Satellite Launch Vehicle Market Size, Share & Industry Analysis, By Vehicle Technology (Convectional Vehicle and Reusable Launch Vehicle), By Orbit Type (GEO, LEO, and MEO), By Component (Propulsion System, Guidance and Control System, Structure, Avionics, Payload, and Others), By Payload Capacity (Less Than 1000 Kg, 1000 Kg to 2500 Kg, and More Than 2500 Kg), By End User (Commercial, Military, and Civil & Government) and Regional Forecasts, 2026-2034

Satellite Launch Vehicle Market Size and Industry Overview

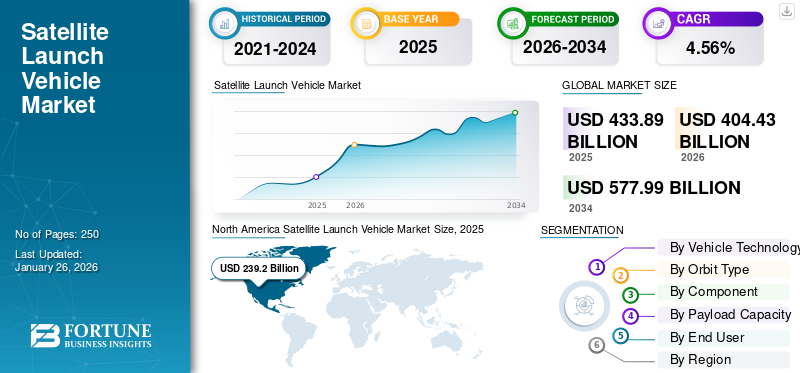

The global satellite launch vehicle market size was valued at USD 433.89 billion in 2025 and is projected to grow from USD 404.43 billion in 2026 to USD 577.99 billion by 2034, exhibiting a CAGR of 4.56% during the forecast period. North America dominated the satellite launch vehicle market with a market share of 55.13% in 2025.

The global satellite launch vehicle market is expected to experience considerable growth in the coming years, driven by a mix of technological innovations, modernization of platforms, digital transformation, and solutions for commercial as well as military applications. For instance, in November 2024, Boeing sent two more O3b mPOWER satellites to SES. The 7th and 8th satellites in the constellation are on their way to Cape Canaveral for a scheduled launch in December. These satellites are equipped with software-controlled integrated payload array technology, enabling SES to flexibly distribute bandwidth and power to particular areas or clients according to demand.

SpaceX, United Launch Alliance, Indian Space Research Organization (ISRO), NASA, China Aerospace Science and Technology Corporation (CASC), and Maxar Technologies are ranked highest due to various factors such as the increasing number of satellite operators and launches, growing manufacturing technologies, and others.

As global challenges become more complex, the necessity for a broader and more robust launch vehicle infrastructure has emerged. This demands a diverse and readily accessible source of launch vehicle manufacturers. The production of rockets is on the rise due to their essential roles in satellite launches in space for various aspects of daily life on Earth, including communication, navigation, weather forecasting, military applications, Earth Observation, and others. The increasing launch of satellites directly impacted the demand for new advanced launch vehicles. Thus, the global satellite launch vehicle market share is significantly growing.

Download Free sample to learn more about this report.

Satellite Launch Vehicle Market Key Takeaways

- 2025 Market Size: USD 433.89 billion

- 2026 Market Size: USD 404.43 billion

- 2034 Forecast Market Size: USD 577.99 billion

- CAGR: 4.56% from 2026-2034

- North America dominated the satellite launch vehicle market with a 55.13% share in 2025.

- The reusable launch vehicle segment is expected to account for a 54.63% share in 2026.

- The LEO segment is projected to hold a 67.17% share in 2026.

North America

North America accounted for USD 239.20 billion in 2025 and is projected to reach USD 222.11 billion in 2026.

Asia Pacific

Asia Pacific reached USD 55.15 billion in 2025 and is projected to attain USD 52.01 billion in 2026.

Europe

Europe accounted for USD 113.03 billion in 2025 and is expected to reach USD 105.88 billion in 2026.

U.S.

The satellite launch vehicle market is projected to reach USD 183.95 billion by 2026.

Japan

The satellite launch vehicle market is projected to reach USD 8.09 billion by 2026.

