Polyester Polyols Market Size, Share & Industry Analysis, By Source (Petroleum-based and Bio-based), By Application (Consumer Goods, Electronics, Pharmaceuticals and Others), and Regional Forecast, 2026-2034

POLYESTER POLYOLS MARKET SIZE AND FUTURE OUTLOOK

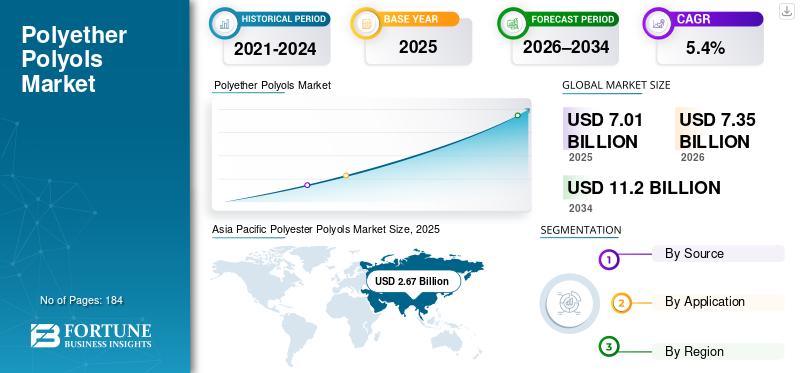

The global polyester polyols market size was valued at USD 7.01 billion in 2025. The market is projected to grow from USD 7.35 billion in 2026 to USD 11.20 billion by 2034 at a CAGR of 5.4% during the 2026-2034 forecast period. Asia Pacific dominated the polyester polyols market with a market share of 38.08% in 2025.

Polyester polyols are hydroxyl-terminated polyesters typically synthesized from diacids/anhydrides and diols/triols, and used as core building blocks in Polyurethane (PU) chemistries. They are selected when formulators need strong mechanical performance, chemical resistance, and durability in applications such as rigid PU insulation foams, CASE (coatings, adhesives, sealants, elastomers), and select flexible foam/elastomer systems.

The market growth is structurally tied to building energy-efficiency and insulation penetration, PU use in industrial coatings and adhesives under VOC and performance requirements, and sustainability-led shifts toward bio-attributed/bio-based or circular feedstocks enabled via certification and mass-balance bookkeeping.

BASF SE, Covestro AG, Dow Inc., Huntsman Corporation, Stepan Company, and COIM Group are the key players operating in the market.

Download Free sample to learn more about this report.

Polyester Polyols Market Key Takeaways

- 2025 Market Size: USD 7.01 billion

- 2026 Market Size: USD 7.35 billion

- 2034 Forecast Market Size: USD 11.20 billion

- CAGR: 5.4% from 2026-2034

- Asia Pacific dominated the polyester polyols market with a 38.08% share in 2025.

- The petroleum-based segment accounted for the dominant market share.

- The consumer goods segment is expected to dominate the market during the forecast period.

North America

North America represents a high-value market, supported by mature CASE demand and the expansion of certified circular and biocircular offerings.

Asia Pacific

Asia Pacific accounted for the largest market share in 2025, driven by strong demand from the construction, automotive, and industrial sectors.

Europe

Europe is supported by stringent energy efficiency regulations in buildings and VOC controls in coatings, driving demand for polyester polyols.

U.S.

The U.S. market was valued at USD 1.23 billion in 2025, accounting for approximately 17.5% of global market sales.

Japan

Japan is expected to witness steady growth, supported by increasing demand from automotive and industrial applications.

Read More

POLYESTER POLYOLS MARKET TRENDS

Performance-focused Differentiation in CASE and Low-VOC Coating Systems is Emerging Market Trend

A key trend reshaping the market is continued product differentiation in CASE markets, especially in industrial/maintenance coatings and adhesives, where performance targets (chemical resistance, hardness, flexibility, hydrolysis resistance) and evolving VOC constraints drive resin/binder choices. Covestro positions Desmophen (including polyester polyols) as versatile PU building blocks for coatings, adhesives and foams, reflecting how suppliers market polyester polyols as tunable performance levers rather than commodity inputs.

