Video Game Market Size, Trends, Share, & Industry Analysis, By Device (Smartphones, PC/Laptop, and Consoles), By Age Group (Generation X, Generation Y, and Generation Z), By Platform Type (Online and Offline), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

Video Game Market Size & Share Overview

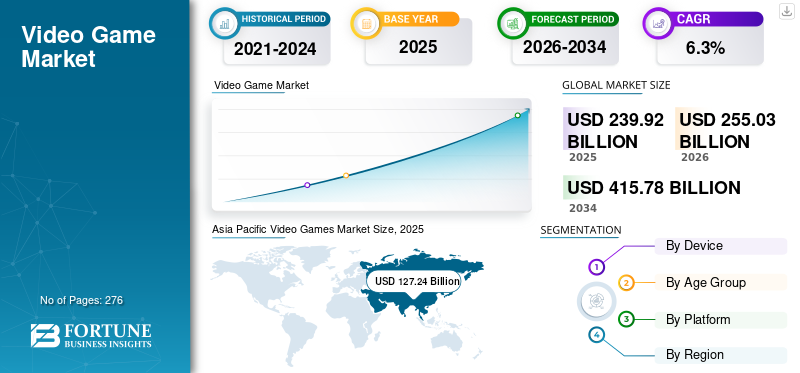

The global video game market size was estimated at USD 239.92 billion in 2025 and is projected to reach USD 255.03 billion in 2026 to USD 415.78 billion by 2034, growing at a CAGR of 6.30% from 2026 to 2034. Moreover, the video game market in the U.S. is expected to grow significantly, reaching USD 67.61 billion by 2032. The rise of digital gaming, cloud-based platforms, and immersive technologies like AR and VR are driving industry growth. Asia Pacific dominated the video game market with a market share of 53.03% in 2025.

Based on the analysis, the global video game industry grew by 24.21% in 2020 compared to 2019. The global COVID-19 pandemic has been unprecedented and staggering, with video games experiencing higher-than-anticipated demand across all regions compared to pre-pandemic levels.

A video game is a form of interactive digital entertainment that an individual can play on devices such as smartphones, PC/laptops, and consoles. They contain unique graphics, Computer-Generated (CG) sound, video effects, and storytelling to make them more realistic and increase individual enjoyment. Rapid technological developments in this domain, such as three-dimensional environments, graphics, and others, to increase the interactivity level of games have further driven market growth.

Platforms for playing video games are online and offline. Thus, video games can be played online through the internet and offline without an active internet connection. Online games have seen rising demand due to the rise in cloud-based games technology, where the resource packs and other required files are stored on the cloud and accessed through the internet by individuals during play. Offline games are available on all devices but are usually developed for PC/laptops and consoles. Users can download and install resource packs and other required data through portable devices such as CDs, pen drives, and others, which usually do not require the Internet.

In recent years, technological advancements in cloud-gaming services such as Google Stadia and Steam Link have made it possible to play games from anywhere around the world. In addition, increased rapid internet penetration has raised the accessibility of high-speed internet. This, in turn, has widened the consumer base by including casual gamers who do not intend to buy high-end hardware required by games. Most online games involve multiple players, whereas most offline games comprise single-player. Multiplayer is where people interact with other players and compete with each other. The growing penetration of the internet and smartphones facilitates market proliferation.

Surging demand for video games from Generation Z is also contributing to market augmentation. For instance, in February 2022, RedMagic, the smartphone brand known for its smartphones with cooling fans, unveiled “7”, which is the global variant of its 2022 flagship gaming smartphone. The flagship model consists of a 165Hz refresh, AMOLED display, cooling system, and Snapdragon 8 Gen 1 SoC.

The rising consumer preference for multiplayer games led to the growth of esports competitions globally. Esports competitions are similar to sports tournaments such as FIFA, NBA, and others, where professional players participate through teams representing a country or region. First-person shooter games, fighting games, card games, real-time strategy games, and multiplayer online battle arena games are some of the genres in these tournaments. Esports players also generate revenue through sponsorships, advertisements, and streaming. For instance, in September 2022, MOGO Esports, which is an India-based esports company, announced its partnership with Somaiya Vidyavihar University (SVU) to launch its first esports arena in India. The company has invested around USD 98.72 million to build this new arena. The company plans to assist students by creating a platform where they can choose esports as a career.

Download Free sample to learn more about this report.

VIDEO GAME MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 239.92 billion

- 2026 Market Size: USD 255.03 billion

- 2034 Forecast Market Size: USD 415.78 billion

- CAGR: 6.30% from 2026–2034

- Asia Pacific dominated the market with a 53.03% share in 2025.

- The Smartphones segment held the largest market share in 2025.

- The Online segment accounted for the largest market share in 2025.

North America

North America remained a key market, supported by advanced gaming consoles and high internet usage.