Read More

SPACE EXPENDITURE

Rising Number of Satellite Launches into Orbit and Increasing Investment in Space by Emerging Nations Are Contributing Significantly to Market's Growth

Various interrelated elements are driving the increase in worldwide expenditure on space, such as technological advancements, heightened private investment, and a deeper comprehension of space's strategic importance. The growth is propelled by satellite and rocket technology developments, enhancing communication, navigation, and Earth observation functions. Furthermore, the rising reliance on space-dependent technologies in areas such as retail and disaster response is another factor contributing to this expansion.

For instance, in 2023, according to a Space Foundation organization report, the global space budget reached USD 570 billion in 2023, reflecting a 7.4% growth from the adjusted figure of USD 531 billion in 2022. This growth corresponds to the industry's five-year Compound Annual Growth Rate (CAGR) of 7.3% and is nearly double the size of the space economy from ten years ago.

The cost of launching satellites into space has decreased by nearly a factor of ten over the past two decades, enabling both governmental and private entities to engage more easily in space endeavors. Furthermore, there has been a remarkable rise in private investment within the space sector.

Moreover, a greater number of countries are venturing into space, leading to a more diverse investment landscape. Nations such as Luxembourg and Australia have launched ambitious space initiatives, and developing economies are also beginning to allocate resources for space research and development.

To know how our report can help streamline your business, Speak to Analyst

Market Dynamics

Market Drivers

Technological Advancements, Increasing Demand for Satellite Launches, and Evolving Market Dynamics Poised for Significant Market Growth

The increasing demand for satellites used in communication, earth observation, and scientific research serves as a major catalyst. As small satellites such as CubeSats become more popular, there is an upsurge in the need for specialized launch services designed specifically for these lighter payloads. Further, the growing commercial space initiatives by private entities such as SpaceX, Rocket Lab, and others are broadening their activities, providing creative and affordable launch options that serve both commercial and governmental requirements, driving the gloabl satellite launch vehicle market growth.

Moreover, companies that invest in advanced material analysis and innovative manufacturing processes can differentiate themselves in a competitive market. The ability to produce high-performance satellites quickly and cost-effectively positions these companies favorably against competitors who rely on traditional methods. Numerous rocket manufacturers are turning to modern manufacturing techniques to enhance efficiency and cut expenses. This involves contracting production to take advantage of reduced labor costs and specialized skills.

For instance, in September 2024, Eutelsat Group and Mitsubishi Heavy Industries Ltd. announced signing a new contract for several launches. According to the agreement, MHI will conduct multiple launches using its H3 launch vehicle starting in 2027. The H3 Launch Vehicle draws upon the proven history of the dependable H-IIA and H-IIB, aiming to provide improved customer support and meet a wider array of launch needs.

Additionally, substantial investments from government organizations in space exploration and satellite launch vehicle technologies are anticipated to improve the effectiveness of national launch services. For instance, in recent years, funding declarations from nations such as India and South Korea have underscored the increasing dedication to space programs.

Market Restraints

High Initial Development Cost and Risk of Failure Impede Market Growth

Creating satellite launch vehicles, especially those that are reusable, demands a considerable initial investment in research, development, and technology. This significant capital need can discourage new players and restrict competition in the industry. The expenses tied to the refurbishment and upkeep of reusable rockets between launches can be quite high. Making certain that these vehicles are safe and functional for several missions presents intricate engineering hurdles and demands considerable resources.

Ensuring that spacecraft can handle multiple launches while adhering to safety regulations presents persistent technical challenges that demand creative solutions and thorough testing. In addition, the dependability of launch vehicles is essential; failures can lead to the loss of payloads and threaten safety on the ground. Past incidents underscore the necessity for ongoing advancements in safety measures and technology.

Market Opportunities

Several Key Areas of Advancements and Innovations in Launch Vehicle System Industry Poised for Significant Growth

Artificial Intelligence (AI) Applications – AI technologies can analyze vast datasets from satellites, enabling better decision-making and operational efficiency. This includes automating satellite operations, optimizing navigation, and managing space debris, which can significantly reduce operational costs and risks. Moreover, AI-driven systems can improve mission planning by predicting environmental conditions and optimizing satellite routes, leading to more successful missions and better resource management.

Integration of 3D Printing – 3D printing technology allows for the production of lightweight, complex components tailored to specific mission requirements. This customization enhances satellite performance while reducing production costs and time, paving the way for more efficient manufacturing processes.

