride Battery · Solid-State Battery · Others |

|

By Materials |

· Lithium-Ion o Cathode § Lithium Cobalt Oxide (LCO) § Lithium Nickel Manganese Oxide (NMC) § Lithium Nickel Cobalt Aluminium Oxide (NCA) § Lithium Manganese Oxide (LMO) § Lithium Iron Phosphate (LFP) o Anode § Artificial Graphite § Natural Graphite § Others o Electrolyte o Separator o Others · Lead Acid o Cathode o Anode o Electrolyte o Separator o Others |

|

By Application |

· Lithium-Ion o Consumer Electronics o Automotive o Industrial o Others · Lead Acid o Automotive o Industrial o Others |

|

By Region |

· North America (By Type, By Materials, By Application, By Country) o U.S. o Canada · Europe (By Type, By Materials, By Application, By Country) o Germany o U.K. o France o Italy o Rest of Europe · Asia Pacific (By Type, By Materials, By Application, By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · South America (By Type, By Materials, By Application, By Country) o Brazil o Mexico o Rest of South America · Middle East & Africa (By Type, By Materials, By Application, By Country) o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 61.63 billion in 2024 and is projected to reach USD 201.82 billion by 2032.

Recording a CAGR of 16.1%, the market is slated to exhibit rapid growth during the forecast period.

The lithium-ion segment leads the market.

The rising demand for electric vehicles is a key factor driving the market growth.

The rise in per-capita disposable income, along with an increase in the production of electric vehicles, shall drive the adoption.

North America dominated the market in 2024.

NICHIA CORPORATION, NEI Corporation, Tokyo Chemical Industry Co. Ltd, Mitsubishi Chemical Corporation, and Hitachi Energy Ltd. are the top players in the market.

- 2019-2032

- 2024

- 2019-2023

- 287

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us