Europe

Europe witnessed steady growth with the rising adoption of online and cloud-based gaming.

Asia Pacific

Asia Pacific led the market due to strong smartphone and internet penetration across China and India.

U.S.

The market is projected to reach USD 67.61 billion by 2032, driven by digital gaming and advanced gaming technologies.

Japan

Strong gaming culture and the presence of leading game developers continue to support market growth.

Read More

VIDEO GAME MARKET TRENDS

- Asia Pacific witnessed video game market growth from USD 127.24 Billion in 2025 to USD 135.25 Billion in 2026.

Growing Trend of Competitive Multiplayer Games has been Fueling Market Growth

The market has observed an exponential rise in the inclination of individuals toward competitive multiplayer mobile games. Esports has become a global phenomenon, and games such as Player Unknown's Battlegrounds (PUBG) and Call of Duty (COD) are highly popular. These games follow a multiplayer game format, providing gamers with the ability to interact with their counterparts, thus contributing to higher engagement. Furthermore, the multiplayer form provides a sense of achievement to players as they compete with other participants in real time. In-game purchases and character customization features help increase user engagement even further.

The launch of Battle Royale games for smartphones has significantly contributed to market augmentation. A rapid rise in the penetration of smartphones is a key contributing factor to the rising number of gamers. Most smartphones available in the market have processors that support games with higher graphics and visual effects. In addition, the rising penetration of high-speed internet globally is a key contributor to the growing trend of online multiplayer games. For instance, in October 2022, Activision Blizzard Inc. launched its all-time celebrated game Overwatch's new version, Overwatch 2, with free-to-play and monetization options to cater to the growing demand for multiplayer games.

VIDEO GAME MARKET GROWTH FACTORS

The rise in Technological Advancements is Driving the Video Game Market Growth

The growing integration of 3D, high-definition graphics, sound effects, Virtual Reality (VR), and Augmented Reality (AR) in games has made them more graphically sound and high-functioning. They are more appealing and thus can grab the attention of a large consumer base. Video games have become more realistic in terms of representation. High-quality visual effects, detailing, and sound effects make them look more natural.

The developers are focused on developing games with more realistic graphics owing to the advancement in technology from 8-bit resolution to 64-bit resolution. The technological advances have been continuous and rapid in game development and have brought a shift toward personalization and user-centricity. This development in resolution technology brings more user traction and likeability, resulting in rapid advancement in the market. The decent graphics of video games are experienced through high-definition displays such as HD, FHD, UHD, and 4K. The high-definition displays, which offer 720p and 1080p, have significantly fueled demand for more realistic games. For instance, in October 2022, Apple announced its plan to launch its new 27-inch pro-motion external display early next year. This external display is 5K with Apple's ProMotion tech, which adjusts the refresh rate depending on the context and can rise as high as 120Hz.

In addition, technological advancements in Graphic Processor Units (GPU) have made performance smooth; thus, a combination of technologically advanced GPU and display offers a perfect ratio of performance and visuals. For instance, in November 2022, Advanced Micro Devices (AMD), an American multinational semiconductor company, announced the launch of its new next-generation graphic card, “RDNA 3”. The launch is to stay ahead of the competition as Nvidia, which is its immediate competitor and a high-speed GPU manufacturer, started discussing its plan to launch RTX 4090 GPU.

RESTRAINING FACTORS

Increasing Health Issues and Concerns Regarding Addiction are Restraining Market Growth

Countries across the globe have been concerned with addiction related to gaming and the promotion of violence through different games to subsequent increases in depression and aggressive behavior in children. Thus, various governments have banned games that can disturb gamers mentally. In addition, a few countries have restricted the time spent by an individual on games. For instance, in August 2021, China imposed a gaming ban that does not allow users under 18 to play online games on weekdays and restricts play to three hours on weekends. This regulation restrains the market growth and user reach of market players.

Data breaches and cyber security threats due to the rapid advancement of cloud gaming technology have caused governments to ban selective games or developer companies, negatively impacting consumer behavior and hindering market proliferation. For instance, in July 2022, the Indian government banned Battle Ground Mobile India (BGMI) due to data breach concerns and asked Play Store and Apple Store to take down the game.

Excessive violence is one of the reasons for banning video games in countries such as Brazil, Venezuela, South Korea, and others. Developers are needed to develop a customized version based on government censorship restrictions, resulting in increased development and maintenance costs. For instance, in August 2020, Call of Duty – Cold War new trailer was censored due to its content which the government did not approve. Thus, the company had to release a short version later.

Download Free sample to learn more about this report.

VIDEO GAME MARKET SEGMENTATION ANALYSIS

By Device Analysis

- The PC/Laptop segment is expected to hold a 20.3% share in 2021.