Sustainable Manufacturing Practices - The development of sustainable manufacturing practices, such as recycling materials for 3D printing, is becoming increasingly important. This shift reduces waste and lowers costs associated with raw materials, making satellite manufacturing more environmentally friendly.

Growth of Small Satellite Market - The small satellite market, particularly CubeSats, is expanding rapidly due to their lower launch costs and versatility in applications ranging from Earth observation to scientific research. This trend is creating new opportunities for manufacturers specializing in smaller satellite technologies.

For instance, in November 2024, SpaceX successfully sent 20 additional Starlink internet satellites into orbit from California. A Falcon 9 rocket transported these 20 Starlink satellites, 13 of which feature direct-to-cell technology.

The outlook for the satellite manufacturing sector is promising, with many opportunities arising from innovations in 3D printing, AI technology, eco-friendly practices, and increasing market needs. These elements will improve operational effectiveness and broaden the potential uses of satellites across different industries.

Market Challenges

Challenges Such as Technical and Economic Significant Impact Its Growth and Sustainability

Limited Payload Capacity – Numerous current launch vehicles, such as India's LVM-3, have a reduced payload capacity compared to rivals such as China's Long March 5. This constraint limits the potential to carry out more ambitious missions that demand heavier payloads, making it essential to enhance capabilities and create new vehicles.

Development of Reusable Technologies – Although there is a movement aimed at creating reusable launch vehicles (RLVs) to lower expenses, the engineering difficulties, including the refurbishment of rocket stages and the assurance of safe re-entry, are intricate and expensive. These substantial development and operational expenses impede the wider acceptance of RLVs.

High Development Costs – The upfront investment needed to create new launch vehicles is significant. This encompasses expenses related to research, testing, and compliance with regulations. Budget excesses during the development stages are frequent, which complicates the ability of companies to remain cost-competitive with current expendable rockets.

Technological Advancements – Improvements in satellite technology have increased operational lifetimes and enhanced efficiencies (such as multi-satellite launches), but they also make demand predictions for launch vehicles more complex. Operators favor satellites with extended lifespans, which can result in a lower number of launches than expected.

Supply-Demand Imbalance – There is a significant gap between supply and demand in the satellite launch industry. For instance, ISRO's existing launch capabilities greatly surpass domestic requirements, raising worries about potential overcapacity. The shift from a supply-focused approach to one driven by demand has not completely come to fruition, leading to an abundance of launch vehicles without a matching number of satellite launches.

Satellite Launch Vehicle Market Trends

Advancements in Engineering and Increasing Need for Cost-Effective Solutions Drives Market Growth

Advanced Propulsion Technologies – In recent times, the approach to space exploration has moved toward sustainability, prompting the creation of environmentally friendly substitutes for conventional rocket fuels. A significant area experiencing groundbreaking advancements is the creation of green propellants for future launch vehicles and spacecraft.

A move is being made toward eco-friendly propellants that minimize the environmental effects of launches. This development corresponds with worldwide sustainability objectives and regulatory demands.

For instance, in January 2024, Bengaluru-based Bellatrix Aerospace successfully validated its advanced Rudra and Arka propulsion systems for operation in space-sensitive environments. The Rudra green propulsion system signifies a groundbreaking transition from conventional toxic propellants such as hydrazine to a high-performance, non-toxic substitute.

Integration of AI and Automation – The integration of artificial intelligence into launch systems is improving both operational efficiency and reliability. AI can refine flight trajectories, oversee payload integration, and enhance mission planning.

- North America witnessed satellite launch vehicle market growth from USD 104 Billion in 2023 to USD 145.83 Billion in 2024.

For instance, in September 2024, Los Angeles-based startup Proteus Space aims to launch the first AI-designed ESPA-class satellite in 2025. This satellite, which will operate in low-Earth orbit (LEO), is expected to carry four separate payloads.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Vehicle Technology

Development and Advancement of Reusable Launch Vehicle Technology to Boost Segmental Growth

Based on vehicle technology, the market is segmented into convectional vehicle and reusable launch vehicle.

