Medical Copper Tubing Market Size, Share & Industry Analysis, By Product Type (Type K and Type L), By Form (Straight and Coiled), By End User (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Medical Copper Tubing Market Size and Future Outlook

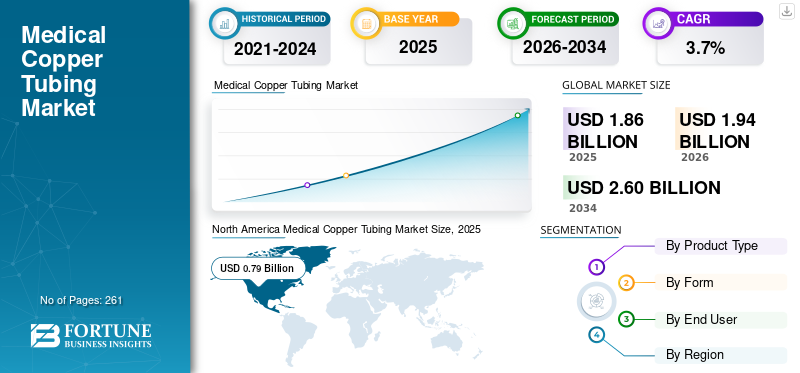

The global medical copper tubing market size was valued at USD 1.86 billion in 2025 and is projected to grow from USD 1.94 billion in 2026 to USD 2.60 billion by 2034, exhibiting a CAGR of 3.7% during the forecast period. North America dominated the medical copper tubing market with a market share of 42.47% in 2025.

Medical copper tubing refers to the non-permeable, durable, and easy-to-sterilize devices used to distribute medical gases, including nitrogen and others, in healthcare settings. Copper tubing is widely used in healthcare facilities due to its durability, corrosion resistance, and antibacterial properties. The rising demand for medical oxygen for acute and chronic diseases, the increasing volume of surgical procedures, the growing geriatric population, and the expansion of healthcare infrastructure are boosting the adoption of the medical copper tubing systems.

For instance, according to the 2020 statistics published by the National Center of Biotechnology Information (NCBI), around 310 million major surgeries are performed annually across the globe.

Top players in the market include Mueller Industries and The Lawton Tubes Co. They focus on the integration of technological innovations in this equipment, boosting market growth.

Download Free sample to learn more about this report.

Medical Copper Tubing Market Trends

Rapid Technological Innovations in Medical Copper Tubing are a Key Market Trend

There is a growing incorporation of advanced innovations into healthcare gas delivery infrastructure. While copper tubing remains a passive but critical component, the systems built around it are becoming more advanced through the adoption of pressure and flow monitoring, digital alarm panels, leak-detection mechanisms, supervisory communication links, and building-management integration.

Healthcare facilities are increasingly shifting toward connected and centrally monitored medical gas pipeline systems to enhance patient safety, reduce downtime, support preventive maintenance, and ensure regulatory compliance. This trend is especially relevant in ICU expansions, new hospital builds, surgical centers, and facility retrofits, due to high-performance copper tubing that supports reliable oxygen, vacuum, and compressed medical air distribution within digitally supervised equipment. Key companies are focusing on raising awareness of their medical copper tubes, which are expected to drive the growing demand for copper tubing for gas delivery.

- In September 2025, Mehta Tubes Limited (MTL) participated in Arab Health 2025 to promote its MEXFLOW Degreased Copper Tubes.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Rise in Surgeries and Launch of Innovative Equipment to Fuel Market Growth

The growing prevalence of chronic disorders, including respiratory diseases, cardiovascular diseases, and others, is resulting in the rising volume of surgical procedures, further boosting the adoption of oxygen supply equipment among patients, consequently driving the demand for medical copper tubing.

- For instance, according to 2021 data published by Science Direct, about 7.7% of people were suffering from cardiovascular disorders in the Americas.

Stringent infection control standards in hospitals and improvements in healthcare infrastructure are augmenting market expansion. Therefore, increased demand, coupled with the growing focus of major companies on R&D activities to introduce innovative equipment, is boosting the global medical copper tubing market growth.

Market Restraints

High Capital Cost Related to Innovative Equipment to Hinder Market Growth

The high installation costs associated with medical copper tubing are a major restraint in the global market. The demand for medical copper tubing is associated with the price of the tube itself and with the broader expense of system design, engineering, validation, brazing, alarm incorporation, commissioning, testing, maintenance services, and periodic updates, which increase the overall cost of the system.

Other investments, including periodic compliance verification, technical staffing, and limited funding initiatives, further make purchasing decisions challenging for low and middle-sized markets, including South Africa, Brazil, among others, further limiting product adoption.