To know how our report can help streamline your business, Speak to Analyst

Rising Penetration of Smartphones will Further Aid Market Growth

By device, the market is divided into smartphones, PC/laptop, and consoles. The PC/laptop segment has been observing significant growth owing to the rise in PC gaming and gaming console trends among Generation Y, although smartphones have the highest market share. The global adoption of smartphones, coupled with increasingly powerful 5G networks and cloud-based infrastructure, has propelled the number of gamers in mobile gaming. Furthermore, mobile devices are now part of most aspects of an individual's daily routine, and the availability of high-speed internet has further made smartphones a significant source of entertainment. In addition, the technological advancement in smartphones has wholly changed gaming habits. The mobile gaming sector has observed an exponential rise, leading to new market opportunities.

For instance, in October 2022, Indian Prime Minister Narendra Modi announced the launch of 5G services in India in the 6th edition of the India Mobile Congress (IMC) 2022. In October 2022, Reliance Jio announced its 5G service would be available in four cities, and Bharti Airtel announced its 5G service would first be available in eight cities.

Developers have been launching new games, free samples, and mobile versions of their best sellers to attract the growing consumer base. Smartphones provide the comfort of playing from anywhere and at any time. In addition, the higher accessibility will further surge the demand for online games. Furthermore, the higher affordability of smartphones significantly contributes to market growth.

For instance, in May 2022, Apex Legends, a free-to-play Battle Royale-hero shooter game developed by Respawn Entertainment, launched its mobile version on Android and iOS to expand its reach and cater to the extensive consumer base.

Smartphones have seen rapid technological advancement and have transformed over the last ten years, which will bring more lucrative opportunities. In addition, augmented reality and virtual reality have been developing faster and are readily available, contributing to market growth.

For instance, in August 2022, Xiaomi's Redmi announced it would soon launch the most speculated gaming smartphone, which will feature the latest MediaTek's new Dimensity 1200 processor.

By Age Group Analysis

Higher Inclination of Generation Z toward Online Games will Boost the Market Growth

By age group, the market is further divided into Generation X, generation Y, and Generation Z. Generation Y and Generation Z have the highest population share. However, generation Z has the dominant share of the market. Generation Z grew up in a highly sophisticated technological environment with advancements in smartphones and laptops during this period. Thus, they are more tech-savvy than their predecessors. Even though Generation Y is more digitally sound as they saw the innovations and advancements, including the launch of the World Wide Web, they are more inclined toward consoles and other gaming moods as major consoles occurred between 1970 to 2010.

In contrast, generation Z has been more inclined toward smartphones as a gaming device, which is the dominant segment in the market. For instance, in March 2022, Game Jolt, the social media platform designed for Generation Z gamers and creators, launched its first mobile application for Android and iOS. Thus, generation Z is a significant contributor due to their curiosity about technological innovations and upgrades.

By Platform Type Analysis

Rapid Penetration of the Internet has been Driving the Market Growth

By platform type, the market is divided into online and offline. The online segment has the highest video game industry share and has observed rapid advancement in recent years owing to several factors, such as technological advancements, rapid internet penetration, and development in the smartphone industry with the launch of new gaming smartphones. The online segment consists of various genres such as First-Person Shooter (FPS) games, Real-Time Strategy (RTS) games, Massively Multiplayer Online (MMO) games, Multiplayer Online Battle Arena (MOBA) games, Battle Royale games, and others. For instance, in June 2022, Tencent announced the launch of its XR division to develop its Benchmark VR product further.

The rapid internet penetration has made the internet accessible to the majority of the population. The penetration was due to digitization occurring in developing countries, which has driven the growth of online games. For instance, in September 2022, Satellite internet provider Hughes Communications India announced its launch of India's first high-throughput satellite (HTS) broadband service powered by the Indian Space Research Organisation (ISRO). Thus, the rapid development in internet technology has further made manufacturers develop more multiplayer games to cater to the growing demand.

REGIONAL INSIGHTS of VIDEO GAME INDUSTRY

The region is further segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Video Games Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region is a significant contributor to market growth and consists of countries such as China, India, Japan, Australia, and others. Most market players have their headquarters in China, and the growing penetration of the internet and smartphones in countries such as China and India has been a significant factor in the market growth. As there has been a significant rise in internet and smartphone users, developers have focused on multiplayer games such as COD, PUBG, and others to cater to the growing consumer base. For instance, in May 2022, the developer Mayhem Studios and SuperGaming announced the plan to launch two new made-in-India battle royal online multiplayer games, Underworld Gang Wars and Indus Battle Royale.

- In Asia Pacific, the PC/Laptop segment is estimated to hold a 54.55% market share in 2021.