The reusable launch vehicle sub-segment is estimated to be the fastest-growing segment during the forecast period with a share of 54.63% in 2026. The development of reusable launch vehicle (RLV) technology is a game-changer in the satellite launch industry. By markedly lowering expenses, advancing technological capabilities, boosting mission adaptability, and increasing dependability, RLVs are setting the stage for a new chapter in space exploration and the deployment of commercial satellites. For instance, in September 2024, India is enhancing its space initiatives by approving the development of the Next Generation Launch Vehicle (NGLV) by ISRO. This advanced vehicle aims to be economical, reusable, and able to transport heavier payloads than existing rockets, positioning it as an essential component of India's upcoming space missions.

Convectional vehicle segment acconted for largest market share in 2024 year. The convectional satellite launch vehicle market is poised for substantial growth over the next several years, fueled by technological advancements, rising demand for satellite services across various sectors, and significant government investment in space initiatives.

By Orbit Type

Rising Number of Satellite Launches into Low Earth Orbit (LEO) is Driven by the Advantages of LEO

Based on orbit type, the market is segmented into the market is categorized into GEO, LEO, and MEO.

LEO is estimated to witness the fastest-growing CAGR during the forecast period with a share of 67.17% in 2026. The rise in launching number of satellites into Low Earth Orbit is fueled by the benefits of reduced latency, affordability, flexibility, wide-ranging coverage, and continuous technological progress. With the increasing requirement for rapid connectivity and immediate data across multiple industries, LEO satellites are set to be instrumental in fulfilling these demands while enhancing the overall functionality of satellite communications. For instance, in September 2024, Geespace, a firm supported by the Chinese automobile manufacturer Geely, initiated the launch of a third set of satellites aimed at creating a mega constellation. The ten satellites in Low Earth Orbit (LEO) were deployed from the Taiyuan Satellite Launch Centre.

The GEO segment is estimated to be the second-fastest growing segment during the forecast period. The GEO segment is on a growth trajectory fueled by technological advancements, rising demand for communication services, and substantial government investments. Despite challenges related to costs and regulatory complexities, the segment’s expansion across various applications presents significant opportunities for stakeholders involved in satellite technology development and deployment.

- The GEO segment is expected to hold a 13.39% share in 2024.

Download Free sample to learn more about this report.

By Payload Capacity

Increasing Trend Toward Manufacturing and Launching of Small Satellites Drives Segmental Growth

Based on payload capacity, the market is segmented into less than 1000 kg, 1000 kg to 2500 kg, and more than 2500 kg.

Less than 1000 kg is estimated to witness the fastest-growing CAGR during the forecast period of 2026-2034. Small satellites are being used more frequently in multiple fields, such as military intelligence, communications, earth observation, and scientific research. Their adaptability enables them to assist in a range of applications, including disaster monitoring, environmental observation, and worldwide broadband internet services. For instance, in April 2024, SAIC secured its initial contract with the Pentagon to develop an AI-enhanced small satellite, collaborating with the spacecraft producer GomSpace. The U.S. defense contractor SAIC will utilize its partnership with GomSpace to integrate this small satellite.

1000 Kg to 2500 Kg segment is estimated to be the second fastest growing segment during the forecast period with a share of 44.29%in 2026. The increasing launches of medium size satellites in LEO, GEO, and MEO orbital to boost segment growth.

By Component

Growing Development in Launch Vehicle Propulsion Systems to Overcome Conventional Challenges Catalyze Market Growth

Based on component, the market is segregated into propulsion system, guidance and control system, structure, avionics, payload, and others.

The propulsion system is set to register the fastest-growing CAGR during the forecast period with a share of 44.54%in 2026. The progress in propulsion systems is essential for addressing the conventional difficulties linked to space missions. By moving toward electric and environmentally friendly propulsion methods, improving miniaturization approaches, and utilizing cutting-edge manufacturing practices, the satellite propulsion industry is set for considerable expansion. For instance, in September 2024, The Air Force Research Laboratory granted Benchmark Space Systems USD 4.9 million to create propulsion systems for the ASCENT monopropellant. This two-year grant encompasses the design of Benchmark propulsion systems ranging from 22 newtons to 100 newtons for ASCENT. ASCENT is a non-toxic propellant that the Air Force Research Laboratory developed.

