Medical Device Connectivity Market Size, Share & Industry Analysis, By Offering (Products {Device Connectivity Hubs, Medical IoT Gateways, Medical Device Integration Platforms, EMR Interoperability Modules, and Others}, and Services {Implementation & Integration Services, Consulting & Workflow Optimization, and Others}), By Technology (Wired and Wireless), By Application (Vital Signs & Patient Monitoring Integration, Anesthesia & OR Device Integration, ICU / NICU Connectivity, Imaging Device Data Integration, Home Health & Others), By End User, and Regional Forecast, 2026-2034

Medical Device Connectivity Market Size and Future Outlook

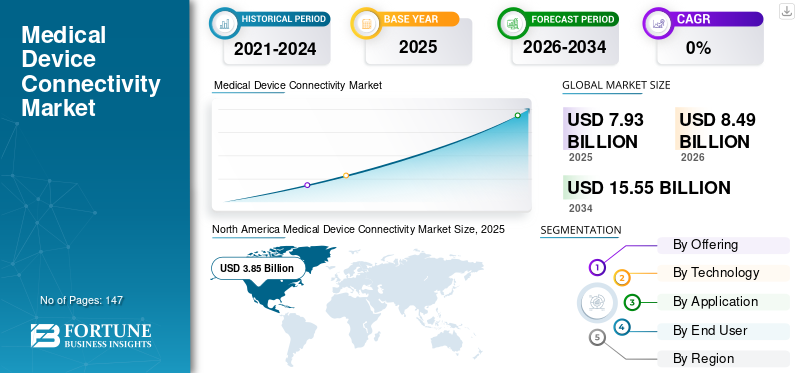

The global medical device connectivity market size was valued at USD 7.93 billion in 2025. The market is projected to grow from USD 8.49 billion in 2026 to USD 15.55 billion by 2034, exhibiting a CAGR of 7.87% during the forecast period.

The medical device connectivity allows secure transfer of clinical device data into hospital systems, IoT platforms, EHRs, and cloud analytics. The market growth is driven by digital transformation in healthcare, telehealth expansion across the globe, interoperability standards adoption, and demand for real-time clinical insights. In addition, various key players are focusing on collaboration and partnerships to advance their market positions.

Furthermore, the market is dominated by several key players, with Koninklijke Philips N.V., Masimo, Ascom, General Electric Company, and others occupying the dominating positions. They focus on advanced technology integration and strengthening product offerings through collaborations to maintain their dominance.

Download Free sample to learn more about this report.

Medical Device Connectivity Market Key Takeaways

- 2025 Market Size: USD 7.93 Billion

- 2026 Market Size: USD 8.49 Billion

- 2034 Forecast Market Size: USD 15.55 Billion

- CAGR: 7.87% from 2026–2034

- North America dominated the medical device connectivity market with a value of USD 3.85 billion in 2025.

- The products segment held the largest market share in 2025.

- The wired technology segment is expected to account for a 58.6% share in 2026.

North America

North America led the market with a valuation of USD 3.85 billion in 2025, driven by strong hospital digitalization and telehealth adoption.

Europe

Europe is projected to reach USD 1.67 billion in 2026, supported by a favorable regulatory environment and strong industry presence.

Asia Pacific

Asia Pacific is expected to attain a market value of USD 2.06 billion in 2026, supported by growing healthcare IT investments across emerging economies.

U.S.

The market is projected to reach USD 3.76 billion in 2026, supported by advanced healthcare infrastructure and increasing device integration initiatives.

Japan

The market is expected to benefit from rising healthcare digitalization and increasing adoption of connected medical technologies.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Digital Transformation Across Healthcare Systems to Boost Market Growth

A key driver of the market is the rapid digital transformation of healthcare systems. With the increasing number of hospitals advancing their infrastructure to enhance clinical efficiency and patient safety, the adoption of bedside devices with EHRs and clinical decision platforms is rapidly increasing. This has resulted in high demand for reliable connectivity as a basic requirement. Digital transformation initiatives also seek to improve interoperability, data mobility, and analytics, all of which rely on medical device connectivity. In addition, governments and health systems are also making significant investments in digital-health modernization, which is driving widespread adoption of connected devices, integration platforms, and wireless IoMT solutions.