Regulatory pressure on solvent emissions further supports this trend. The EU “Decopaint” Directive (2004/42/EC) limits VOC emissions from certain paints/varnishes and refinishing products, which continues to push formulators toward lower-VOC solutions (e.g., higher-solids, 2K PU systems, and other compliance-friendly architectures). Polyester polyols that enable target viscosity/reactivity windows and final film properties that remain central to these coating system optimizations.

MARKET DYNAMICS

MARKET DRIVERS

Building Energy-Efficiency Push Strengthens Rigid PU Insulation Demand

The strongest volume anchor for polyester polyols is rigid PU and PIR insulation, where the polyols are widely used to engineer foam performance (thermal insulation, mechanical strength, and processing behavior). COIM explicitly positions its ISOEXTER polyester polyols for rigid polyurethane insulating foams, demonstrating their alignment with insulation-led PU demand.

Policy and energy-system fundamentals reinforce this driver. Buildings remain a major global energy-demand center, and heating/cooling efficiency improvements keep insulation among the most scalable levers to reduce operating energy use. In the EU, the recast Energy Performance of Buildings Directive (Directive (EU) 2024/1275) is designed to accelerate renovations and move toward a zero-emission building stock, sustaining demand for high-performance insulation materials used in retrofits and new builds. These factors collectively drive the polyester polyols market growht.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Feedstock and Cost Volatility (Petro-Intermediates and Energy) Compress Margins

Most conventional polyester polyols remain tied to petrochemical chains (diacids/anhydrides and glycols), which means producers and downstream PU formulators can face cost swings when upstream energy and chemical markets tighten. This becomes a practical restraint in price-sensitive foam and adhesive systems, where reformulation flexibility is limited by performance constraints (viscosity, reactivity, hydrolysis resistance, fire performance) and qualification cycles.

Similarly, compliance and sustainability requirements can increase “cost-to-serve” (certification, chain-of-custody documentation, PCF reporting, segregation/mass-balance bookkeeping), especially when customers demand verified claims (bio-circular or circular attribution). Mass-balance systems such as ISCC PLUS explicitly formalize traceability/accounting to substantiate these claims, which are valuable but not cost-free, leading to uneven adoption across regions and end uses.

MARKET OPPORTUNITIES

Bio-based / Circular Polyester Polyols Scale Through Certification and Capacity Additions

A clear opportunity is the “upgrade” cycle from purely fossil-based polyols to renewable, bio-attributed, or circular alternatives without forcing customers to redesign PU systems from scratch. Multiple major producers now point to certification-enabled approaches as a scalable bridge, with Covestro describes using ISCC PLUS certification to provide a verifiable method for attributing alternative materials via mass balance.

This opportunity is increasingly backed by tangible investments. COIM’s 2025 New Boston (Texas) acquisition included a renewable polyol product line (based principally on cashew nutshell liquid) and plans to add 100 million lbs of capacity for additional product lines by mid-2027, an indicator that suppliers expect sustained customer pull for lower-carbon polyols.

MARKET CHALLENGES

Qualification Cycles and Risk Management Across Safety/Regulatory and Sustainability Claims

A recurring challenge is that polyurethane systems are highly application-specific, and changes in polyol backbone (molecular weight distribution, functionality, aromatic/aliphatic balance, renewable attribution) can trigger extensive requalification. This slows substitution, particularly in regulated or high-liability end uses (construction products with fire codes, appliance insulation, industrial coatings).

At the same time, sustainability claims are under higher scrutiny. Suppliers can support customers with certified approaches (e.g., ISCC PLUS mass-balance chain-of-custody and product-level statements). However, downstream users still need alignment across documentation, audit readiness and customer communication. Covestro explicitly frames ISCC PLUS-based mass balance as a credibility mechanism, highlighting that the challenge is not only technical performance, but also defensible verification.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

U.S. Tariffs Influence the Chemical Imports and Leads to Surging Raw Mateirals Cost

U.S. tariffs in 2025, building on Section 301 duties, target chemical imports, including polyols and feedstocks from China and India, and surging raw material costs for U.S. manufacturers. This squeezes margins, prompts alternative sourcing from Southeast Asia or Europe, and passes higher prices to downstream sectors such as construction and furniture. China counters by redirecting exports to India, the Middle East and Europe amid declining shipments to the U.S.