Avionics segment estimated to be the second fastest growing during the forecast period of 2026-2034. The rising complexity of satellite missions necessitates sophisticated avionics systems for precise navigation, control, and communication, driving demand for advanced technologies such as GPS and inertial navigation systems. Moreover, the surge in commercial satellite launches, particularly for communication and Earth observation purposes, is propelling investments in avionics to ensure reliability and performance in increasingly competitive markets

By End User

Military Segment to Grow at a Fastest CAGR due to Satellite Investments Among Defense Users

Based on end user, the market is divided into commercial, military, and civil & government.

The military segment is projected to estimated to be the fastest-growing segment during the forecast period of 2026-2034. A variety of strategic and technological elements are fueling the increasing interest in satellite investments among defense users. These investments are essential for strengthening national security, enhancing operational capabilities, and utilizing advanced technologies. The growth in satellite investments from defense users is a complex trend driven by the demand for improved surveillance, secure communications, accurate navigation, and the advantages offered by technological progress. As countries continue to focus on national security in response to changing threats, the significance of satellites will only grow in shaping contemporary defense strategies. For instance, in March 2024, in the coming years, India plans to invest around USD 3 billion in contract grants associated with space to reduce its dependence on foreign satellites and strengthen its counter-space abilities.

The commercial segment is accounted for the largest market share during the 2025. The rise in satellite launches for the commercial applications by commercial market players propel the segmental growth.

PESTLE Analysis

The PESTLE analysis reveals that the launch vehicle sector is shaped by a complex interaction of political backing, economic feasibility, societal demand for connectivity, technological progress, legal regulations, and environmental factors. Grasping these elements is crucial for stakeholders seeking to navigate this ever-evolving industry successfully.

Political Factors - Raising government investment in space initiatives greatly influences market development. For example, nations such as India and Japan have dedicated significant funds to space exploration and satellite launches, boosting their proficiency in the global satellite launch vehicle system market share. Further, national and international regulations governing space activities can either facilitate or hinder market growth. Compliance with safety standards and launch licensing is crucial for companies operating in this sector.

Economic Factors - The movement toward reusable launch vehicles is reducing expenses, making it cheaper to access space. This financial transformation is drawing in new participants in the market, such as startups and smaller enterprises. An increasing amount of venture capital and private funding is being funneled into the space industry, fostering innovation and the advancement of new technologies.

Social Factors - The rising public enthusiasm for space missions, spurred by media attention and educational programs, is nurturing a favorable atmosphere for investments in satellite technology. The growing demand for worldwide internet connectivity, particularly in areas lacking adequate services, has resulted in a boost for satellite communication solutions, contributing to market expansion.

Technological Factors - Advancements in propulsion technologies, including electric drives and environmentally friendly propellants, are improving the efficiency and sustainability of satellite launches. Further, the shift toward smaller satellites, such as CubeSats and NanoSats, enables more regular launches at reduced expenses, boosting overall market activity. Furthermore, the development of reusable launch vehicle (RLV) technology is revolutionizing the sector by lowering costs and enhancing launch frequency, facilitating the process of placing satellites into orbit.

Legal Factors - Safeguarding innovations via patents is essential for businesses in the satellite launch industry to preserve their competitive edge. Compliance with agreements such as the Outer Space Treaty influences how governments carry out their space missions. Legal regulations surrounding satellite activities need to be adhered to in order to prevent disputes. Companies must manage intricate liability concerns associated with possible damages caused by satellites or launch vehicles during their operations.

Environmental Factors - There is a growing focus on establishing sustainable practices in the industry. This includes lowering the carbon emissions linked to rocket launches and reducing space debris by implementing responsible satellite design. In addition, worries about the environmental consequences of rocket launches on climate change are leading to conversations about regulatory actions to alleviate these impacts. With the rising number of satellites, it is essential to manage space debris effectively. Companies are researching technologies to bring down inactive satellites or shorten their operational lifespans to lessen risks.