For instance, in July 2023, GE HealthCare and Medanta signed a collaboration for the launch of Tele-ICU services in India.

MARKET RESTRAINTS:

Cybersecurity Vulnerabilities in Connected Medical Devices to Restrict Market Growth

One of the most significant factors restraining the global medical device connectivity market growth is cybersecurity vulnerabilities in connected medical devices. As more devices become networked, there is a high risk of cyberattacks. This results in increasing the risk of unauthorized access, data tampering, ransomware, or operational shutdowns. These risks force healthcare providers to invest heavily in cybersecurity tools, network segmentation, patching, and device certification. As a result, cybersecurity challenges directly hinder market growth by raising barriers to implementation and decreasing provider confidence.

- For instance, in August 2024, the U.S. Cybersecurity and Infrastructure Security Agency (CISA) issued a security advisory warning of multiple vulnerabilities in Capsule Technologies’ Capsule Medical Device Information Platform (MDIP).

MARKET OPPORTUNITIES:

Advances in Wireless and IoT Technology to Offer Lucrative Growth Prospects

Rapid advances in wireless communication standards and IoT-enabled medical devices are creating significant opportunities in the market. Wireless connectivity removes the physical limitations of cabling and enables the real-time transmission of clinical data. This allows health systems to expand monitoring beyond hospital settings. IoT-enabled sensors and connected vitals devices provide continuous surveillance, early-warning alerts, and automated documentation that can help improve efficiency and outcomes. This helps in reduced deployment times, cloud-based integration, and reduced long-term infrastructure costs, making wireless medical devices and IoT solutions a high-growth opportunity for connectivity vendors.

- For instance, GE Healthcare is one of the leading players that offers a wireless, wearable monitoring system.

MEDICAL DEVICE CONNECTIVITY MARKET TRENDS:

Growth of Remote Patient Monitoring (RPM) and Telehealth is a Significant Market Trend

In recent years, the market has witnessed a rapid expansion of RPM and telehealth. This is revolutionizing the landscape of medical device connectivity as healthcare delivery is shifting beyond traditional hospital settings into homes, outpatient centers, and virtual-care settings. This trend has boosted the demand for robust connectivity platforms that are capable of securely transmitting real-time physiological data into hospital EHRs and clinical dashboards. Additionally, strategic initiatives by operating players also supported this market trend.

- For instance, in March 2023, Koninklijke Philips N.V. launched Philips Virtual Care Management solutions to enhance telehealth offerings.

MARKET CHALLENGES:

High Capital and Operational Costs Pose a Significant Challenge for Market Growth

One of the major challenges in the global market is the high capital and operational costs. The integration of medical devices into a hospital IT system is often a costly affair. It requires substantial upfront capital investment as well as ongoing operational expenditures for maintenance, compatibility updates, training, and compliance. This creates a significant financial barrier, especially for smaller or resource-constrained institutions. The combination of high initial cost, unpredictable ongoing expenses, and uncertain return on investment results in slower adoption of these technologies in the market.

- For example, according to an article published by SaijiTech in June 2024, the integration processes are complex and resource-intensive, noting that legacy devices, proprietary protocols, and data-security requirements significantly increase costs and implementation efforts.

Download Free sample to learn more about this report.

Segmentation Analysis

By Offering

Frequent Purchases of Products to Drive the Segmental Growth

Based on the offering, the market is classified into products and services. Products are further segmented into device connectivity hubs, Medical IoT gateways, medical device integration platforms, EMR interoperability modules, and others. In addition, the services segment is classified into implementation & integration services, consulting & workflow optimization, and others.