Tensions such as U.S.-China trade wars and conflicts (Russia-Ukraine, Middle East) exacerbate supply disruptions, pushing friendshoring to allied nations for resilience. Asia Pacific, led by China and India, holds a major market share but sees volatility from tariffs and anti-dumping duties.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Developers produce bio-based polyester polyols from vegetable oils, coconut monoglycerides, biosuccinic acid and recycled PET, thereby reducing carbon footprints and replacing fossil fuels. Advances include closed-loop recycling of polyurethanes into high-purity monomers for new polyols that meet commercial specs. Vegetable oil polyols enable energy-saving polyurethane foams with degradability and low emissions.

Hyperbranched structures enhance the unique properties of polyurethane coatings, while specialty grades optimize molecular weight and functionality for rigid foams. Coconut-derived polyols enhance the tensile/compressive strength of flexible foams through microphase separation and an open-cell morphology. Tailored formulations enhance compatibility with blowing agents, cell structure and adhesion for faster production lines.

SEGMENTATION ANALYSIS

By Source

Petroleum-based Segment Dominates Due to Established Petrochemical Feedstock Integration and Cost Performance Predictability

Based on source, the market is segmented into petroleum-based and bio-based.

Among these, the petroleum-based segment has a dominant market share. Petroleum-based are produced on mature, high-volume value chains tied to conventional diacids/anhydrides and glycols, and they deliver highly repeatable performance across rigid foams and CASE formulations. For large PU consumers, the biggest advantage is qualification stability where predictable viscosity, hydroxyl value, functionality and reactivity windows allow formulators to maintain foam-processing performance and end-product compliance without frequent requalification cycles. This low switching friction supports sustained petroleum-based dominance, especially in construction insulation and appliance foams, where formulation drift is costly and regulatory testing cycles can be long.

Bio-based/circular polyester polyols are the fastest-growing subsegment as customers scale verified low-carbon inputs without sacrificing PU performance. Bio-based and circular adoption is being accelerated by certification-enabled substitution and recycled-content polyester polyols made from circular feedstocks, such as recycled PET streams.

By Application

To know how our report can help streamline your business, Speak to Analyst

Consumer Goods Leads Due to High Aluminum Intensity and Casting Demand

Based on application, the market is segmented into consumer goods, electronics, pharmaceuticals, and others.

The consumer goods segment is expected to dominate the market during the forecast period. This segment growth is associated with the adoption of polyester-polyol-based polyurethane systems in high-volume, everyday products where durability, abrasion resistance and aesthetics are considered, especially in PU coatings, adhesives, sealants, elastomers and foams. Industry bodies describe polyurethane’s broad role across flexible/rigid foams and CASE applications that enhance product appearance and lifespan, directly aligning with consumer goods (furniture/cushioning, footwear components, protective coatings for plastics/wood, and durable adhesives).

The electronics segment is expected to register significant growth during the forecast period. Electronics demand is underpinned by the need for protective polymer systems, including coatings and adhesive/sealant chemistries, to shield sensitive components from moisture, vibration and chemical exposure. Covestro positions its Desmophen portfolio (including polyester polyols) as PU building blocks for coatings, adhesives and many other applications, reflecting how suppliers directly target electronics-grade protective and bonding systems.

The pharmaceuticals segment is experiencing strong market growth. In the pharmaceutical industry, polyester polyols are typically incorporated into polyurethane biomaterials and medical-grade PU systems. The scientific literature on polyurethane biomaterials highlights the role of polyester polyols/macroglycols in PU architectures and their relevance to degradation behavior and performance in biomedical contexts.

Others segment consists of construction-related and industrial end uses, where polyester-polyol-based PU systems are used in protective coatings, industrial adhesives/sealants, elastomers and certain foam systems.

POLYESTER POLYOLS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Polyester Polyols Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading polyester polyols market share in 2025. The growth is due to the concentration of downstream PU manufacturing and regional product capacity expansion. The region benefits from large-scale manufacturing ecosystems (consumer goods and electronics production, and industrial coatings/adhesives demand) and visible capacity expansions. In October 2020, A concrete example is Huntsman’s start-up of a 22,000-ton TEROL aromatic polyester polyols plant in Kuan Yin, Taiwan, explicitly aimed at expanding downstream polyurethanes capabilities in Asia Pacific.

China Polyester Polyols Market

China’s market is one of the largest worldwide, with 2025 revenue at USD 1.19 Billion, representing 16.9% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a high-value market, supported by mature CASE demand and the scaling of certified circular/biocircular offerings. A key enabler is certification and chain-of-custody infrastructure that helps customers adopt lower-carbon inputs without redesigning formulations.