To know how our report can help streamline your business, Speak to Analyst

North America

Furthermore, the availability of social media platforms, such as Twitch and YouTube, has allowed gamers to socialize beyond games, further contributing to the expansion of market reach. The growing technological advancements in consoles and other devices have made North America a significant contributor to the market. The gaming community has seen an exponential rise in North America due to the latest advancements in the technology of devices and the easy availability of the internet. For instance, in November 2020, Sony launched its new console Play Station 5, in the U.S. The console was upgraded from its successor in terms of design and technology.

KEY INDUSTRY PLAYERS

Players in the global market focus on innovations and product developments tailored to customer requirements and advanced technological adaptation. Manufacturers and developers are launching new games and events to cater to the growing demand. Furthermore, new technological innovations such as augmented and virtual reality have increased competition. The manufacturers focused on developing gaming smartphones, gaming PCs/laptops, and consoles with high-definition technology and high-end GPU, which shall further contribute to the growth in gaming revenue of the gaming companies. For instance, in July 2022, ASUS, a multinational computer hardware and consumer electronics company, introduced multiple gaming laptops in India equipped with AMD’s quick and effective Ryzen 6000H processors. ROG Zephyrus G15 comes with the AMD Ryzen 9 6900HS processor with 8 cores with 16 threads. In addition, ROG Zephyrus is compatible with graphics cards such as NVIDIA GeForce RTX 3080.

List of Top Video Game Companies:

- Sony Group Corporation (Japan)

- Microsoft (U.S.)

- Nintendo (Japan)

- Tencent (China)

- Activision Blizzard (U.S.)

- Electronic arts (U.S.)

- Epic Games (U.S.)

- Take-two interactive (U.S.)

- Ubisoft (France)

- Bandai Namco Holdings Inc. (Japan)

KEY INDUSTRY DEVELOPMENTS:

- In July 2022, Asus expanded its gaming smartphone ROG line by launching its new ROG Phone 6 and ROG Phone 6 Pro. The phone comes with the latest Snapdragon 8+ Gen 1 system-on-chip, IPX4 rating, AMOLED screen of 165Hz refresh rate, up to 18GB RAM, and 512GB onboard storage.

- In March 2022, OnePlus launched its new flagship phone, the OnePlus 10 Pro, with advanced features such as 150W SuperVOOC fast charging, HyperBoost Gaming Engine, and others for targeting gamers.

- In October 2022, Samsung launched a new 55-inch curved gaming monitor Odyssey Ark. The new game has advanced features such as a 165 Hz refresh rate, 4K resolution, 1 ms of response time, AMD FreeSync Premium Pro, Cockpit Mode, and Ark Dial.

- In August 2022, Philips expanded its gaming monitor range with the launch of its new flagship gaming monitors, 27M1N3200ZA and 24M1N3200ZA, in India.

- In December 2022, Nintendo announced the launch date of its well-known franchise Fire Emblem. The new Fire Emblem Engage will be launched in January 2023 with upgrades and developments in characters and new features which shall make the game more engaging.

REPORT COVERAGE

The research report analyzes the video games market in depth and highlights crucial aspects such as prominent companies, the competitive landscape, product types, categories, and distribution channels. It also provides insights into video game industry trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market's growth.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

By Device |

|

|

By Age Group |

|

|

By Platform Type |

|

|

North America (By Device, Age Group, Platform, and Country)

Europe (By Device, Age Group, Platform, and Country)

Asia Pacific (By Device, Age Group, Platform, and Country)

South America (By Device, Age Group, Platform, and Country

Middle East and Africa (By Device, Age Group, Platform, and Country)

|

Frequently Asked Questions

According to Fortune Business Insights, the global video game market was valued at USD 239.92 billion in 2025 and is projected to reach USD 415.78 billion by 2034, growing at a CAGR of 6.3% during the forecast period.

Growth is driven by advances in cloud gaming, mobile penetration, VR AR technology, and rising demand from Gen Z gamers. Subscription models and live-service games also contribute significantly to recurring revenues.

Asia-Pacific holds the largest market share, accounting for over 53.03% of global revenue, led by countries like China, Japan, and India, due to high smartphone penetration and a massive online gaming user base.

The most popular platforms are smartphones, followed by PCs/laptops and gaming consoles like the PlayStation 5 and Xbox Series X. Mobile gaming leads due to accessibility and lower cost of entry.

Top companies include Sony, Microsoft, Nintendo, Tencent, Activision Blizzard, Electronic Arts, Epic Games, and Ubisoft, all driving innovation in hardware, game development, and online ecosystems.

Mobile gaming is the fastest-growing segment, driven by widespread smartphone use and 5G networks. Titles like PUBG Mobile and Genshin Impact have attracted millions of daily active users worldwide.

Key challenges include regulatory restrictions, data privacy issues, cybersecurity threats, and growing concerns about gaming addiction, especially among younger demographics.

- 2021-2034

- 2025

- 2021-2024

- 276

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us