The products segment held the largest global medical device connectivity market share in 2025. This can be attributed to the increasing need for high-reliability connectivity hardware, coupled with expansion in remote patient monitoring, resulting in increasing demand for the products. Additionally, new product launches by key players further supported the segment growth.

- For instance, in October 2025, BD launched the BD Incada Connected Care Platform to drive connectivity across healthcare settings.

The services segment is the fastest-growing with a 10.07% CAGR during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Increasing Usage of Wired Applications to Lead Segment Growth

In terms of technology, the market is categorized into wired and wireless.

In 2025, the wired segment dominated the market with the largest share. In 2026, the segment is anticipated to dominate with a 58.6% share. The segment dominated the market owing to the high reliance of hospitals on wired connectivity for devices such as patient monitors, ventilators, and anesthesia machines. As this technology offers stable and uninterrupted communication, its adoption among end users is relatively higher.

- For instance, according to the white paper published by Lantronix, Inc., many ICUs and operating rooms still use wired connectivity to network critical devices such as patient monitors, ventilators, infusion pumps, and lab/diagnostic instruments.

The wireless technologies segment is expected to grow at a CAGR of 9.70% in the coming years.

By Application

Large Volume of Data Generation to Drive Vital Signs & Patient Monitoring Integration Segment Growth

In terms of application, the market is categorized into vital signs & patient monitoring integration, anesthesia & or device integration, ICU / NICU connectivity, imaging device data integration, home health & remote patient monitoring (RPM), and others.

The vital signs & patient monitoring integration segment captured the leading share of the market in 2025. In 2026, the segment is anticipated to dominate with a 30.7% share. This dominance is supported by key factors such as advantages offered by these technologies for this application, scalability across hospital departments, and strong adoption for remote monitoring and hybrid care models.

- For instance, according to a study published in ScienceDirect in October 2024, wearable + IoT-based continuous vital sign monitoring highlights that integrating patient monitoring systems with IoT connectivity enables continuous surveillance in the ICU, along with general wards, and even in home-care settings.

The home health & remote patient monitoring (RPM) segment is expected to rise at a CAGR of 11.54% over the projected period.

By End User

Increasing Adoption of Advanced Technologies to Drive Hospitals & ASCs Segmental Growth

In terms of end user, the market is categorized into hospitals & ASCs, diagnostic centers, homecare, and others.

The hospitals & ASCs segment accounted for the largest share of the global market in 2025 and is expected to maintain its dominance in 2026 with an estimated 72.8% share. This dominance is primarily driven by the large device density and complexity in hospitals, the requirement of continuous monitoring and real-time data exchange, and strategic initiatives between operating players and hospitals for integration of these technologies.

- For instance, according to an article published in July 2023, more than 88% of hospital IT leaders plan to increase investments in third-party technology, with priorities including remote patient monitoring and advanced connectivity/interoperability solutions.

The homecare segment is expected to grow at a CAGR of 15.29% over the forecast period.

Medical Device Connectivity Market Regional Outlook

In terms of region, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America Medical Device Connectivity Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained strong momentum in 2024, valuing at USD 3.61 billion, and also held the largest share in 2025, with USD 3.85 billion. The regional dominance can be attributed to factors such as high penetration of digitalization in hospitals, high telehealth adoption, and significant investments in device integration. The U.S. market is set to reach a valuation of USD 3.76 billion in 2026. The U.S. is leading the North American market, owing to factors such as strong increasing focus of operating players on collaboration with hospitals for product penetration, and availability of advanced infrastructure for device integration. Additionally, strategic initiatives undertaken by end users also support the market growth over the study period.

· For instance, according to a study by RAND Corporation, the willingness of American individuals to use video telehealth increased by 11% between March 2019 and March 2021.