U.S. Polyester Polyols Market

In 2025, the U.S. represented a USD 1.23 billion market in North America, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 17.5% of global market sales.

Europe

Europe’s market is shaped by strong regulatory pull on energy efficiency in buildings and on VOC controls in coatings, supporting other sectors (construction/industrial) and higher-value CASE consumption. The EU’s Energy Performance of Buildings Directive (EU) 2024/1275 reinforces renovation and performance upgrades across the building stock, thereby indirectly supporting polyurethane insulation and demand for building materials.

Germany Polyester Polyols Market

The Germany market in 2025 was valued at USD 0.56 billion, representing roughly 8.0% of global market revenues.

U.K. Polyester Polyols Market

The U.K. market in 2025 reached USD 0.16 billion, representing roughly 2.3% of global market revenues.

Latin America

Latin America remains smaller but growing, supported by gradual expansion in consumer goods manufacturing, electronics assembly in select hubs as well as demand for industrial coatings and adhesives tied to infrastructure as well as maintenance. This regional rowth is also driven by practical industrialization trends, increasing use of durable protective coatings and bonded assemblies applications, where PU systems remain relevant.

Middle East & Africa

The Middle East & Africa shows targeted growth linked to construction activity, industrial projects, and demand for protective coatings, with market size influenced by local PU systems capacity and reliance on imported intermediates. The region’s growth is typically project-led, but durable coatings and adhesives, as well as industrial applications, create a steady pull for PU building blocks in priority sectors.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Major investments are underway in the market as manufacturers respond to rising sustainability expectations and higher performance requirements across end-use industries. Leading producers, such as BASF SE, Covestro AG, Dow Inc., Huntsman Corporation, Stepan Company, and COIM Group, are directing capital toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices. Innovation efforts are increasingly focused on enhancing purity consistency, reducing the environmental footprint, and developing sources suitable for advanced products.

LIST OF KEY POLYESTER POLYOLS COMPANIES PROFILED

- BASF SE (Germany)

- Covestro AG (Germany)

- Dow Inc. (U.S.)

- Huntsman Corporation (U.S.)

- Stepan Company (U.S.)

- COIM Group (Italy)

- Cargill (U.S.)

- UBE Corporation (Japan)

- LANXESS (Germany)

- Tosoh Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- May 2025: COIM USA announced the acquisition of a 20-acre property from Palmer International, highlighting that the site includes a new renewable polyol product line based principally on cashew nutshell liquid (CNSL) and will complement COIM’s existing Isoexter polyester polyols portfolio. The company also communicated a plan to add ~100 million lbs of capacity by mid-2027, signaling an investment cycle tied to sustainable feedstocks and portfolio expansion for polyurethane value chains.

- March 2025: BASF announced the introduction of biomass balance grades for its Elastoflex polyurethane systems, reflecting continued scaling of mass-balanced approaches in PU value chains

- January 2024: Dow announced it had received ISCC PLUS certification for its PO/PG and Polyols manufacturing site, positioning the certification as an enabler for decoupling from fossil feedstocks through waste-sourced feedstocks and audited chain-of-custody practices. For market positioning, this development supports faster customer adoption of verified circular/biocircular raw materials (especially in downstream PU systems where procurement increasingly requires auditable sustainability claims).

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, Source, and Application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.4% from 2026 to 2034 |

|

Segmentation |

By Source, By Application, By Region |

|

By Source |

· Petroleum-based · Bio-based |

|

By Application |

· Consumer Goods · Electronics · Pharmaceuticals · Others |

|

By Region |

· North America (By Source, By Application, By Country) o U.S. (By Application) o Canada (By Application) · Europe (By Source, By Application, By Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Source, By Application, By Country) o China (By Application) o India (By Application) o Japan (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Source, By Application, By Country) o Mexico (By Application) o Brazil (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Source, By Application, By Country) o GCC (By Application) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 7.01 Billion in 2025 and is projected to reach USD 11.20 Billion by 2034.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The consumer goods segment led in 2025.

Asia Pacific held the highest market share in 2025.

Building energy-efficiency push drives the market growth.

- 2021-2034

- 2025

- 2021-2024

- 184

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us