- For instance, according to the 2024 data published by the United Nations Global Marketplace, the average price of medical gas pipeline equipment ranges from USD 40,000 for a limited installation/commissioning scope to more than USD 200,000 for large-scale pipeline construction projects.

Market Opportunities

Rapid Growth of Healthcare Infrastructure in Emerging Markets to Create Lucrative Growth Opportunities

There is an ongoing expansion of healthcare facilities in emerging countries, including Mexico, China, and others. The rising prevalence of chronic conditions, growing number of surgical procedures among patients, and rising number of hospitals, ambulatory surgical centers, and clinics are consequently boosting the adoption of medical copper tubing in clinical settings.

The increasing healthcare expenditure is further resulting in growing demand for these devices in ICU blocks, hospital wings, ambulatory facilities, surgical complexes, and specialty care centers to provide reliable gas supply, distribution regulation, and monitoring, thereby creating an opportunity for companies globally.

- According to 2025 data published by the International Trade Administration (ITA), the healthcare expenditure was USD 135.0 billion in Brazil.

Market Challenges

Limited Healthcare Access in Emerging Countries to Hamper Market Growth

There is a growing demand for surgical procedures for chronic disorders among the patient population. However, competition from alternative materials, supply chain disruptions, fluctuations in raw material availability, along with stringent regulatory compliance, a limited number of healthcare facilities, especially in emerging markets, are resulting in limited access to healthcare facilities among the patient population.

A limited number of experienced healthcare professionals, an inadequate reimbursement framework, among others, are some of the key factors, resulting in the delayed number of surgeries, further hampering the adoption rate of medical gas devices, especially in emerging countries, including South Africa and India, among others.

- For instance, according to 2023 data published by The World Bank Group (WBG), about 4.5 billion people lack full access to essential health services globally.

SEGMENTATION ANALYSIS

By Product Type

Type L Segment Led Market Due to Its Several Benefits

Based on product type, the market is classified into type K and type L.

The type L segment accounted for the largest medical copper tubing market share in 2025. The growing prevalence of chronic conditions, including respiratory disorders, and the benefits associated with type L tubes, including lightweight, higher calculated internal working pressures, are resulting in a growing demand for innovative medical copper tubes globally. This, along with the growing focus of key companies on introducing innovative equipment, is further expected to boost segment growth.

- For instance, according to 2024 data published by the Centers for Disease Control & Prevention (CDC), about 16 million adults have chronic obstructive pulmonary disease (COPD) in the U.S.

The type K segment is expected to grow at a CAGR of 4.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Form

Rising Need for Seamless Medical Air Distribution Fueled Straight Segment Expansion

Based on form, the market is bifurcated into straight and coiled.

The straight segment dominated the global market with a the largest market share in 2025, driven by rising numbers of surgeries, which in turn increased demand for medical gases. The installation of medical gas systems as permanent brazed pipeline networks favors rigid straight tubing for hospital-wide vacuum, oxygen, and medical air distribution.

- For instance, according to 2020 data published by the National Center for Biotechnology Information (NCBI), about 40-50 million major surgeries are performed each year in the U.S.

The coiled segment is predicted to flourish with a CAGR of 4.4% in the coming years.

By End User

Rising Patient Admissions in Hospitals & ASCs Bolstered Segment Growth

By end user, the market is divided into hospitals & ASCs, specialty clinics, and others.

The hospitals & ASCs segment dominated the market in 2025, attributed to the growing prevalence of chronic conditions, rising patient admissions in hospitals, increasing number of hospitals, and rapid adoption of advanced copper tubes. Furthermore, the segment is set to hold a 76.4% share in 2026.

- For instance, according to 2025 statistics published by The Trustees of Princeton University (TPU), there are approximately 8,000 hospitals in Japan.

Specialty clinics are projected to grow at a 4.0% CAGR over the projected period.

Medical Copper Tubing Market Regional Outlook

In terms of region, the market is segmented into North America, Latin America, the Middle East & Africa, Europe, and Asia Pacific.

North America

North America Medical Copper Tubing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, at USD 0.76 billion, and maintained the lead in 2025, at USD 0.79 billion. The increasing prevalence of chronic disorders, including respiratory and urological conditions, an adequate reimbursement framework, and the growing adoption of advanced medical gas pipeline systems are fueling market growth in the region.

- For instance, according to 2026 statistics published by the Asthma and Allergy Foundation of America (AAFA), about 28 million people in the U.S. have asthma.

U.S. Medical Copper Tubing Market

On the basis of North America’s solid role and the U.S. supremacy within the region, the U.S. market is estimated to reach USD 0.71 billion in 2026, accounting for roughly 36.7% of global sales.