Satellite Launch Vehicle Market Regional Outlook

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Satellite Launch Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest share in the global satellite launch vehicle market. The market in North America reached USD 239.2 billion in 2025, representing 55.13% of total market revenue, and is projected to reach USD 222.11 billion in 2026. The region is experiencing a rise in investment within the industry, fueled by technological innovations, growing demand for satellite launches from commercial and private sectors, and substantial defense expenditure. Increased government spending on defense is driving expansion within the defense sector. The U.S. Department of Defense is consistently making significant investments in defense space initiatives, incorporating advanced avionics technology to spur market growth. Furthermore, commercial, private, and government organizations are substantially increasing their financial commitments to space programs in the U.S. For instance, in April 2024, NASA designated USD 2.4 billion in the budget for the Earth Science program to support missions and initiatives that advance Earth systems science and improve the accessibility to the information for mitigating natural hazards, supporting climate action, and managing natural resources. The U.S. market is projected to valued at USD 183.95 billion by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 55.15 billion, representing 12.71% of global demand, and is projected to grow to USD 52.01 billion in 2026. Asia Pacific is estimated to be the fastest-growing region during the forecast period. Countries such as China, India, Japan, and Australia are placing considerable emphasis on investing in the space industry. Governments are acknowledging the strategic significance of space for their national security. Nations such as China, India, and Australia are strengthening their abilities to monitor regional threats without depending on foreign technologies independently. Furthermore, the emergence of private companies in the space sector is becoming prominent, especially in China, India, and Japan, where commercial initiatives are beginning to support government efforts. For instance, in August 2024, India successfully launched its inaugural reusable hybrid rocket, ‘RHUMI 1’, which was created by the Tamil Nadu-based startup Space Zone India in collaboration with Martin Group. The rocket, carrying 3 Cube Satellites and 50 PICO Satellites, ascended into a suborbital trajectory utilizing a mobile launcher. These satellites aim to gather data for research related to global warming and climate change. The Japan market is projected to valued at USD 8.09 billion by 2026, the China market is projected to valued at USD 24.81 billion by 2026, and the India market is projeted to valued at USD 12.23 billion by 2026.

Europe

Europe contributed approximately USD 113.03 billion to the global market in 2025, accounting for 26.05% share, and is expected to reach USD 105.88 billion in 2026. Europe is projected to be the second-fastest growing region during the forecast period. The rising awareness of space technology's significance for economic recovery and resilience has prompted governments and developing nations to boost their investments in this field. Nations such as Germany and France are also raising their financial commitments to space exploration and the advancement of satellite technology. For instance, in November 2024, ESA is extending its commitment to the new generation of commercial-led European launch services through its ‘Boost!’ programme, awarding contract extensions with four companies toward the deployment of their launch services. The UK market is projected to valued at USD 15.27 billion by 2026, and the Germany market is valued at USD 11.46 billion by 2026.

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 20.52 billion in 2025, accounting for 4.73% share, and is expected to reach USD 18.93 billion in 2026. Over the study period, growth in the Middle East & Africa will be moderate. This growth is attributed to the increased focus on space sector development and the launch of ambitious space programs by Israel, Saudi Arabia, the United Arab Emirates, and other countries. For instance, in July 2024, Yahsat chose SpaceX to launch its state-of-the-art geostationary satellites, Al Yah 4 (AY4) and Al Yah 5 (AY5), utilizing SpaceX’s reliable Falcon 9 rocket.

Latin America

The Latin America market accounted for USD 5.99 billion in 2025, representing 1.38% of the global industry, and is expected to reach USD 5.5 billion in 2026. In Latin America, nations mainly focus on space services and equipment associated with space. The market expansion in the region is expected to be driven by an increase in contracts for space launches in Brazil, Argentina, and Colombia. For instance, in November 2024, the Brazilian government entered into agreements with China's National Data Administration and with SpaceSail, a company focused on low-orbit internet satellites that seek to compete with Starlink.

Competitive Landscape

Key Industry Players

Leading Players Focus on Technological Advancements to Enhance Various Applications for Space Missions

The satellite launch vehicle market is characterized by a mix of established aerospace giants and emerging players, each striving to capture market share through innovation, strategic partnerships, and technological advancements. The market is dynamic and evolving rapidly due to technological advancements, increasing demand for satellite services, and intense competition among major players. Companies that leverage innovation, maintain operational efficiency, and adapt to regulatory changes are likely to thrive in this growing sector. As the market continues to expand, collaboration between private enterprises and government agencies will also play a crucial role in shaping future developments within the industry.

For instance, in September 2024, NASA chose eight companies for a new initiative aimed at obtaining Earth observation data and offering related services for the agency. The Commercial SmallSat Data Acquisition Program On-Ramp1 Multiple Award contract is a firm-fixed-price indefinite-delivery/indefinite-quantity multiple-award contract with a total maximum value of USD 476 million shared among all the selected contractors, with a performance period extending until November 15th, 2028.