Europe

Europe region is projected to record a growth rate of 6.48%, which is the second highest among all regions, and reach a valuation of USD 1.67 billion by 2026. This can be attributed to the strong presence of key companies in device connectivity solutions, along with a supportive regulatory framework in the region. Backed by these factors, countries including U.K. anticipates to record the valuation of USD 0.34 billion, Germany to record USD 0.37 billion, and France to record USD 0.27 billion in 2026.

Asia Pacific

The market in Asia Pacific is expected to reach USD 2.06 billion in 2026 and secure the place of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.37 and USD 0.62 billion, respectively in 2026.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to register a slower growth in this market space. The Latin America market in 2026 is set to reach a valuation of USD 0.39 billion. Growing advancements in healthcare IT infrastructure in these regions are expected to drive growth in these regions further. In the Middle East & Africa, the GCC is set to reach a value of USD 0.10 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Technological Innovations and Strategic Initiatives Strengthen Leading Position of Key Companies

The global medical device connectivity market shows a moderately consolidated framework, with the presence of several key players, including digital-health innovators and device manufacturers. Medical device connectivity companies such as Koninklijke Philips N.V., Masimo, GE HealthCare, Ascom Holding AG, and Oracle Health are among the most dominating market entities. Advanced connectivity platforms, enterprise-wide clinical workflow solutions, and strong geographical presence are some of the factors supporting their market leadership. Additionally, increasing adoption of products offered by these players also supports their leading position.

- For instance, in October 2021, Koninklijke Philips N.V. announced that its Philips Capsule Medical Device Information Platform (MDIP) has been integrated with more than 1,000 unique medical device models.

Apart from this, other medical device connectivity companies such as BD, Baxter International, ICU Medical, Lantronix, and others are investing in offering connectivity hubs, smart infusion interoperability, and wireless gateways to maintain their competitive edge in the market.

LIST OF KEY MEDICAL DEVICE CONNECTIVITY COMPANIES PROFILED:

- Koninklijke Philips N.V. (Netherlands)

- Masimo (U.S.)

- Ascom (Switzerland)

- General Electric Company (U.S.)

- Oracle (U.S.)

- Siemens Healthineers AG (Germany

- BD (U.S.)

- Baxter (U.S.)

- ICU Medical, Inc. (U.S.)

- LANTRONIX, INC. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- September 2025: Koninklijke Philips N.V. and Masimo extended their collaboration for the integration of Masimo’s sensor technology directly into Philips’ multi-parameter patient monitor.

- July 2025: Koninklijke Philips N.V. partnered with Dräger, Hamilton Medical, Getinge, and B. Braun Melsungen AG to launch an open patient monitoring ecosystem” for vendor-neutral device connectivity.

- November 2024: GE Healthcare collaborated with RadNet to accelerate the adoption of artificial intelligence (AI) and transform imaging systems with SmartTechnology.

- January 2024: Nanyang Technological University, Singapore, and Imperial College London received a USD 20 million grant from the National Research Foundation, Singapore (NRF), for the development of advanced products to protect health data and wearable devices.

- December 2021: Planet Innovation introduced NeoSync – an innovative product that connects medical devices to Electronic Health Records (EHR).

REPORT COVERAGE

The global medical device connectivity market analysis provides n comprehensive study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It also provides overviews of technological advancements, product development, key industry developments, mergers & acquisitions, and strategic insights into market growth. The global market forecast report also encompasses a detailed competitive landscape with information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAIL |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.87% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Offering Products

Services

By Technology

By Application

By End User

By Region North America (By Offering, Technology, Application, End User, and Country)

Europe (By Offering, Technology, Application, End User, and Country/Sub-region)

Asia Pacific (By Offering, Technology, Application, End User, and Country/Sub-region)

Latin America (By Offering, Technology, Application, End User, and Country/Sub-region)

Middle East & Africa (By Offering, Technology, Application, End User, and Country/Sub-region)

|

- 2021-2034

- 2025

- 2021-2024

- 147

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us