Europe

Europe is projected to record a CAGR of 3.2% in the coming years, the second-highest among all regions, and to reach a valuation of USD 0.54 billion in 2026. The growing adoption of advanced devices and rising healthcare expenditure are likely to support the market growth.

U.K. Medical Copper Tubing Market

The U.K. market in 2026 is estimated at around USD 0.09 billion, representing roughly 4.6% of global revenues.

Germany Medical Copper Tubing Market

The German market is projected to reach around USD 0.12 billion in 2026, equivalent to around 6.1% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.41 billion in 2026 and secure the position of the third-largest region in the market. The growing number of surgeries, rising healthcare expenditure, among others, is expected to drive the market growth. In the region, India and China are both estimated to reach USD 0.06 billion and USD 0.13 billion, respectively, in 2026.

Japan Medical Copper Tubing Market

The Japan market in 2026 is estimated at around USD 0.08 billion, accounting for roughly 4.2% of global revenues. Japan has historically reported a relatively growing prevalence of chronic conditions, with a strong adoption of medical copper tubes.

China Medical Copper Tubing Market

China is projected to be one of the major markets globally, with 2026 revenues estimated at around USD 0.13 billion, representing roughly 6.7% of global sales.

India Medical Copper Tubing Market

The India market size in 2026 is estimated at around USD 0.06 billion, accounting for roughly 3.2% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.10 billion in 2026. The growth is driven by the growing adoption of medical copper tubes in the region. The Middle East & Africa region is also anticipated to grow as more key companies introduce novel devices. In the Middle East & Africa, the GCC is set to reach a valuation of USD 0.03 billion in 2026.

South Africa Medical Copper Tubing Market

The South Africa market is projected to reach around USD 0.01 billion in 2026, representing roughly 0.6% of global revenues.

Competitive Landscape

Key Industry Players

Establishment of New Gas Facility to Support Their Dominance

Top players’ dominance is attributed to an extensive range of product offerings and growing emphasis on inorganic growth tactics globally. Leading companies in the market include Mueller Industries and The Lawton Tubes Co. They focus on acquisitions and mergers to reinforce their market presence.

- For instance, in March 2026, Mueller Industries acquired Bison Metals Technologies LLC., a manufacturer of copper tubes, with an aim to strengthen its product channel.

Other key players such as Cambridge-Lee Industries LLC, are engaged in research and development activities to boost their market presence.

List of Key Medical Copper Tubing Companies Profiled

- Mueller Industries (U.S.)

- The Lawton Tubes Co. (Germany)

- Cambridge-Lee Industries LLC (U.S.)

- Amico Group of Companies (Canada)

- ElvalHalcor (Greece)

- Cupori (Finland)

- Precision UK (U.K.)

- MediStreams (India)

- Metal Alloys Corporation (India)

- Wieland (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Wieland announced its plan to establish a new USD 27.0 million plant dedicated to expanding semi-finished brass and copper production exclusively in the U.S.

- September 2025: Mexflow presented at HITEX Exhibition Center to showcase MEXFLOW Degreased Copper Tubes & Fittings for Medical Gas Pipeline Systems for efficiency, safety & reliability in healthcare facilities.

- May 2024: The Lawton Tubes Co. received approval from the Oman Ministry of Health (MOH) and International Hospitals Group (IHG) to supply copper pipes and fittings for the construction of three Middle Eastern hospitals as part of a joint U.K./Oman government-funded project.

- November 2023: Cupori announced the upgradation of their copper quality, which has the lowest carbon footprint. This helped the company to strengthen its presence.

- March 2023: Wieland launched a new copper tube at the ISH trade fair in Frankfurt that advances both building technology and construction in the area of sustainability: cuprolife.

- February 2021: The Lawton Tubes Co. published a COVID-era case study showing that its medical gas copper pipe was supplied to the government, the NHS, and healthcare providers in the U.K. The company said it supplied 120 miles of medical gas copper pipes, made more than 200 deliveries, and served over 70 sites, including Nightingale-related capacity projects. This helped the company in strengthening its presence.

REPORT COVERAGE

The report provides a detailed global medical copper tubing market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, form, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Form, End User, and Region |

| By Product Type |

|

| By Form |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.86 billion in 2025 and is projected to reach USD 2.60 billion by 2034.

In 2025, North America regional market value stood at USD 0.79 billion.

Growing at a CAGR of 3.7%, the market will exhibit steady growth over the forecast period.

By product type, the type L segment led the market.

Rise in surgeries and launch of innovative equipment to fuel market growth.

Mueller Industries and The Lawton Tubes Co. are the major players in the global market.

North America dominated the market share in 2025.

The rapid growth of healthcare infrastructure in emerging markets is expected to boost the adoption of these devices globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us