LIST OF KEY COMPANIES PROFILED:

- Airbus S.A.S (Netherlands)

- Arianespace (France)

- The Boeing Company (U.S.)

- Rocket Lab (U.S.)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Northrop Grumman (U.S.)

- Lockheed Martin Corporation (U.S.)

- Blue Origin Enterprises, L.P. (U.S.)

- SpaceX (U.S.)

- ISRO (India)

KEY INDUSTRY DEVELOPMENTS

November 2024: - Rocket Lab USA, Inc. revealed that it has entered into a multi-launch contract with a private operator of a commercial satellite constellation for its latest medium-lift rocket, Neutron.

November 2024: - The director of Space Transportation Civil Space Programs at ESA, representing ArianeGroup, signed two contract addendums valued at around USD 232.47 million to further the testing of the Prometheus engine and the reusable rocket stage demonstrator, Themis.

September 2024: - CU Aerospace, LLC (CUA), a prominent player in the realm of small satellite propulsion, obtained a significant contract worth USD 3.29 million from the Defense Advanced Research Projects Agency (DARPA).

April 2024: - The European Space Agency (ESA) launched two navigation initiatives, Genesis and low-Earth-orbit positioning, navigation, and timing (LEO-PNT), under its FutureNAV program. ESA allocated contracts worth a total of USD 235.34 million to various European organizations to kick off the development of these missions.

February 2024: - A green propulsion system, created through the Technology Development Fund (TDF) initiative of the Defence Research and Development Organisation (DRDO), has proven its in-orbit capabilities on a payload that was launched during the PSLV C-58 mission.

REPORT COVERAGE

The report provides an in-depth market analysis. It comprises all major aspects, such as R&D capabilities, supply chain management, competitive landscape, and optimization of the manufacturing capabilities and operating services. Moreover, it offers insights into the global satellite launch vehicle market trends, growth analysis, and size and highlights key industry developments. In addition to the above-mentioned factors, it mainly focuses on several factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.56% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Technology, By Orbit Type, By Component, By Payload Capacity, By End User, and By Geography |

|

By Vehicle Technology

|

|

|

By Orbit Type

|

|

|

By Component · Propulsion System · Guidance and Control System · Structure · Avionics · Payload · Others |

|

|

By Payload Capacity · Less Than 1000 Kg · 1000 Kg to 2500 Kg · More Than 2500 Kg |

|

|

By End User · Commercial · Military · Civil & Government |

|

|

By Geography |

· North America (By Vehicle Technology, By Orbit Type, By Component, By Payload Capacity, By End User, and By Country) o U.S. (By Orbit Type) o Canada (By Orbit Type) · Europe (By Vehicle Technology, By Orbit Type, By Component, By Payload Capacity, By End User, and By Country) o U.K. (By Orbit Type) o Germany (By Orbit Type) o France (By Orbit Type) o Finland (By Orbit Type) o Russia (By Orbit Type) o Rest of Europe (By Orbit Type) · Asia Pacific (By Vehicle Technology, By Orbit Type, By Component, By Payload Capacity, By End User, and By Country) o China (By Orbit Type) o India (By Orbit Type) o Japan (By Orbit Type) o South Korea (By Orbit Type) o Rest of Asia Pacific (By Orbit Type) · Middle East & Africa (By Vehicle Technology, By Orbit Type, By Component, By Payload Capacity, By End User, and By Country) o Egypt (By Orbit Type) o UAE (By Orbit Type) o Israel (By Orbit Type) o Rest of Middle East & Africa (By Orbit Type) · Latin America (By Vehicle Technology, By Orbit Type, By Component, By Payload Capacity, By End User, and By Country) o Brazil (By Orbit Type) o Argentina (By Orbit Type) o Rest of Latin America (By Orbit Type) |

Frequently Asked Questions

As per a study by Fortune Business Insights, the market size was USD 433.89 billion in 2025.

The market is likely to grow at a CAGR of 4.56% during the forecast period.

The LEO segment is leading the market due to the increasing number of satellite due to cost efficiency.

The market size in North America stood at USD 239.2 billion in 2025.

Technological advancements, increasing demand for satellite launches, and evolving market dynamics are poised for significant market growth.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us